Debt Settlement Explained: How It Works and If It's a Good Option for You

Transform Your Financial Future

Contact UsDebt settlement can be a lifesaver for those drowning in debt and seeking a way out without resorting to bankruptcy. For individuals burdened with unsecured debts, such as credit card balances or personal loans, finding a manageable solution can often seem impossible.

Debt settlement offers an alternative path by allowing you to negotiate with creditors to reduce the amount owed. However, it’s not a one-size-fits-all solution, and there are important factors to consider.

This blog will guide you through the process of debt settlement, helping you understand how it works, its potential benefits, and the possible drawbacks, so you can determine if it’s the right option for your financial situation.

Key Takeaways

- Debt Settlement Provides Immediate Relief, But It Comes at a Cost: Debt settlement can reduce the total amount owed by negotiating with creditors, but it can cause a drop in your credit score and may lead to potential tax liabilities.

- It Can Be a Last Resort for Those Avoiding Bankruptcy: Debt settlement offers an alternative to filing for bankruptcy, which comes with long-lasting consequences on credit and financial stability.

- The Process Involves a Long-Term Commitment: While debt settlement can help resolve debt quicker than other options, it often takes 2–4 years to complete. The process involves monthly payments into an escrow account, which can then be used to settle debts once sufficient funds are accumulated.

- High Fees and Legal Risks Are Significant Considerations: Debt settlement companies often charge substantial fees, ranging from 15% to 25% of the total enrolled debt.

- Explore Alternatives Like Nonprofit Credit Counseling or Debt Management: If debt settlement seems too risky, other options like nonprofit credit counseling, debt management plans, or even DIY debt settlement might be better fits.

What is Debt Settlement?

Debt settlement is a financial strategy where a borrower negotiates with creditors to reduce the total amount of debt owed. It typically applies to unsecured debts, such as credit card balances, personal loans, and medical bills.

This process is usually facilitated by a debt settlement company or a negotiator who works on behalf of the borrower to reach a favorable arrangement with creditors. While debt settlement can provide relief from debt, it involves fees, has a negative impact on credit scores, and may result in tax consequences.

