Using Technology to Improve Debt Collection Compliance in 2025

Transform Your Financial Future

Contact UsAs we move into 2025, compliance in debt collection is more crucial than ever. With tightening regulations, a growing emphasis on consumer rights, and increased scrutiny from agencies like the Consumer Financial Protection Bureau (CFPB), debt collection practices must evolve. The risk of non-compliance includes lawsuits, audits, and hefty fines, among other potential consequences.

Whether you're an SMB looking to streamline your debt collection compliance or a financial institution worried about legal exposure, the right compliance resolutions can help you avoid costly penalties while ensuring efficient recovery practices.

In this blog, we'll understand the key compliance risks in debt collection automation, how the right tech solutions can mitigate these risks, and what steps you can take to stay compliant in 2025 and beyond.

TL;DR (Key Takeaways)

- Compliance Changes: Stricter debt collection laws in states like California and Florida, plus new rules on medical debt reporting and data collection.

- Top Compliance Risks: Outdated systems, vendor lock-in, and weak data security threaten compliance in automation.

- Tech Solutions: AI & ML, RPA, and cloud computing help streamline processes, reduce errors, and ensure compliance.

- How TFHM Helps: TFHM offers customized tech solutions to optimize debt collection and maintain compliance.

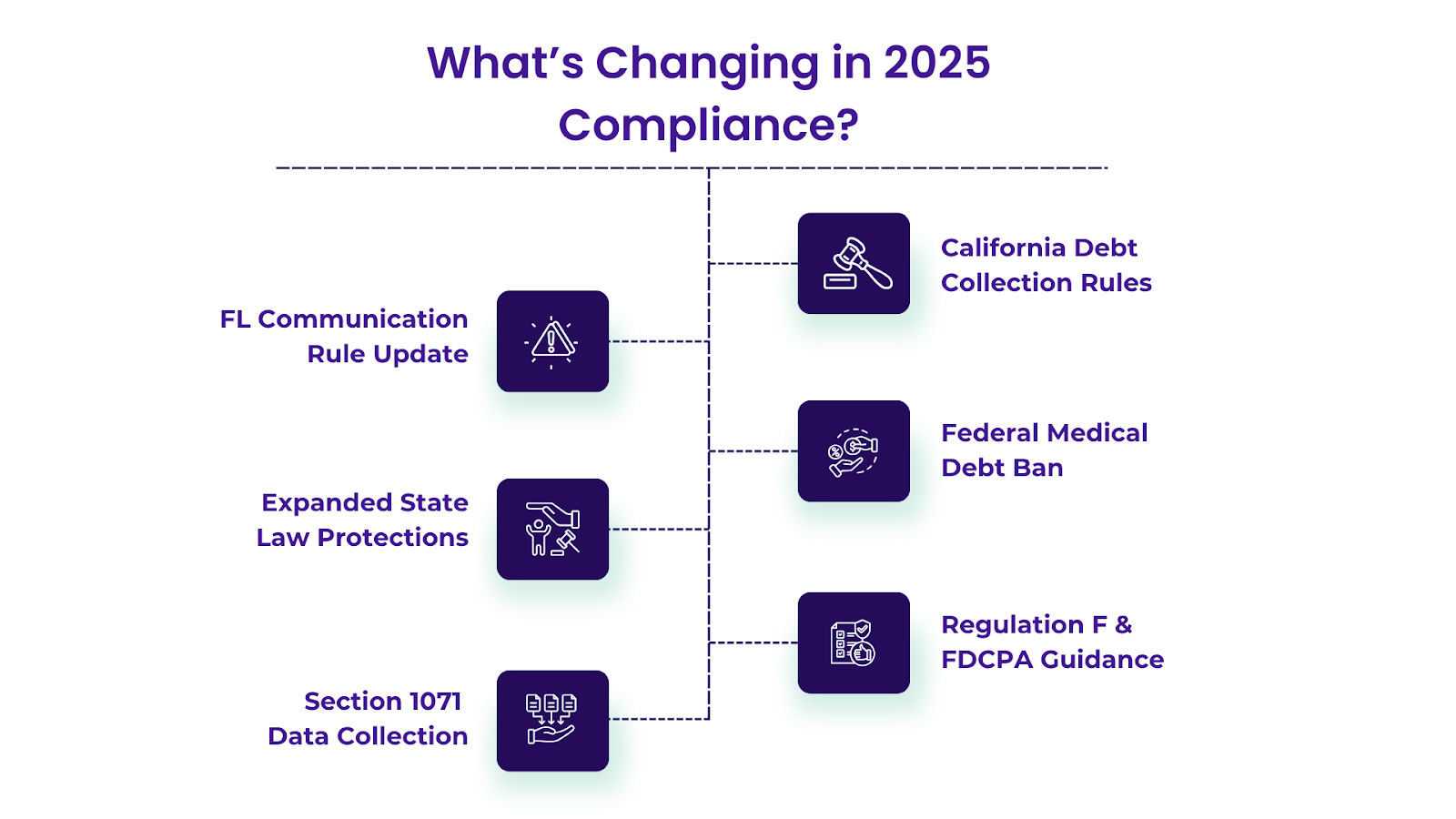

What’s Changing in 2025 Compliance?

As 2025 approaches, debt collection regulations are becoming more stringent and complex. Small and medium-sized enterprises (SMBs), financial institutions, and debt recovery firms must adapt quickly to avoid compliance pitfalls. Below is a breakdown of key regulatory changes:

1. California’s New Debt Collection Regulations (Effective July 1, 2025)

California’s new debt collection regulations, effective July 1, 2025, will require businesses to adhere to the California Consumer Privacy Act (CCPA) and the California Debt Collection Licensing Act (DCLA), strengthening consumer protections.

For businesses, this means:

- Clearer Disclosures: Debt collectors will need to provide more detailed information on debt amounts and the names of creditors.

- Accountability: There will be more stringent documentation requirements for every communication made with debtors.

- Licensing Requirements: Debt collectors are required to obtain and maintain a valid license to operate in California.

The Forest Hill Management helps SMBs with automated compliance tracking systems to ensure clear documentation in real-time and reduce the risk of non-compliance.

