Understanding Legal Collections and Their Processes

Transform Your Financial Future

Contact UsDealing with unresolved debt or outstanding accounts can feel overwhelming; calls, letters, and mounting pressure often lead to stress and uncertainty about your financial future. You might wonder what comes next or how best to protect your interests when creditors mention legal action.

If these concerns sound familiar, you're not alone. Understanding "what is legal collection" is the first step to regaining control and making informed decisions about your financial situation.

When debt recovery takes a legal turn, the process can quickly become complex, impacting everything from your credit score to your peace of mind. But legal collections work within a structured system designed to uphold rights on both sides, offering solutions that prioritize clarity and fairness.

In this blog, let's understand the legal collections process step by step to address your most pressing questions and face financial challenges with confidence.

Key Takeaways

- Legal collections follow a clear process from demand letter to judgment, ensuring rights and options for both creditors and debtors.

- Regulatory compliance with laws like the FDCPA and CFPB rules protects consumers, enforces transparency, and prevents abuse.

- Compliance improves outcomes by reducing legal risks, building trust, and enhancing debt recovery success.

- Each party's role, including creditors, debtors, attorneys, process servers, and judges, is essential for fair and effective collections.

- Best practices include thorough research, clear communication, strict privacy, and tech-driven compliance to maximize ethical collections.