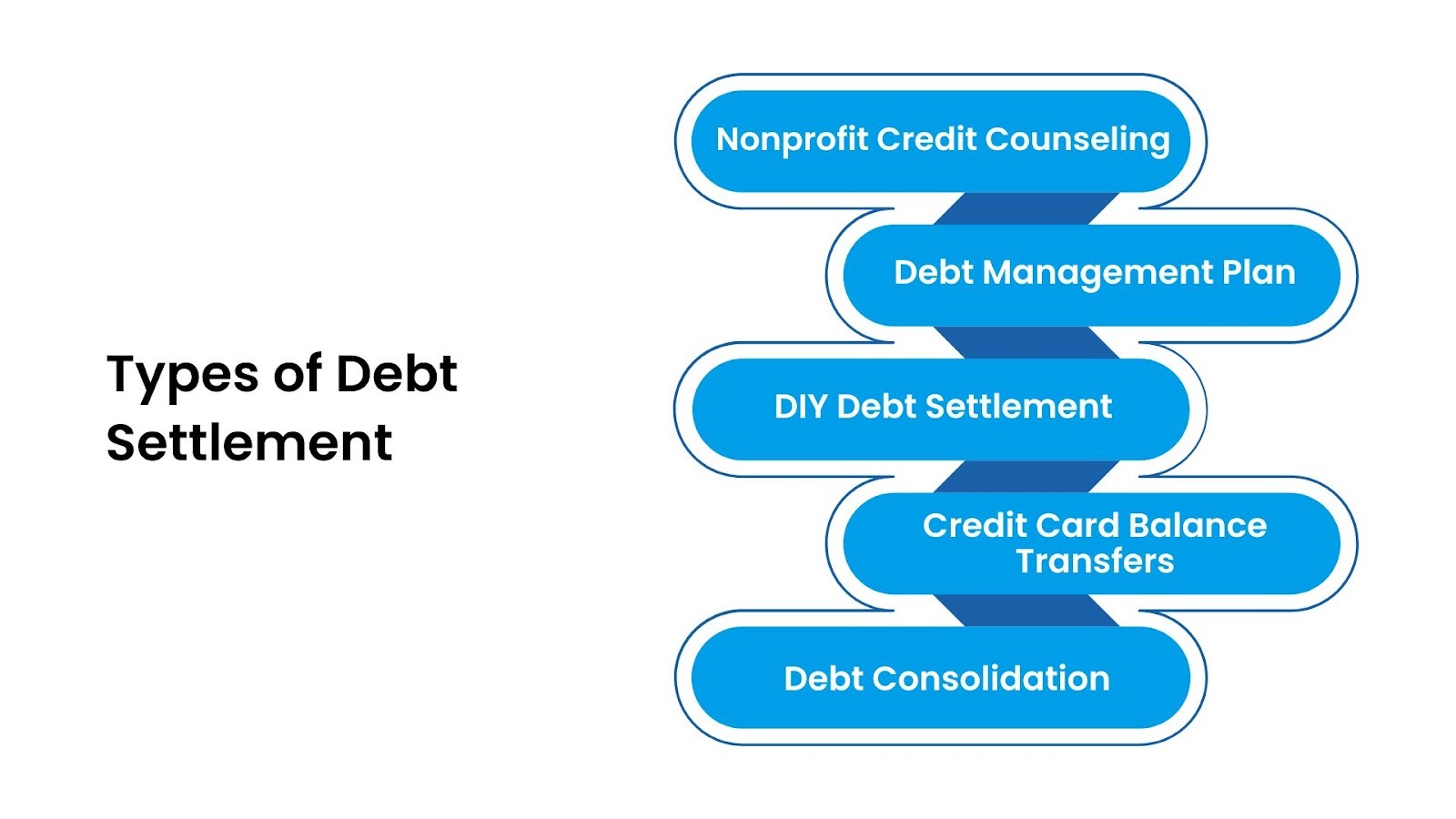

Types of Debt Settlement

Before you decide to pursue debt settlement, here are some types to consider. Each of these methods may offer a more suitable approach depending on your financial situation and long-term goals.

- Nonprofit Credit Counseling: While there's no one-size-fits-all solution, nonprofit credit counseling provides a personalized approach. A certified counselor reviews your financial situation and helps develop a customized plan. The first session is often free, making it a good starting point to explore your options.

- Debt Management Plan: A credit counselor can enroll you in a debt management plan (DMP), which can lower credit card interest rates to around 8%, far below the median rate of 24.37%. With this, you can pay off your credit card debt in 3-5 years, sometimes sooner.

- DIY Debt Settlement: If you’re wary of using a debt settlement company, consider negotiating directly with creditors. This eliminates the middleman and avoids fees, allowing for faster resolution without the risk of third-party involvement.

- Credit Card Balance Transfers: If you qualify for the right balance transfer card, you can move high-interest debt to one with a low or zero introductory rate (often for 12-18 months). However, after the promotional period ends, the interest rate may increase sharply, so paying off the balance quickly is key.

- Debt Consolidation: Debt consolidation involves taking out a single loan to pay off multiple credit cards, often at a lower interest rate. This simplifies payments, as you only have one monthly payment instead of several, and can save you money on interest in the long run

While these alternative debt relief options each have their merits, debt settlement remains a powerful solution for those facing severe financial hardship with unsecured debts.

How Debt Settlement Works to Restore Your Financial Stability

Debt settlement allows individuals to reduce the total amount of their debt by negotiating with creditors to pay a lump sum that's less than what is owed. This process is often chosen when debt becomes overwhelming, and bankruptcy is being avoided.

Here's a step-by-step breakdown of how it works:

1. Evaluate Your Debt and Negotiate with Creditors

The first step in the debt settlement process is evaluating your total debt, especially unsecured debts. You or a debt settlement company will negotiate with creditors, offering a reduced payment as a settlement.

For example, if you owe $15,000, you may negotiate to pay just $8,000. This happens when creditors realize it may be harder to recover the full amount through regular payments or legal action.

2. Settle Payments Through an Escrow Account

Instead of paying creditors directly, you make fixed monthly payments to a debt settlement company, which deposits them into an escrow account. The money accumulates in this account until it reaches the agreed-upon lump sum amount for settlement.

Depending on the size of your debt, it could take 2–3 years to gather enough funds in the escrow account. This helps you manage the debt repayment without paying creditors directly.

3. Credit Impact

After the debt is settled, it will be reported as ‘settled’ on your credit report. However, this status can significantly affect your credit score, often causing a drop of 100 points or more. A ‘settled’ status means that the debt was not paid in full, which creditors view negatively. This record will stay on your credit report for up to 7 years, though it is marked as “resolved.”

