The Ultimate Guide to Repair Your Credit Fast: 8 Sure Steps for a Stronger Score

Transform Your Financial Future

Contact UsIs your credit score holding you back from achieving your financial goals? You're not alone. As of 2025, approximately 15.5% of Americans have a credit score below 600, placing them in the "bad credit" category. This can make securing loans, obtaining favorable interest rates, or even renting a home more challenging.

However, the good news is that repairing your credit doesn't have to be a challenging task. With the right strategies and consistent effort, you can improve your credit score and regain control over your financial future. In this guide, we'll walk you through simple, actionable steps to help you repair your credit and set you on the path to financial stability. Let's get started!

Key Takeaways

- Regularly Check and Dispute Your Credit Report: Identify errors and fraudulent activities early on to prevent damage to your score. Dispute inaccuracies to improve your credit standing.

- Bring Past-Due Accounts Current: Address overdue accounts by negotiating with creditors or setting up payment plans. Timely payments have a significant impact on your credit score.

- Lower Your Credit Utilization: Keep your credit utilization under 30% by paying down balances or requesting higher credit limits, which can significantly boost your score.

- Use Secured Credit Cards: A secured credit card can help rebuild your credit by demonstrating responsible credit use. This can lead to an improved score over time.

- Set Up Autopay for Timely Payments: Automating your bill payments ensures you never miss a deadline, preventing late fees and negative marks on your credit report.

What is Credit Repair and Why is it Important?

Credit repair is the process of identifying and addressing inaccuracies or outdated information on your credit report that may impact your credit score. This could be disputing errors with credit bureaus, negotiating with creditors, or implementing strategies to improve your credit habits.

While individuals can undertake credit repair independently, many others engage with professional services to expedite the process, especially in cases of complex issues.

Here are the key reasons why repairing your credit is essential for long-term financial health:

- It can help secure lower interest rates on loans and credit cards

- Good credit is often required for renting a home or signing a lease

- Employers in some industries may review your credit score as part of the hiring process

