Is Paying Debt Collection Agencies a Bad Idea?

Transform Your Financial Future

Contact UsGetting a call or letter from a debt collection agency can be scary. Unpaid debts handed over to collectors can leave you worried about your finances, your credit, and your next steps. Questions like Is debt collection bad may weigh heavily on your mind, especially when you're unsure about what actions will actually protect your financial health. Also, dealing with debt collectors often feels confusing and stressful.

You might be worried about being sued, receiving numerous phone calls, or further damaging your credit. But if you take the right steps and know what to look out for, you can regain control of your finances. Let's understand what happens when debt goes to collections with real tips to handle the situation.

Key Takeaways

- Debt collection impact varies by debt type, size, and reporting; medical and small debts are often less harmful.

- Ignoring collections can increase debt, lead to aggressive collection efforts, credit damage, and lawsuits.

- Evaluate your debt carefully, consider the size, account activity, statute limits, and verify the debt before paying.

- You have alternatives like debt management, consolidation, settlement, and legal protections under FDCPA and FCRA.

- Professional services like Forest Hill Management provide expert guidance, negotiation help, and protect your rights and data.

What happens when your debt is sent to a collection agency?

When your debt is sent to a collection agency, it means your original creditor has given up on collecting the payment directly and passed the responsibility to a third party. Usually, this happens after you miss payments for several months, typically between 60 to 120 days. The collection agency then takes over to recover the unpaid amount.

Here's what typically happens next:

- The agency buys or is assigned your debt, often at a discounted rate, and aims to collect the full balance from you to earn its fee.

- They will contact you through phone calls, letters, or emails to confirm the debt details and try to arrange repayment.

- The agency may ask for a lump sum payment or offer you a payment plan or settlement option, depending on your financial situation.

- Your credit report usually reflects that the debt is in collections, which can lower your credit score. The impact varies by debt type and reporting policies.

- If you ignore the collection attempts, the debt can increase with added fees and interest, and collectors may escalate their efforts, sometimes leading to legal action.

Understanding this process is crucial to making informed decisions. Rather than reacting out of fear, knowing what to expect helps you negotiate wisely and protect your financial future.

