How To Pay Debt in Credit Collection Services

Transform Your Financial Future

Contact UsIf you've fallen behind on payments and your debt has landed in collections, your financial situation is spiraling out of control. The constant calls, letters, and looming threats of legal action can be overwhelming. However, understanding how the process works and taking the proper steps to resolve the debt can help you regain control.

By following a clear and structured approach, you can manage your debt, negotiate settlements, and work toward financial stability. To better understand this, it's beneficial to examine the following essential steps for effectively paying off your debt through credit collection services.

TL;DR (Key Takeaways)

- Verify Debt Ownership: Before making any payments, confirm that the debt is truly yours by requesting written proof and cross-checking with your records.

- Know Your Rights: Familiarize yourself with consumer protection laws like the FDCPA to avoid harassment and ensure fair treatment from debt collectors.

- Negotiate Smartly: Debt collectors may agree to a settlement or flexible payment plan; start with a lower offer and get all agreements in writing.

- Impact on Credit: Having debt in collections can severely damage your credit, but paying off the debt or negotiating settlements can improve your credit standing over time.

Step 1: Confirm the Debt is Yours

Mistakes happen, and sometimes debts are sold or transferred to the wrong person. If the debt is not yours or the information is incorrect, you should not be held responsible.

How to confirm

- Request Verification: Under the Fair Debt Collection Practices Act (FDCPA), you have the right to ask the collection agency for written proof of the debt. This includes the amount owed and the name of the original creditor.

- Check Your Records: Cross-reference the debt details with your personal records, including account statements, credit reports, and payment history, to verify that the debt is indeed yours.

Taking these steps will prevent you from paying for something you don't owe, and if an error occurs, you can address it before it escalates further.

Step 2: Know Your Debt Collection Rights

The FDCPA protects consumers from harassment and outlines the actions that debt collectors can and cannot take. Knowing these rights will help you avoid being bullied or misled during the process.

Key rights to know

- Right to Dispute the Debt: If you believe the debt is incorrect or you're unable to pay, you can dispute it within 30 days of receiving the notice from the collector.

- No Harassment: Debt collectors cannot contact you at unreasonable hours, use abusive language, or threaten you with violence or imprisonment.

- Right to Stop Communication: If you don't want to be contacted by the collector, you can send a written request for them to cease communication.

By understanding and asserting your rights, you can navigate the collections process with confidence, free from fear of mistreatment or unfair practices.

Step 3: Check the Statute of Limitations

Each state has a statute of limitations that determines the maximum time a debt can be legally collected. If the debt is older than the statute of limitations in your state, the creditor or collector cannot legally sue you for the debt, though they may still attempt to collect it.

How to check

- Know Your State's Laws: Research the statute of limitations for debt in your state, as it varies by state and type of debt.

- Verify Debt Age: If the debt is close to or past the statute of limitations, consult a legal expert to ensure your rights are protected before making any payments.

Understanding the statute of limitations helps you avoid paying for old debts that are no longer legally enforceable.

Step 4: Determine Collectability

Before agreeing to any payments, it's essential to assess whether the debt is collectible. This involves determining whether the collection agency is likely to collect the full amount or if there is any potential for negotiating a reduced settlement.

Key factors to consider

- The Debt Amount: Is the debt large or small? Smaller debts may be easier to settle for less than the full amount.

- Your Financial Situation: Can you afford to pay the full amount, or will you need to negotiate a reduced payment?

- Collection Agency's Track Record: Some agencies are more willing to settle debts than others. Research the collector's reputation to understand your options and make informed decisions.

Knowing whether the debt is collectible helps you make informed decisions about how to handle the situation.

Step 5: Figure Out How Much You Can Pay

One of the most important steps is figuring out how much you can realistically afford to pay. Struggling with debt is difficult, but taking a careful look at your finances will help you avoid taking on more than you can handle.

How to calculate

- List Your Income and Expenses: Determine how much you're earning versus how much you're spending on necessities.

