Consumer Impact Recovery and Debt Collection Guide

Transform Your Financial Future

Contact UsHave you ever wondered what happens when you don't pay your bills on time? Or how one phone call from the consumer impact recovery company could change your financial future?

Debt collection is not just about numbers. It's a complex process that involves your rights, emotions, and decisions that can significantly impact your life and business. If you want to take control of overdue bills or protect your credit, it helps to understand how a consumer impact recovery company works. Knowing how to check the official consumer impact recovery phone number is also very important.

This blog is made for anyone who feels overwhelmed by debt, whether you are a consumer with growing bills, a small business managing unpaid invoices, or a bank handling many accounts. Let's learn about your rights and responsibilities, including easy ways to handle calls from collectors, correct errors, and maintain your financial health.

Ready to explore how the right information and the right consumer impact recovery company can put you back in control? Let's get started.

Key Takeaways

- Know your rights under laws like the FDCPA to dispute debts and stop unfair collection practices.

- Different debts (credit cards, loans, medical bills) have specific collection and protection rules.

- Collection agencies get paid differently; understanding their payment models helps you navigate interactions.

- Trusted companies like The Forest Hill Management offer fair, compliant debt recovery support tailored to your needs.

What is Consumer Impact Recovery?

Consumer Impact Recovery refers to the process where a company, often called a consumer impact recovery company, works to recover unpaid debts while minimizing negative effects on consumers.

Unlike harsh or aggressive collection tactics, this approach focuses on treating consumers fairly, respecting their rights, and providing clear communication. The goal is to help consumers resolve debts in a way that supports financial recovery and reduces stress.

This process includes verifying debts, setting up manageable payment plans, and helping consumers understand their rights. If you need assistance, always make sure to contact the company using their official consumer impact recovery phone number to avoid scams or fraud.

Now that we understand what consumer impact recovery involves, let's examine the key parties in the debt collection process and how their roles influence your financial journey.

Key Parties Involved in Debt Collection

Understanding the key parties in debt collection is essential to managing the process effectively and protecting your rights. Each participant plays a distinct role and has specific rights and responsibilities that impact how debts are recovered and resolved.

1. Creditor

The original lender or service provider you owe money to. They may collect payments themselves or hire others to do so on their behalf. Creditors must follow debt collection laws.

2. Debt Collector

A third-party company can be hired to collect unpaid debts. They contact consumers, negotiate payments, and must follow rules like the Fair Debt Collection Practices Act (FDCPA). Always verify contact information, such as the official consumer impact recovery phone number.

3. Debt Buyer

A company that buys unpaid debts from creditors at a discount and tries to collect the full amount. Verify legitimacy before sharing information.

4. Consumer

The debtor has the right to dispute debts, request verification, and limit communication with the creditor. Always confirm you're dealing with a legitimate consumer impact recovery company and use their official consumer impact recovery phone number.

Understanding who is involved leads us to the next step: recognizing the kinds of debts that commonly end up in collections and how each type may require different handling strategies.

Types of Debt That Can Go to Collections

Many kinds of debt can end up in collections if they remain unpaid. Knowing which debts are commonly sent to collections can help you stay informed and prepared. Here are some common examples:

- Credit Card Balances: Unpaid credit card bills often become collection accounts after a period of missed payments.

- Student Loans: Federal and private student loans can go to collections if payments are missed for a long time.

- Auto Loans: Even if your vehicle is repossessed, you may still owe money if the car's resale value is less than your loan balance.

- Personal Loans: Unpaid personal loans can be handed over to collection agencies or debt buyers.

- Utility Bills: Outstanding amounts for electricity, water, gas, and other utilities can be sent to collections.

- Bank Fees and Overdrafts: Unpaid fees or overdraft balances may be collected by third parties.

- Fines and Fees: Money owed to courts, law enforcement, or government agencies, such as traffic tickets or taxes, can also be converted into collection accounts.

- Unpaid Tuition: Schools or educational institutions may send unpaid tuition balances to a collection agency.

- Late Rent Payments: Landlords may report unpaid rent to debt collectors or agencies specializing in rental debts.

