Financial Management Tools to Strengthen Debt Collection

Transform Your Financial Future

Contact UsLate payments aren’t just inconvenient; they can stall growth, drain internal resources, and pose regulatory risks. In Q1 2025, U.S. household debt reached $18.2 trillion, with $1.18 trillion tied up in credit card balances alone.

At the same time, credit card delinquencies, particularly those 90 days past due, are climbing sharply.

For businesses, this plateau in consumer finances means more accounts fall behind, and often without a straightforward or compliant recovery process.

That’s where financial management services for debt collection come in. With the right strategies, tools, and adherence to CFPB regulations, your business can improve recovery rates, maintain legal compliance, and protect its financial health.

In this article, we’ll walk through how tailored financial strategies can streamline collections, strengthen customer trust, and support sustainable business growth.

What Are Financial Management Services in Debt Collection?

Effective debt collection isn’t just about chasing payments; it’s about managing the entire process with precision, compliance, and empathy. This includes the timing and method of outreach, dispute resolution procedures, account management practices, and compliance oversight.

Financial management services support this by offering structure:

- Clear communication protocols

- Receivables oversight

- Risk mitigation strategies

- Compliance alignment (especially under CFPB guidelines)

- Use of automation and data to streamline recovery

To fully understand this, let’s start with two key components:

Debt Collection

More than reminders or follow-ups, debt collection is the coordinated process of recovering unpaid balances while preserving the customer relationship. It involves consistent communication, negotiation, documentation, and, when necessary, legal action.

Portfolio Management

In the context of collections, portfolio management involves actively overseeing accounts receivable to identify patterns, prioritize actions, and minimize financial exposure. It turns a reactive collections process into a proactive financial strategy.

Understanding these foundational terms and the systems behind them is crucial to establishing a compliant and customer-conscious collection process. That’s why the CFPB Debt Collection Rule is the next piece of the puzzle. It provides the compliance guardrails every modern debt strategy must follow.

How the CFPB Debt Collection Rule Supports Compliance

Staying compliant isn’t just about checking legal boxes. It’s about building trust and protecting your business from costly mistakes.

The Consumer Financial Protection Bureau’s Debt Collection Rule, built on Regulation F, provides the legal framework for fair, respectful, and structured debt recovery. Following it doesn’t just reduce risk. It enhances your engagement with consumers.

Here’s how the rule strengthens your collection strategy:

- Sets Clear Contact Limits: The “7-in-7 Rule” limits debt collectors to seven calls within seven days to the same consumer about a specific debt. This reduces excessive outreach and encourages more respectful communication.

- Mandates Consumer-Friendly Communication: Collectors must provide multiple contact methods, such as phone, email, or text, and respect the consumer’s preferences. This improves engagement and fosters trust.

- Requires Transparent Disclosures: Validation notices must clearly explain the debt, outline consumer rights, and provide instructions for dispute. This reduces confusion and reinforces accountability.

- Prohibits Abusive or Deceptive Practices: The rule bans threats, false claims, and harassment. This safeguards both consumers and your brand reputation.

What This Means for You

By following the CFPB rule, your collections process becomes:

- Legally sound

- Customer-conscious

- Reputation-safe

When paired with financial management tools such as automated contact tracking, compliance logs, and proper documentation, businesses can maintain complete alignment without relying on manual oversight.

Forest Hill Management helps clients maintain CFPB compliance by embedding these protections directly into every step of the collection process.

How to Optimize Debt Collection Processes for Faster Recovery and Lower Risk

Efficient debt collection is crucial for maintaining healthy cash flow and minimizing resource strain. Here’s how to optimize your collection processes:

Steps to Improve Collection Efficiency

To improve collection efficiency, it’s essential to take proactive measures that address issues before they grow. Here are key strategies to implement:

- Early Intervention: Contact customers as soon as payments are overdue to avoid escalating issues. Early action increases the likelihood of successful recovery.

- Flexible Payment Options: Offer payment plans or alternative payment methods to facilitate more manageable repayment and encourage prompt action.