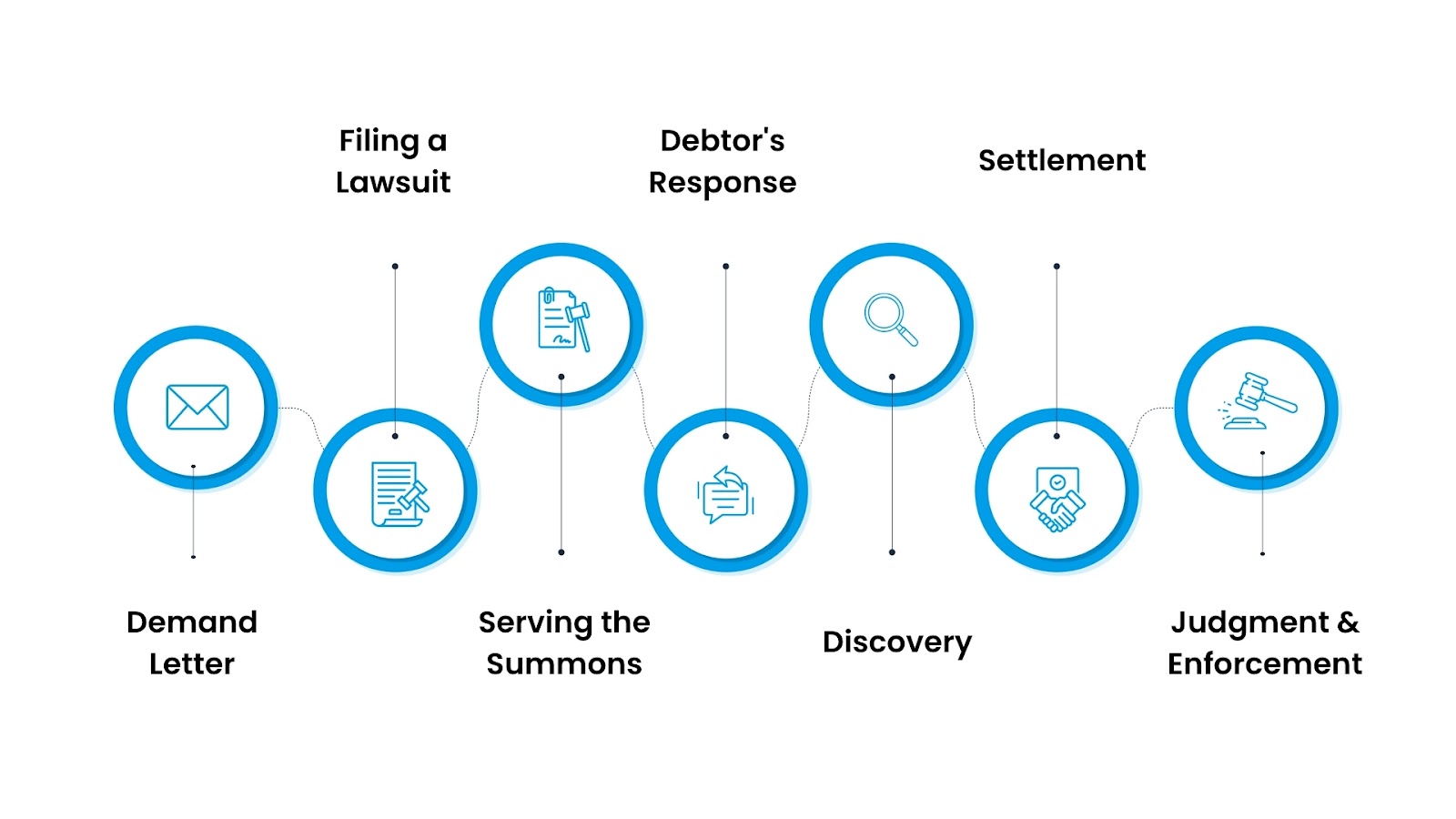

Step 1: Demand Letter

- Purpose and Power: The demand letter isn't just a warning; it triggers the legal timeline. This document details the debt, clearly sets payment deadlines, and outlines possible legal action, giving you a written record from the start.

- What This Means: Knowing that a demand letter is a signal to act quickly can help you avoid deeper legal trouble and open an opportunity to settle before extra costs or court involvement arise.

Step 2: Filing a Lawsuit

- Court Involvement: The creditor files a claim in court, officially requesting a judge’s intervention.

- Legal Fundamentals: This step creates a public record and puts due process in motion, protecting both parties' rights and allowing debtors time to prepare a defense or counteroffer.

Step 3: Serving the Summons

- Transparency: Legal action requires that you be formally notified, protecting you from judgment without knowledge.

- Importance: Proper service provides a clear timeline and the right to respond, which can significantly impact the outcome.

Step 4: Debtor's Response

- Choice and Control: Responding isn't just a procedural matter; it's your opportunity to share your side, admit, dispute, or negotiate the debt.

- Strategic Insight: Providing timely answers can prevent a default judgment and offer leverage for structured settlements.

Step 5: Discovery

- Evidence Exchange: This step makes the process fair by requiring both sides to share facts, documents, and answers under oath.

- Key Strength: Understanding discovery helps you to request information that could change the trajectory of the case.

Step 6: Settlement or Trial

- Negotiation: Most cases end here. Settlement avoids court costs, preserves relationships, and may lead to creative solutions (like payment plans).

- Understanding Options: Even at this late stage, you have the option to compromise or let a judge decide.

Step 7: Judgment and Enforcement

- Legal Force: A court judgment holds the weight of law; failing to comply may result in wage garnishment or liens.

- Personal Impact: Know that enforcement measures can impact your income or assets, making it vital to act early in the process.

Understanding the legal steps involved is just one side of the equation; equally important is knowing the regulatory compliance in debt collection. Let's see how it ensures fairness, transparency, and respect for consumer rights.

