Consumer Collections Explained: Rights, Process & Solid Next Steps

Need Help Reviewing Your Account?

Contact UsA consumer collection notice rarely arrives with clear explanations. It often shows up as a missed call, a short letter, or a balance that doesn't quite make sense at first glance.

In that moment, you may hesitate to respond, unsure what's required of you, what questions you're allowed to ask, or how to move forward without making things harder.

This guide is meant to steady that moment and give you clear, practical direction you can trust.

Key Takeaways

- Consumer collections are about communication and clarification, not immediate legal action

- You have defined rights around contact, privacy, and written information

- Most collection situations allow time to review details before decisions are made

- Clear, consistent information helps reduce confusion and unnecessary stress

- Resolution paths vary, and sustainable options exist based on individual circumstances

Here's What Consumer Collections Means In Simple Terms

Consumer collections means you’re being contacted about a personal or household account that is considered past due. This could involve a credit card balance, medical bill, utility charge, or another everyday financial obligation. At this stage, the contact is about addressing an unpaid account, not a judgment, and not a final outcome.

There are several common reasons you might hear from a collection company. A payment may have been missed, an account may have moved from the original creditor to a third party for communication purposes, or follow-up may be needed to confirm balance details and repayment status. Being contacted does not, by itself, mean the situation has reached a legal phase.

Important clarification: a consumer collection notice does not automatically mean you are being sued. Legal action and wage-related orders follow separate procedures and typically involve additional notices and formal steps before anything is enforced.

What Do Consumer Collections Often Look Like in Practice?

- A written notice asking you to review an unpaid balance

- A phone call or voicemail requesting a return call

- A letter listing the creditor, amount owed, and contact details

- Information about payment options or the ability to discuss repayment

At this point, the focus is usually on confirming the details of the account and outlining ways it may be resolved. Understanding what this stage represents can help you respond thoughtfully, without rushing or assuming the worst.

The First 48 Hours After You’re Contacted

The first day or two after a consumer collections contact is less about taking action and more about setting the situation up correctly.

What you do, or don’t do, during this window can determine whether the process feels manageable or confusing later on. Rushing to respond without clarity often leads to mistakes, while slowing things down helps you keep control.

