How to Use the Debt Avalanche Method to Pay Off Debt

Need Help Reviewing Your Account?

Contact UsInterest charges keep growing quietly in the background, even when you keep sending payments every month, and that reality can feel deeply discouraging. You may wonder why you’re trying so hard while your balances barely change, which slowly drains your motivation and sense of control.

You might already juggle multiple due dates, minimum payments, and constant alerts, yet nothing seems to truly improve your situation. That constant pressure can leave you feeling stuck, confused, and unsure which move actually helps instead of making things worse.

The avalanche method offers a practical way to take control by focusing your energy where it matters most, without asking you to overhaul your entire life.

This strategy prioritizes the debt costing you the most in interest, so every dollar you pay works harder for you.

In this blog, you’ll learn what the avalanche method really means, how to set it up without added stress, and how to stay consistent when life interferes. You’ll also see how flexible repayment options, secure online payments, and steady advisory support can help you follow through with confidence.

Key Takeaways

- The avalanche method helps you regain control by prioritizing high-interest debt while keeping all other accounts protected.

- Reducing interest first lowers long-term pressure, even when balances take time to visibly decline.

- Sustainable payments matter more than aggressive goals, especially when income or expenses fluctuate.

- Secure online payments reduce missed deadlines and mental overload, helping you stay consistent month after month.

- Flexible repayment options and advisory support help you adjust without losing momentum or starting over.

What the Avalanche Method Means When You’re Overwhelmed with Debt

The avalanche method gives you a structured way to reduce debt when mental fatigue and financial pressure already feel constant. Instead of guessing where to send extra money, you follow a clear priority that protects your progress over time.

This strategy directs additional payments toward the debt with the highest interest rate while keeping all other accounts current. By reducing the most expensive balance first, you limit how much interest continues to work against you each month.

Here’s what the avalanche method requires in practical terms:

- List each debt with its balance, interest rate, and minimum payment

- Continue making all minimum payments to avoid further harm

- Apply any extra funds to the highest-interest balance

- Reallocate that payment after each balance is resolved

If organizing this feels intimidating, that reaction is understandable under sustained financial stress. Secure online payments help maintain consistency, while flexible repayment options allow adjustments without restarting your plan.

With a clear understanding of the method, the next step is learning how to set it up without increasing pressure or confusion.

Step-by-Step Instructions You Can Start Without Adding More Stress

Once you decide to use the avalanche method, the real challenge becomes following through while managing daily financial pressure.

These steps are designed to help you move forward without creating additional anxiety or unrealistic expectations.