4. Legal and Tax Implications

One important consideration is that forgiven debt may be considered taxable income by the IRS. For instance, if $5,000 of your debt is forgiven, you may need to report that as income and pay taxes on it. It’s important to consult with a tax professional to understand the potential tax consequences.

The process itself is straightforward, but the real question is: what makes this approach worth considering when you're drowning in debt? The benefits extend beyond just reducing what you owe; they touch multiple aspects of your financial recovery.

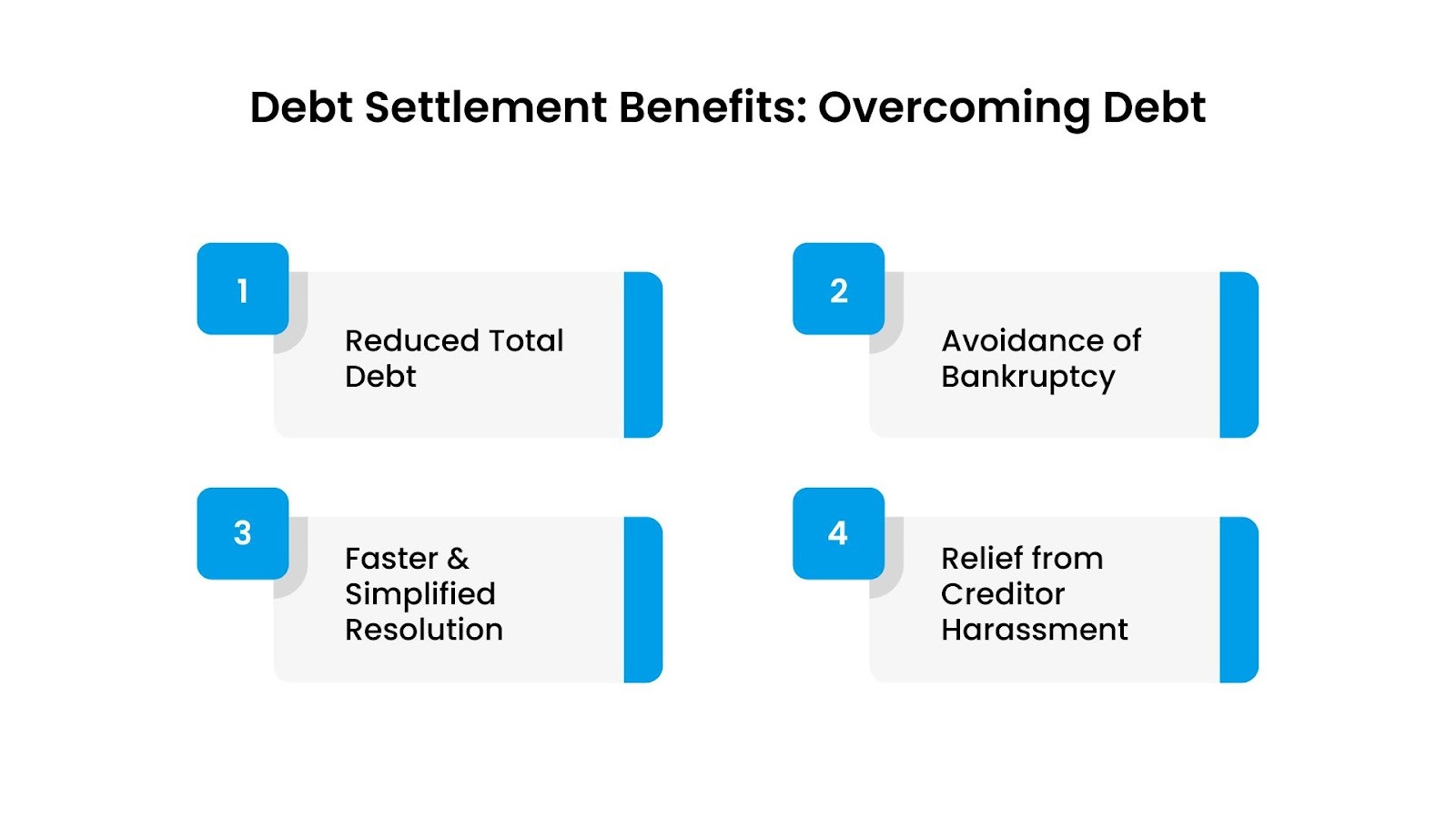

Advantages of Debt Settlement: How It Can Help You Overcome Debt

Debt settlement can offer significant benefits for individuals struggling with overwhelming unsecured debt. By negotiating with creditors to reduce the total amount owed, debt settlement provides financial relief. Below are some of the key advantages:

1. Reduced Total Debt

One of the primary benefits of debt settlement is that creditors may agree to accept a lump-sum payment that's less than the outstanding balance, forgiving the remainder of the debt.