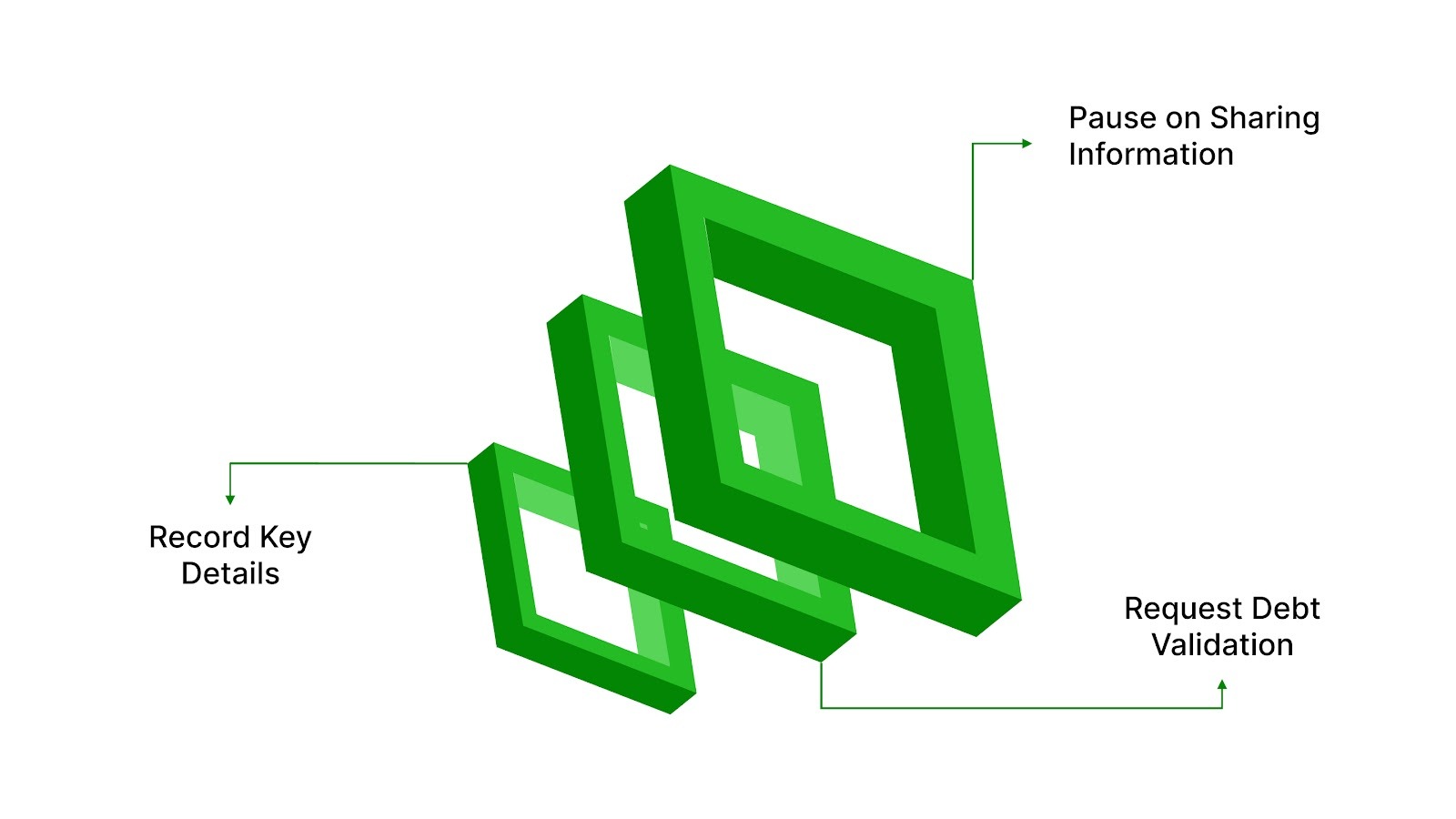

Step 1: Don’t Share Sensitive Information Too Fast

It’s reasonable to want the situation resolved quickly, but the first contact is not the moment to confirm personal or financial details. Until you understand who is contacting you and why, it’s appropriate to pause on sharing information that could be misused or misunderstood.

Information to hold back at this stage includes:

- Social Security number or partial SSN

- Bank account or debit card details

- Employer or payroll information

What is safe and useful is asking basic identifying questions. A legitimate collection contact should be able to clearly explain:

- The name of the company contacting you

- A mailing address where they can be reached

- The name of the creditor connected to the account

- The total balance they are referencing

These questions help you confirm that the communication is real and relevant before the conversation goes any further.

Step 2: Write Down Six Details Before You Respond Further

Collection situations can feel overwhelming because information arrives in pieces. Writing things down early creates a record you can rely on later, especially if you're contacted more than once or need time to review your options.

Before returning a call or responding in writing, note:

- The date and time of the contact

- The name of the person or company that reached out

- The phone number, email, or address used

- Any account or reference number provided

- The creditor name associated with the balance

- What the caller or letter said the next step would be

This isn’t about preparing for conflict; it’s about staying organized, so you’re not relying on memory during a stressful moment.

Step 3: Ask for the Validation Information

One of the most important early steps is requesting what’s commonly called validation information. In plain terms, this is written confirmation that explains the debt being referenced and who is authorized to collect it. Asking for this information is a normal part of the process and helps prevent confusion or errors.

Validation information typically includes:

- The name of the company collecting the debt

- The name of the original creditor

- The amount claimed as owed

- Instructions on how to dispute or ask questions about the debt

Receiving this information gives you a clear starting point. It allows you to review the details on your own time, confirm whether the account is accurate, and decide how you want to move forward, without pressure to respond immediately.