2. Florida’s Modernization of Communication Rules

Florida is modernizing its debt collection communication rules, allowing digital channels, such as text, email, and social media, to be used for debt collection, provided that consumers have granted explicit consent.

For businesses, this presents:

- Explicit Consent: Businesses must obtain clear consent from consumers before communicating via digital channels.

- Stricter Rules on Automated Messaging: Digital communication must comply with both state and federal laws.

The Forest Hill Management supports businesses by integrating CRM platforms that streamline consent management and ensure automated communication is compliant with the latest digital communication rules.

3. Federal Ban on Reporting Medical Debt

The federal government is introducing a ban on reporting medical debt to credit bureaus unless the debt is more than one year overdue. This is aimed at protecting consumers who may face significant challenges paying medical bills.

For debt collectors, this means:

- New Handling Protocols: Debt recovery processes must adapt to this ban, particularly when it comes to the credit score impact.

- Updated Communication Methods: Debt collectors will need to adjust their communication methods for medical debt to consumers.

The Forest Hill Management utilizes debt management tools that can keep consumers informed about changes in medical debt reporting, promoting transparency.

4. Expanded State Law Protections

States such as New York, New Jersey, and Massachusetts are enhancing consumer protections, adding complexity to debt collection practices. New regulations include:

- Shorter Statutes of Limitation for debt collection.

- Consumers will have more opportunities to challenge debts before they are pursued or reported.

- Stricter Restrictions on harassment and deceptive practices.

For businesses, this means:

- State-Specific Compliance: Debt collectors must monitor the evolving laws across various states to ensure they remain compliant.

The Forest Hill Management helps SMBs, financial institutions, and debt recovery firms track and integrate state-specific compliance regulations into their systems, reducing manual oversight and ensuring businesses stay compliant across multiple jurisdictions.

5. Federal Regulation F and Ongoing FDCPA Guidance

The FTC's Regulation F, part of the Fair Debt Collection Practices Act (FDCPA), continues to refine how debt collectors communicate with consumers. These updates focus on:

- Electronic Communications: Clear guidelines for emails, texts, and digital channels.