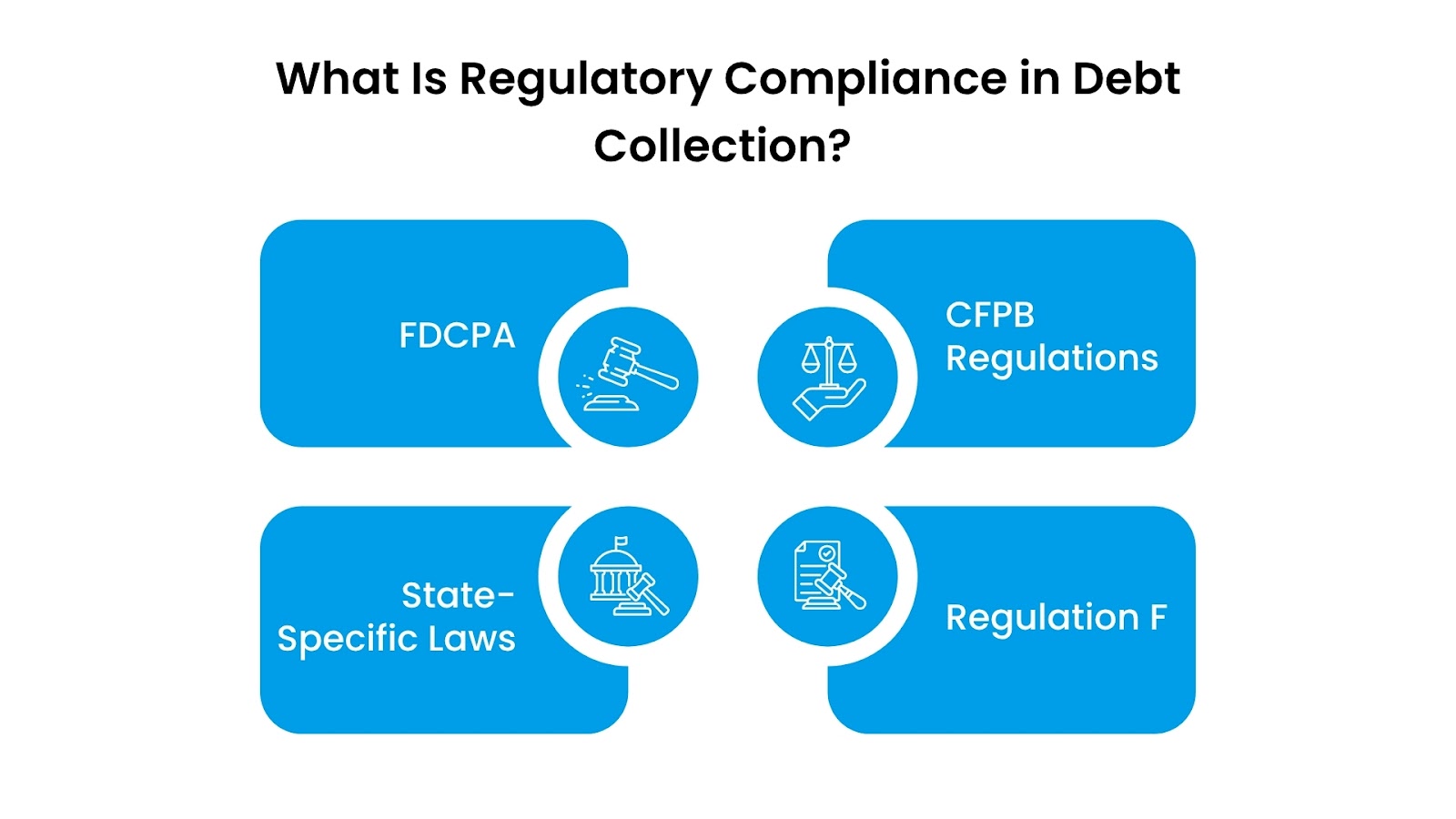

What Is Regulatory Compliance in Debt Collection?

Regulatory compliance in debt collection refers to adhering strictly to the laws and rules designed to protect consumers and ensure ethical practices throughout the collection process.

These regulations establish clear guidelines for how debt collectors communicate, interact, and enforce debts, striking a balance between creditor rights and safeguards against harassment or unfair treatment.

1. The Fair Debt Collection Practices Act (FDCPA)

Enacted in 1977, the FDCPA is the foundational federal law aimed at eliminating abusive, deceptive, and unfair debt collection practices. It protects consumers from harassment and false representation by debt collectors and provides a formal process to dispute and validate debts.

Alongside its fundamental prohibitions, the FDCPA grants critical consumer protections:

- Right to Verification: You can request written proof of the debt, which collectors must provide, aiding in fraud prevention and transparency.

- Limits on Communication: Collectors are restricted from contacting consumers at odd hours or using threatening language, upholding your privacy and peace of mind.

- Reporting Violations: Consumers are empowered to report unfair practices, with the FDCPA creating accountability for collection agencies.

Value tip: If contacted about a debt, always ask for validation in writing. This is your first line of defense against scams and erroneous claims.

2. The Consumer Financial Protection Bureau (CFPB) Regulations

The CFPB is a federal agency established to enforce consumer financial laws, including those regulating debt collection practices. It issues rules and guidance that update and clarify existing laws to keep pace with evolving financial markets and technology.

The CFPB plays a proactive oversight role by:

- Monitoring Industry Trends: Tracking and acting against problematic collection practices on a national level.

- Consumer Complaints: Offering a portal for reporting issues, ensuring your concerns are not ignored.

- Risk Assessments: Large agencies are subject to regular audits, promoting sustained industry compliance.

Practical tip: Utilize the CFPB’s free complaint tool if you encounter suspicious or aggressive debt collection—your case can drive broader enforcement and reform.

3. State-Specific Laws

In addition to federal regulations, each U.S. state implements its own laws governing debt collection. These can include stricter rules on the frequency and manner of contact, licensing requirements for collectors, and enhanced consumer protections beyond federal mandates.

