Importance of Licensing for National Collection Agencies

Transform Your Financial Future

Contact UsLicensing is a crucial element for any national debt collection agency. It goes beyond meeting legal requirements; it allows an agency to operate across multiple states, building trust with both clients and consumers. Debt collection laws vary from state to state, and without the proper licenses, agencies face legal risks, reputational damage, and lost opportunities.

Understanding the complexities of obtaining and maintaining these licenses is key, as it helps agencies expand their reach and strengthen their credibility. This blog will dive into why licensing is more than a formality; it’s a vital part of running a successful, compliant debt collection business.

Key Takeaways

- Licensing Ensures Legal and Ethical Operations: Licensing is essential for debt collection agencies to comply with federal and state regulations like the FDCPA. It ensures fair practices and protects consumers from abuse.

- Non-Compliance Can Lead to Severe Consequences: Operating without proper licensing risks fines, penalties, and reputational damage. Agencies must adhere to regulations to avoid legal actions and maintain operational legitimacy.

- Transparency and Ethical Practices Are Key: Licensing fosters transparency by requiring debt collectors to disclose their terms, fees, and processes, which builds trust with both clients and debtors.

State-Specific Regulations Add Complexity: Each state has unique licensing requirements, and agencies must navigate these varying rules to avoid penalties. For example, states like California and Texas have their own specific guidelines. - Forest Hill Management’s Commitment to Compliance: Forest Hill Management prioritizes regulatory compliance with a focus on transparency, advanced technology, and personalized debt recovery solutions, ensuring ethical and efficient practices.

What Is a National Debt Collection Agency and Its Role in Debt Recovery

A national debt collection agency is a firm contracted by creditors, including banks, healthcare providers, and utility companies, to recover overdue or defaulted debts across multiple states.

Unlike in-house collections teams, these agencies operate under a federal and state-regulated framework, adhering to the Fair Debt Collection Practices Act (FDCPA) and other relevant laws.

Their core responsibilities encompass:

- Debt Recovery: Engaging with debtors to negotiate repayment plans or settlements, aiming to recover outstanding balances.

- Legal Compliance: Operating within the boundaries of federal and state regulations to ensure ethical collection practices.

- Communication Management: Utilizing various channels to contact debtors, including phone calls, letters, and digital platforms, while adhering to legal guidelines on communication.

- Credit Reporting: Reporting collected debts to credit bureaus, which can impact a debtor's credit score and creditworthiness.

National debt collection agencies serve as intermediaries that help creditors recover funds while maintaining compliance with legal standards and protecting debtor rights.

