Role and Responsibilities of a Client Advisor

Role and Responsibilities of a Client Advisor

Transform Your Financial Future

Contact UsFinancial planning can be confusing, especially when you're facing major decisions or moving through unfamiliar territory. A client advisor provides clarity by helping you organize your finances, set goals, and stay on track, even when market conditions or life changes occur.

Imagine trying to balance student loans while saving for a wedding, or managing an inheritance after a loved one passes away. These situations come with emotional and financial challenges. A client advisor steps in with objective guidance and a clear plan forward.

In this guide, you’ll discover what a client advisor does, their key responsibilities, common misconceptions about their role, how they’re compensated, and when you should consider consulting one.

Key Takeaways

- Client advisors offer personalized, long-term financial guidance, helping individuals and families manage everything from investments to retirement and estate planning.

- Their core responsibilities include evaluating financial health, creating tailored plans, monitoring performance, and maintaining open communication for continuous alignment with your goals.

- Contrary to common myths, client advisors are not just for the wealthy and their services go far beyond selling products or managing investments.

- Client advisors are compensated through various models—fee-only, hourly, commission-based, or hybrid—each with distinct pros and cons depending on your needs.

- Consulting a client advisor is especially valuable during life transitions, retirement planning, asset growth, or when you need expert, objective financial insight.

Understanding the Role of Client Advisors

A client advisor is a financial professional who provides personalized advice tailored to your specific needs and aspirations. Unlike stockbrokers who focus on trades or accountants who handle tax filings, client advisors take a broader approach. They often work with high-net-worth individuals, families, or businesses, offering strategies that encompass investments, retirement planning, and wealth preservation.

Their primary goal is to understand your financial objectives, whether that’s building a nest egg, funding a significant purchase, or ensuring a comfortable retirement, and to develop a roadmap to help you achieve them.

What sets client advisors apart is their commitment to long-term relationships. They don’t just offer a one-time solution; they stay by your side, adapting plans as your life evolves. This ongoing partnership provides you stability and reassurance, particularly during uncertain economic times. With a solid grasp of what a client advisor does, let’s explore their core responsibilities in greater detail.

Also Read: How To Master Corporate Financial Planning?

Main Responsibilities of a Client Advisor

A client advisor’s role is multifaceted, requiring a blend of analytical skills, market knowledge, and interpersonal finesse. Their responsibilities are designed to keep your financial plan aligned with your goals. Here’s what you can expect:

- Evaluating Your Financial Health: The process begins with a thorough examination of your finances. A client advisor reviews your income, expenses, assets, debts, and existing investments to get a clear picture. This assessment helps them pinpoint opportunities and risks, laying the foundation for a strategy that suits them.

- Crafting Customized Plans: Once they understand your situation, they design a financial plan personalized to your goals and risk tolerance. This might include investment options, savings strategies, or tax-efficient approaches.

- Tracking and Refining Strategies: Financial plans aren’t static. A client advisor monitors your investments and overall progress, making adjustments to account for market shifts or changes in your life. This proactive oversight keeps your plan effective and responsive to new circumstances.

- Maintaining Open Communication: Regular updates are an integral part of their service. They’ll keep you informed about performance, market conditions, and any recommended changes. This consistent dialogue ensures you’re never in the dark about your financial standing.

- Educating You on Options: Beyond managing your money, client advisors teach you about financial concepts. They might explain how compound interest works or why diversification matters, empowering you to make informed choices with confidence.

These duties show the comprehensive support a client advisor offers. However, myths about their role can sometimes obscure their actual value. Let’s address those misconceptions next.

Misconceptions About Client Advisors

You might have heard ideas about client advisors that don’t fully align with reality. Clearing up these misunderstandings can help you make a more informed decision about working with one.

- "They’re Only for the Ultra-Rich": Many assume client advisors cater exclusively to millionaires. While they do serve wealthy clients, many advisors work with individuals at various income levels. They can help you build wealth over time, even if you’re starting with modest means.

- "It’s All About Investments": Investments are essential, but they’re just one piece of the puzzle. Client advisors also tackle budgeting, debt reduction, insurance needs, and long-term planning. Their holistic approach ensures all parts of your financial life are addressed.