State regulations often extend beyond federal rules:

- Caps on Contacts: Some states strictly regulate the frequency and timing of collection calls.

- Licensing Requirements: Certain states demand that collectors hold licenses, ensuring professional standards are met.

- Custom Protections: Statutes of limitations and dispute procedures vary, sometimes offering broader consumer rights.

Helpful advice: Always check your state's official consumer protection resources. Laws differ, and local guidance ensures you know your rights in detail.

3. Regulation F

Regulation F, introduced by the CFPB, updates the FDCPA’s rules with detailed requirements for debt collection communications, especially focusing on transparency and consumer privacy in modern communication channels.

Regulation F introduces practical, modern standards:

- Communication Clarity: Debt collectors must disclose debt details, origin, and your rights using clear language.

- Electronic Communication: Strict regulations on texts, emails, and social media messages ensure your consent and privacy are honored.

- Limits on Harassment: Concrete restrictions on repetitive contacts deter aggressive collection tactics.

Key insight: Collectors are now required to keep detailed records of every interaction, creating a documented trail you can reference if any disputes arise.

Now, let’s understand how Compliance is fundamental within legal collections because it protects consumers, mitigates risks, builds trust, and ultimately improves the success of debt recovery efforts.

Why Compliance Matters in Debt Collection

Compliance in debt collection is not just a legal requirement; it is foundational for building a fair, effective, and sustainable debt recovery process. For individuals and businesses managing financial obligations, understanding why compliance matters can make a significant difference in outcomes.

Here are the key reasons compliance plays such a crucial role in debt collection:

1. Protecting Consumers

Compliance safeguards consumers from harassment, deception, and unfair practices. It ensures respectful communication and upholds consumer rights like verifying debts and disputing inaccuracies, fostering transparency and fairness.

2. Mitigating Legal and Financial Risks

Adhering to regulations reduces the risk of costly lawsuits, penalties, and reputational damage. Strong compliance programs help organizations avoid violations by staying updated on laws and training staff accordingly.

3. Enhancing Credibility and Trust

Lawful and ethical practices build goodwill, encouraging debtor cooperation and improving relationships with clients and partners. Trustworthiness enhances long-term business sustainability.

4. Improving Collection Success Rates

Regulated, respectful communication enhances debtor engagement and increases the likelihood of payment. Compliance-driven strategies optimize contact methods to recover debts efficiently while minimizing disputes.

5. Adapting to Changing Regulations

Ongoing monitoring of evolving laws and adoption of compliance technologies help organizations remain agile, avoid costly disruptions, and maintain operational excellence in an ever-changing legal landscape.