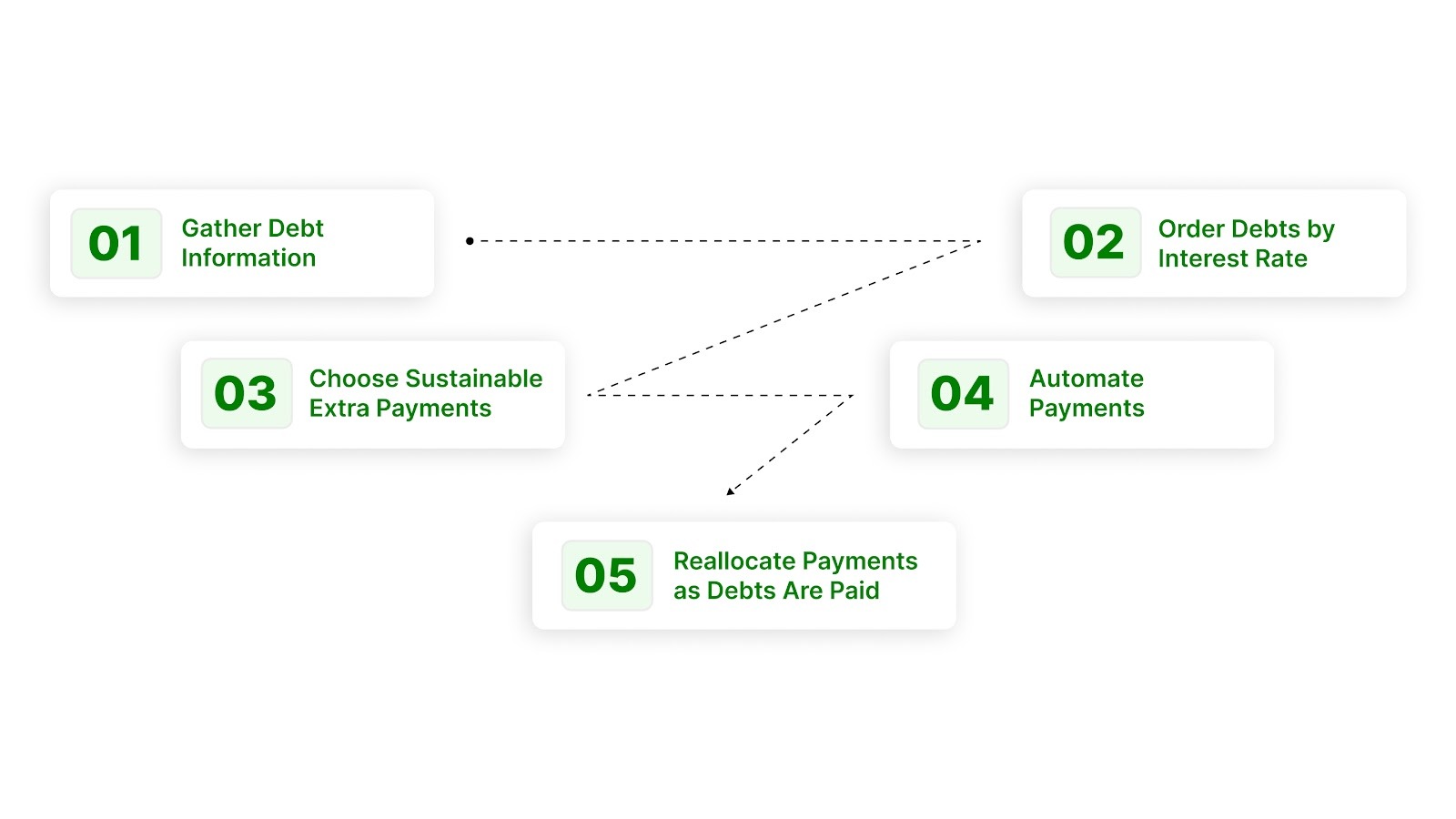

Gather Your Debt Information in One Place

Start by listing each debt with its balance, interest rate, minimum payment, and due date.

Seeing everything together can feel uncomfortable, but clarity reduces uncertainty and prevents costly oversights.

- Credit cards, personal loans, medical bills, and collections should all be included.

- Accuracy matters more than speed at this stage.

Order Debts by Interest Rate, Not Balance

Next, rank your debts from highest to lowest interest rate, regardless of how large or small they feel.

This step ensures your extra payments reduce the debt costing you the most over time.

- Highest interest goes first, even if the balance feels intimidating.

- Lower-interest debts stay protected with minimum payments.

Choose an Extra Payment Amount You Can Sustain

Decide on an extra amount that fits your current cash flow without pushing you into late payments elsewhere.

A smaller, reliable amount often works better than an aggressive number you cannot maintain.

- Consistency protects progress during stressful months.

- Flexible repayment options allow adjustments if income changes.

Automate Payments to Reduce Mental Strain

Set up secure online payments so your minimums and extra payments happen automatically each month.

Automation lowers the risk of missed payments and reduces the constant worry of tracking deadlines.

- One system replaces multiple reminders and alerts

- Secure payment tools help keep your plan stable

Reallocate Payments as Each Debt Is Paid Off

When your highest-interest debt is resolved, roll that full payment to the next highest interest balance.

This creates steady momentum without increasing your overall monthly commitment.

With these steps in place, the next section explores how theavalanche method compares to other strategies when emotional exhaustion is part of the equation.

Avalanche vs. Snowball When Emotional Exhaustion Shapes Your Decisions

At this stage, you may question whether saving the most money matters if staying consistent already feels difficult. That concern is valid, especially when stress and fatigue influence how long you can stick with a plan.

The avalanche and snowball methods differ mainly in what keeps you moving forward.

Understanding that difference helps you choose a strategy you can realistically maintain.

How the Avalanche Method Supports Long-Term Relief

The avalanche method prioritizes financial efficiency by reducing high-interest costs as early as possible.

This approach often leads to lower total debt costs, which can ease pressure over time.

- Less money lost to interest each month.

- Faster reduction of financial drag on your income.

- Stronger protection when balances take longer to decline.

How the Snowball Method Affects Motivation

The snowball method focuses on paying off smaller balances first to create quick wins.

Those early payoffs can feel encouraging, especially when confidence feels low.

- Faster visible results.

- Emotional momentum early on.

- Less emphasis on interest savings.

Choosing What You Can Sustain Under Stress

When exhaustion is part of your reality, the best method is the one you can follow consistently. Some people need emotional momentum first, while others need financial relief to feel stable again.

Flexible repayment options can support either approach by adjusting payments when life interferes. Secure online payments also reduce friction, helping you stay consistent regardless of the method you choose.

Once you decide which strategy fits your emotional and financial capacity, the next section addresses common obstacles that can disrupt progress.

Common Roadblocks That Can Disrupt the Avalanche Method

Even with a clear plan, real-life financial pressure can interrupt progress and make the avalanche method feel harder to sustain. Understanding these roadblocks helps you respond calmly instead of abandoning a strategy that still serves your long-term stability.