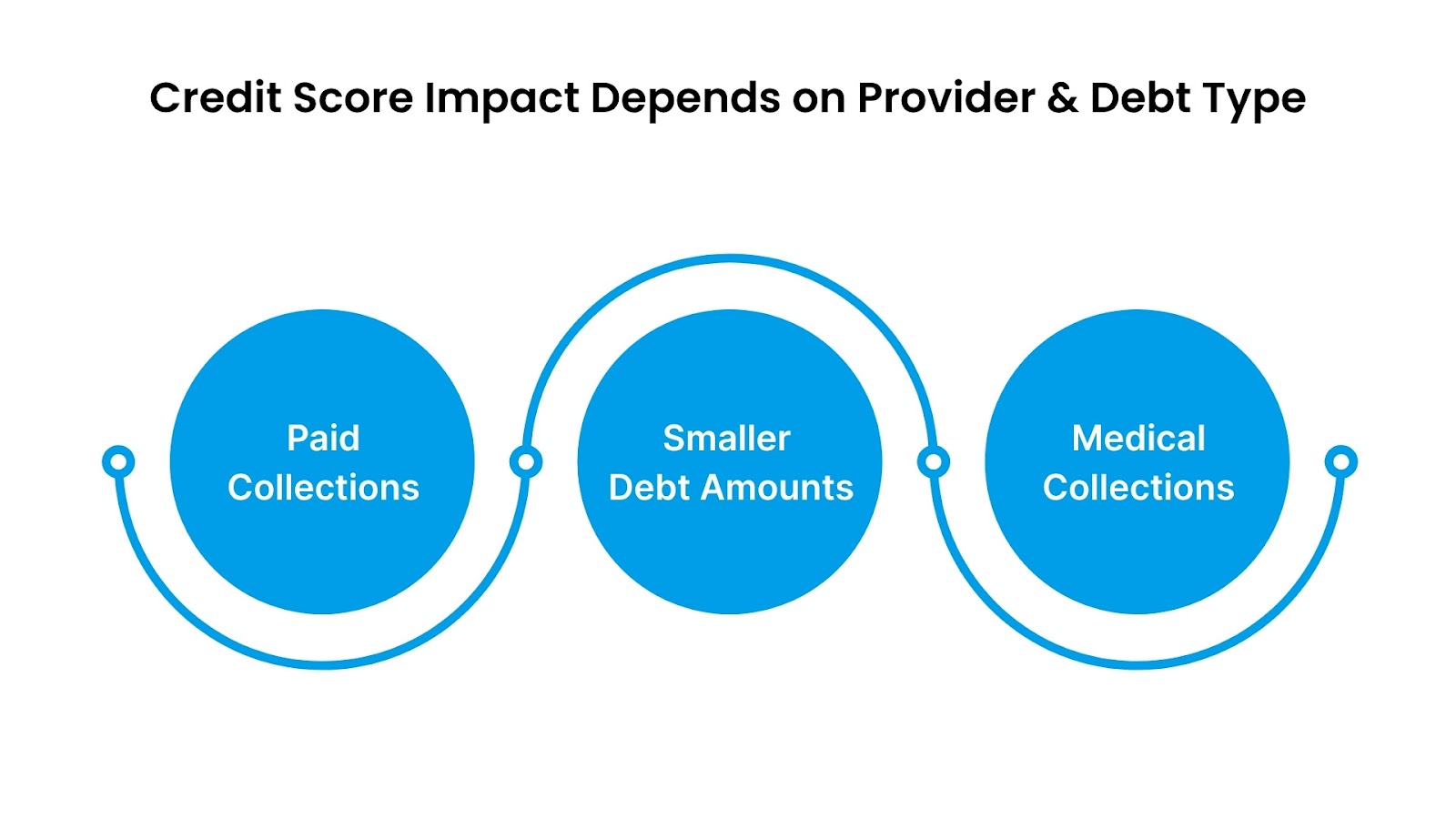

Effect on Credit Scores Depends on Provider and Debt Type

When debt is sent to a collection agency, its impact on your credit score is not the same across all situations. Several key factors come into play, including the type of debt, its size, and how credit bureaus and collection agencies report the information.

- Paid Collections: Paying a collection debt often lessens its negative impact, but the record may stay on your credit report up to seven years. Paid medical collections are frequently removed sooner, speeding credit recovery.

- Smaller Debt Amounts: Debts under $500, particularly medical ones, usually don’t affect your credit score because credit bureaus exclude them, preventing unnecessary damage.

- Medical Collections: Medical providers don't report unpaid bills directly; after 60–120 days, debts may be sent to collections. Credit bureaus delay reporting medical collections for one year, allowing time to resolve disputes.

Ignoring collections can worsen your financial situation. Before thinking "Is debt collection bad?", it's crucial to understand the serious consequences of unpaid debts.

What are the consequences of not paying a collection agency?

Failing to pay a collection agency is far more than just ignoring a bill; it sets off a series of financial problems that can follow you for years. Understanding these specific outcomes helps you make choices that protect your long-term financial health.

1. Your Debt Will Continue to Grow

When an account remains unpaid, collection agencies typically continue to add interest, late charges, and other fees to your balance. Even a relatively small debt can grow into an overwhelming amount, making eventual repayment more challenging and adding stress to your budget.

2. Debt Collector May Ramp Up Collection Efforts

Debt collectors have the legal right to contact you repeatedly in their efforts to recover what's owed. You may receive numerous calls, letters, texts, and sometimes even social media messages. These attempts can become stressful and difficult to avoid, and though there are laws protecting you from harassment.

3. Your Credit May Take a Hit

Unpaid debts sent to collections are reported to credit bureaus, which often results in a significant drop in your credit score. This decline not only affects your ability to qualify for new credit cards or loans but can also impact major life events, such as renting an apartment, obtaining a mortgage, or securing a job in certain industries.

4. You Could Be Sued in Court

If standard collection efforts do not yield payment, the agency may decide to take legal action. A court judgment against you can result in consequences such as wage garnishment (where a portion of your paycheck is withheld), freezing your bank account, or placing a lien on your property.

Now, let's review key factors that help you weigh your options and see when paying might or might not be the best choice.

Factors to consider before deciding whether to pay a collection agency

When a collection agency contacts you, making the right decision is crucial for your financial well-being. Answering the question Is debt collection bad depends on several important factors. Rushing to pay without considering these details may not always be in your best interest.