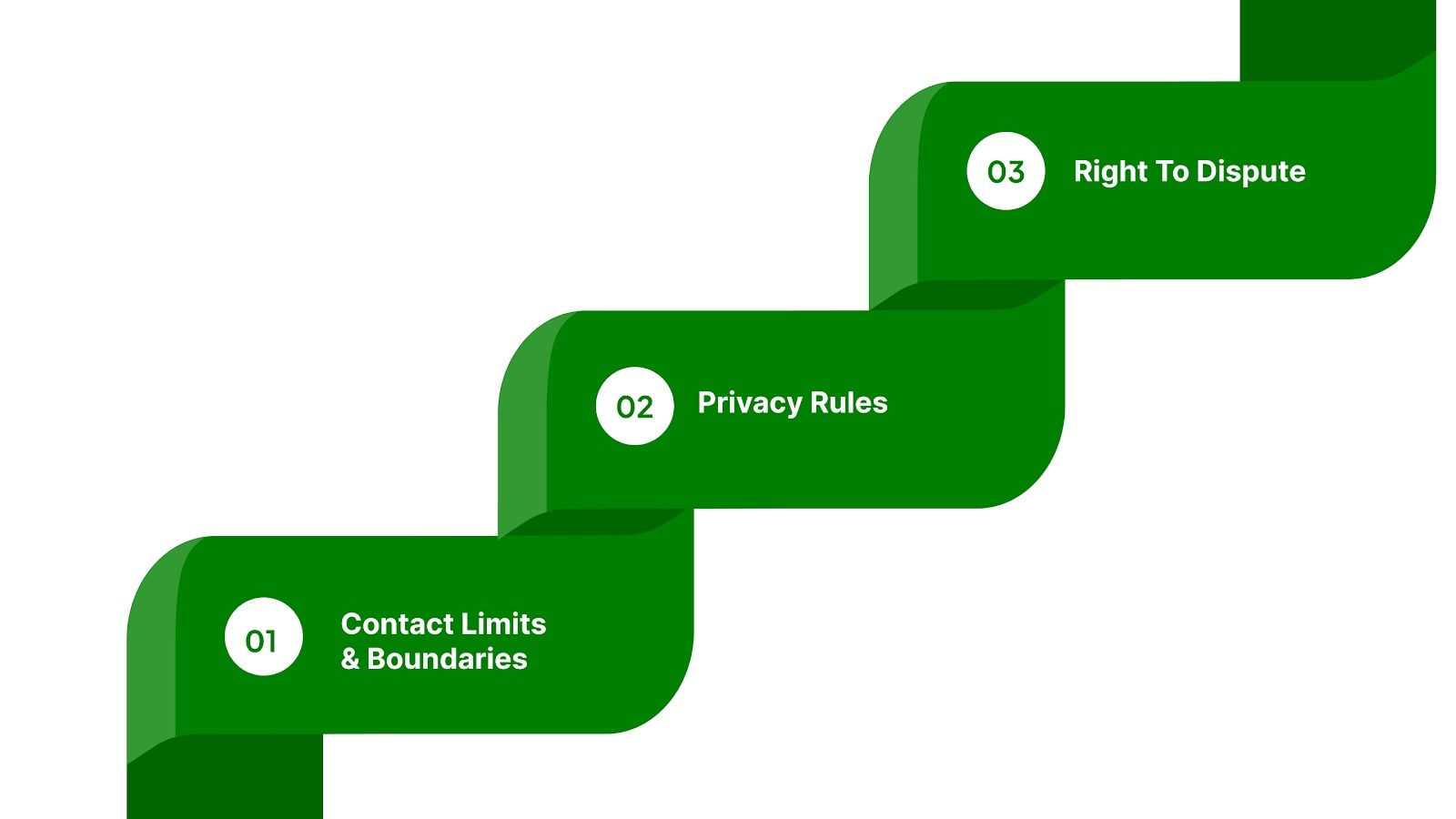

Your Core Rights During Consumer Collections (Without the Legal Speak)

When you’re contacted about a debt, you don’t lose control of the situation. U.S. consumer protection rules set clear boundaries around how collection communication works, and those boundaries exist to protect your time, privacy, and ability to respond thoughtfully.

