Everything You Need to Know About Funded Debt: Meaning, Examples, and Benefits

Everything You Need to Know About Funded Debt: Meaning, Examples, and Benefits

Transform Your Financial Future

Contact UsFunded debt is a key element of corporate finance, yet it's often overlooked until companies find themselves struggling with long-term liabilities. At its core, funded debt refers to the money a company borrows that is due for repayment over a period longer than one year.

Unlike short-term debt, funded debt can have a profound impact on a company’s financial health, influencing everything from its ability to secure future loans to how it manages growth. Understanding the nuances of funded debt is crucial, especially when making decisions about financial planning, debt management, and business strategy.

This blog will unpack the meaning of funded debt, why it matters, and how it affects both businesses and investors, offering clear insights into an often misunderstood aspect of corporate finance.

Key Takeaways

- Funded Debt vs. Unfunded Debt: Funded debt refers to long-term financial obligations due over a period longer than one year. Unfunded debt is short-term debt used for operational needs with repayment due within one year.

- Tax Benefits: Interest paid on funded debt is typically tax-deductible, providing companies with a financial advantage by lowering their taxable income.

- Funded Debt-to-EBITDA Ratio: This ratio is essential for evaluating a company's ability to manage its long-term debt relative to its operating earnings. A higher ratio can indicate financial strain and increased risk.

- Predictability in Debt Payments: Funded debt allows businesses to plan with more certainty, as it typically involves fixed payment schedules for interest and principal, making it easier to manage cash flow.

- Retention of Ownership: Unlike equity financing, funded debt doesn’t require giving up a stake in the business, allowing owners to maintain control and keep profits within the company.

What is Funded Debt?

Funded debt refers to the money a company borrows that is due for repayment over a period longer than one year. Unlike short-term debt, which needs to be paid back within a year, funded debt includes long-term loans, bonds, and other forms of borrowing that the company must settle over an extended time.

These types of debts help companies finance large projects or expansions, and they’re typically recorded as long-term liabilities on the company’s balance sheet.

Examples of Funded Debt

Funded debt includes long-term financial obligations that companies or individuals must repay over a period longer than one year. Common examples of funded debt include:

- Bonds with Maturities Longer Than One Year: These are debt securities issued by a company that come due after a period exceeding one year, over several years, or even decades.

- Convertible Bonds: These are bonds that can be converted into company stock at a later date, usually under specific conditions.

- Debentures: Unsecured debt instruments, debentures are issued by companies as a way to raise capital, with repayment terms extending beyond one year.

- Long-Term Notes Payable: These are promissory notes that a company agrees to pay back over a long period, usually more than one year.

- Mortgages: Mortgages are loans taken out by businesses or individuals to buy property. The loan is repaid over a long period (usually 15 to 30 years) and is secured by the property itself. Mortgages are a classic example of funded debt due to their extended repayment terms.

Also Read: How to Recover from Debt: A Simple Step-by-Step Guide

While these examples illustrate what funded debt encompasses, the full picture emerges only when we contrast it with its short-term counterpart. The distinction between these two debts reveals how companies approach their financing strategies.

Funded Debt vs. Unfunded Debt: A Comparative Overview

Understanding the distinction between funded and unfunded debt is crucial for assessing a company's financial health and its ability to meet obligations. These two categories of debt differ primarily in their maturity periods and the purposes they serve.

In summary, the primary difference between funded and unfunded debt lies in their maturity periods and intended uses. Funded debt supports long-term investments and projects, providing stability and predictability in financing. Unfunded debt addresses short-term financial needs, offering flexibility but requiring careful management to mitigate associated risks.

Knowing the difference between debt types is one thing, but evaluating whether a company's debt level is sustainable requires specific metrics. Financial analysts rely on key ratios to determine if a company's long-term obligations are manageable given its earning power.

Understanding the Funded Debt-to-EBITDA Ratio

The Funded Debt-to-EBITDA ratio is a critical financial metric that evaluates a company's ability to meet its long-term debt obligations using its operating earnings. This ratio is particularly useful for investors, analysts, and lenders to assess financial leverage and the risk associated with a company's capital structure.

Formula: Funded Debt-to-EBITDA = Funded Debt / EBITDA

The Funded Debt-to-EBITDA ratio measures a company's ability to pay off its long-term debt using its operational earnings. It compares the total amount of funded debt (long-term debt) with the company's earnings before interest, taxes, depreciation, and amortization (EBITDA), which is a common indicator of a company's operational profitability.

A lower ratio indicates that the company can more easily manage its debt, while a higher ratio suggests that it may face challenges in servicing its debt, potentially signaling higher financial risk.

This ratio is often used by credit rating agencies and financial institutions to assess the creditworthiness of a company and its ability to meet long-term financial obligations.

Example:

Consider a company with $100 million in funded debt and an EBITDA of $25 million. The Funded Debt-to-EBITDA ratio would be:

100 million / 25 million = 4.0

This ratio suggests that it would take the company 4 years to repay its funded debt using its current operating earnings, assuming no changes in debt levels or earnings.