- "They Push Unnecessary Products": Some worry that advisors are motivated by sales quotas. In truth, many operate on fee-only models, meaning their advice isn’t tied to commissions. This structure prioritizes your interests over product sales.

- "DIY Tools Are Enough": Online platforms offer convenience, but they lack the nuance a client advisor brings. Advisors provide personalized insights, emotional support during market dips, and expertise that generic tools can’t replicate.

By debunking these myths, you can gain a deeper appreciation for the role client advisors play. With that clarity in mind, let’s examine how they’re compensated for their efforts.

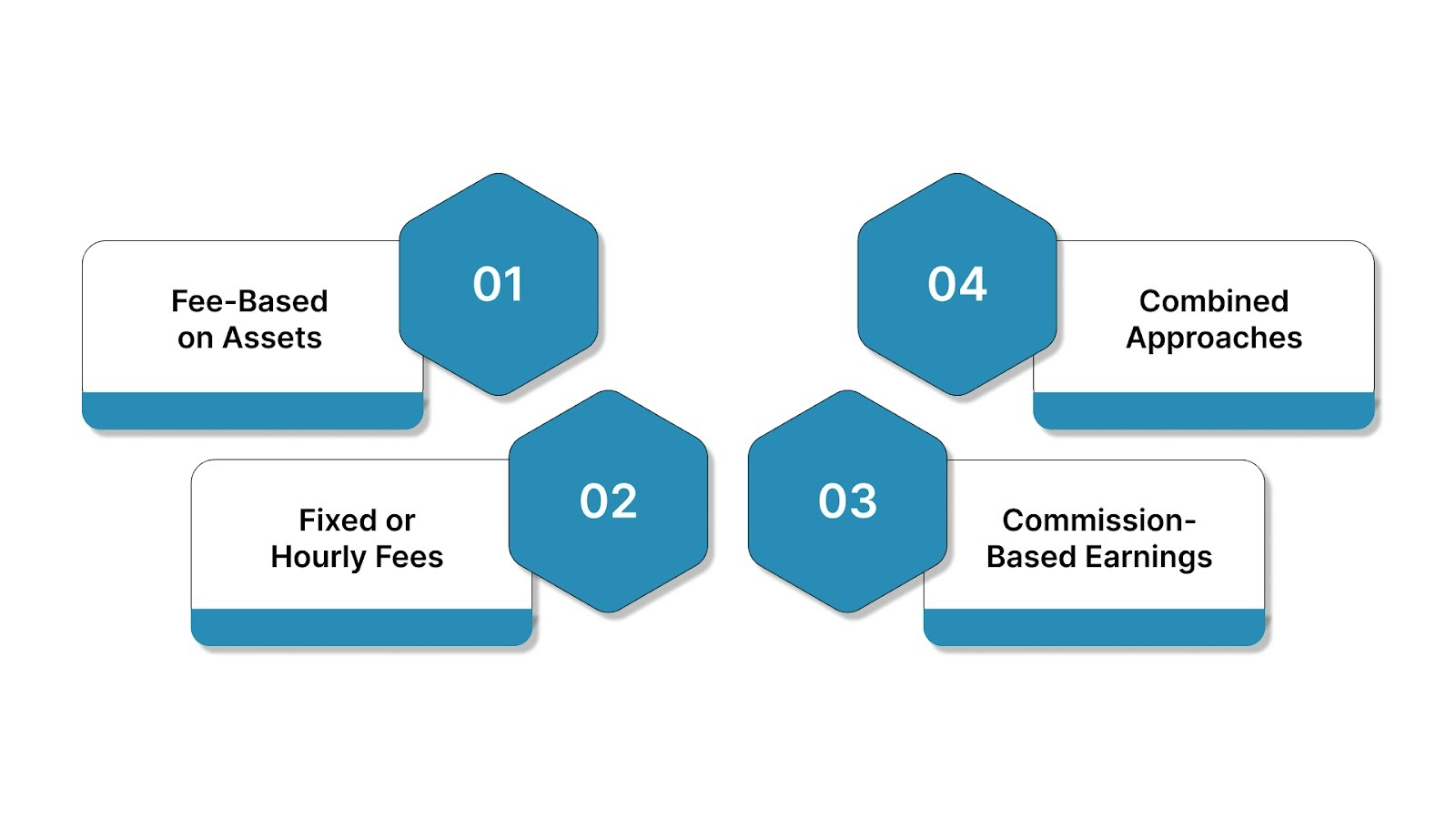

Compensation Structures for Client Advisors

How client advisors earn their income affects the way they serve you. Understanding these structures helps you select an advisor whose interests align with yours. Here are the primary models:

- Fee-Based on Assets: Many advisors charge a percentage of the assets they manage, often 1-2% per year. This ties their earnings to your portfolio’s growth, creating a shared incentive for success. It’s a popular choice for ongoing management.

- Fixed or Hourly Fees: Some offer services for a flat rate or hourly charge. This can be economical if you need a specific plan or occasional advice. However, it might not include continuous oversight, so weigh your needs carefully.

- Commission-Based Earnings: In this model, advisors earn money by selling financial products, such as mutual funds or insurance. While this can reduce upfront costs, it might influence their recommendations. Transparency about commissions is key here.

- Combined Approaches: Hybrid models blend fees and commissions. For instance, you might pay a planning fee plus commissions on certain products. This flexibility can work well, provided you understand all associated costs.

Each structure has its merits, depending on your financial situation and goals. Now that you know how advisors are paid, let’s consider the moments when their expertise becomes especially valuable.

Also Read: 9 Steps to Gain Financial Stability

When to Consult a Client Advisor

Deciding when to seek a client advisor depends on your circumstances and comfort level with financial management. Certain situations, however, make their guidance particularly beneficial.

- Life Milestones: Events such as getting married, starting a family, or losing a loved one can significantly shift your financial priorities. A client advisor helps you adjust your plan, ensuring it supports your new reality.

- Retirement Planning: As you approach retirement, decisions about savings, withdrawals, and income streams become increasingly complex. An advisor can streamline this process, maximizing your resources for the years ahead.

- Wealth Accumulation: If you’re aiming to grow your assets but feel unsure about investing, an advisor offers strategies and discipline. They help you avoid common pitfalls and stay focused on growth.

- Time Constraints: Managing finances requires effort. If your schedule is packed or financial details overwhelm you, an advisor can take the reins, giving you peace of mind.

- Objective Insights: Even if you’re financially savvy, an advisor provides an outside perspective. They spot blind spots and offer specialized knowledge you might not have.

These scenarios highlight the practical advantages of professional advice. Let’s wrap up with some final reflections on why a client advisor could be your next step.

Conclusion

A client advisor is your ally in mastering your financial future. From crafting tailored plans to dispelling myths and adapting to life’s changes, they bring expertise and reassurance to the table. By understanding their compensation and knowing when to seek their help, you can confidently take control of your finances.

If you’re ready to partner with someone who prioritizes your success, reach out to Forest Hill Management. We are here to guide you every step of the way. Contact us today to begin building the future you deserve.

Frequently Asked Questions

Q1. What exactly does a client advisor do?

A client advisor helps assess your financial situation, set and refine goals, build tailored strategies, and offer ongoing support to help you stay on track—especially during major life or market changes.

Q2. Do I need to be rich to work with a client advisor?

No. While many advisors serve high-net-worth individuals, many also work with clients who are just starting out or building wealth over time. Advisors can help at nearly every stage of your financial journey.

Q3. How are client advisors paid?

They may be compensated through a percentage of assets under management (AUM), hourly or flat fees, commissions on products, or a combination. Understanding their payment model ensures transparency and alignment with your interests.

Q4. Can’t I just use an app or robo-advisor instead?

DIY tools are helpful but limited. A client advisor offers personalized advice, emotional guidance during volatile markets, and the ability to adjust your plan based on real-time life events—something generic tools can’t fully replicate.

Q5. When should I consider hiring a client advisor?

Key moments include getting married, planning for retirement, managing a windfall or inheritance, starting a business, or simply wanting expert help managing complex finances or saving time.