- Written Disclosures: Debt collectors must provide more transparent written disclosures.

- Prohibited Practices: Enhanced Protection Against Harassment.

The Forest Hill Management ensures financial institutions and debt recovery firms stay compliant with Regulation F by integrating automated systems that support electronic communication.

6. Data Collection Under Dodd-Frank Section 1071

As part of the Dodd-Frank Act, businesses will need to collect and report more detailed data about consumer credit and debt collections, particularly for small businesses and women- and minority-owned enterprises.

For businesses, this means:

- Enhanced Data Collection: New reporting requirements for demographic and debt status data.

- New Reporting Tools: Businesses must implement systems that can accurately manage and report this information.

The Forest Hill Management provides data management tools that help businesses comply with Section 1071 by automating data collection and reporting, ensuring financial institutions and acquisition firms meet new regulations with ease.

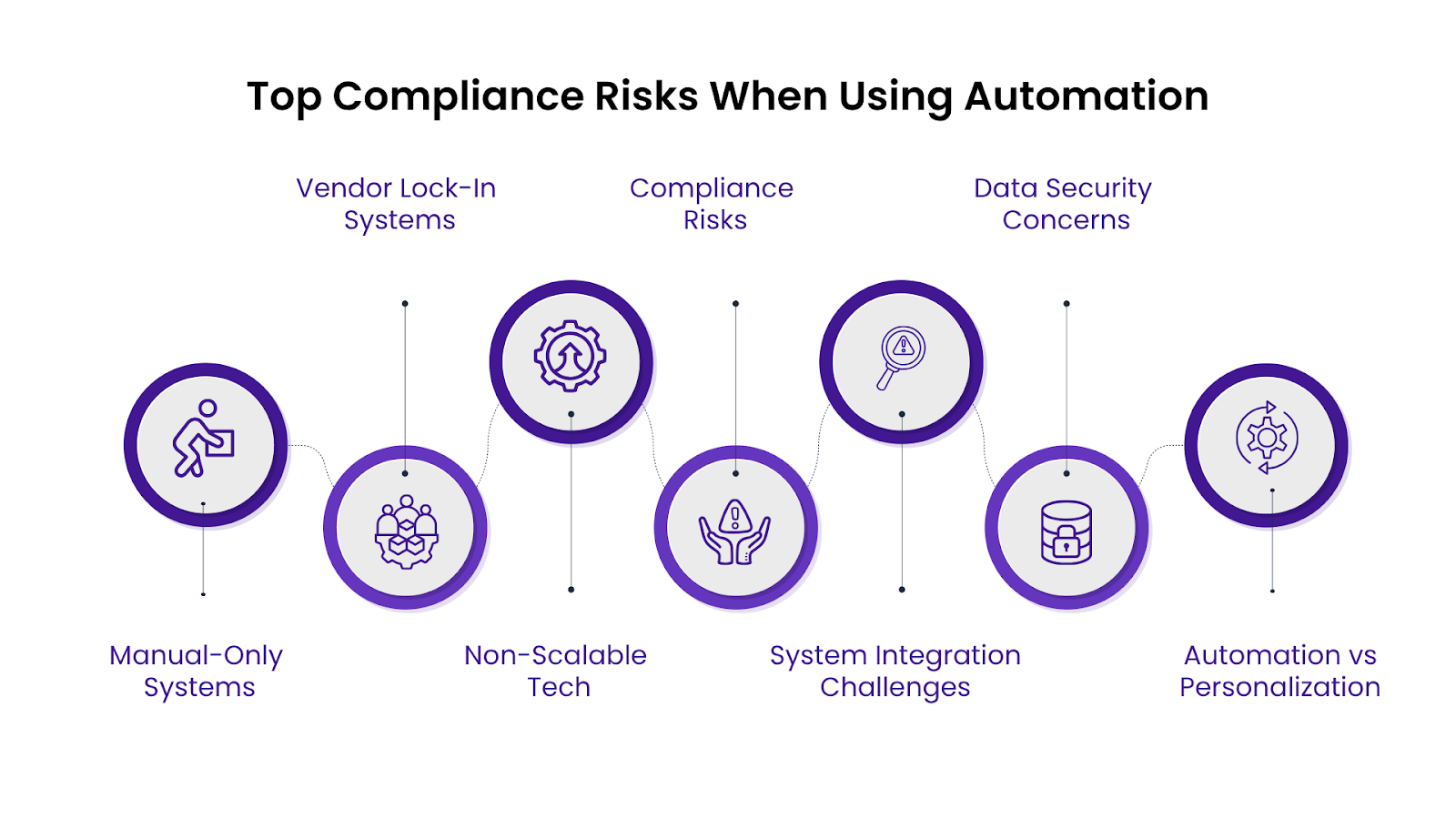

Top Compliance Risks When Using Automation

In debt collection, portfolio management, and financial operations, automation offers a significant advantage, but it also introduces specific compliance risks that businesses must navigate carefully. Below are the top compliance risks that enterprises face when using automation.

1. Rigid, Manual-Only Systems

While automation aims to replace manual processes, many businesses still rely on rigid, manual-only systems that aren't fully integrated with automated tools. This rigidity can create bottlenecks and increase the risk of compliance issues when these systems cannot adapt to changing regulations.

Risks include:

- Outdated systems that cannot scale with new compliance regulations.

- Inability to adapt quickly to regulatory changes, leading to missed deadlines and penalties.

What to avoid:

- Relying on outdated, inflexible systems that don't integrate well with modern automation tools.

- Overlooking the importance of regular system updates to keep pace with evolving regulations.

2. Closed Ecosystems and Vendor Lock-In

Businesses often fall into the trap of using closed ecosystems where all tools and systems are provided by a single vendor. While this might seem convenient, it can create vendor lock-in, restricting your ability to adapt to new regulations or technologies, which could lead to compliance risks.

Risks include:

- Limited ability to switch vendors or integrate new tools as regulations change.