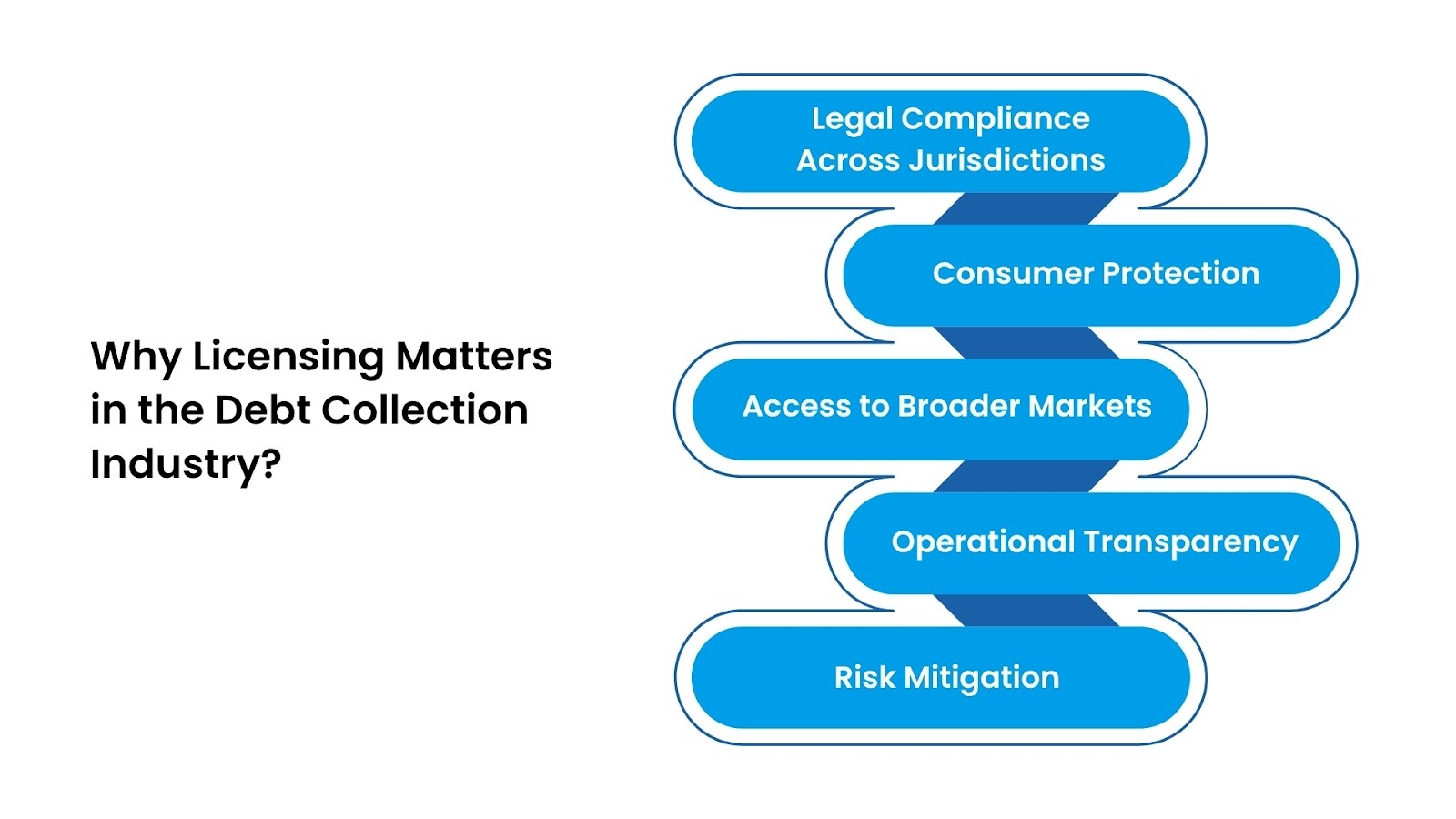

Why Licensing Matters in the Debt Collection Industry?

Licensing in the debt collection industry is not just a legal formality but a vital component of maintaining compliance, protecting consumers, and ensuring business operations are legitimate. Here’s why it’s crucial:

1. Legal Compliance Across Jurisdictions

In the U.S., each state has its own set of laws regulating debt collection practices. For example, in California, debt collectors must be licensed by the California Department of Business Oversight, while Texas requires agencies to register with the Texas Office of Consumer Credit Commissioner. Each jurisdiction has unique rules, application procedures, fees, and renewal timelines. Operating without the necessary licenses can lead to hefty fines, penalties, or legal actions.

2. Consumer Protection and Ethical Standards

State licensing ensures that debt collection agencies comply with consumer protection laws, such as the Fair Debt Collection Practices Act (FDCPA). In states like California, additional protections, like the Rosenthal Fair Debt Collection Practices Act, are in place to prevent abusive or deceptive practices. Licensing enforces ethical behavior so that debtors' rights are respected.

3. Access to Broader Markets

For agencies operating nationwide, state-specific licenses are critical to expand into multiple markets. A debt collection agency licensed in states like Florida, Illinois, and Ohio can legally manage debts across the country, providing services to clients in various industries. This national reach helps diversify revenue streams and improves the agency’s growth potential.

4. Operational Transparency and Trust

Licensing serves as a guarantee that a collection agency adheres to state laws and ethical guidelines. It builds trust with clients, as they can be confident the agency is operating transparently and in good faith. For instance, the New York State Department of Financial Services requires licensed debt collectors to outline their practices and fees, maintaining transparency.

5. Risk Mitigation

Without proper licensing, debt collectors risk facing lawsuits, hefty fines, or business shutdowns. For example, in Texas, unlicensed collection agencies can be fined up to $5,000 per violation. Obtaining and maintaining licenses in key states reduces these risks and assures the agency can legally collect debts without facing regulatory issues.

Understanding why licensing matters provides the foundation, but the real complexity lies in the specific regulations agencies must follow. The regulatory system forms a multi-layered system where federal mandates intersect with state-specific requirements.

