What Happens If You Miss a Payment on Consumer Easy Credit?

Transform Your Financial Future

Contact UsIt’s easier to miss a payment than most people think.

A busy month, a forgotten due date, or a tight paycheck is all it takes. Suddenly, you’re staring down a late fee, a credit score drop, and growing financial stress.

And you’re not the only one. As of early 2025, 43% of Americans say they’ve missed at least one payment in the past five years.

The consequences of these late payments can range from minor fees to significant credit damage. Most people don’t realise how quickly one missed consumer easy credit payment can spiral into a bigger problem, sometimes even leading to legal action against them.

However, it’s not all doom and gloom.

We are here to walk you through exactly what happens when you miss a payment. You’ll learn how it affects your credit, what financial and legal risks to watch for, and how to protect yourself going forward.

What Is Consumer Easy Credit?

Consumer easy credit, also known as Consumer EZ Credit, is precisely what it sounds like: credit that’s easier to get, even if your credit history isn’t strong.

It’s designed for people who may not qualify for traditional credit products. This includes:

- First-time borrowers

- Individuals with low or no credit scores

- Anyone working to recover from past financial setbacks

Instead of relying on high credit thresholds and heavy collateral, consumer easy credit focuses on accessibility. It typically comes in the form of:

- Starter credit cards

- Small personal loans

- Retail or buy-now-pay-later credit lines

When used responsibly, these tools can help you move toward a better financial footing. Why use them?

Here are the key benefits:

- It Helps Build or Rebuild Credit: Your payment history is reported to the major credit bureaus. Paying on time improves your credit score over time.

- It Provides Access to Basic Financial Tools: If you need a phone plan, car loan, or apartment lease, having some credit history makes approval easier.

- It’s Quick and Accessible: Applications are usually simple. Approvals are fast. There is often no need for a high credit score or a long financial history.

What to Watch Out For

Consumer easy credit can be helpful due to its relatively lower processing time, but it’s not risk-free. Common pitfalls include:

- High Interest Rates: Some consumer easy credit products can charge interest rates of up to 30% to 40% APR, making them more expensive than traditional loans.

- Steep Penalties for Missed Payments: Late payments can result in costly fees, penalty interest rates, or even expedited collection efforts.

- Temptation to Overspend: Easy access to credit often leads to impulse purchases, especially with “buy now, pay later” options that mask the actual cost.

- Cycle of Repeat Borrowing: Short-term loans can quickly snowball into ongoing debt if you repeatedly rely on them to cover regular expenses.

- Risk of Legal Action: If the debt remains unpaid, lenders may pursue legal action, including lawsuits, wage garnishment, or account levies, to recover the outstanding amount.

The takeaway here is that consumer easy credit can be an innovative tool to build financial momentum if you understand the terms and use it with discipline. Still, even the most well-intentioned borrowers can sometimes fall behind on their payments.

Why It’s So Easy to Fall Behind on Consumer Easy Credit

Even the most responsible individuals occasionally fall behind. A missed payment isn’t always a result of carelessness. More often, it’s the result of everyday financial pressure, timing conflicts, or unexpected life events.

Here are some reasons why people fall behind on their credit payments:

1. Multiple Bills with Mismatched Timing

You may be managing multiple obligations, each with a different due date. So, when your income schedule doesn’t align with their bill calendar, staying current becomes a logistical challenge.

For example, you may be trying to keep up with:

- Rent or mortgage

- Utilities and subscriptions

- Credit card and loan payments

- Medical bills or insurance premiums

If your paycheck arrives mid-month but your bills are due throughout the month, just keeping everything in order can feel overwhelming.

2. No Budget or Autopay to Fall Back On

Without basic systems in place, staying on top of due dates becomes harder. Two of the most common barriers are:

- A lack of autopay means you're relying on memory or reminders (that you may sometimes miss) to pay on time

- No precise budgeting makes it easy to overspend without realizing what’s left for bills

Setting up autopay for at least the minimum amount and creating a basic spending plan can go a long way in preventing missed payments.

3. Life Events That Disrupt Everything

Sometimes, it’s not about financial habits at all. It's about urgent circumstances taking priority. People often miss payments during times of:

- Job loss / Layoffs

- Medical emergencies

- Family or caregiving responsibilities

- Sudden, unexpected, but substantial expenses

All in all, it's more common than you think. If you’ve missed a payment, you’re not alone. Millions of others are in the same situation.

Understanding the consequences can make you more aware of the risks associated with Easy Credit and also help you mitigate stress.