- Struggling to keep up with evolving compliance standards due to vendor restrictions.

What to avoid:

- Committing to a single vendor without considering long-term flexibility.

- Failing to ensure that your systems can integrate with third-party tools as needed.

3. Outdated Tech That Can't Scale

Automation tools that rely on outdated technology are not equipped to handle increasing data or meet evolving regulatory demands. These legacy systems can't scale effectively, leading to significant compliance risks and operational inefficiencies.

Risks include:

- Inability to scale with increasing data and changing regulations.

- Data inaccuracies or processing delays can compromise compliance.

What to avoid:

- Holding onto legacy systems that cannot handle the growing volume of data or complex compliance requirements.

- Failing to invest in scalable, future-proof technology.

4. Hidden Compliance Risks

Automation can sometimes introduce hidden compliance risks that are not immediately visible, such as overlooked data tracking or improperly handled consent. These risks can escalate into significant compliance violations if not carefully monitored.

Risks include:

- Gaps in audit trails, data handling, or missing regulatory checks.

- Untracked compliance documentation or mismanagement of consumer consent.

What to avoid:

- Relying solely on automated systems without regular human oversight.

- Failing to implement audit mechanisms to ensure automated processes meet compliance standards.

5. Integration with Existing Systems: Overcoming Compatibility Issues

Integrating new automation tools with your existing infrastructure can be challenging, especially when dealing with legacy systems. Compatibility issues can lead to data silos, errors, and compliance lapses, resulting in inefficiencies and increased regulatory risks.

Risks include:

- Data mismatches or missed information due to poor integration.

- Compliance breaches are often caused by incompatible software platforms that fail to synchronize effectively.

What to avoid:

- Implementing automation tools without ensuring they are fully compatible with your existing systems can lead to significant issues.

- Overlooking integration testing and proper system synchronization.

6. Data Security Concerns: Safeguarding Sensitive Information

Automation increases the volume of sensitive data processed by financial institutions, making data security a critical concern. Breaches, unauthorized access, or failure to comply with data protection laws can lead to significant legal and reputational damage.

Risks include:

- Data breaches or unauthorized access to sensitive customer information.