- Allows you to gain access to better financial products

- Increase your chances of approval for a mortgage

- A higher score may result in lower insurance premiums

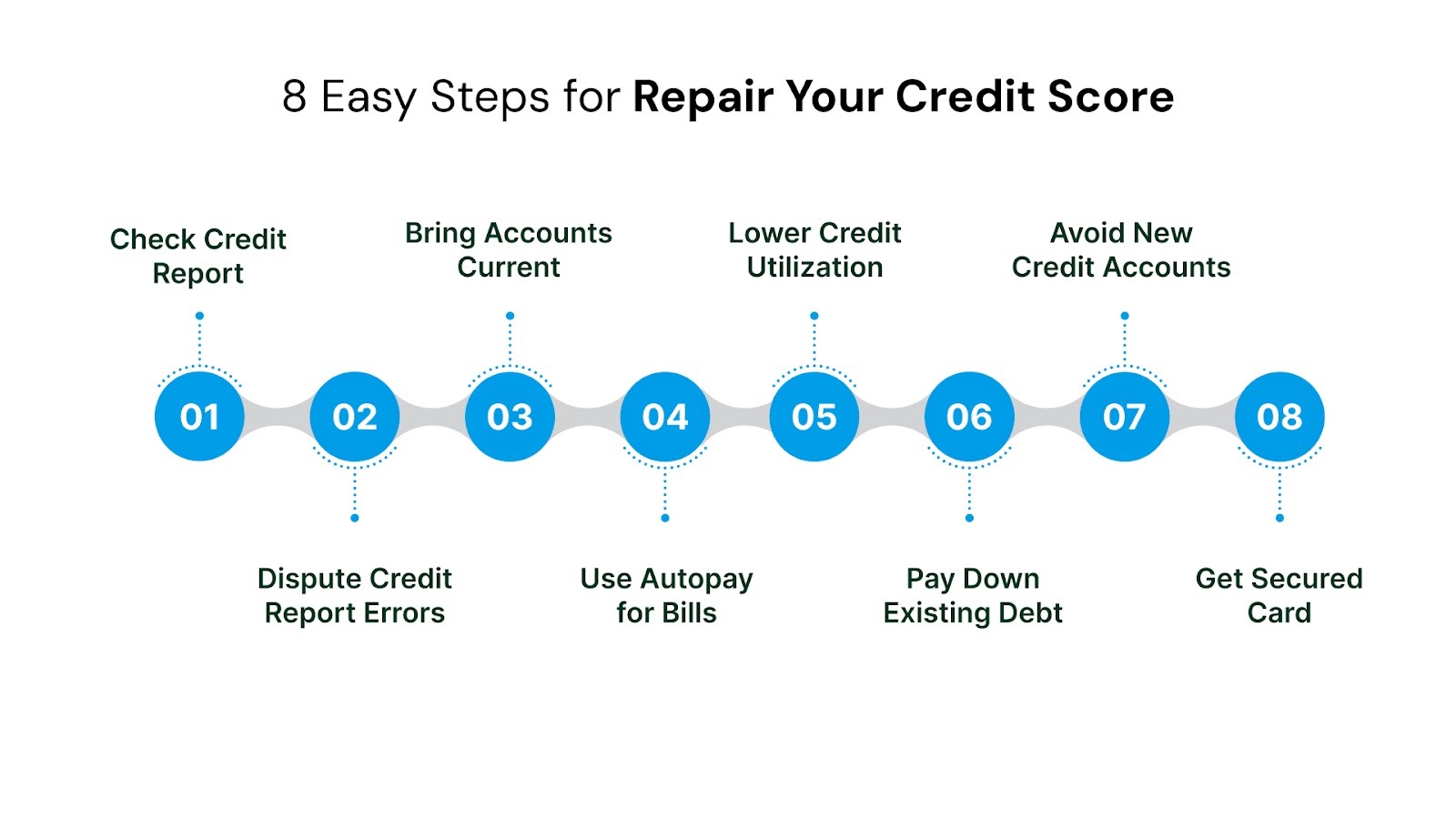

Top 8 Easy Steps to Repair Your Credit Score

Repairing your credit score doesn’t happen overnight, but by following these easy steps, you can see significant improvements. The process may vary depending on factors like your current credit score, the efforts you put into managing your debt, and the type of credit issues you’re dealing with. However, with your consistent effort, you’ll be on the path to a stronger score in no time.

1. Check Your Credit Report

Your credit report is a record of your credit history, encompassing details about your credit accounts, payment history, and any public records such as bankruptcies or judgments.

This report plays an important role in determining your credit score, which in turn helps you secure loans, obtain favorable interest rates, and even employment opportunities.

Why It's Crucial to Check Your Credit Report?

- Identify Errors: Mistakes on your credit report, such as incorrect account information or outdated personal details, can impact your credit score. Regularly reviewing your report allows you to spot and dispute these inaccuracies promptly.

- Detect Fraudulent Activity: Unauthorized accounts or unfamiliar inquiries may indicate identity theft. Monitoring your credit report helps in early detection, enabling swift action to mitigate potential damage.

- Understand Your Credit Standing: Familiarizing yourself with your credit report provides insight into factors affecting your credit score, such as payment history, credit utilization, and the length of your credit history.

How to Obtain Your Free Credit Report

Under the Fair and Accurate Credit Transactions Act (FACTA), you're entitled to a free credit report from each of the three major credit bureaus- Equifax, Experian, and TransUnion—once every 12 months.

2. Dispute Credit Report Errors

Identifying inaccuracies in your credit report is a crucial step in repairing your credit. These errors can arise from various sources, including clerical mistakes, outdated information, or fraudulent activities. Addressing these discrepancies promptly can prevent potential impacts on your credit score and financial opportunities.

Steps to Dispute Errors on Your Credit Report

- Identify the Error: Carefully review your credit report for inaccuracies, such as wrong personal details, outdated information, or unfamiliar accounts.

- Collect Supporting Documents: Gather any relevant documents (e.g., bank statements, receipts) to support your dispute.

- Dispute with the Credit Bureau: File your dispute online or by mail with the credit bureau (Equifax, Experian, or TransUnion) where the error appears.

- Contact the Furnisher: Reach out to the company that reported the error (e.g., your lender) and ask them to correct the information.

- Wait for Resolution: The credit bureau must investigate the dispute within 30 days and notify you of the outcome.

- Monitor Your Credit: Check your credit report regularly and file a complaint with the Consumer Financial Protection Bureau (CFPB) if any issues arise.

3. Bring Past-Due Accounts Current

Bringing past-due accounts current is one of the most effective ways to repair your credit score. Your payment history accounts for around 35% of your FICO credit score, the most influential factor in determining your score.

This means any missed payments or overdue accounts can have a major negative impact on your credit. When your payments are late by 30, 60, or 90 days, it’s reported to the credit bureaus and can cause your score to drop significantly. If these overdue accounts continue to remain unresolved, the damage to your credit score can be long-lasting.

Steps to Bring Past-Due Accounts Current

- Prioritize Accounts Based on Impact: Begin with accounts that have the most substantial effect on your credit score, such as credit cards and personal loans. Addressing these can lead to more noticeable improvements in your credit profile.

- Contact Creditors to Negotiate Terms: Reach out to your creditors to discuss your situation. Many creditors offer hardship programs or may be willing to adjust your payment terms to help you get back on track.