Understanding these rights early can help you separate what’s allowed from what feels unsettling but isn’t actually required of you.

a) Contact Limits and Communication Boundaries

Collectors must contact you during reasonable hours (no early morning or late-night calls). Repeated calls meant to pressure or overwhelm you are not allowed. You can also request that they stop calling you at work if it’s prohibited by your employer or creates discomfort. Setting these boundaries helps ensure communication is manageable and non-disruptive.

b) Privacy Rules: Who They Can and Can’t Talk To

Collection communication is private. A collector can’t discuss your debt with family, coworkers, or employers. They may contact others to verify basic details but cannot disclose your debt. These rules protect your privacy and prevent unnecessary embarrassment.

c) The Right to Dispute and Ask for Proof

You have the right to request written verification of the debt within 30 days of first contact. Disputing the debt doesn’t mean you're refusing to pay; it just means you're asking for clarity. Once disputed, collection activities should pause until verification is provided.

At this stage, you are allowed to:

- Ask for proof that the debt is accurate

- Correct errors or missing information

- Request that details be provided in writing

Using these rights isn’t confrontational. It’s a normal part of navigating consumer collections with clarity and confidence.

How Consumer Collections May Affect Your Credit Report

When you're contacted about a consumer collection, it's natural to be concerned about how it might impact your credit. Collection accounts can have a significant effect on your credit score, but understanding the process and how to manage it can give you control over the outcome.

Here's what you need to know:

- Initial Reporting: When a debt is handed over to a collection agency, it is often reported to the credit bureaus. This can show up as a negative mark on your credit report and can lower your credit score. However, not all collections are immediately reported, and the timing can vary depending on how the creditor and collection agency handle the account.

- Impact on Credit Score: The severity of the impact will depend on the type of debt, the amount owed, and how long the debt has been outstanding. A collection account can reduce your score by 50–100 points or more, especially if it’s a high-balance or long-standing account. The earlier in the collections process it’s reported, the more it will affect your score.

- Debt Settlement and Recovery: If you manage to settle the debt or make a full payment, the collection account may be marked as "paid" or "settled." This doesn't entirely remove the negative mark from your credit report, but it does show that the issue has been resolved. It’s crucial to request written confirmation that the account has been updated.

- Time and Credit Repair: Collection accounts typically stay on your credit report for seven years from the original delinquency date, even if the debt is paid off. However, after this period, it will be removed, and your score may start to recover. Over time, as you establish good credit behavior, the negative effect of the collection account can diminish.

- The Role of Creditors: Some creditors may be willing to work with you to remove the collection from your report once the debt is settled. This is called a “pay for delete” agreement, though it’s not always guaranteed or standard practice.

What You Can Do Now?

- Verify the Debt: Before making any payments, make sure the debt is accurate and truly yours. Request validation information from the collection agency and check your credit report.

- Request Removal: After settling or paying the debt, ask the collection agency or creditor to remove the account from your credit report as part of the agreement.

- Monitor Your Credit: Regularly monitor your credit report to ensure all information is correct and reflects the status of your debt.

Understanding the long-term effects of consumer collections on your credit report and proactively managing your debt can help you rebuild your credit score over time. Avoiding missed payments and addressing collections quickly can prevent further damage and set you on the right path.

How to Tell if a Collections Contact Is Legit (Quick Scam Filter)

Not every collection's contact feels the same, and it can be hard to tell what deserves attention and what deserves caution. A legitimate collection effort is usually structured, documented, and willing to slow down.