- Medical Bills: Hospital or doctor bills left unpaid for a long time are often sent to collections to recover the balance.

Each type of debt may require different approaches when dealing with collections. If you receive a call or notice from a consumer impact recovery company about any of these debts, always verify their identity through the official consumer impact recovery phone number.

With debts and parties identified, it's critical to know the legal rules designed to protect you. These regulations ensure debt collection is conducted fairly and respectfully.

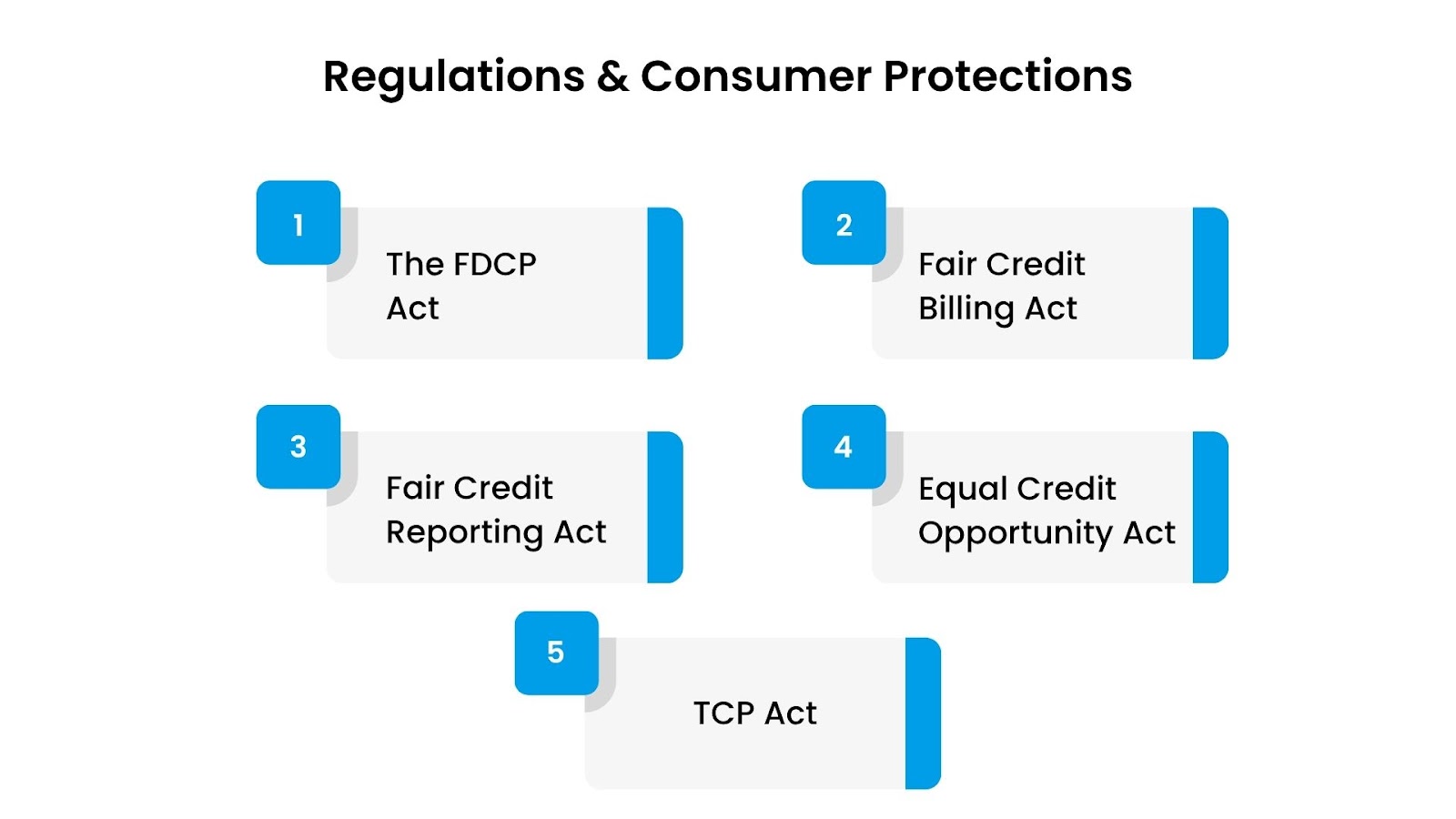

Regulations and Consumer Protections

When dealing with debt collection, it's crucial to know the protections in place to safeguard consumers. Several important federal laws ensure that debt collectors act fairly and that consumers' rights are respected.