Take time to review these key points before moving forward.

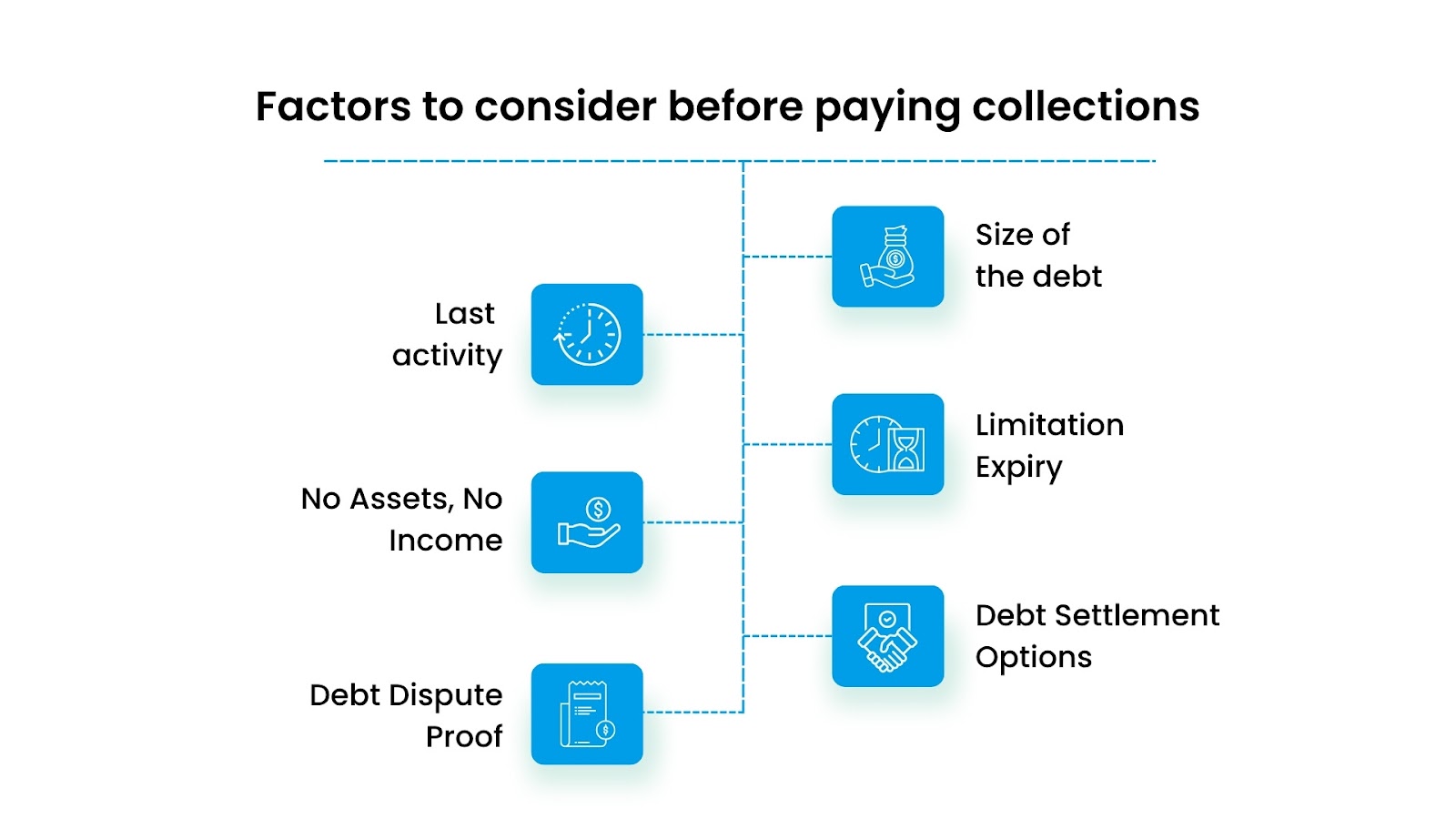

1. Size of the debt

Start by looking at how much you owe. If the balance is substantial, it’s wise to understand all your options and the potential impact of payment or non-payment. Large debts may require legal advice or negotiation, while minor amounts might be settled quickly without major consequences to your credit.