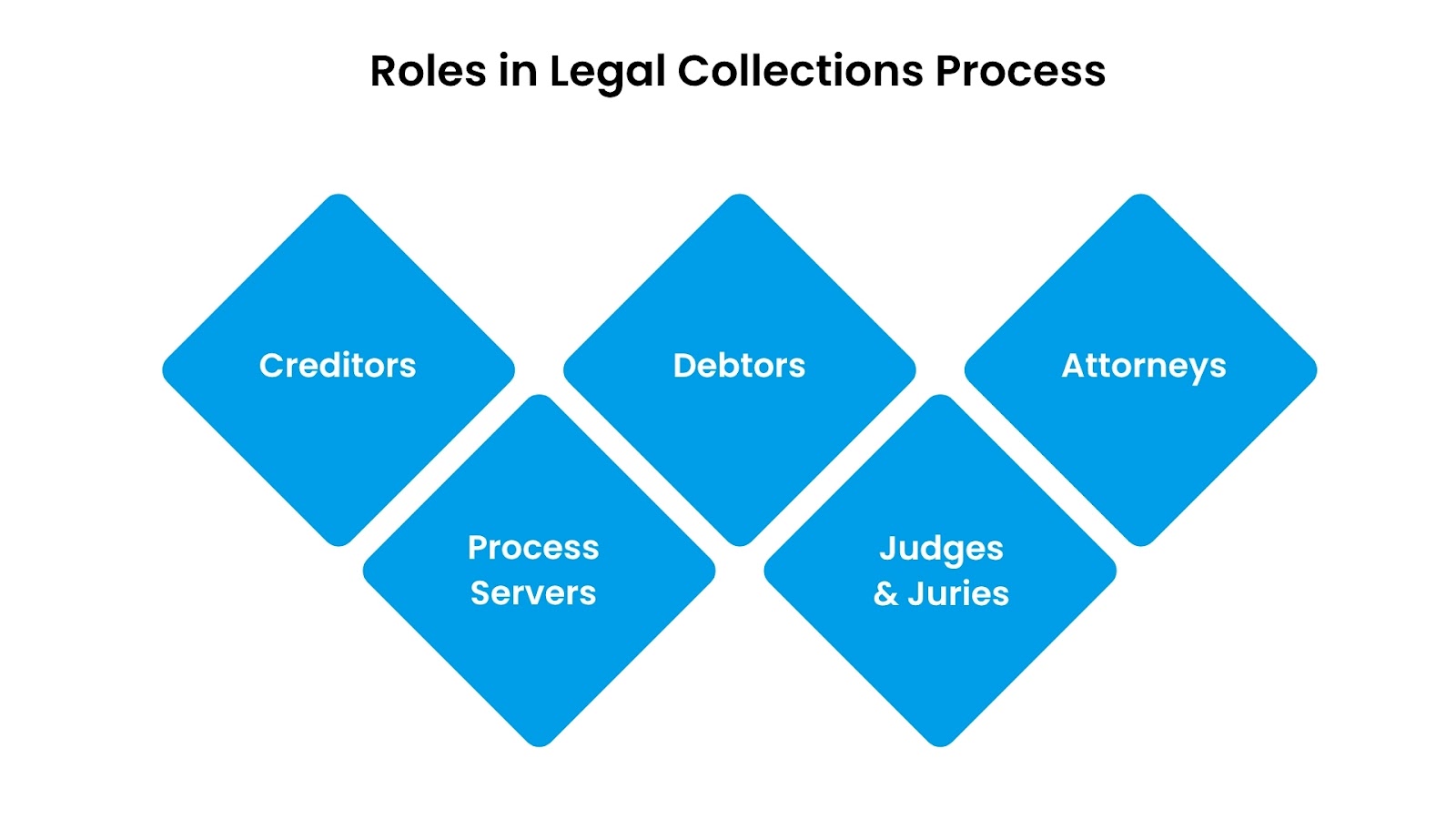

To understand "what is legal collections?", it's essential to know the distinct roles played by creditors, debtors, attorneys, process servers, and judges throughout the process.

The Role of Various Parties in the Legal Collections Process

In the legal collections process, each party plays a distinct and vital role to ensure that debt recovery is conducted fairly and effectively, within the boundaries of the law. Understanding these roles helps both creditors and debtors manage the process with greater clarity and confidence.

Creditors

Creditors are the individuals, businesses, or financial institutions that are owed money. Their role is to initiate the collection process by identifying unpaid debts and attempting to recover what is due. They provide essential evidence supporting their claims, such as contracts, invoices, or account statements, to validate the debt.

Debtors

Debtors are the individuals or businesses who owe money. Their role is crucial in responding to collection efforts, whether by acknowledging the debt, disputing it, or negotiating repayment terms. Debtors have rights protected by consumer laws, including the right to receive validation of the debt and to be free from harassment or unfair collection tactics.

Attorneys

For creditors, legal counsel prepares filing documents, presents cases in court, and advises on compliance with laws. For debtors, attorneys may contest claims, negotiate settlements, or defend against improper collection practices. Their legal expertise ensures procedural fairness and helps protect the rights of both parties.

Process Servers

Process servers act as neutral third parties responsible for delivering official legal documents such as summons and complaints to debtors. Their role is to ensure proper and timely notification of legal actions, which is fundamental to upholding due process by guaranteeing the debtor has the opportunity to respond.

Judges and Juries

Judges oversee legal collection cases in court, ensuring hearings follow due legal standards and making rulings based on evidence and law. In some cases, juries may be tasked with determining facts or deciding liability. Their judgments result in enforceable orders, such as repayment mandates or legal remedies, that concludes the collections process in a fair and authoritative manner.

Now, let's examine effective debt recovery practices through legal collections, which rely on strategic and compliant approaches that maximize results while respecting legal and ethical standards.

Strategies and Best Practices for Effective Legal-Based Collection

1. Conducting Background Research on Debtors

Before pursuing legal action, it is critical to gather detailed information about the debtor's financial status, past payment behaviour, and potential ability to pay. Comprehensive research helps tailor collection strategies and prioritize efforts effectively.

Pro tip: Use credit reports, public records, and financial statements to assess risk and identify the best approach, minimizing wasted effort on uncollectible accounts.