According to a study from the American Association for Debt Resolution, the typical client seeking debt settlement had an average debt of around $27,000. With a 50% reduction through settlement, that debt could be lowered to approximately $13,500, providing substantial relief for those struggling with large balances.

2. Avoidance of Bankruptcy

For individuals on the brink of filing for Chapter 7 or Chapter 13 bankruptcy, debt settlement offers a less damaging alternative. While bankruptcy can have long-lasting negative effects on credit scores and financial stability, debt settlement helps to reduce debt without the severe consequences of bankruptcy.

3. Faster and Simplified Debt Resolution

Debt settlement not only leads to faster debt resolution compared to other options like debt management plans, but it also simplifies the repayment process. The settlement process takes 2 - 4 years, allowing individuals to become debt-free more quickly. Instead of juggling multiple monthly payments to various creditors, debt settlement consolidates payments into a single monthly deposit into an escrow account.

4. Relief from Creditor Harassment

Once a debt settlement agreement is in place, individuals may experience a reduction in calls and collection efforts from creditors. This can reduce stress and provide a sense of relief during the debt resolution process.

Every financial strategy carries trade-offs, and debt settlement comes with considerations that could impact your financial future if overlooked.

Disadvantages and Risks of Debt Settlement: What You Should Know Before Settling Your Debt

Knowing the risks of debt settlement is essential before choosing this path. While it can provide relief from overwhelming debt, it comes with drawbacks. These include a substantial hit to your credit score, potential tax liabilities on forgiven debt, and high fees charged by debt settlement companies.

1. Impact on Credit Score

Engaging in debt settlement can lead to a decline in your credit score. Typically, settling a debt for less than the full amount owed is reported to credit bureaus, which can lower your score by 100 points. This negative mark can remain on your credit report for up to 7 years, thereby making it difficult to secure loans or credit in the future.

2. Tax on Forgiven Debt

The IRS may consider forgiven debt as taxable income. For instance, if you settle a $20,000 debt for $10,000, the $10,000 forgiven amount could be considered taxable income, leading to a significant tax bill. Creditors are required to report forgiven debts over $600 to the IRS, which you must then report on your tax return.

3. Uncertain Success Rates

Not all creditors are willing to negotiate settlements, and some may refuse to work with debt settlement companies. Additionally, past investigations have revealed that only a minority of consumers successfully complete debt settlement programs, with many dropping out due to unmet expectations or financial difficulties.

4. Charge-Offs

A charge-off occurs when a creditor deems your debt uncollectible, closing your account and writing it off as a loss. This is bad news for your credit, as it signals to future creditors that you've failed to meet your obligations. A charge-off will remain on your credit report for up to 7 years.

5. High Fees Charged

Debt settlement companies often charge substantial fees for their services, typically ranging between 15% to 25% of the total debt enrolled in the program. In some cases, these fees could be even higher. These fees are usually not applied to your debt but are retained by the agency, reducing the overall benefit of the settlement.

6. Legal Actions from Creditors

While some creditors may agree to settle debts, others may pursue legal actions to recover the full amount owed. This can result in lawsuits, judgments, and other legal consequences, further complicating your financial situation.

One of the key advantages of working with Forest Hill Management is its commitment to offering personalized payment plans that are designed to fit each client’s unique financial circumstances.

Unlike generic, one-size-fits-all solutions, Forest Hill takes the time to understand your specific situation, whether it’s the total amount of debt, income fluctuations, or other financial obligations, and then crafts a repayment plan that works for you. Make a payment online today!

Is Debt Settlement Right for You? How to Determine Its Suitability

Debt settlement can be an effective way to reduce overwhelming debt, but it’s not the best option for everyone. Here’s how to figure out if it aligns with your financial situation:

- Are you dealing with unsecured debt? Debt settlement is most effective for unsecured debts like credit cards. If these make up the majority of your debt, settling might be a good option. It helps you reduce the total debt owed by negotiating with creditors for a lower payment.