- Technology Solutions: Utilize automated systems and CRM tools to efficiently track payments, send reminders, and manage accounts, thereby reducing manual effort.

Handling Disputes Effectively

Resolving disputes quickly and fairly prevents legal complications and ensures smoother collection efforts:

- Acknowledge the Dispute: Respond promptly and professionally to the consumer’s concerns.

- Provide Clear Documentation: Ensure that all communications and agreements are documented for both parties.

- Offer Solutions: Collaborate with the consumer to find a mutually agreeable resolution, such as a payment extension or negotiated settlement.

By optimizing these strategies, businesses can enhance collection efficiency, resolve disputes effectively, and maintain a strong customer reputation. Now, let's dive deeper into how you can implement financial management tools to ensure smoother, more effective outcomes.

Financial Management Tools That Streamline Debt Collection

Technology is no longer optional in debt recovery; it’s essential. The right financial tools can reduce errors, speed up collections, and give your team better visibility into what’s working (and what’s not).

Here’s how these tools can benefit your collection strategy:

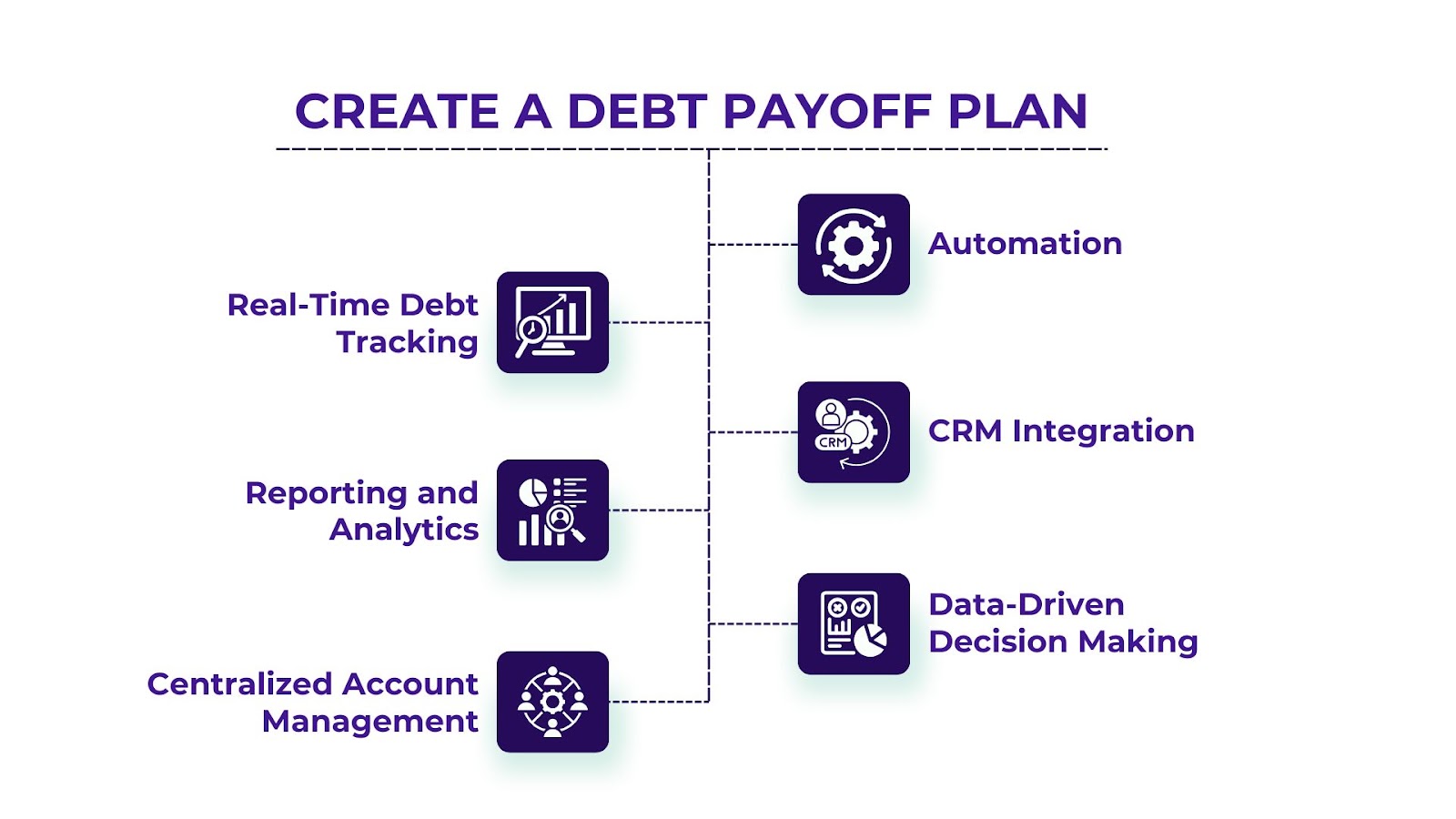

1. Real-Time Debt Tracking

Automated systems track overdue accounts and flag them in real time, allowing your team to act quickly and prioritize high-risk cases.

Why it matters: Faster visibility means faster action and fewer accounts falling through the cracks.

2. Reporting and Analytics

Modern tools generate detailed reports on receivables, aging accounts, and collector performance.

Why it matters: These insights enable you to fine-tune your outreach strategies and allocate resources more effectively.

3. Centralized Account Management

One dashboard gives your team a unified view of account history, payment status, and next steps.

Why it matters: It reduces manual errors, improves follow-ups, and keeps every team member aligned.

4. Automation

Set up automated reminders, payment confirmations, and recurring tasks to reduce admin time.

Why it matters: Automation accelerates the collection cycle, allowing your team to focus on high-value interactions.

5. CRM Integration

CRM tools record every customer touchpoint, from emails and phone calls to settlement offers, ensuring timely and consistent communication.

Why it matters: Keeps your process professional and prevents missed follow-ups or duplicate outreach.

6. Data-Driven Decision Making