2. Date of your last account activity

Every action on your account starts a new timeline, affecting when a collection agency can take legal action. If it’s been a long time since you made a payment or contacted the creditor, the debt may be nearing or past its statute of limitations, limiting the collector’s ability to sue.

3. Statute of limitations expiry date

Each state has different rules on how long agencies can sue you for a debt. If the debt is "time-barred," you are not legally required to pay, and it may not be worth settling unless you want to clear your credit history. Confirm the statute of limitations for your type of debt and your state.

4. You own no assets and have no income

If you have no assets or income, you may be what's called "judgment proof." Even if a collection agency sues and wins, it may not be able to collect from you. But, unpaid collections can still cause stress and credit damage, so weigh your options carefully.

5. You have options for debt settlement

There are often alternatives to paying the full balance. Debt settlement, where you negotiate to pay less than owed, or payment plans set up with the agency, can sometimes resolve the issue for a fraction of the initial amount. Always get agreements in writing to avoid misunderstandings.

6. The collection agency can't prove you owe the debt

Agencies must be able to validate the debt before you pay. If they can't provide documentation proving you owe the money, you have the right to dispute the debt. Respond in writing and request verification; never pay a debt you're unsure about.

Evaluating your debt from every angle ensures you make informed decisions to protect your finances. Let's examine the other ways to deal with debt.

Other Ways to Deal With Debt Sent to a Collection Agency

If paying the full amount owed to a collection agency isn't an option right now, don't worry, there are other paths to manage your debt responsibly. Understanding these alternatives can help you regain financial control without making hasty decisions.

Here are some effective options to consider:

Debt management plan

A DMP partners with a credit counseling agency to negotiate lower interest rates and fees, combining debts into one monthly payment. It doesn’t involve new credit and usually lasts 3 to 5 years, offering structured support to pay off debt steadily.

Debt consolidation

This merges multiple debts into a single loan with one payment, often at a lower interest rate. It simplifies repayment but typically requires good credit to qualify and suits those who can handle a new loan.

Debt settlement

Negotiating to pay less than owed, usually via lump sum or partial payments. It can resolve debt faster, but often harms credit more than DMP or consolidation, so expert guidance is recommended.

Bankruptcy

A legal process to eliminate or reorganize debt when it becomes unmanageable. It stops most collection efforts but has long-term negative effects on credit and should be a last resort after other options are considered.

Knowing the right option helps you avoid unnecessary risks and take steps toward regaining financial stability. Now, let’s follow these six steps to negotiate confidently and turn a difficult situation into an opportunity.

5 Steps for Negotiating With Debt Collection Agencies

Negotiating with a debt collection agency can feel intimidating, but having a clear plan makes the process easier and helps protect your financial well-being. Here are six key steps to guide you through negotiating effectively and confidently:

1. Learn About the Debt

Request a written validation of the debt; this ensures the collector has the right information and that you fully understand the total balance, including any fees or interest. Knowing these details positions you to negotiate and avoid overpayment or scams.

2. Understand What You Can Afford To Offer

Debt collectors often prefer some payment over none, and a well-prepared offer shows your willingness to resolve the debt responsibly without overextending yourself.

- Payment Plans: Propose manageable installments that fit your income while covering other essential expenses.

- Partial Payments: Sometimes collectors accept less than the full balance if paid upfront or in a lump sum.

3. Speak to the Debt Collector

Express your intention to resolve the debt, but also share your financial constraints honestly. Ask questions and listen carefully to the collector’s terms. Communicate and focus on reaching a mutually acceptable agreement.

4. Make Your Payments

After agreeing on the terms, stick strictly to the payment schedule. Timely payments build trust and prevent further collection activity or legal actions. Keep records of all transactions and receipts for your reference.

5. Negotiate Improvement to Your Credit Reports

Request that the collection agency update your credit report to reflect the payment. Some collectors may agree to remove the collection account entirely (“pay for delete”), improving your credit score.

Let's understand the rights afforded by laws such as the FDCPA and FCRA and how they facilitate safe debt collection.

What Are Your Rights and Protections?

When your debt is in collections, understanding your rights can protect you from unfair treatment and help you manage the situation with confidence. Several important laws ensure that debt collectors follow rules and do not abuse their power.

What is The Fair Debt Collection Practices Act (FDCPA)?

The FDCPA is a federal law created to protect you from abusive and unfair practices by third-party debt collectors. It restricts how, when, and where collectors can contact you and outlines your rights during debt collection.