Questionable contacts often rely on urgency or confusion to push you into a response before you’ve had time to think.

This quick filter recognizes patterns that help you decide how to proceed.

Green Flags (Usually Legit)

Legitimate collection contacts tend to be consistent and transparent. You’re not expected to take anything on trust alone.

Common signs include:

- Written details are offered without resistance, either immediately or after you ask

- The creditor is clearly named, along with the company contacting you

- Dispute or question instructions are explained, not avoided

- Professional contact channels are used, such as a business phone number or mailing address

These signals don’t mean you need to agree or pay right away. They simply indicate that the contact can be verified and reviewed calmly.

Red Flags (Slow Down)

Some contacts rely on pressure rather than clarity. When that happens, it’s reasonable to pause before responding further.

Situations that warrant extra caution include:

- Pressure to pay “right now” or claims that delay will automatically make things worse

- Refusal to provide information in writing, even after you ask

- Requests for unusual payment methods, such as gift cards, wire transfers, or peer-to-peer apps

- Threats of serious outcomes that aren’t explained clearly or backed up in writing

These behaviors don’t require confrontation. They’re simply signals to slow the process down, document what’s happening, and ask for written confirmation before taking any next step.

Most legitimate consumer collection situations can withstand time, questions, and documentation. If a contact discourages all three, that’s your cue to pause and reassess before moving forward.

If the Debt Is Yours, Here’s How to Pick a Realistic Way Forward

Once you’ve reviewed the details and confirmed the account is yours, the decision isn’t just whether to pay, it’s how to move forward in a way you can actually maintain. The right choice depends on timing, cash flow, and clarity around the balance, not pressure or assumptions about what you “should” do.

This stage is about choosing a path that reduces uncertainty and keeps the situation from resurfacing later.

Option A: Pay in Full (When It’s Actually Possible)

Paying the full balance at once can make sense when the amount is manageable and won’t disrupt essential expenses. For some people, this is the simplest way to close the account and move on, but only if it’s truly affordable.

Before paying in full, it’s reasonable to confirm:

- The exact payoff amount being accepted

- That the payment will be applied to the correct account

- How and when the balance will be updated after payment

After payment, ask for written confirmation or a receipt showing the updated balance. This creates a clear record and avoids confusion later.

Option B: Flexible Repayment Plan (The Most Common Path)

When paying in full isn’t realistic, a structured repayment plan is often the next step. A structured plan simply means agreeing to a predictable amount on dates you can meet, nothing more complicated than that.

A helpful way to choose a monthly amount is to start with what you can commit to consistently, not what feels optimistic in the moment. A smaller, reliable payment is usually more effective than a larger one that becomes difficult to maintain.

Before agreeing to a plan, it’s appropriate to ask:

- The payment amount and due dates

- Whether any fees or interest apply during the plan

- How payments will be applied to the balance

Clear answers upfront help you avoid surprises and keep the plan on track.

Option C: If You Can’t Pay Yet (What to Do Instead)

Sometimes, the right move is not choosing a payment option immediately. If your finances need review or the balance details still feel unclear, it’s reasonable to pause before committing.

In this situation, you can:

- Ask for a clear written breakdown of the balance

- Request clarity on what the next steps would be if no payment is made right away

- Set a specific time to revisit the decision after reviewing your budget

Taking time to assess doesn’t mean ignoring the situation; it means responding thoughtfully instead of reactively.

How Forest Hill Management Helps at This Stage

At this point in the process, clarity matters more than speed. Forest Hill Management supports consumers by clearly outlining balances, explaining available repayment paths, and helping identify next steps that align with individual circumstances.

Secure online payment options are available for those who prefer visibility and control, and structured account resolution options are explained clearly, helping consumers understand available paths and make informed decisions.

The goal is to help you choose a way forward that you can sustain with confidence.