- Set a Realistic Budget: Based on your disposable income, calculate how much you can afford to pay toward the debt each month.

- Factor in Other Obligations: Consider any other existing debts or essential expenses that you need to pay to maintain financial stability.

Once you have a clear picture of your finances, you can determine the most suitable payment amount.

Step 6: Negotiate a Settlement with the Collector

In many cases, collectors may be willing to settle the debt for less than the full amount. If you're unable to pay the full balance, negotiating a settlement can provide a mutually beneficial solution.

Tips for negotiating

- Start Low: Offer a lower amount initially, as collectors often expect some back-and-forth.

- Explain Your Situation: Be transparent about your financial challenges and explain why you can't afford to pay the full amount.

- Get It in Writing: Always request written confirmation of the settlement agreement, including the amount and payment terms.

Negotiating a settlement can reduce your financial burden, helping you pay off the debt more affordably.

Step 7: Set Up a Repayment Plan

If a settlement isn't possible or you prefer to pay off the debt over time, negotiating a repayment plan is another option. Many debt collectors are open to setting up payment plans that fit within your budget.

How to set up

- Determine Payment Terms: Collaborate with the collector to establish the payment amount and frequency (e.g., monthly or weekly).

- Stick to the Plan: Once the plan is in place, ensure that you adhere to the agreed-upon payment schedule. Missing payments can result in the debt being sent back to collections.

Setting up a repayment plan ensures that you can manage your debt in a way that doesn't overwhelm your finances.

Step 8: Make Your Payments as Agreed

Once your payment plan or settlement agreement is in place, it's essential to follow through with your payments as agreed. Consistency is key to resolving the debt and rebuilding your financial stability.

How to stay on track

- Set Up Automatic Payments: Automate payments to ensure you never miss a deadline.

- Keep Records: Save all receipts and documentation related to your payments to keep a record of your progress.

- Review Your Finances Regularly: Monitor your financial situation to ensure you can keep up with your payments.

By sticking to the agreement and making regular payments, you can resolve your debt and move forward with confidence.

Impact of Debt in Collections on Your Credit

Having debt sent to collections can significantly harm your credit score and overall financial standing. Here's how:

1. Credit Score Decline

When a debt is placed in collections, it indicates to lenders that you have missed payments. This can cause your credit score to drop by up to 100 points or more, making it harder to secure new credit or favorable rates.

2. Lasting Credit Report Impact

Accounts in collections can remain on your credit report for up to seven years, even after settlement or payment, making it challenging to repair your credit history.

3. Loan Approval Challenges

A collection account, especially one that remains unpaid, can make you appear high-risk to lenders, potentially resulting in loan rejections, higher interest rates, or stricter terms.

4. Broader Financial Impact

A low credit score affects more than just loans. It can lead to higher insurance premiums, difficulties renting a home, or challenges in securing jobs that require credit checks.

5. Duplicate Reporting Damage

If both the original creditor and the collection agency report the same debt, it can double the negative impact on your credit score.

6. Paying Off Collections Doesn’t Fully Restore Credit

Even after settling or paying off collections, the record will stay on your credit report for up to seven years, impacting potential lenders’ view of your financial responsibility.

7. New Credit Scoring Models May Overlook Paid Collections

Some newer scoring models, like FICO 9 and VantageScore 3.0, give less weight to paid collections, potentially reducing their impact. However, many lenders still use older models, so the effect on your credit may remain significant.