- Failing to comply with data protection laws like GDPR, CCPA, and others.

What to avoid:

- Using automation tools that lack strong encryption and role-based access.

- Neglecting data privacy when automating processes that handle sensitive consumer data.

7. The Balance Between Automation and Personalization: Maintaining the Human Touch

While automation increases efficiency, it’s essential not to lose the human touch in customer-facing operations. In sensitive areas like debt collection, personalized communication is crucial to maintaining positive relationships and adhering to consumer protection regulations.

Risks include:

- Overrelying on automation for customer interactions can lead to impersonal communication.

- Failing to meet regulations that require personalized communication and fair treatment.

What to avoid:

- Automating all customer interactions without allowing for human oversight when needed.

- Sacrificing empathy in critical communications, especially in debt resolution scenarios.

How the Right Technology Solves Debt Collection Compliance Risks

Utilize the latest technology to ensure compliance and maintain operational efficiency. From artificial intelligence (AI) to cloud computing, the right technology can help businesses overcome many of the challenges they face in adhering to complex compliance regulations.

Let’s explore the technologies that directly address debt collection compliance challenges, streamlining operations for SMBs, financial institutions, investors, and individuals seeking debt resolution.

1. Artificial Intelligence and Machine Learning (AI & ML)

AI and machine learning (ML) enhance decision-making processes, improve accuracy, and ensure compliance with regulations. AI can analyze vast amounts of data in real time, allowing debt collectors to predict payment behaviors, customize debt recovery strategies, and enhance customer interactions.

Solution for you:

- SMBs struggling with limited resources can utilize AI-powered systems to automate repetitive tasks, thereby making debt recovery more efficient and compliant, without requiring large teams.

- Financial institutions can use machine learning algorithms to identify patterns in large datasets, flagging potential risks and ensuring legal compliance with every communication and interaction.

- Investors can benefit from AI-driven insights that help them evaluate high-value portfolios with higher accuracy, ensuring compliance with industry regulations during acquisitions.

2. Robotic Process Automation (RPA)

Robotic Process Automation (RPA) streamlines repetitive, rule-based tasks, thereby reducing the need for manual intervention. RPA bots can automate processes such as data entry, invoice generation, compliance checks, and follow-up reminders, ensuring that all regulatory steps are followed precisely.

Solution for you:

- SMBs looking to reduce manual efforts can implement RPA to automate debt recovery workflows and ensure that all necessary compliance tasks are completed on time.

- Financial institutions managing large portfolios can benefit from RPA bots that ensure no compliance steps are missed, such as tracking overdue accounts, sending reminders, and maintaining audit trails for every action.

- Investors and acquisition firms can use RPA to automate due diligence tasks, ensuring that each acquisition is compliant with regulatory requirements and reducing the risk of costly compliance mistakes.

3. Blockchain Technology

Blockchain technology provides transparency and security in data management. By recording transactions in a decentralized ledger, blockchain ensures that all data is immutable and traceable, offering an effective solution for managing compliance records in debt collection.

Solution for you:

- Financial institutions can use blockchain to securely track debt collections and document every transaction with an unalterable record, ensuring full compliance and avoiding potential legal disputes over missed actions.

- SMBs can enhance data integrity by utilizing blockchain to track debt recovery processes, ensuring that their clients' data is secure and reducing the risk of data breaches.

- Investors and acquisition firms benefit from blockchain's transparency, ensuring that debt portfolios are accurately tracked and compliant with all regulatory standards throughout the acquisition process.

4. Internet of Things (IoT)

The Internet of Things (IoT) can streamline debt collection processes by improving real-time data access and enabling better communication with clients. IoT-enabled devices allow businesses to track payment behaviors, assess client preferences, and personalize recovery strategies.

Solution for you:

- SMBs can leverage IoT devices to gather real-time insights into customer behaviors, improving how they manage overdue accounts and personalize debt collection without violating privacy regulations.

- Financial institutions can benefit from IoT-enabled sensors that provide real-time data about debtors' financial activities, helping them ensure compliance with timing restrictions for communications and payment requests.

- Investors can utilize IoT-enabled data to better understand the financial health of their portfolios, ensuring acquisitions align with compliance regulations and minimize risks.