2. Establishing Clear Communication

Open, respectful, and transparent communication builds trust and encourages cooperation from debtors. Clearly explain debt details, payment options, and potential legal consequences in a straightforward and non-aggressive manner.

Pro tip: Personalize communication channels based on debtor preferences, whether phone, email, or text, to maximize engagement and responsiveness.

3. Developing Compliant Debt Collection Policies and Procedures

Ensure that all collection practices strictly adhere to federal, state, and local regulations such as the FDCPA and Regulation F. Consistent policies help prevent legal risks and reinforce ethical standards in every interaction.

Pro tip: Regularly review and update collection policies to incorporate changes in law and industry best practices, while providing staff with compliance training.

4. Implementing a Robust Follow-up Mechanism

Timely and organized follow-ups maintain momentum in the collection process. Automated reminders, scheduled calls, and systematic record-keeping ensure no account is overlooked and responses are tracked efficiently.

Pro tip: Employ technology like CRM systems with built-in compliance checks to automate follow-ups and maintain detailed audit trails.

5. Respecting Debtors' Privacy

Handling sensitive financial and personal data with the utmost confidentiality is both a legal and ethical obligation. Secure data storage and limited access reduce risks of breaches and build debtor confidence.

Pro tip: Implement strict data protection protocols aligned with regulations such as GDPR or CCPA where applicable, and train employees on privacy best practices.

6. Partnering with Attorneys

Involving legal experts early can streamline complex collections, ensure procedural accuracy, and enhance negotiation outcomes. Attorneys can advise on filing lawsuits, settlements, and post-judgment enforcement.

Pro tip: Build strong relationships with specialized debt collection attorneys who understand your business needs and local jurisdictional nuances.

7. Reporting to Credit Bureaus

Updating credit bureaus with accurate and timely information about debtor accounts can motivate repayment and improve long-term credit market transparency.

Pro tip: Ensure reports are compliant and fact-checked to avoid disputes or damage to your organization's credibility.

Managing legal collections can be complex, but specialized partners like Forest Hill Management provide expert guidance and tailored solutions to simplify and optimize the process.

How Forest Hill Management Can Help You

Forest Hill Management is a trusted leader in financial management, specializing in guiding individuals and businesses through complex financial challenges with confidence. With over two decades of experience, the company has built a strong reputation for empowering clients to regain control over their financial futures.

Their tailored services cover the full legal collections cycle:

- Portfolio Management: Efficiently tracks and manages accounts with customized solutions, reducing client workload and ensuring strategic handling throughout collections.

- Portfolio Acquisitions: Conducts thorough due diligence and manages smooth, compliant portfolio acquisitions to support client growth and stability.

- Compliance & Technology: Combines cutting-edge technology with strict regulatory adherence to protect data, minimize legal risks, and ensure ethical collection practices.

Schedule your consultation today! Gain expert guidance, personalized strategies, and robust compliance support.

Conclusion

Understanding "what is legal collections?" with the complex process behind it helps you to take control of your financial challenges and navigate debt recovery with confidence. Legal collections are designed not only to protect creditors' rights but also to ensure debtors are treated fairly, with clear regulatory frameworks preventing abusive practices.

By knowing the step-by-step process, the critical role of compliance, and the responsibilities of all parties involved, you are better prepared to respond effectively and safeguard your interests.

FAQs

1. What does it mean when an account is placed in legal collections?

When an account is placed in legal collections, it means the creditor has escalated the unpaid debt to a formal court-driven process to recover the owed amount. This usually follows unsuccessful attempts to collect the debt through regular means, and it involves legal notices, possible lawsuits, and enforcement actions.

2. What happens if you never pay collections?

If a collection debt is never paid, it can lead to severe consequences such as court judgments, wage garnishments, liens on property, and damage to credit scores. Unpaid collections may remain on your credit report for up to seven years, making it harder to access credit or loans.

3. Do I have to pay a debt that has been sold?

Yes, if your debt has been sold to a third-party collection agency, you are still legally obligated to pay it. The new owner of the debt assumes all rights to collect it, and payment must be made to them to resolve the obligation.

4. What's the worst a debt collector can do?

The worst a debt collector can do within legal limits is obtain a court judgment against you, leading to enforcement measures like wage garnishments, bank account levies, or property liens. Illegal actions like harassment or threats are prohibited under laws such as the FDCPA and can be reported.