Beyond measuring debt sustainability, companies must also decide how to raise capital in the first place. The choice between borrowing and selling ownership stakes shapes not just the balance sheet, but the entire strategic direction of the business.

Funded Debt vs. Equity Funding: How Debt Financing Shapes Business Strategy and Control

When companies seek to raise capital, they often face the decision of whether to use debt financing or equity financing. Both options have their advantages and trade-offs, and understanding the role of funded debt within the broader context of corporate financing is key to making informed strategic decisions.

1. Debt Financing (Funded Debt)

Funded debt is a subset of debt financing that specifically refers to long-term borrowing obligations, such as bonds, long-term loans, and mortgages. Companies opt for debt financing when they want to raise capital without giving up ownership or control of the business.

However, the challenge of funded debt lies in the obligation to make regular debt payments, regardless of the company’s financial performance. If the company is unable to meet its debt obligations, it can face serious financial difficulties, including the risk of default. This is where the Funded Debt-to-EBITDA ratio can be a critical metric, as it measures the company’s ability to service its long-term debt using its earnings.

2. Equity Financing

In contrast, equity financing involves raising capital by selling shares of the company to investors. This gives investors a stake in the company, often with voting rights and a claim on the company’s profits through dividends. Unlike debt, equity financing does not require repayment, and the company is not burdened with interest expenses.

One of the key benefits of equity financing is that it does not add to the company’s debt load, which may be preferable for businesses with volatile cash flows or those seeking to avoid the risk of default.

Given this strategic choice between debt and equity, understanding why so many companies gravitate toward long-term borrowing becomes essential. The benefits extend beyond simple capital acquisition.

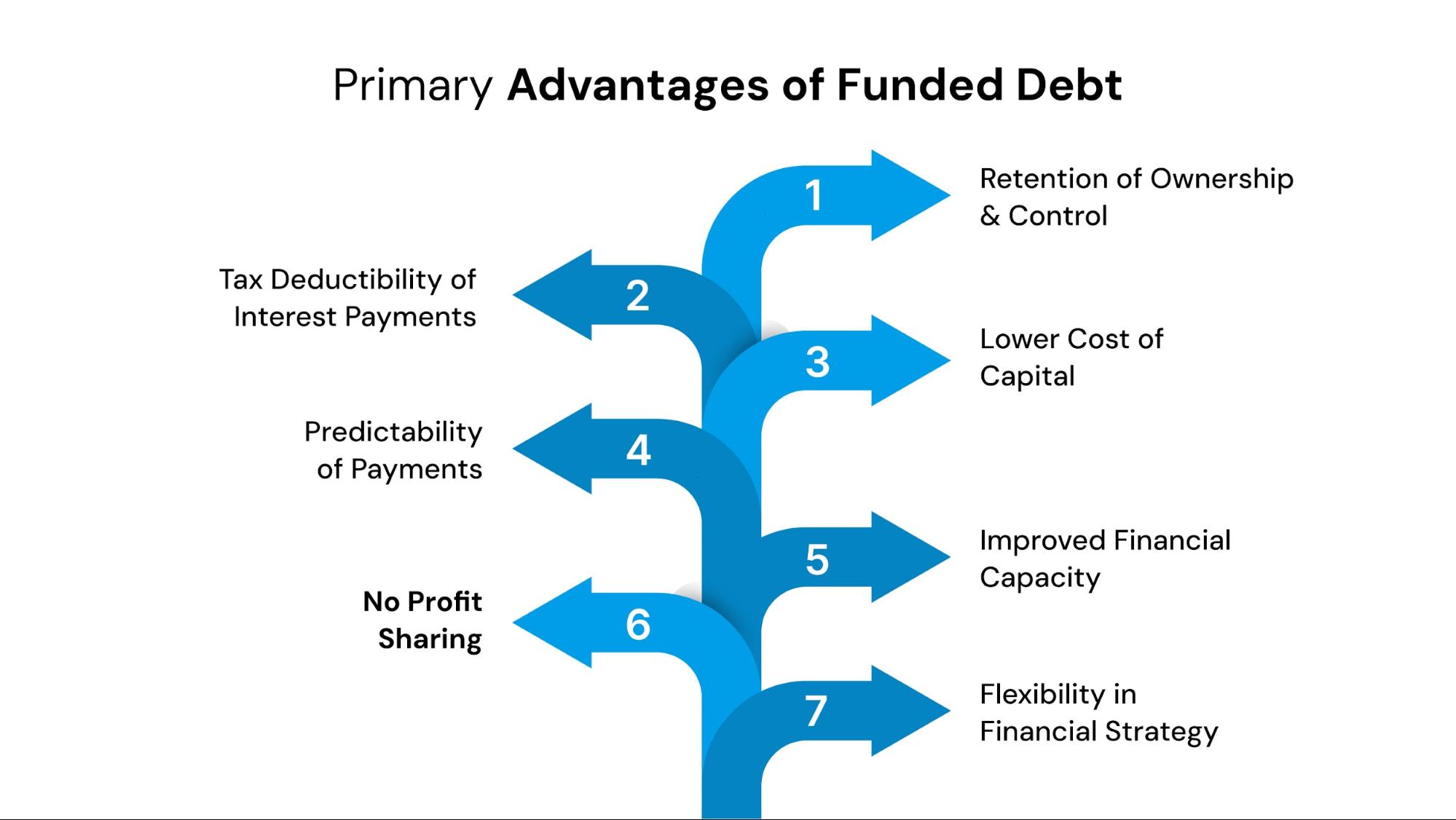

Advantages of Funded Debt

Funded debt offers several benefits to businesses, especially when compared to other financing options like equity financing. While it comes with certain risks, its advantages make it an attractive option for companies looking to raise capital.