Here's a clear overview of these key regulations and their implications for you.

The Fair Debt Collection Practices Act (FDCPA)

The FDCPA is the primary federal law that protects consumers from abusive or unfair debt collection practices. It applies to third-party debt collectors handling consumer debts.

Here are the key provisions:

- Communication: Debt collectors must contact consumers at reasonable times (typically 8 a.m. to 9 p.m.) and only through acceptable methods. They cannot contact you at work if your employer forbids it. Always confirm the collector's identity and use the official consumer impact recovery phone number before sharing information.

- Harassment or Abuse: Collectors cannot harass, oppress, or abuse you. This means no threats, obscene language, or repeated calls meant to annoy or intimidate.

- False Statements: Debt collectors must be truthful. They cannot lie about the debt, falsely claim legal action has been taken, or misrepresent themselves.

- Validation of Debts: Within five days of first contacting you, a collector must send a validation notice with details of the debt, including the amount owed and the creditor's name.

- Disputing the Debt: You have 30 days to dispute the debt in writing. If you do, the collection must stop until the debt is verified.

Fair Credit Billing Act (FCBA)

The FCBA protects consumers from billing errors on credit accounts, like credit cards.

Its main features include:

- Billing Error Rights: You can dispute charges that are incorrect, unauthorized, or not delivered as agreed.

- Dispute Handling: Once a dispute is filed, the creditor must investigate and resolve it, often suspending disputed charges during that time.

- Protection from Credit Damage: You won’t be penalized or have your credit report negatively affected during an ongoing dispute.

Fair Credit Reporting Act (FCRA)

The FCRA ensures the accuracy and privacy of information in your credit reports.

Important provisions are:

- Accuracy of Information: Credit reporting agencies must maintain accurate and complete data on your credit history.

- Consumer Access to Information: You can get a free credit report once a year and anytime your credit is denied.

- Dispute Mechanism: If you find errors, you can dispute them; the agency must investigate, usually within 30 days.

- Limited Access: Only people or companies with a legal reason can access your credit information.

- Privacy of Information: Your credit data must be kept confidential and not shared improperly.

Equal Credit Opportunity Act (ECOA)

The ECOA forbids discrimination in credit lending based on race, color, religion, national origin, sex, marital status, age, or public assistance income.

Key points include:

- Non-Discriminatory Lending: Credit decisions must be fair and impartial.

- Equal Terms and Conditions: Everyone must receive the same loan terms for the same creditworthiness.

- Consideration of Public Assistance Income: Income from welfare or other public assistance must be considered fairly.

- Spousal Guarantors: Whether a spouse guarantees the loan cannot affect credit decisions discriminatorily.

- Adverse Action Notification: If credit is denied, you must be informed of the reasons.

The Telephone Consumer Protection Act (TCPA)

The TCPA regulates how and when debt collectors can contact you by phone or text message.

Key points include:

- Consent: Collectors need your consent for automated calls or texts.

- Do-Not-Call (DNC) Lists: If you register your number on a national or company-specific DNC list, debt collectors must respect it.

- Timing of Calls: Calls can only be made during reasonable hours, usually 8 a.m. to 9 p.m.

- Identification: Debt collectors must identify themselves clearly during calls.

Next, let's understand how collection agencies are compensated for their efforts, which often shapes how they operate when recovering debts.

How Collection Agencies Get Paid

Understanding how collection agencies get paid can help you better navigate your interactions with them. Collection agencies use different payment models based on their role and the arrangement with the original creditor.

Below are the most common payment methods, along with how they work, their fee structures, and advantages.