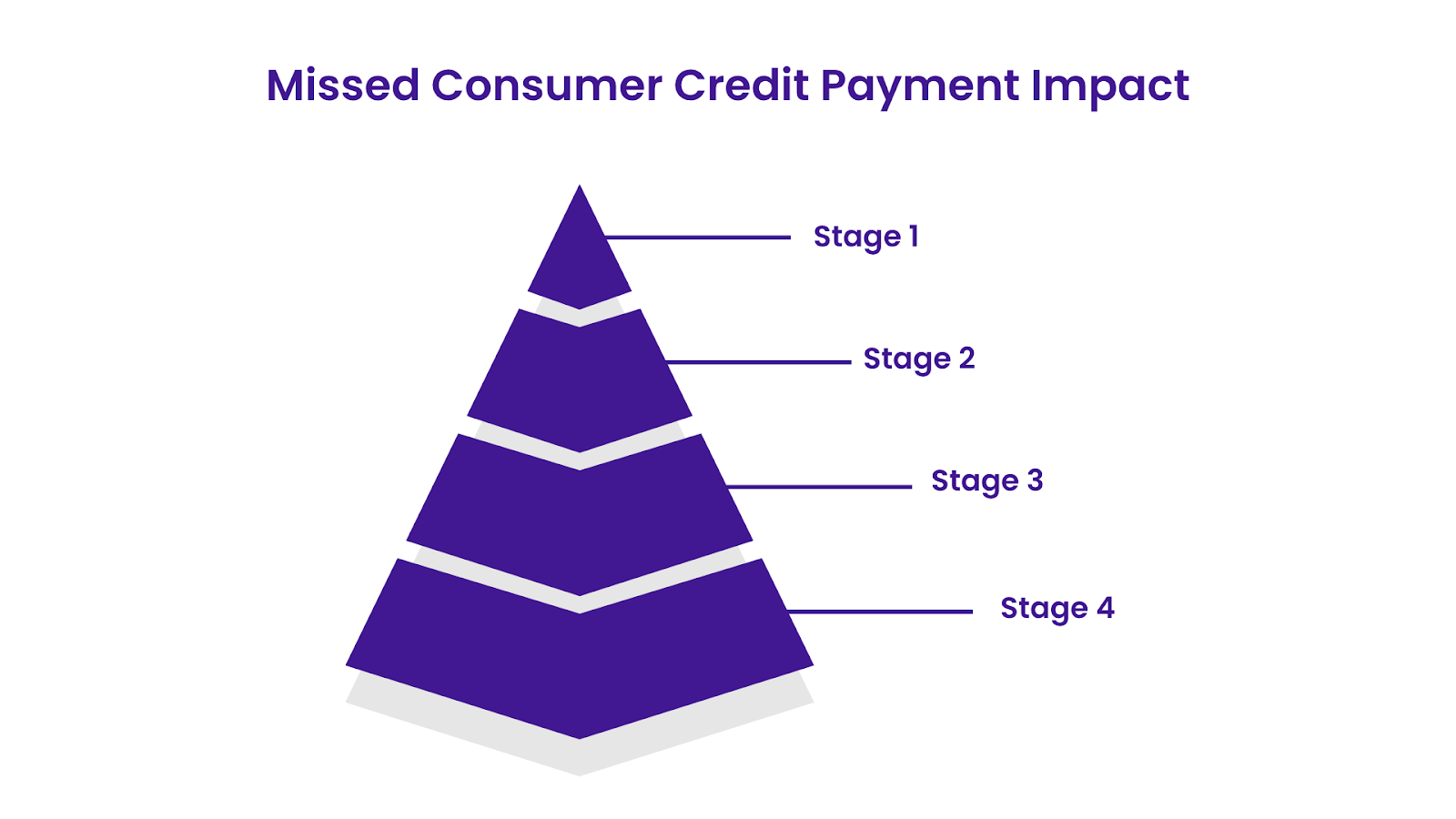

What Happens When You Miss a Payment On Consumer Easy Credit

When it comes to consumer easy credit, the consequences of a missed payment depend on how long it has been overdue.

The longer the delay, the more serious the impact on your finances and credit health.

Here’s what typically happens at each stage:

Stage 1: Day 1 to 29

If you’re just a few days late, you may be able to recover quickly. However, even short delays can trigger added costs.

During this window, you may experience:

- A late payment fee, which can go up to $41, depending on your issuer

- Loss of promotional benefits like 0 percent intro APR offers

- No impact on your credit report yet, as most issuers only report missed payments after 30 days

Here are some steps you can take:

- Pay at least the minimum amount immediately

- Call your issuer and ask if they’ll waive the late fee; they may do so if it’s your first time

- Set a reminder or enable autopay to prevent future slips

Takeaway: Taking early action within 30 days can prevent the issue from appearing on your credit report.

Catch up during this period, and you can often avoid long-term consequences. Acting quickly makes a big difference.

Stage 2: Day 30 to 59

Once your payment is 30 days late, the situation becomes more serious. Lenders typically report the delay to the credit bureaus, which means:

- Your payment history now reflects a delinquency (a serious mark that tells lenders you’ve fallen behind)

- Your credit score may drop significantly, anywhere from 17 to 83 points, based on your current score

- You may be charged a penalty APR (a higher interest rate applied because of late payments, often over 29%), which can make it much more expensive to carry a balance

What to do at this stage :

- Make a payment, it doesn’t matter if it’s partial. Your goal is to show activity on the account

- Contact your creditor to ask if you can reinstate your original APR after consistent on-time payments

Takeaway: The sooner you pay, the less long-term damage you’ll face. Even now, it's not too late to limit the impact.