Key protections include:

- Limits on Communication: Collectors can only contact you between 8 a.m. and 9 p.m. They cannot call at odd hours, repeatedly call you at work if your employer forbids it, nor contact you at inappropriate places.

- Stop Contact Requests: You have the right to request in writing that a collector stop contacting you. Once they receive this request, the collector can only contact you to notify you about legal action or other important information.

- No Harassment: Collectors cannot harass, threaten, or abuse you, or use obscene language. They may not call repeatedly or try to embarrass you publicly.

- Social Media and Electronic Communications: Collectors cannot publicly post about your debt or contact you through social media. Any electronic contact must comply with FDCPA rules.

- Attorney Representation: You have the right to have a lawyer represent you. If an attorney is handling the debt, the collector must communicate with your lawyer, not directly with you.

What is The Fair Credit Reporting Act?

The Fair Credit Reporting Act (FCRA) protects your rights related to credit reporting. It ensures that credit reporting agencies provide accurate and fair information. If debts in collections appear on your credit report, the FCRA allows you to:

- Request a free copy of your credit report annually.

- Dispute inaccurate or incomplete information on your report.

- Have errors corrected within 30 days once disputed.

- Know how long negative information, like collection accounts, can stay on your report (usually seven years).

This act helps you maintain fairness and accuracy in your credit history.

Common Methods of Debt Collection Fraud

Unfortunately, scammers often misuse debt collection to trick people. Being aware of common fraud types can protect you:

- Debt Settlement Scams: Promises to erase debt for an upfront fee, but fail to deliver. Legitimate companies do not ask for large fees before services are provided.

- Fake Lawsuits or Arrest Claims: Scammers may threaten fake lawsuits or even arrests to scare you. Remember, debt collection does not involve criminal charges.

- Phony Debt Collectors: Fraudsters impersonate collectors and demand immediate payment, often using unusual payment methods like gift cards or wire transfers.

Warning Signs of Fraud

- Pressure to pay immediately without validating the debt.

- Requests for unusual payment methods.

- Threats of police action or lawsuits without proper documentation.

- Lack of company contact information or refusal to provide debt verification.

Ways to Avoid Debt Collection Fraud

- Always ask for written validation of the debt before making any payments.

- Verify the collector’s identity and contact information independently.

- Never pay without reviewing your rights and the legitimacy of the claim.

- Report suspicious activity to the Consumer Financial Protection Bureau (CFPB) or your state attorney general.

This knowledge is essential for evaluating whether debt collection is detrimental to you and how to respond safely and effectively.