- Are monthly payments becoming a struggle? If you’re having trouble making minimum payments and find yourself juggling multiple bills, debt settlement can offer relief by consolidating your payments and reducing the overall debt.

- Is your credit already affected? If your credit score has already taken a hit due to missed payments, debt settlement might not hurt as much as it would for someone with a healthy score.

- Do you have the means to make a lump sum payment or monthly contributions? Debt settlement usually requires a lump sum to settle debts or a fixed monthly payment into an escrow account. If you have the ability to make either of these payments, it could be a feasible path for you to get out of debt sooner than through a debt management plan.

- Are you prepared for potential legal actions? During the settlement process, creditors may threaten legal action if you stop making payments. Although creditors often prefer to settle, there is still a risk of lawsuits or wage garnishment.

- Have you explored other options like bankruptcy or debt management plans? While debt settlement can be effective, it’s important to consider other debt relief options. Bankruptcy and debt management plans can help manage debt without risking your credit score.

Once you've determined that debt settlement aligns with your financial situation and goals, the next crucial step is finding the right partner to guide you through the process.

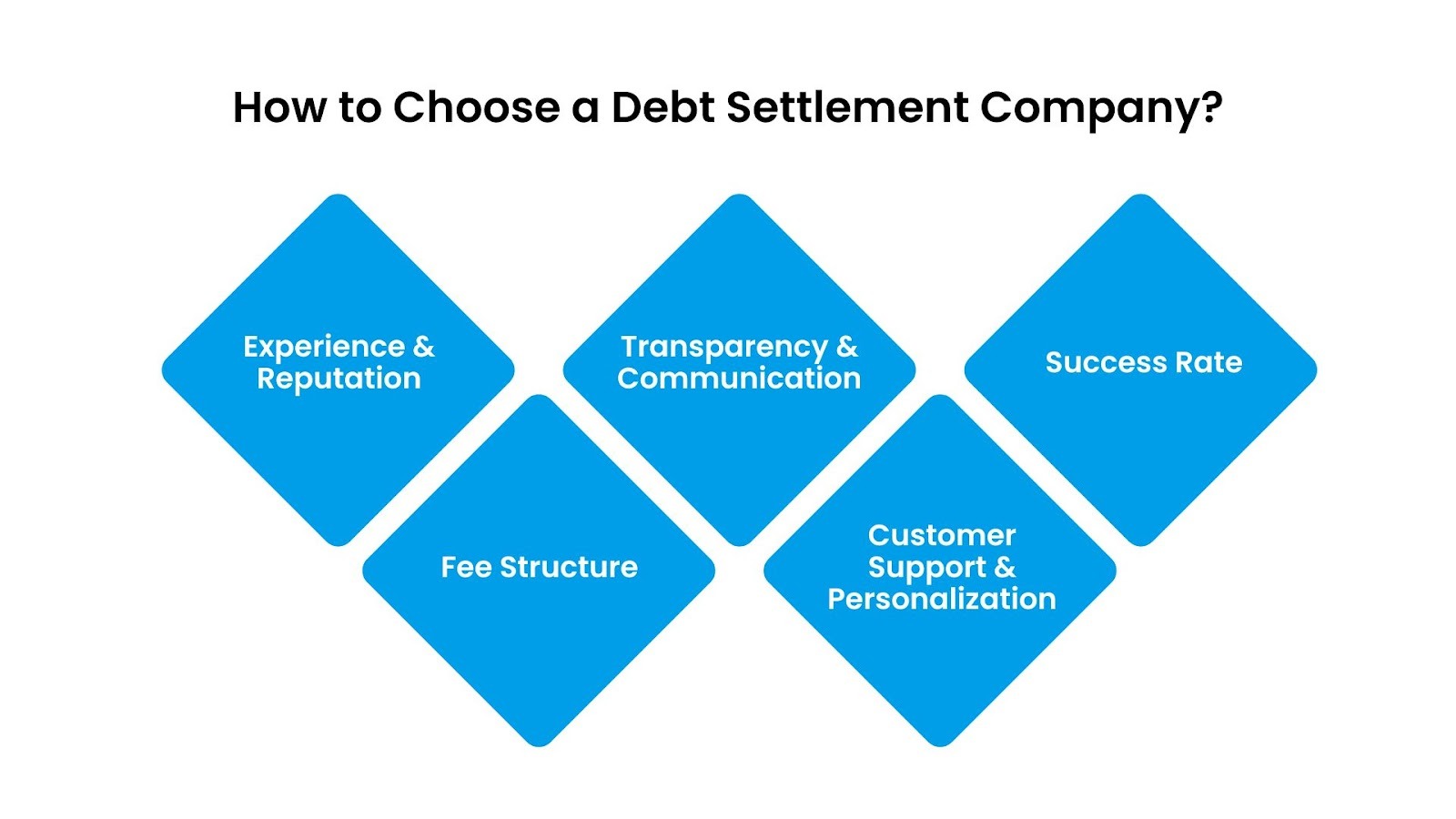

Choosing a Debt Settlement Company

Choosing the right debt settlement company is a critical step in the debt resolution process. It’s important to find a company that aligns with your financial goals and ensures ethical practices throughout the negotiation process.

- Experience and Reputation: Look for a debt settlement company with a proven track record and positive customer reviews. Check for certifications and affiliations with reputable organizations, such as the American Fair Credit Council (AFCC).

- Fee Structure: Many debt settlement companies charge fees based on a percentage of the debt enrolled in the program. Make sure the fees are reasonable and only paid once a settlement is successfully achieved.

- Transparency and Communication: A good debt settlement company should be transparent about the process and fees. They should keep you informed of progress and offer regular updates.

- Customer Support and Personalization: Choose a company that offers personalized solutions, as every financial situation is unique.

- Success Rate: A company’s success rate in settling debt is an important consideration. Look for a debt settlement company with a strong track record of negotiating with creditors and achieving satisfactory settlements for clients.

So, where to find a company that actually embodies these principles? Forest Hill Management has built its reputation on the very qualities that distinguish effective debt settlement services from those that merely promise results.

Why Choose Forest Hill Management for Debt Settlement?

Forest Hill Management is a reputable receivables management organization specializing in the management of past-due accounts. With a history dating back to 2020, they have assisted thousands of consumers in resolving their financial obligations. Their mission is to help individuals achieve financial freedom and move forward confidently in their lives.