Also Read: What Happens If You Miss a Payment on Consumer Easy Credit?

Wage Garnishment Concerns & What Typically Happens Before That Point

Wage garnishment is one of the most common fears people associate with consumer collections, but it’s important to understand that it is not an immediate outcome. Garnishment generally comes later in the process and involves additional steps, notices, and formal procedures before it can occur.

In most situations, collection activity begins with communication, calls, letters, or notices meant to clarify an unpaid balance and outline possible ways to address it. Wage-related actions usually require separate legal steps and do not happen without warning or documentation.

Knowing this can help you respond thoughtfully instead of assuming the most severe outcome is already underway.

If You Receive Court-Related Paperwork

Court documents feel serious because they are. If you receive paperwork that appears to come from a court, it’s important not to ignore it, even if the language feels confusing or overwhelming.

At that point, focus on a few practical steps:

- Read the document carefully to understand deadlines

- Respond within the timeframe listed, even if you’re unsure what to say

- Seek guidance or support if you don’t understand what’s being requested

Responding on time helps preserve your options. Ignoring court-related notices can limit your ability to address the situation later.

How Early Communication Can Help Reduce Escalation

Many collection situations are resolved before they reach a legal stage. Clear communication and timely discussions about repayment, when possible, can sometimes prevent matters from progressing further. This doesn’t mean outcomes are guaranteed, and it doesn’t mean every situation can be resolved the same way.

What it does mean is that understanding your options early, asking questions, and exploring realistic repayment paths can reduce uncertainty and help keep the process focused on resolution rather than escalation.

If wage garnishment is a concern for you, addressing the situation sooner, rather than waiting in silence, often provides more room to respond calmly and deliberately.

Simple Scripts You Can Use (So You Don’t Freeze on the Phone)

When you’re contacted about a debt, it’s easy to feel caught off guard. You don’t need the perfect words or detailed knowledge to respond appropriately. These short scripts are designed to help you slow the conversation down, gather information, and protect your ability to decide what comes next.

Use them as-is, or adjust the wording so it feels natural to you.

Script 1: “I Need This in Writing”

“I want to make sure I understand everything correctly.

Could you please send the details of this account to me in writing?

That will help me review the information and respond appropriately.

What’s the best mailing address or email to expect that from?”

Script 2: “I Don’t Recognize This Debt”

“I don’t immediately recognize this account.

Before we go further, I’d like to review the written details about the debt.

Please include the creditor name and the balance you’re referencing.

Once I receive that, I can look it over and follow up.”

Script 3: “I Want a Repayment Plan I Can Actually Maintain”

“I’m open to resolving this, but I need to understand my options first.

I’d like to discuss a payment plan that fits my current situation.

Can you explain what repayment options are available and how payments would be applied?

I want to be sure I’m agreeing to something I can keep up with.”

Script 4: “Do Not Contact Me at Work”

“I’m not able to receive calls or messages at work.

Please don’t contact me there going forward.

You can reach me through the contact information we’ve already discussed.

Thank you for noting that.”

These scripts aren’t about avoiding responsibility or creating conflict. They’re simply tools to help you stay clear, calm, and informed, especially in moments when it’s hard to think on the spot.

A One-Page Consumer Collections Checklist

This checklist is designed to help you stay organized and make decisions calmly, even if the situation feels stressful.

You don’t need to complete everything at once; use it as a guide to keep track of what matters.

Before You Pay Anything

- Confirm who is contacting you and why

- Review the balance details carefully

- Make sure you understand which account the payment would apply to

- Avoid sharing sensitive financial information until details are clear

What to Request in Writing?

- The name of the creditor connected to the account

- The total balance being claimed

- Instructions for asking questions or disputing the debt

- Any repayment options being offered

What to Track for Your Records?

- Dates and times of calls or letters

- Names of companies or representatives you speak with

- Phone numbers, email addresses, or mailing addresses used

- Any reference or account numbers provided

Keeping simple notes can help prevent confusion if you’re contacted again.