What are the Regulatory Compliance and Legal Obligations in Debt Collection

Operating a debt collection agency in the United States necessitates strict adherence to both federal and state regulations. These laws are designed to protect consumers from unethical practices, and agencies can conduct their operations legally and transparently.

Let’s take a look at some of the Regulatory Bodies for Collection Agencies:

- Fair Debt Collection Practices Act (FDCPA): This federal law prohibits debt collectors from using abusive, unfair, or deceptive practices to collect debts. It also sets guidelines on communication, including restrictions on calling times.

- Telephone Consumer Protection Act (TCPA): Regulates the use of automated dialing systems, prerecorded voice messages, and unsolicited faxes. Debt collectors must obtain prior express consent before using these methods to contact consumers.

- Debt Collection Rule (Regulation F): Issued by the Consumer Financial Protection Bureau (CFPB), this rule provides detailed guidelines on communication practices, including the use of limited-content messages and restrictions on contact frequency.

- State Licensing Requirements: Each state has its own licensing requirements for debt collection agencies.

- California: License Required: Yes, Bond Required ($25K–$50K), Must apply via DFPI.

- New York (City): License Required: Yes, No Bond Required, DCWP license required

- Massachusetts: License Required: Yes, $5,000 Bond Required; Out-of-state agencies must license if collecting from MA residents.

- Texas: License Required: Yes, $10,000 Bond Required, Requires registration with the Secretary of State

- Illinois: License and Bond Required: Yes, Must register with IDFPR

- Florida: License Required: Yes (local level), Bond Requirement varies, Counties may require local business licenses and tax registrations.

- Operational Requirements: Some states have specific operational mandates, such as maintaining a physical office, designating a qualified individual to manage operations, and submitting regular financial reports.

What are the Consequences of Non-Compliance?

Failure to comply with these regulations can result in severe legal and financial repercussions:

- Civil Liability: Consumers can sue for actual damages, statutory damages up to $1,000 per violation, and attorney's fees.

- Federal Penalties: Under the FDCPA, violations are considered unfair or deceptive practices, allowing the Federal Trade Commission (FTC) to impose civil fines exceeding $50,000 per violation.

- State-Level Fines: For instance, New York City imposes fines ranging from $525 to $3,500 for violations such as harassment, false representations, or failure to comply with communication requirements.

- Reputational Damage: Non-compliance can lead to loss of business licenses, operational disruptions, and diminished consumer trust.

Beyond avoiding penalties, licensing serves a more fundamental purpose in shaping how agencies interact with consumers.

The ethical foundation that licensing establishes directly translates into tangible business advantages. In an industry often viewed with skepticism, showing legitimacy through proper licensing becomes a powerful differentiator.

How Licensing Enhances Agency Reputation

Licensing is a cornerstone of trust and credibility in the debt collection industry. Here's how it boosts an agency's reputation:

- Demonstrates Legal Compliance: Holding licenses in multiple states signifies adherence to both federal and state regulations, such as the Fair Debt Collection Practices Act (FDCPA) and state-specific laws. This commitment to legality reassures clients and consumers alike.

- Builds Consumer Trust: Consumers are more likely to engage with agencies that are licensed, as it indicates a commitment to ethical practices and consumer protection. This trust is vital in encouraging cooperation and timely debt resolution.

- Market Reach: Licensing in multiple states allows agencies to operate across a broader geographic area, increasing their marketability and potential client base. This expansion can lead to increased business opportunities and revenue streams.

- Trust-building with Clients and Consumers: Licensing assures both clients and consumers that the debt collection agency adheres to industry regulations. For consumers, knowing that an agency is licensed means they are protected from harassment and unfair treatment. For clients, it signifies that the agency is professional, compliant, and capable of handling collections legally.

- The Impact of Licensing on Business Relationships: Licensing opens doors to partnerships with larger clients, including banks, healthcare providers, and other industries that require reliable and compliant debt collection services.

Reputation benefits represent just one dimension of licensing's value proposition. The operational and financial implications of maintaining proper licenses create efficiencies that many agencies underestimate when calculating the true cost-benefit of compliance.