5. Cloud Computing

Cloud computing provides scalable storage and processing capabilities to manage vast amounts of data securely. By storing data in the cloud, businesses can ensure they maintain compliance with data protection regulations, such as GDPR or CCPA, through easy access to real-time compliance reports.

Solution for you:

- SMBs can access cloud-based debt collection solutions that provide secure, real-time data storage, enabling them to scale operations while maintaining compliance without heavy upfront investments.

- Financial institutions can securely store and manage large portfolios in the cloud, ensuring compliance with industry regulations while having easy access to data for audits and reports.

- Investors benefit from the scalable nature of cloud computing, as it allows them to handle large datasets and ensure compliance when managing multiple portfolio acquisitions.

6. Payment Fraud Protection

Payment fraud protection systems use advanced fraud detection algorithms, encryption, and multi-factor authentication (MFA) to safeguard transactions. These systems ensure that payments are processed securely and that businesses comply with anti-fraud regulations.

Solution for you:

- SMBs can reduce fraud risks by integrating payment fraud protection systems into their debt collection processes, ensuring that they are compliant with financial regulations while offering secure payment options to clients.

- Financial institutions can implement advanced fraud detection systems to monitor payments and ensure that their collection practices comply with industry security standards.

- Investors can benefit from fraud protection tools that ensure safe transactions when acquiring new portfolios, reducing the risk of fraud and compliance violations.

How The Forest Hill Management Supports Debt Collection Compliance with the Right Technology

With over two decades of industry experience, The Forest Hill Management offers customized solutions designed to smooth your operations, minimize compliance risks, and protect your financial interests.

Whether you're an SMB, a financial institution, an investor, or an individual seeking debt resolution, The Forest Hill Management provides the expertise and technology you need to stay compliant while driving business success.

Key Services Include:

- Portfolio Management: The Forest Hill Management helps businesses optimize and manage portfolios efficiently while ensuring regulatory compliance and data security.

- Debt Collection Services: The Forest Hill Management offers automated debt collection systems that reduce human error, improve recovery rates, and ensure full compliance with industry regulations.

- Technology Integration: Get cutting-edge technology solutions like RPA, AI, and cloud computing that seamlessly integrate with your existing systems, improving compliance and operational efficiency.

- Compliance & Risk Management: Expert team ensures that your operations are fully aligned with ever-evolving regulatory standards, from data protection to payment fraud prevention.

By partnering with The Forest Hill Management , you gain access to tailored, scalable solutions that not only address your current challenges but also prepare your business for future regulatory changes.

Reach out to learn how the services can help you navigate debt collection compliance with confidence and efficiency.

Conclusion

Debt collection compliance presents unique challenges, but implementing the right technology can significantly reduce risks and improve efficiency. From AI & ML driving smarter decision-making to RPA automating repetitive tasks and cloud computing offering scalable solutions, businesses can enhance their operations while staying compliant with evolving regulations.

The Forest Hill Management provides customized, technology-driven solutions that empower businesses to manage debt collection processes securely and efficiently.

Partner with The Forest Hill Management to implement the right technology for your debt collection needs and secure a compliant and successful future.

FAQs

1. What is the 77 rule for collections?

The 7/7 rule requires debt collectors to wait seven days after initial contact before further communication. If a debtor requests written verification, it must be provided within seven days, ensuring compliance with proper procedures and debtor rights.

2. What is compliance in collections?

Compliance in collections ensures that debt collectors follow legal regulations, such as the Fair Debt Collection Practices Act (FDCPA), while acting ethically and transparently. It focuses on maintaining fairness, consumer rights, and adherence to legal standards.

3. What is the most common compliance issue?

A common issue is violating communication protocols, such as contacting debtors at inconvenient times or using abusive language. This leads to fines and legal issues, which are often resolved through improved staff training and adherence to legal communication standards.

4. What are the three pillars of compliance?

The three pillars of compliance in debt collection are legality, transparency, and accountability. Agencies must comply with legal regulations, communicate openly with debtors, and hold themselves accountable to reduce risks and build trust.