When Income Changes or Expenses Spike

Unexpected costs or reduced income can quickly limit your ability to make extra payments.

This situation does not mean the method failed; it means your plan needs short-term flexibility.

- Temporarily reduce extra payments while keeping minimums current.

- Adjust repayment expectations to match your current cash flow.

Flexible repayment options help you stay engaged with your plan without forcing unrealistic decisions during difficult months.

When You Miss or Fall Behind on a Payment

Missed payments often trigger shame, which can lead to avoidance and deeper financial setbacks.

Addressing the issue early helps limit damage and restores a sense of control.

- Resume minimum payments as soon as possible.

- Set up secure online payments to reduce the risk of repeat misses.

Consistency, not perfection, keeps the avalanche method working over time.

When Progress Feels Too Slow to Matter

High-interest debts may take time to visibly decline, which can weaken motivation.

This stage often feels discouraging, even when the strategy is doing its job behind the scenes.

- Track interest savings, not just balance reductions.

- Focus on monthly follow-through instead of short-term results.

Progress during this phase is quiet but meaningful.

When Collection Pressure or Legal Risk Appears

Accounts in collections or the threat of wage garnishment can quickly intensify stress.

These moments require structure, prioritization, and professional guidance.

- Identify debts with immediate legal or income consequences.

- Seek advisory support to protect stability and prevent escalation.

With these challenges addressed, the next section explains how ongoing support and structured payment systems help you stay on track long term.

Turning Your Plan Into Monthly Action With the Right Support

The avalanche method only works when it becomes part of your monthly routine, not another task competing for attention. When stress is high, reliable systems matter more than discipline or constant follow-through.

Secure online payments create consistency by removing timing decisions and reducing the risk of missed deadlines. When payments run automatically, you regain mental space and lower the chance of avoidable setbacks.

- Automated payments keep minimums and extra payments on schedule.

- Secure systems protect your information while reducing errors.

Consistency becomes easier when your plan allows room for real-life changes.

Flexible repayment options let you adjust payments during tight months without undoing progress. Instead of stopping entirely, you can scale responsibly and return to your plan when stability improves.

- Payment amounts can adapt to temporary income shifts.

- Small adjustments help preserve long-term momentum.

Advisory support provides clarity when choices feel overwhelming.

With guidance, you can prioritize confidently and keep moving forward without second-guessing every decision.

With these systems in place, the next section focuses on tracking progress realistically and staying engaged over time.

Next Steps When the Avalanche Method Needs Extra Support

There may come a point when strategy alone does not feel sufficient, especially if pressure continues to build. That moment does not signal failure; it signals a need for added structure and guidance.

If payments feel fragile or balances stop moving, support can help stabilize your plan before setbacks escalate. Advisory guidance provides clarity when choices feel overwhelming or consequences feel high.

- Review your repayment structure to identify hidden strain points.

- Reprioritize debts if collections or legal risk increases.

Support works best when paired with tools that reduce friction and protect consistency.

Secure online payments help you maintain control during stressful periods, even when attention feels divided. Flexible repayment options allow you to respond to short-term challenges without undoing months of progress.

When the avalanche method is reinforced with the right support, it becomes sustainable instead of exhausting. That stability creates space to focus on long-term recovery, not constant crisis management.

Conclusion

Living under constant financial pressure can make every decision feel heavier than it should, especially when debt never seems to move. You may feel tired of juggling balances, worried about mistakes, and unsure whether your efforts are actually leading anywhere.

The avalanche method gives you a way out of that cycle by replacing uncertainty with structure and focus. By prioritizing high-interest debt, using consistent payment systems, and adjusting when life changes, progress becomes steady and measurable.

With the right support, debt repayment stops feeling like a personal failure and starts feeling like a plan you can trust. Forest Hill Management helps you simplify payments, stay flexible during tough months, and make confident decisions without carrying the burden alone.

Contact our financial advisors for personalized support.

FAQs

1. Is the avalanche method better if I’m already behind on payments?

The avalanche method can still work if you’re behind, but stability comes first.

You’ll want to protect essential payments and address urgent accounts before aggressively targeting interest.

2. Does the avalanche method work with collections or medical debt?

Yes, but prioritization matters more when collections are involved.

Advisory guidance helps you decide which debts require immediate attention to reduce risk and stress.

3. How much extra should I pay using the avalanche method?

There is no “correct” number; sustainability matters more than speed.

A smaller, consistent extra payment often works better than an aggressive amount you cannot maintain.

4. What if my income changes while using the avalanche method?

Income changes do not mean the plan failed; they mean it needs adjustment.

Flexible repayment options allow you to scale payments without undoing progress or falling further behind.

5. Is the avalanche method emotionally harder than the snowball method?

It can feel slower at first because balances may not drop immediately.

However, reducing interest pressure often brings long-term relief that feels more stable and predictable.