Key Services:

- Portfolio Management: Forest Hill offers personalized portfolio management plans designed to help clients effectively manage outstanding financial obligations and achieve financial freedom.

- Portfolio Acquisitions: They provide seamless portfolio acquisitions to offer relief to businesses burdened with delinquent accounts, ensuring a fair opportunity for portfolio holders to settle their obligations.

- Compliance & Technology: Forest Hill ensures strict adherence to industry regulations and employs advanced technology to safeguard clients' financial data, maintaining confidentiality throughout the process.

Client-Centric Approach:

- Personalized Solutions: Understanding that every financial journey is unique, Forest Hill tailors strategies that align with clients' specific needs and aspirations.

- Expert Guidance: Clients have access to knowledgeable financial advisors who provide support and guidance every step of the way, ensuring informed decision-making.

Conclusion

Debt settlement can provide much-needed relief for individuals overwhelmed by unsecured debt. It offers an alternative to bankruptcy by allowing you to negotiate with creditors to reduce the amount owed, often by paying a lump sum that's lower than the full debt.

While debt settlement can lead to significant financial relief, it comes with potential risks, including a negative impact on your credit score, the possibility of tax liabilities on forgiven debt, and high fees charged by settlement companies. Additionally, creditors may refuse to settle or pursue legal action, complicating the process.

If you decide that debt settlement is the best option for you, Forest Hill Management offers personalized debt resolution strategies tailored to your needs. With their expertise and transparent fee structure, they can help you regain control of your finances.

Contact our advisors for personalized support and make a payment online today.

FAQs

1. Does a debt settlement ruin your credit?

Yes, debt settlement can significantly lower your credit score since creditors report settled debts as “paid for less than owed.” This mark stays on your credit report for up to seven years.

2. Is it better to settle or pay in full?

Paying in full is always better for your credit, as it avoids the negative marks associated with settlements. However, if paying in full isn’t possible, settlement can be an option to reduce your debt burden.

3. Will my credit score increase after the settlement?

Initially, your credit score may decrease after a settlement due to the negative report. Over time, however, it can improve as you reduce debt and rebuild your financial habits.

4. Is it true that after 7 years, your credit is clear?

Yes, most negative marks, including settled debts, will drop off your credit report after seven years. However, the long-term impact may still be felt, as potential lenders may consider your past history.

5. Can I pay the full amount after settlement?

Yes, you can pay the full amount after a settlement if you choose to do so. Some creditors may allow you to repay the full debt after settling, though it may not reverse the settlement status on your credit report.