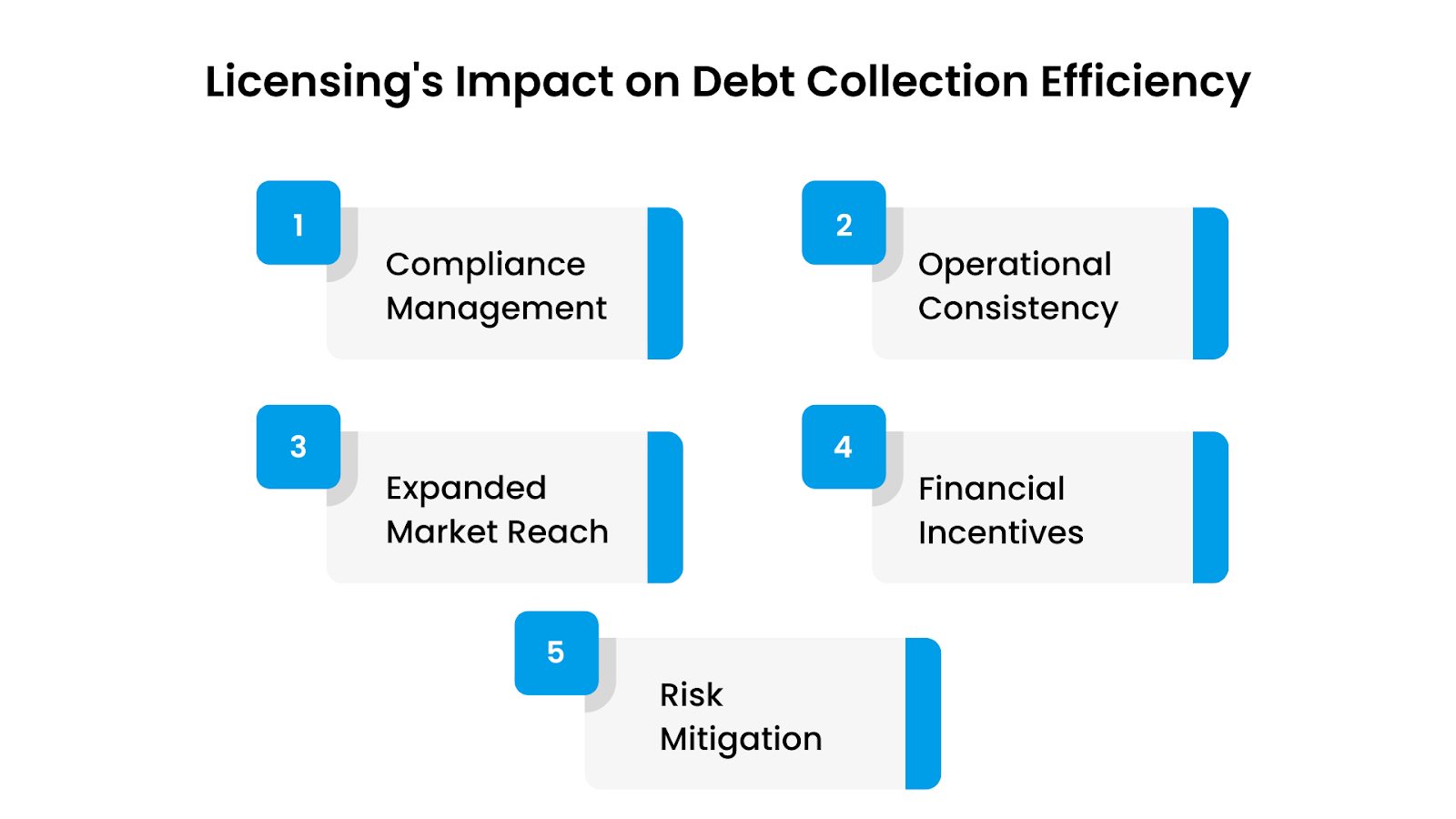

How Licensing Drives Operational Efficiency and Financial Benefits in Debt Collection

Licensing is not just about legal compliance; it also plays a pivotal role in improving the operational efficiency and financial stability of debt collection agencies

- Streamlined Compliance Management: Licensing standardizes compliance across jurisdictions, reducing administrative overhead and ensuring adherence to state-specific regulations.

- Enhanced Operational Consistency: Agencies licensed in multiple states can unify training programs and operational procedures, leading to more efficient workflows and reduced complexity.

- Expanded Market Reach: Nationwide licensing opens access to a broader client base, including national banks and healthcare providers, thereby increasing business opportunities.