1. Retention of Ownership and Control

One of the biggest advantages of funded debt is that it allows businesses to retain full control and ownership. Unlike equity financing, which requires the company to issue shares to investors and relinquish some control, funded debt doesn’t require giving up a stake in the company.

2. Tax Deductibility of Interest Payments

The interest payments made on funded debt are tax-deductible. This means that businesses can reduce their taxable income by the amount of interest paid on the debt, effectively lowering their tax liability.

3. Lower Cost of Capital

Generally, debt financing comes at a lower cost compared to equity financing. With funded debt, companies can access capital at fixed interest rates, which can often be more favorable than the returns expected by equity investors.

4. Predictability of Payments

Funded debt involves fixed payment schedules, including both interest and principal payments. This structure offers predictability, which can help businesses plan their finances and cash flow more effectively.

5. Improved Financial Capacity

By utilizing funded debt, businesses can increase their borrowing power, allowing them to undertake large-scale investments or expansions without depleting their own equity. This can lead to higher returns on equity for existing shareholders, as the company can generate profits from borrowed capital.

6. No Profit Sharing

Unlike equity financing, where businesses must share their profits with shareholders in the form of dividends, funded debt does not require any profit-sharing. Once the debt is repaid, the company retains all of its profits.

7. Flexibility in Financial Strategy

Funded debt gives companies the flexibility to choose the duration of their repayment terms, allowing them to match their financing structure with their financial goals and project timelines.

With a clear understanding of how funded debt works and why it serves as a powerful financial tool, the next step involves implementing these strategies effectively. Professional guidance can make the difference between simply managing debt and truly optimizing your financial structure.

Achieve Financial Stability with Forest Hill Management: Expert Debt Solutions and Advisory Services

Forest Hill Management specializes in providing personalized financial solutions tailored to meet your unique needs. Their team of experienced professionals is committed to delivering expert advice and support so that you can make informed decisions on your journey to financial stability.

Forest Hill Management offers a range of services to assist you in managing your finances effectively:

- Portfolio Management: Receive personalized strategies to manage and optimize your financial portfolio, helping you achieve your financial goals.

- Portfolio Acquisitions: Explore opportunities to acquire portfolios that can provide relief from delinquent accounts, offering a fresh start.

- Compliance & Technology: Benefit from advanced technology solutions and strict adherence to industry regulations, ensuring the security and confidentiality of your financial data.

- Flexible Payment Plans: Access generous and tailored payment plans designed to fit your financial situation, making it easier to manage your obligations.

- Expert Financial Advice: Consult with knowledgeable financial advisors who are dedicated to providing guidance and support every step of the way.

Conclusion

Understanding funded debt is essential for both businesses and investors to navigate the complexities of long-term financial obligations. By leveraging funded debt, companies can secure capital for major investments, expansions, and acquisitions, all while maintaining control over ownership and benefiting from tax advantages.

The Funded Debt-to-EBITDA ratio serves as a vital metric to assess a company’s ability to manage its debt relative to its operating earnings, providing insight into its financial health and stability.

While funded debt comes with its own set of risks, particularly the responsibility of meeting long-term repayment obligations, it remains a powerful tool for companies aiming to fuel growth and remain competitive in the market.

For companies looking to improve their financial management and make the most of their capital options, Forest Hill Management offers expert guidance and personalized financial strategies. Contact our advisors today to take the next step toward financial success.

FAQs

1. What is the difference between financed and funded?

"Financed" generally refers to the method of providing money for a project or purchase, often on a short-term basis. "Funded," however, specifically refers to providing long-term capital, often for larger-scale investments or obligations like debt repayment.

2. What happens when a loan is funded?

When a loan is funded, the lender disburses the approved amount of money to the borrower, who is then obligated to repay the loan over an agreed period, typically with interest.

3. Is debt funding a good idea?

Debt funding can be a good idea for businesses that need capital for expansion or projects, as it allows them to retain ownership. However, it comes with the responsibility of managing repayments and the risk of default if the business struggles financially.

4. Is a funded debt a debt?

Yes, funded debt is a type of debt, specifically long-term debt that companies borrow and are obligated to repay over a period longer than one year, typically through instruments like bonds, loans, or mortgages.

5. What is the difference between debt and a loan?

"Debt" is a broad term that refers to any amount of money borrowed, while a "loan" is a specific form of debt with agreed-upon terms like interest rates, repayment schedules, and a fixed amount borrowed.