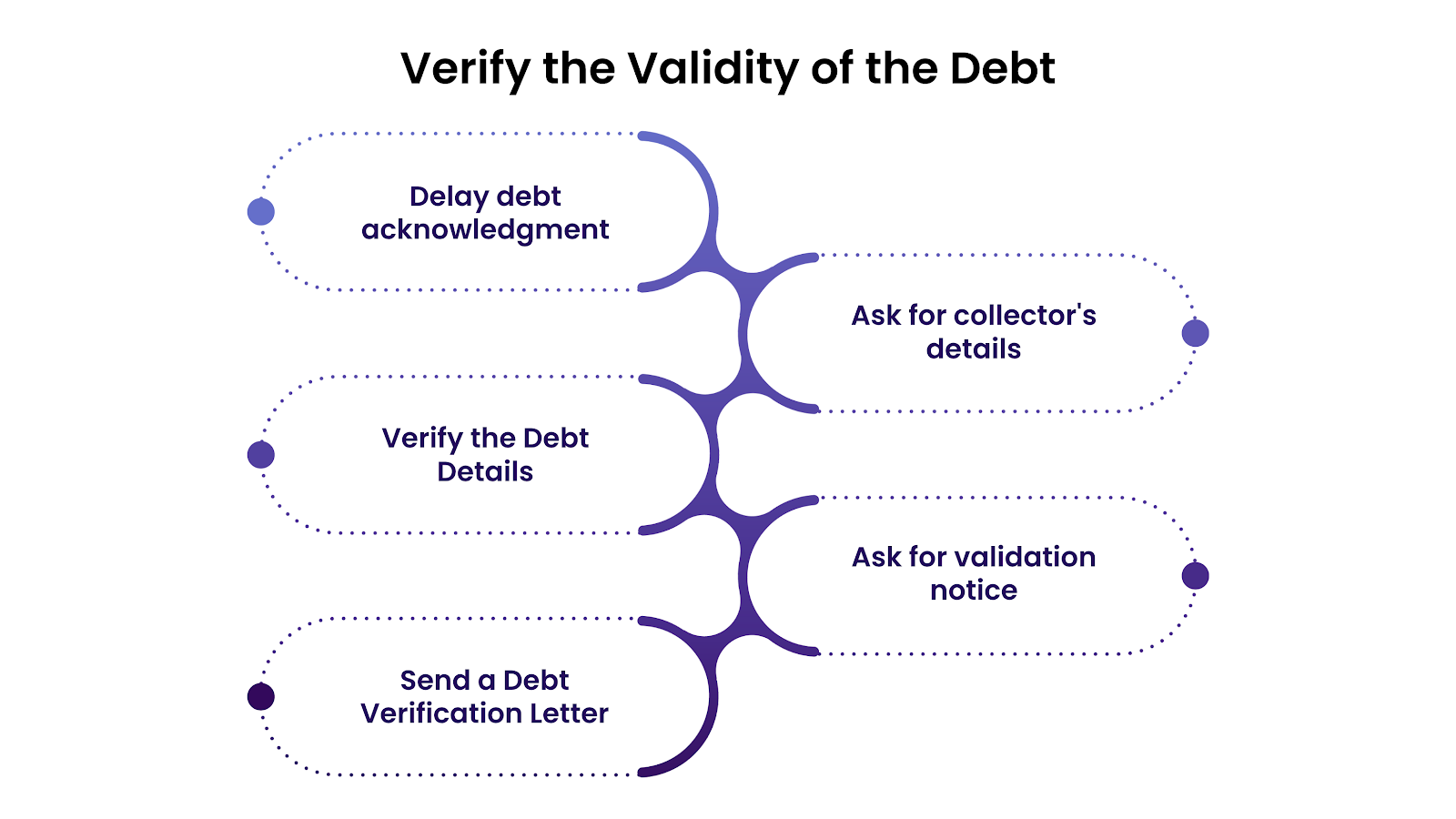

Verify the Validity of the Debt

To protect yourself from paying debts you don't owe, follow these steps to verify the legitimacy of a debt when contacted by a collector:

1. Do Not Acknowledge the Debt Immediately

Avoid confirming the debt or sharing personal details during the first contact. Acknowledging the debt can restart the statute of limitations, extending collection efforts. It also prevents potential fraud, as scammers may use this opportunity to steal your information.

2. Request Debt Collector’s Information

Ask for the debt collector's full name, company name, address, and phone number. Legitimate collectors will provide this information. If they hesitate or provide incomplete details, it’s a red flag.

3. Verify the Debt Details

The collector must provide the creditor’s name and the amount owed. If they refuse or give inconsistent details, the debt may not be legitimate.