1. Contingency Collection

In contingency collection, agencies only get paid when they successfully collect a debt. They work on a commission basis, attempting to recover funds on behalf of a creditor or a business.

Fee Structure: The agency charges a percentage of the amount collected, typically ranging from 25% to 50%, depending on factors like the age of the debt and difficulty in recovery.

Advantage: This model motivates the agency to work efficiently since their earnings depend solely on recovery success. It also means the creditor or business doesn’t pay upfront fees if the debt remains unpaid.

2. Debt Purchasing

In this model, debt buyers purchase portfolios of unpaid debts from creditors, usually for a fraction of the total owed amount. After the purchase, the debt buyer owns the debt and tries to collect the full balance directly from consumers.

Fee Structure: Debt buyers pay a one-time lump sum to acquire the debt portfolio at a discount. Their profit comes from recovering more than the purchase price.

Advantage: This approach transfers the risk away from the original creditor or business, which no longer has to manage collections. It lets companies free up resources while debt buyers specialize in maximizing debt recovery.

3. First-Party Collection Services

First-party collections happen when creditors handle their overdue accounts internally or through a dedicated in-house department. Sometimes, businesses hire external agencies to act as their first-party collectors, often under their brand name.

Fee Structure: First-party collection services usually involve a flat fee or a fixed contract fee, sometimes combined with bonuses for performance. Because these agencies represent the original creditor, fees tend to be lower than third-party contingency fees.

Advantage: Being directly linked to the original creditor, first-party collectors may maintain better relationships with consumers, leading to higher collection rates and fewer complaints. It also allows creditors to maintain control over how their accounts are managed.