Recovery becomes harder at this stage, but it’s still within reach.

Stage 3: Day 60 to 89

At this stage, the consequences become more severe. If your payment is still unpaid:

- Your credit score may take another hit, especially if you miss a second billing cycle

- Your account could be frozen or restricted.

- You may start receiving frequent notices or calls from your lender.

What to do at this stage:

- Contact your creditor to discuss payment arrangements or hardship plans

- Review your credit report to monitor how the account is being reported

Takeaway: Effective communication is your most valuable tool. Many creditors are more flexible than you think, especially before the account reaches default.

This is a critical window to communicate with your creditor and explore any available options before the account defaults.

Stage 4: Day 90 and Beyond

By the 90-day mark, most credit issuers consider the account severely delinquent. This can lead to:

- Account default, which may trigger full balance acceleration (meaning the lender can demand the entire unpaid amount right away)

- Assignment to a debt collection agency or legal department

- Risk of a formal collection account appearing on your credit report

What to do at this stage:

- Review your original credit agreement to understand the default terms

- Contact a credit professional or legal advisor if you're receiving collection threats

Takeaway: Even now, you can take action to mitigate the long-term damage and prevent the issue from escalating into a court case.

These outcomes can affect your ability to borrow for years to come. However, even now, taking action can help limit the damage and set you on the path to recovery.

Your Legal Protections (And How to Use Them)

Falling behind on a payment doesn’t mean you lose all control. Even if your account enters default, you have rights that protect you from unfair treatment.

Under the Fair Debt Collection Practices Act (FDCPA), debt collectors are required to:

- Communicate respectfully: They must refrain from harassing, threatening, or using abusive language.

- Provide written verification: If you request it, they must send written proof of the debt before continuing collection.

- Pause collection during disputes: Once you dispute the debt in writing, they must stop contact until they verify the information.

These protections apply whether you're dealing with a traditional loan or a consumer easy credit account.

Understanding the Statute of Limitations On Consumer Easy Credit

Every state sets a time limit on how long a creditor can sue you for unpaid debt. This is known as the statute of limitations.

Once that window closes, the debt becomes time-barred, meaning the creditor can no longer sue you for payment. However, they may still contact you to request payment.

While collectors can still request payment, they can no longer take legal action to enforce it. Be careful, though, as making a payment or even acknowledging the debt in some states can restart the statute of limitations.

If you’re unsure how to respond to collection attempts or navigate the legal side of credit issues, professional guidance can help.

Forest Hill Management works with individuals facing debt-related challenges and offers clear, compliant strategies rooted in both financial recovery and long-term credit health. Our team stays up-to-date on the latest regulations to help you exercise your rights and make informed decisions under pressure.

Your Next Step Toward Financial Stability

Missing a payment on Consumer Easy Credit can feel overwhelming, but it doesn’t have to define your financial future. With the correct information, a clear plan, and timely action, you can take control, rebuild your credit, and move forward with confidence.

Throughout this guide, you’ve learned what happens when payments are missed, how your credit score responds, what legal protections you have, and how to avoid long-term financial setbacks.

If you’re feeling the pressure of overdue accounts or are unsure how to manage your next steps, expert support can make all the difference.

At The Forest Hill Management, we have helped thousands of individuals and organizations regain control of their finances through customized, tech-enabled strategies.

With more than two decades of experience and a commitment to ethical, client-focused solutions, we’re here to help you protect your credit, manage your debt, and build a more stable future.

Ready to take back control? Contact The Forest Hill Management today and let’s build your credit comeback together.

Frequently Asked Questions

1. What qualifies as a missed payment on Consumer Easy Credit?

A payment is typically considered “missed” if it’s not made by the due date stated in your credit agreement. However, most lenders only report it to credit bureaus after it’s 30 days overdue. Acting quickly within this window can help you avoid long-term damage.

2. How much does a missed payment affect my credit score?

The impact depends on your current credit score. If your score is high, a 30-day missed payment could lower it by 60 to 80 points. For someone with a lower score, the drop might be smaller. The longer the payment remains unpaid, the greater the hit to your credit profile.

3. Can one missed payment lead to legal action?

Not immediately. But if your account remains unpaid for 90 days or more, your creditor may declare it in default. This can lead to collections, lawsuits, wage garnishment, or even asset seizure, depending on the laws in your state.

4. How long does a missed payment stay on my credit report?

A missed payment can remain on your credit report for up to seven years from the date of delinquency. However, its impact on your score lessens over time, especially if you build a consistent history of on-time payments afterward.

5. What are my rights if my debt goes to collections?

You are protected under the Fair Debt Collection Practices Act (FDCPA). This includes the right to receive written verification of the debt, to dispute it, and to be free from harassment or deceptive practices during collection efforts.

6. Is it possible to recover from missed payments without professional help?

Yes, but having support can speed up the process and reduce stress. You can recover by catching up on payments, setting up autopay, and building better financial habits.