4. Request a Written Validation Notice

Within five days of contacting you, the collector must send a written notice with details about the debt, including the amount owed and the creditor's name. If they don't, consult a legal professional.

5. Send a Debt Verification Letter

After receiving the collector's information, send a debt verification letter via certified mail requesting proof of the debt. Include the original creditor's name, the amount owed, and any relevant agreements. Keep a copy of the letter and any responses for your records.

These steps help ensure you’re not paying for a debt that isn’t yours or one that cannot be legally enforced.

Assess Your Repayment Ability

Understanding your financial situation is crucial to creating a repayment plan that works for you. Here’s how to assess your ability to repay debt:

1. Understand Your Financial Situation

Review your income, expenses, savings, and existing debt to form a clear picture of your finances. This will help guide your repayment plan.

2. Calculate Your Income and Expenses

Add up your income sources and list your monthly expenses. Subtract expenses from income to determine how much you can allocate to debt repayment.

3. Calculate Your Debt-to-Income Ratio

This ratio measures the percentage of your income dedicated to debt. A higher ratio may suggest the need for debt relief options or prioritizing higher-interest debts.

4. Assess Your Assets and Liabilities

List your assets (savings, investments) and liabilities (loans, credit card debt). Subtract liabilities from assets to determine your net worth and adjust your repayment strategy if needed.

5. Evaluate Your Credit Profile

Check your credit report for errors or areas to improve. A stronger credit profile may offer more repayment flexibility.

6. Create and Stick to a Budget

Use budgeting tools to allocate a portion of your income toward debt repayment while covering essentials. Regularly review and adjust your budget to stay on track.

7. Lower Your Bills

Cut unnecessary spending, renegotiate contracts, and find more affordable options for services to free up more money for debt repayment.

8. Explore DIY Debt Payoff Methods

Use strategies like Debt Snowball (smallest debts first) or Debt Avalanche (highest interest first) to tackle debt systematically.

9. Consider Debt Consolidation

Combine multiple debts into a single loan with a lower interest rate, simplifying payments and reducing interest costs.

10. Explore Debt Relief Options

If your debts are overwhelming, consider debt settlement or bankruptcy, but consult a financial advisor or legal expert before pursuing these options.

11. Analyze Your Debt Servicing Plan

Prioritize debts, stick to your plan, and review your progress regularly. A solid plan helps you stay focused and make steady progress toward financial freedom.

Negotiate with Credit Collection Services

Negotiating with the right approach can reduce your debt, establish manageable payment terms, and even improve your credit. Here's how to do it successfully:

1. Learn About the Debt

Understand the debt fully before negotiating. Request a detailed breakdown from the collector, including fees and interest, and check your credit report to ensure accuracy.

2. Understand What You Can Afford

Assess your income and expenses to determine how much you can realistically offer without affecting essential needs. This ensures you don’t over-promise during negotiations.

3. Calculate a Realistic Repayment Plan

Develop a repayment plan based on your budget. Ensure the payment amount and timeline are manageable for your financial situation.

4. Make a Repayment Proposal

Approach the collector with a fair proposal. Start with a lower amount than what you can afford and explain your financial difficulties. Propose a settlement or payment plan if needed.

5. Speak to the Debt Collector

Maintain a calm, respectful tone during communication. If the collector's offer is too rigid, ask for flexibility, such as reduced interest or extended payment terms.

6. Get Everything in Writing

Ensure the terms of your settlement or repayment plan are documented in writing. Include the total debt, payment schedule, and settlement details.

7. Negotiate Credit Report Updates

Ask the collector to report the debt as “paid” or “settled” once you’ve made the payment. Ensure it’s reflected accurately on your credit report.

8. Make Your Payments

Follow the agreed payment schedule. Set up automatic payments if possible and keep documentation of each payment.

To ensure a successful outcome in your negotiations, it's essential to maintain open and organized communication with the credit collection service. Here's how you can approach this crucial step effectively.