- Financial Incentives: Licensed agencies may qualify for performance-based contracts and are less likely to face penalties, leading to improved profitability.

- Risk Mitigation: Adherence to licensing requirements helps avoid legal challenges and potential fines, protecting the agency's financial stability.

While licensing provides clear benefits, obtaining and maintaining credentials across multiple jurisdictions presents its own set of obstacles. The debt collection industry faces numerous challenges that extend beyond regulatory compliance alone.

What are the Challenges Faced by National Debt Collection Agencies?

With the dynamic and often complex web of state and municipal licensing requirements, agencies must remain vigilant to ensure compliance and functionality across various jurisdictions.

- Regulatory Changes: Debt collection agencies operate within a constantly evolving regulatory framework. Keeping up with shifting laws and requirements is important to avoid penalties. Agencies must stay informed about federal and state regulations, such as the FDCPA, TCPA, and state-specific licensing rules.

- Technological Advancements: With the rise of automation, artificial intelligence (AI), and machine learning, debt collection is becoming more efficient. However, agencies face the challenge of integrating these technologies to manage large volumes of data and improve debtor communication while minimizing errors.

- Securing Sensitive Data: With rising cyber threats, maintaining data security is non-negotiable. Agencies must employ encryption technologies, secure communication channels, and comply with data protection regulations like GDPR and CCPA.

- Adapting to Economic Fluctuations: Economic downturns or recessions can significantly affect the ability of debtors to repay. National collection agencies must adapt to these changes by offering flexible repayment solutions and working closely with debtors in financial distress.

- Staffing and Employee Retention: The debt collection industry is facing high turnover rates, driven by the stress and emotional toll of the job. Agencies struggle to retain experienced personnel, which can impact efficiency and consistency.

Successfully managing these challenges requires expertise, technology, and an unwavering commitment to compliance. Organizations that prioritize regulatory excellence while maintaining operational efficiency set themselves apart in a competitive field.

Forest Hill Management: A Trusted Partner in Debt Collection Services

Forest Hill Management is a reputable receivables management organization specializing in the management of past-due accounts. With a history dating back to 2020, the company has assisted thousands of consumers in resolving their financial obligations. Their mission is to help individuals achieve financial freedom and move forward confidently in their lives.

Services Offered:

- Portfolio Management: Tailored strategies to help clients effectively manage outstanding financial obligations and achieve financial freedom.

- Portfolio Acquisitions: Seamless and efficient process for acquiring portfolios, conducting thorough due diligence to identify portfolios that align with clients' goals and objectives.

- Compliance & Technology: Commitment to upholding the highest standards of industry compliance while leveraging cutting-edge technology to enhance efficiency and security.

- Flexible Payment Plans: Customized repayment options to accommodate clients' financial situations

- Secure Online Payments: A user-friendly platform for clients to make payments conveniently and safely.

Conclusion

Licensing is a vital component for national debt collection agencies, providing a legal framework that ensures compliance with state and federal regulations. It’s not just about meeting legal obligations; licensing protects both consumers and agencies by enforcing ethical practices, transparency, and accountability.

Debt collection agencies, like Forest Hill Management, understand the complexities of compliance and are dedicated to upholding these standards while offering tailored debt collection services. Contact our advisors today for personalized support and guidance.

FAQs

1. Can you start your own debt collection agency?

Yes, you can start your own debt collection agency, but it requires obtaining the necessary licenses, meeting state and federal regulations, and ensuring compliance with laws like the FDCPA to operate legally and ethically.

2. Can I ignore a debt collection agency?

Ignoring a debt collection agency can lead to serious consequences, including legal action, wage garnishment, and damage to your credit score. It’s better to communicate and resolve the debt as soon as possible.

3. How profitable is a debt collection agency?

Debt collection agencies can be highly profitable, especially if they manage large portfolios of delinquent debts. Profitability depends on factors like the volume of debt, successful recoveries, and the agency’s fee structure.

4. Can you dispute a debt if it was sold to a collection agency?

Yes, you can dispute a debt even if it has been sold to a collection agency. You are entitled to request validation of the debt and challenge its legitimacy within 30 days of receiving the collection notice.

5. How long before a debt is uncollectible?

In most cases, a debt becomes uncollectible after seven years due to the statute of limitations. However, this period can vary by state and the type of debt, so it’s important to check local laws.