- Set Up Payment Plans: If you're unable to pay the full amount, negotiate a payment plan that fits your budget. Ensure that the agreed-upon terms are documented in writing.

- Avoid Closing Accounts: Even if you pay off a past-due account, consider keeping it open. Closing accounts can reduce your available credit and potentially increase your credit utilization ratio.

- Monitor Your Credit Reports: After bringing accounts current, regularly check your credit reports so that the updates are reflected accurately.

4. Pay Your Bills On Time with Autopay

Consistently paying bills on time helps you avoid late payment fees, which can add up over time and strain your finances. Setting up automatic payments (autopay) can significantly reduce the risk of missing due dates.

Autopay is a feature offered by many banks, credit card companies, and service providers that allows you to automate your bill payments. This means that you can set up recurring payments to be made automatically on a specific date, eliminating the need for you to manually make payments each month.

Advantages of Autopay

- Convenience: Once set up, autopay handles your recurring bills automatically, saving you time and effort.

- Consistency: Autopay ensures that payments are made on time, every time, which is crucial for maintaining a positive credit history.

- Peace of Mind: With autopay, you can rest assured that your bills are being paid promptly, reducing financial stress.

Considerations When Using Autopay

- Monitor Your Bank Account: Ensure that your bank account has sufficient funds to cover the scheduled payments to avoid overdraft fees.

- Review Bills Regularly: Even with autopay, it's important to periodically review your bills for any discrepancies or unauthorized charges.

- Update Payment Information: If you change your bank account or credit card, remember to update your autopay settings to prevent missed payments.

5. Lower Your Credit Utilization Rate

Your credit utilization ratio—the percentage of your available credit that you're using—is a crucial factor in determining your credit score. It accounts for approximately 30% of your FICO® Score, making it the second most influential factor after payment history. Maintaining a low credit utilization rate demonstrates to lenders that you manage credit responsibly, which can positively impact your creditworthiness.

Understanding Credit Utilization

Credit utilization is calculated by dividing your total credit card balances by your total credit limits. For example:

- If you have two credit cards with limits of $5000 and $3000, respectively, your total credit limit is $8000.

- If your balances are $2000 and $500, your total balance is $2500.

Your credit utilization ratio would be ($2500 ÷ $8000) × 100 = 31.25%.

Financial experts recommend keeping your credit utilization below 30% to maintain a healthy credit score.

Strategies to Lower Your Credit Utilization

- Pay Down Existing Balances: Lower your credit utilization by paying down your credit card balances. Prioritize paying off cards with the highest balances or interest rates first.

- Request a Credit Limit Increase: Contact your credit card issuer to request a higher credit limit. An increased limit, while maintaining the same spending level, reduces your credit utilization ratio.

- Open a New Credit Card: Opening a new credit card can increase your total available credit, thereby lowering your overall credit utilization ratio.

- Avoid Closing Unused Credit Accounts: Closing old or unused credit cards reduces your total available credit, potentially increasing your credit utilization ratio.

- Make Multiple Payments Throughout the Month: Making payments before your billing cycle ends can lower the balance reported to credit bureaus, thus reducing your credit utilization ratio.

- Monitor Your Credit Utilization: Regularly check your credit card balances and credit limits to stay informed about your credit utilization.

6. Pay Down Existing Debt

Reducing outstanding debt is a fundamental step in improving your credit score and achieving financial stability. Your credit score is influenced by several factors, with the amount you owe accounting for approximately 30% of your score. By strategically paying down existing debt, you can lower your credit utilization ratio, enhance your creditworthiness, and reduce the financial strain caused by high-interest obligations.

Steps to Pay Down Debt

- Assess Your Debt Load: Begin by compiling a list of all your debts, including credit cards, personal loans, medical bills, and any other outstanding balances. Note the interest rates and minimum payments; this will help prioritize repayment strategies.

- Choose a Repayment Strategy: There are two primary methods for paying down debt:

- Debt Snowball Method: Focus on paying off the smallest debt first while making minimum payments on others.

- Debt Avalanche Method: Prioritize paying off debts with the highest interest rates first, which can save money on interest over time.

- Create a Budget: Establishing a detailed budget is crucial for managing expenses and allocating funds toward debt repayment. Track your income and expenditures to identify areas where you can cut back and redirect those savings.

- Consider Debt Consolidation: If managing multiple debts is challenging, consolidating them into a single loan with a lower interest rate can simplify payments and reduce overall interest costs.

- Avoid Accumulating More Debt: While focusing on paying down existing debt, avoid taking on additional debt. Refrain from making new credit card purchases or taking out new loans unless absolutely necessary.