Behavioral analytics help you predict which accounts are most at risk and when customers are most likely to respond to your offers.

Why it matters: You can tailor follow-ups and offers based on real patterns, not guesswork.

By embedding financial management tools into your collection workflow, you reduce overhead, increase consistency, and give your business the control it needs to recover debt without damaging relationships.

Complaint Resolution Processes That Build Trust

By ensuring customers have clear channels to voice their concerns, businesses can address issues promptly and resolve disputes effectively.

Here’s how to set up a clear complaint submission system:

- Clear Contact Information: Provide customers with easy access to contact details, whether by phone, email, or an online portal.

- Acknowledgement of Receipt: Ensure that complaints are acknowledged immediately, letting customers know their concerns are being taken seriously.

- Trackable Process: Develop a system that tracks the status of complaints, enabling both the business and the customer to view progress and outcomes.

- Listen Actively: Show genuine interest in the consumer’s concerns. Listening carefully builds rapport and can prevent escalation.

- Provide Clear Solutions: Offer reasonable and actionable solutions to resolve the complaint. Whether it’s a payment arrangement or an account adjustment, make sure the solution is fair to both parties.

- Follow-up: After resolving a complaint, follow up with the consumer to ensure their satisfaction and reinforce a positive relationship.

By implementing clear procedures and addressing complaints with empathy and fairness, businesses can enhance customer loyalty and maintain a strong reputation in the debt collection process.

Conclusion

A strong debt collection strategy improves repayment rates, customer retention, legal compliance, and your financial portfolio. By maintaining clear communication, utilizing practical tools, and respecting consumer rights, businesses can streamline debt recovery while preserving customer relationships.

As debt collection processes adapt to new regulations and market conditions, lenders must stay informed and flexible. This ensures long-term success and mitigates risks in a changing environment.

Looking to strengthen your collection strategy without compromising relationships?

The Forest Hill Management’s expert financial services help businesses recover more quickly, stay compliant, and mitigate risk; all while building long-term economic resilience.