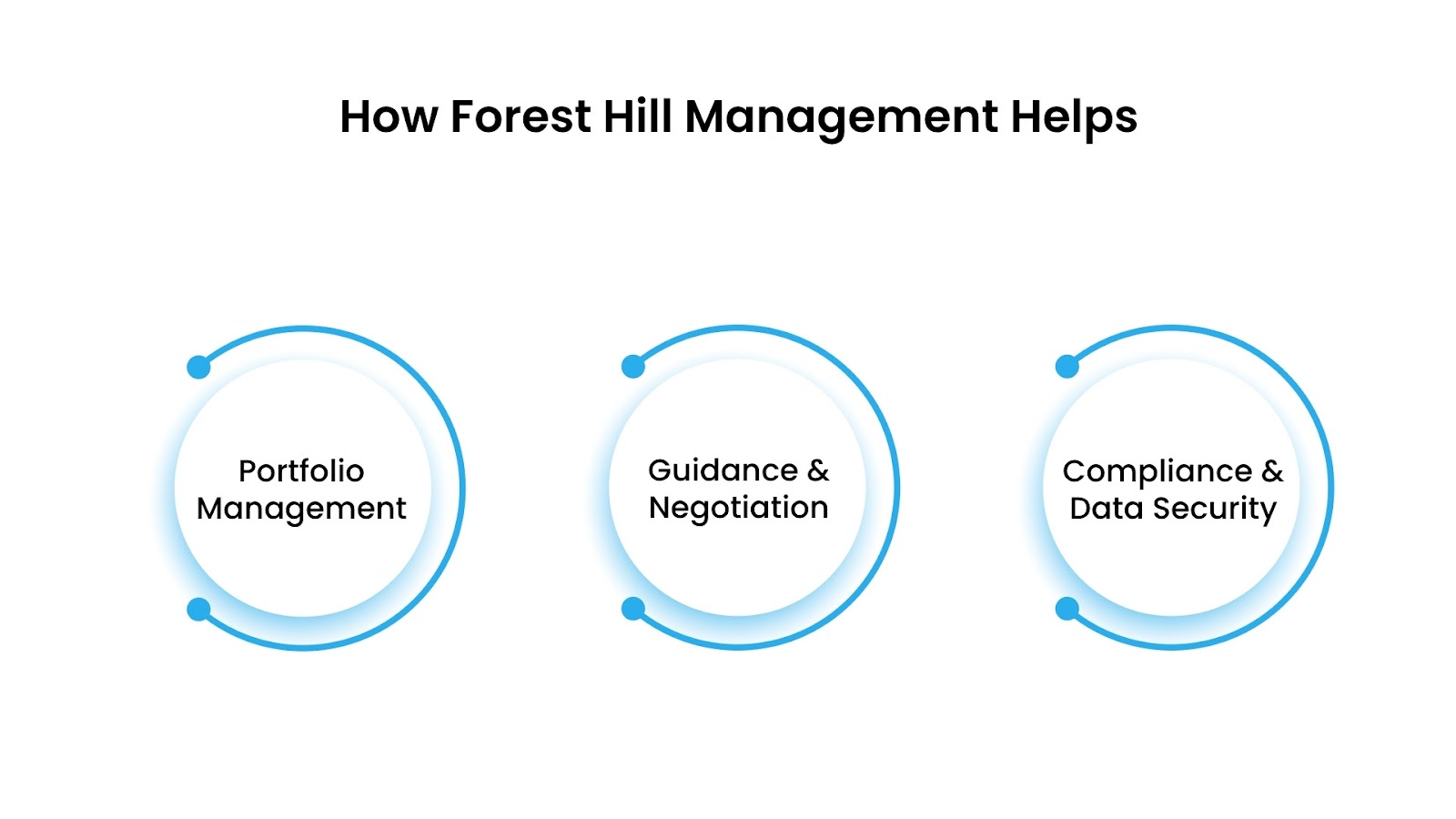

How The Forest Hill Management Services Can Help

The Forest Hill Management is a trusted expert in financial management with over 20 years of experience helping individuals and businesses regain control of their finances. They provide tailored, strategic solutions designed to ease your financial burden and promote long-term stability.

- Portfolio Management: Their team creates personalized repayment plans that fit your financial situation, helping to reduce your debt burden while easing stress.

- Expert Guidance and Negotiation: Forest Hill Management ensures you fully understand your debts and assists in negotiating fair payment terms.

- Compliance and Data Security: With advanced technology and strict adherence to legal standards, they safeguard your financial information and ensure all actions are compliant and ethical.

Learn how The Forest Hill Management supports you in navigating debt payments and reclaiming financial stability.

Conclusion

Not every collection situation harms your credit the same way, and not every debt must be paid immediately or in full. By carefully evaluating your debts, communicating strategically with collectors, and exploring alternatives like debt management or settlement, you can protect your financial health and rebuild your credit. Working with experienced partners such as Forest Hill Management can further ease this process, providing tailored solutions and expert guidance.

FAQs

1. Is debt collection serious?

Yes, debt collection is serious because it indicates your creditor has turned your account over to a third party. This can affect your credit score, lead to persistent collection efforts, or even legal action. Understanding your rights helps you manage this challenge effectively.

2. Is it bad to let debt go to collections?

Letting debt go to collections often harms your credit and can increase your balance due to fees and interest. "Is debt collection bad?" depends on your situation; ignoring collections usually worsens financial outcomes, so addressing debt proactively is better.

3. What happens if I ignore debt collectors?

Ignoring debt collectors doesn’t erase the debt; it can grow larger and lead to aggressive collection attempts or lawsuits. This worsens your credit and may result in wage garnishment or liens, making it critical to respond and verify any collection notices.

4. Is it bad to settle with a debt collector?

Settling with a debt collector isn’t necessarily bad; it can resolve debt faster by paying less than owed. Although it may affect credit scores, careful negotiation and written agreements can make settlement a sensible option when full repayment isn’t possible.