Communicate Directly with Credit Collection Services

Handle the situation in the most effective way possible by following the communication process directly with the credit collection service.

1. Be Willing to Communicate

Avoiding communication can worsen the situation. Be honest about your financial difficulties and set boundaries for follow-up.

2. Stay Calm During Conversations

Maintain professionalism, even when frustrated. Document every conversation for your records.

3. Organize Your Information

Gather all relevant details, including debt information, payment history, and financial data, to strengthen your position during negotiations.

4. Know Your Rights

Understand your legal rights under the FDCPA. You have the right to request validation, dispute the debt, and stop contact if needed.

5. Know the Statute of Limitations

Research the statute of limitations in your state. If the debt is past this time frame, don't acknowledge it to avoid restarting the collection process.

6. Be Open to Other Forms of Communication

Email or text can be less stressful and offer better documentation than phone calls. Use these methods for flexibility and record-keeping.

7. Settle the Debt

If possible, offer a lump sum payment or negotiate a manageable payment plan to settle the debt.

8. Go to Court

If negotiations fail, consider legal action, especially if the debt is incorrect or past the statute of limitations.

By staying organized, informed, and proactive, you can effectively negotiate with credit collection services and regain control of your finances.

How The Forest Hill Management's Services Help You Manage and Resolve Debt Effectively

The Forest Hill Management designs comprehensive services to help individuals and businesses manage debt and navigate credit collection processes. Here's how their specialized services can support you in paying off debt:

Portfolio Management

This helps clients efficiently manage and track overdue accounts. With expert strategies and tailored solutions, they ensure your portfolios are well-managed, reducing stress and improving your financial situation.

Portfolio Acquisitions

The Forest Hill Management simplifies the process of acquiring profitable portfolios. This service is ideal for businesses or investors seeking to strengthen their financial position by acquiring high-value accounts, ensuring a seamless and compliant acquisition process.

Compliance & Technology Solutions

The Compliance and Technology Service ensures that all debt collection actions comply with industry regulations. By utilizing advanced technology, The Forest Hill Management ensures the protection of your financial data while enhancing the efficiency of debt recovery.

By utilizing these services, clients can effectively manage and resolve outstanding debts, ensuring financial stability and improved cash flow.

Conclusion

Effectively paying off debt in credit collection services requires clear communication, accurate information, and proactive management. By verifying the validity of the debt, organizing your finances, and negotiating directly with collectors, you can significantly reduce the burden of outstanding obligations. It's important to stay engaged with the process and be prepared to adjust your repayment plan as needed.

Ultimately, the key to successfully navigating credit collections and paying off debt lies in staying informed, disciplined, and proactive. Whether you're negotiating better terms, exploring settlement options, or simply ensuring that all agreements are in writing, these steps will empower you to regain control over your financial situation and move toward a debt-free future.

FAQs

1. Can I hire a collection agency to collect a debt?

Yes, you can hire a credit and collection agency to recover overdue debts. These collection companies specialize in collecting debt services, using established processes to help recover the money owed to you. By hiring a debt collection service, you can focus on other aspects of your business while professionals handle the debt recovery process.

2. What is the 11-word phrase to stop debt collectors?

The 11-word phrase is: "Please cease all communication with me, I am requesting validation of debt." This phrase is often used when you want to stop contact from a debt recovery agent. By requesting verification, you can ensure the legitimacy of the debt before proceeding further with any debt collection service.

3. What is a debt recovery agent?

A debt recovery agent is a professional hired by a credit and collection agency to collect overdue debts. They work on behalf of individuals or businesses to recover money from debtors. These agents are trained to handle collection services while ensuring compliance with regulations and maintaining ethical practices in the debt recovery process.

4. What happens if you ignore debt recovery?

Ignoring debt recovery can lead to serious consequences, including legal action and damage to your credit score. Suppose you neglect to address or refuse to work with a debt collection agency. In that case, your debt may escalate, and collection companies may seek court intervention to recover the funds owed. It's crucial to respond promptly to avoid these adverse outcomes.