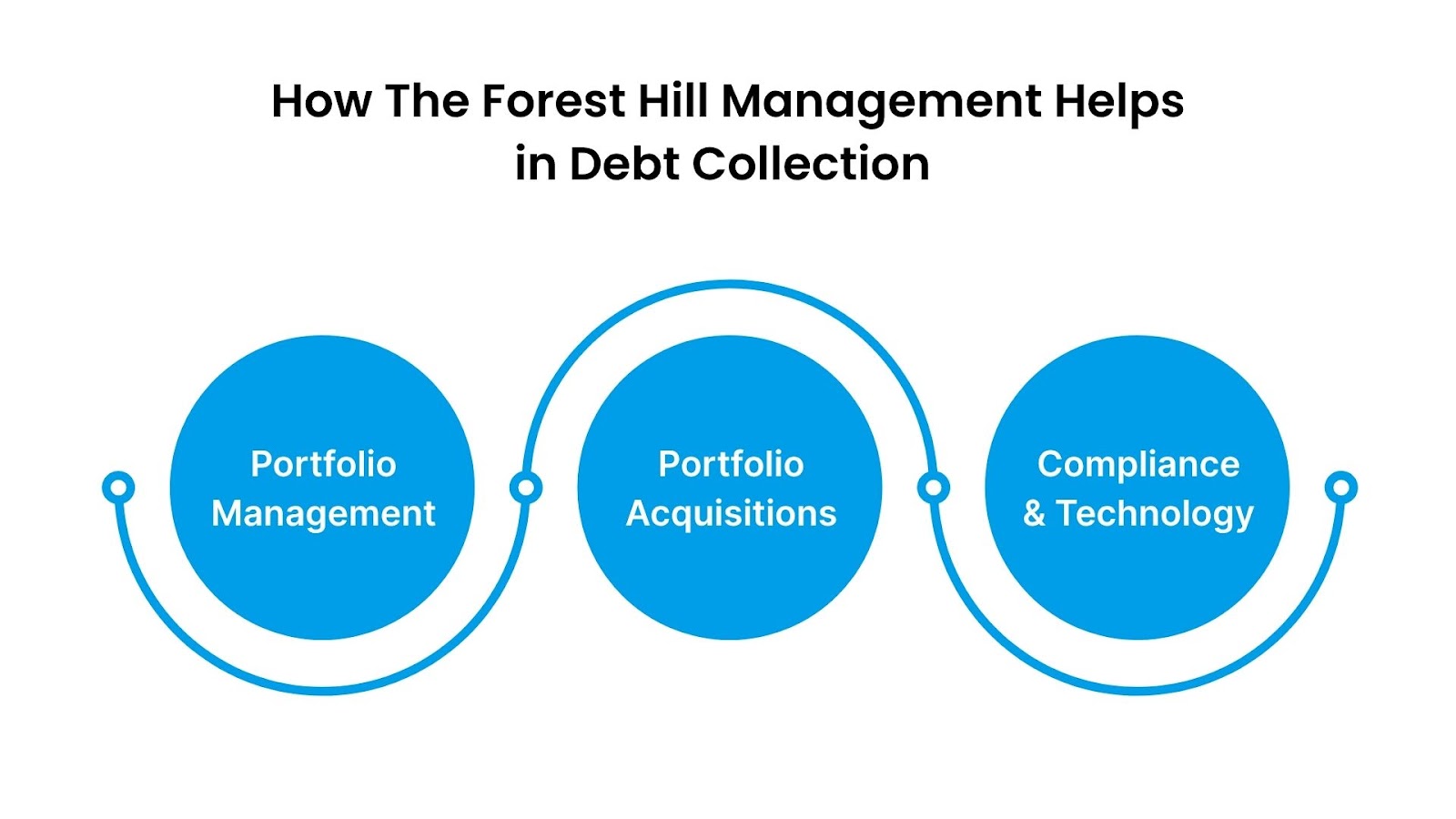

Now, let’s see how The Forest Hill Management offers expert, trustworthy services to support consumers and businesses through consumer impact recovery and debt collection challenges.

How The Forest Hill Management Helps in Debt Collection

With over two decades of industry experience, The Forest Hill Management helps individuals and businesses manage debt recovery fairly and effectively.Their personalized solutions help clients regain control over their financial health while ensuring compliance and ethical practices.

Let’s look at their key services:

- Portfolio Management: They handle overdue accounts with tailored strategies, easing the debt burden and providing clear support. Consumers can reach them safely via the official consumer impact recovery phone number.

- Portfolio Acquisitions: The company assists investors and businesses in acquiring debt portfolios through thorough due diligence and compliant processes, ensuring ethical recovery practices.

- Compliance & Technology: Using advanced technology, they secure consumer data and strictly follow all industry laws, giving clients confidence and protection.

If you’re facing overdue accounts or want expert help in managing your debts, contact our financial advisors to create a custom plan for you.

Conclusion

Whether you’re an individual struggling with unpaid debts or a business managing receivables, knowing how collection agencies operate and how reputable companies like The Forest Hill Management handle consumer impact recovery helps you manage the process more confidently and fairly.

Remember to always verify the identity of any debt collector by confirming their official consumer impact recovery phone number to protect yourself from scams and ensure you are working with a trustworthy company.

With the right knowledge and support, you can take control of your financial future, resolve debts responsibly, and move toward long-term financial stability.

FAQs

1. Is Consumer Collections a legitimate company?

Consumer Collections, also known as Consumer Collection Management, is generally considered a legitimate company that collects debts on behalf of original creditors. But, it's important to verify their legitimacy by asking for official documentation and confirming their contact details, such as the consumer impact recovery phone number, to avoid scams.

2. Can credit recovery companies sue you?

Yes, credit recovery companies, including consumer impact recovery companies, can sue you to recover unpaid debts if you fail to respond or settle the debt. They must follow legal procedures and provide proper validation of the debt before taking legal action.

3. How long before a debt is uncollectible?

Debts typically become uncollectible after the statute of limitations expires, which varies by state but usually ranges from 3 to 6 years for most consumer debts. After this period, a consumer impact recovery company can no longer sue to collect the debt, although they may still attempt to contact you.

4. What is the 11-word phrase to stop debt collectors?

The key phrase to stop debt collectors from contacting you is: “Please stop contacting me about this debt.” Sending a written request with this or similar wording to a consumer impact recovery company legally requires them to cease communication, except for specific situations like confirming no contact or taking legal action.