What to Do if the Balance Looks Wrong?

- Ask for a written breakdown of the amount

- Compare it with your own records or statements

- Dispute the part that doesn’t look accurate, if needed

- Take time to review before agreeing to anything

What to Do if You’re Worried About Escalation?

- Read all notices carefully instead of setting them aside

- Pay attention to deadlines mentioned in writing

- Respond on time, even if your response is a request for clarification

- Seek support if you receive documents you don’t understand

When Secure Online Payment Helps You Stay Consistent

- When you want clear visibility into payments and balances

- When making payments on a predictable schedule

- When you prefer confirmation and records, you can access them later

Having a clear, organized approach can make consumer collections feel less overwhelming and easier to manage step by step.

How Forest Hill Management Supports You

Consumer collections can feel confusing when information arrives in pieces, and the next steps aren’t clearly explained.

Forest Hill Management’s role is to bring structure and clarity to the process, so you can understand your situation and make informed decisions without added pressure.

Helps You Understand Where You Stand

Forest Hill helps make account details easier to follow by clearly outlining:

- Which account is being discussed

- What the current balance represents

- What options are available moving forward

This clarity helps reduce guesswork and allows you to focus on the next steps with confidence.

Protects Your Rights and Your Privacy

Forest Hill relies on compliance-focused processes and secure systems designed to follow U.S. consumer protection standards. In practice, this means:

- Communication that stays appropriate and respectful

- Contact that follows required boundaries

- Careful handling of personal and financial information

These safeguards are in place to help ensure your rights and privacy are respected throughout the process.

Gives You Control Through Secure Payments

When you’re ready to make a payment, secure online payment options provide:

- Clear visibility into balances and payment history

- Confirmation that payments are received and applied

- Records you can access later if questions come up

Having this visibility can make it easier to stay organized and consistent.

Supports Realistic Repayment Options

Forest Hill helps explain available account resolution options so consumers can choose arrangements that align with their circumstances. These plans are designed to:

- Set predictable payment amounts and dates

- Reduce pressure from uncertainty

- Support steady progress without overcommitment

The focus is on helping you choose a path forward that feels manageable and sustainable over time.

Suggested Read: 10 Successful Debt Collection Techniques for Maximizing Success

Conclusion

Dealing with consumer collections can feel uncertain at first, but clarity and steady steps make a real difference. When you understand what’s happening and what your options are, the situation becomes something you can address thoughtfully, not something that controls you.

Here’s what to keep in mind as you move forward:

- Consumer collections follow clear rules, and you have rights throughout the process

- Taking time to confirm details and choose a realistic path helps prevent added stress later

- Consistent, informed action is often more effective than rushing decisions

If you’re ready to take the next step, doing so calmly and deliberately can help bring relief and a sense of control back into the process. Contact our advisors for personalized support

FAQs

Q1. Can consumer collections affect my credit report?

A1. Consumer collections can be reported to credit bureaus, but reporting usually happens after initial contact or written notice. Reviewing the details early helps you understand what may be reported and when.

Q2. Should I talk to a debt collector or ignore the calls?

A2. Ignoring contact rarely makes the situation clearer. A short, controlled conversation, or requesting details in writing, often gives you more information and helps you decide next steps without pressure.

Q3. What happens if I pay a collections account?

A3. When you make a payment, it should be applied to the specific account discussed. It’s reasonable to request confirmation showing how the payment was applied and what the updated balance is afterward.

Q4. Can I be contacted about a debt I don’t recognize?

A4. Yes. Errors, outdated records, or similar names can lead to confusion. You have the right to request written details and review the information before taking any action.

Q5. How long do consumer collections usually last?

A5. There’s no single timeline. The length depends on factors like communication, whether the debt is confirmed, and whether a repayment plan is in place. Early clarity often helps shorten the process.