7. Avoid Opening New Credit Accounts

When working to repair your credit, it's crucial to be mindful of opening new credit accounts. While it might seem beneficial to increase your available credit, doing so can have unintended negative effects on your credit score.

Why Opening New Credit Accounts Can Harm Your Credit?

- Hard Inquiries Impact Your Score: Each time you apply for a new credit account, the lender conducts a hard inquiry (or hard pull) on your credit report. This process can cause a temporary dip in your credit score by a few points. While a single inquiry might have a minimal impact, multiple inquiries within a short period can compound the effect and raise concerns for lenders.

- Reduces Average Age of Credit Accounts: The length of your credit history accounts for about 15% of your credit score. Opening new accounts decreases the average age of your credit accounts, which can lower your score.

- Potential Increase in Credit Utilization: While opening a new credit account increases your total available credit, it can also lead to higher balances if you're not careful with your spending. This increase in balances can raise your credit utilization ratio.

- Signals Financial Instability to Lenders: Applying for multiple new credit accounts in a short period can signal to lenders that you're experiencing financial instability or are overextending yourself.

8. Apply for a Secured Credit Card

A secured credit card is a great option for individuals looking to rebuild their credit. Unlike traditional credit cards, a secured card requires a cash deposit, which acts as collateral and determines your credit limit. This makes it a low-risk option for lenders, making it easier to obtain, even if you have a poor or limited credit history.

Tools and Methods

- Compare Different Secured Credit Cards: Look for cards with low annual fees and favorable terms. Some cards may even offer perks like cash back or rewards points for responsible use. (nerdwallet.com)

- Pay Your Bill on Time: Ensure you make timely payments, as late payments can negatively affect your credit score. Many secured cards report to the major credit bureaus, which is key to rebuilding your score.

- Start with a Low Deposit: Start with a deposit you can afford, and over time, as you build credit, your credit limit may be increased.

Benefits

- Improved Credit Score: Responsible use of a secured credit card can help rebuild your credit score by showing you can manage debt and make payments on time.

- Opportunity for Unsecured Credit: After consistently demonstrating responsible use, some secured cards offer the chance to upgrade to an unsecured credit card, with better benefits and terms.

- Low Risk for Lenders: Because the credit limit is secured by your deposit, it’s less risky for lenders, which can help you qualify for other credit products in the future.

Empower Your Financial Future with Forest Hill Management

Forest Hill Management is a trusted financial services provider specializing in personalized credit repair, debt management, and portfolio acquisition solutions. With over two decades of experience, they are committed to helping individuals and businesses navigate financial challenges and achieve lasting financial freedom.

Key Services

- Debt Management: They provide comprehensive debt management services, including negotiating with creditors, consolidating debts, and creating manageable repayment plans to alleviate financial stress.

- Portfolio Acquisitions: The company assists businesses in acquiring portfolios of delinquent accounts, offering a fair opportunity to settle obligations and improve financial standing.

- Financial Advisory Services: Forest Hill Management offers expert financial advice, helping clients make informed decisions to secure and grow their financial assets.

- Personalized Approach: They understand that each client's financial situation is unique and provide customized solutions to meet individual needs.

- Commitment to Compliance: The company adheres to industry regulations, ensuring that all services are provided ethically and legally.

Conclusion

Repairing your credit is a journey that requires consistent effort, but with the right steps, it’s entirely achievable. By checking your credit report regularly, disputing errors, paying your bills on time, and using tools like secured credit cards, you can see substantial improvements in your credit score. While it may take time, each step brings you closer to a stronger financial future, where loans, mortgages, and better financial opportunities are within reach.

For those looking for additional guidance in managing their debts and credit, Forest Hill Management offers expert services that can help you get back on track. Contact our advisors today to learn more about how we can help you achieve financial freedom.

FAQs

1. What is the 2 2 2 credit rule?

The 2-2-2 rule suggests keeping two credit cards, maintaining a 2% credit utilization ratio, and making at least two credit payments per month to improve credit scores.

2. What is the 30 percent rule for credit?

The 30% rule advises keeping your credit utilization below 30% of your total available credit to maintain a healthy credit score and demonstrate responsible credit usage.

3. Is 700 credit at 20% good?

A credit score of 700 is considered good, and if you have a 20% utilization rate, it indicates that you are managing your credit responsibly, though lowering utilization further may improve your score.

4. Does income affect my credit score?

Income doesn’t directly affect your credit score, but it influences your ability to pay off debt, which can indirectly improve your credit score by ensuring timely payments.

5. What happens if I use 80% of my credit?

Using 80% of your available credit negatively impacts your credit score by raising your credit utilization ratio, which may indicate to lenders that you’re over-relying on credit.