Understanding U.S. Consumer Debt Trends

Transform Your Financial Future

Contact UsMillions of Americans are carrying more debt than ever before. Total U.S. household debt hit $18.8 trillion in Q1 2026, and headlines keep framing this as a looming crisis. For many readers, though, this isn't an abstract statistic — it's the credit card balance that keeps growing, the car payment that stretches the budget, or the student loan bill that just reappeared after years of forbearance.

The full picture is more nuanced than the headlines suggest. Some debt categories are genuinely under stress. Others are holding up better than the numbers imply. And for the millions of Americans already struggling with past-due accounts, knowing the difference matters less than knowing what to do next.

This article breaks down what's actually driving U.S. consumer debt, where the real pressure points are, and what practical steps you can take if you're feeling the squeeze.

Key Takeaways

- U.S. household debt reached $18.8 trillion in Q1 2026, but debt service payments as a share of income remain well below 2008 crisis levels.

- Credit cards and student loans are the most stressed categories — auto loans show strain too, while mortgage delinquencies stay relatively contained.

- Rising prices and flat real wages are pushing more Americans toward revolving credit, not reckless spending habits.

- If you're behind on accounts, acting early (before default) preserves far more options than waiting.

Consumer Debt 101: What It Is and How It's Measured

Before interpreting any debt headline, it helps to know what's actually being measured. Two different reports dominate the coverage, and they're not measuring the same thing.

The two most cited sources are:

- Fed G.19 Consumer Credit: Tracks revolving debt (credit cards) and nonrevolving debt (auto, student loans). Excludes anything secured by real estate.

- NY Fed Household Debt and Credit Report: Pulls from actual consumer credit files to include mortgages, home equity lines, auto loans, credit cards, and student loans — a complete household balance-sheet picture.

This distinction matters when you read a headline claiming "consumer debt hits record." If the figure includes mortgages, it tells a very different story than if it only covers credit cards and auto loans. Most major news reports mix these terms without clarifying which measure they're using.

The Current State of U.S. Consumer Debt

The Headline Numbers

According to the New York Fed's Q1 2026 Household Debt and Credit Report, total U.S. household debt stands at $18.8 trillion, broken down as follows:

- $13.19 trillion — Mortgages (the largest share by far)

- $1.69 trillion — Auto loans

- $1.66 trillion — Student loans

- $1.25 trillion — Credit cards

- $446 billion — Home equity lines (HELOCs)

- $562 billion — Other consumer debts

The credit card figure gets the most attention. At $1.25 trillion, it sounds alarming, but it reflects both more cardholders and higher prices on everyday purchases, not people spending beyond their means. Inflation-adjusted, per-cardholder balances remain close to pre-pandemic levels.

Where the Real Stress Lives

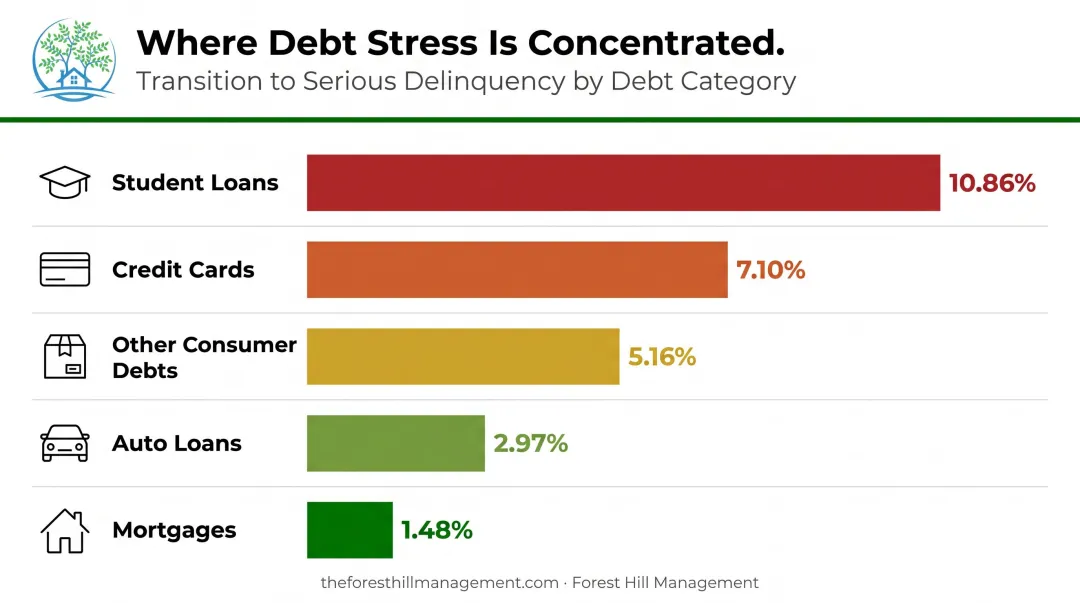

Not all debt categories are under equal pressure. Delinquency flows (the rate at which balances transition into serious delinquency, 90+ days past due) vary sharply by product type:

- Student loans: 10.86% annualized serious-delinquency transition rate

- Credit cards: 7.10%

- Other consumer debts: 5.16%

- Auto loans: 2.97%

- Mortgages: 1.48%

Auto loan balances remain elevated partly because vehicle prices are too. Kelley Blue Book reported the average new vehicle transaction price at $49,220 in May 2026, up 1.2% year over year, which stretches monthly payments for millions of borrowers.

These stress points are real — but they don't tell the whole story.

The Context That Gets Left Out

Despite the record nominal figure, the Federal Reserve's household debt service ratio stood at 11.16% of disposable personal income in Q1 2026 — compared to 15.78% during Q1 2008, at the height of the financial crisis. Households are carrying more debt in dollar terms, but they're devoting a smaller share of their income to servicing it than they were before the Great Recession.

That nuance doesn't eliminate individual hardship. It does mean that for most households, the path forward involves managing specific accounts — not weathering a systemic collapse like 2008.

What's Driving the Rise in Consumer Debt

The Inflation-Wage Gap

The core driver isn't reckless borrowing. It's a mismatch between what things cost and what paychecks cover. The BLS reported CPI-U up 4.2% for the 12 months ending May 2026, while real average hourly earnings fell 0.7% over the same period. Food, shelter, transportation, and healthcare (the four categories that dominate household budgets) all rose faster than wages.

When essential expenses outpace income, revolving credit fills the gap — not because of poor decisions, but because the math leaves few other options.

Interest Rates Compound the Problem

The Federal Reserve's rate-hiking cycle pushed credit card APRs to near-record levels. The Fed's G.19 report shows average APRs at 21.00% for all credit card accounts and 21.52% for accounts carrying a balance as of Q1 2026.

For the 46% of cardholders who carry a balance month-to-month (per the Fed's 2024 Economic Well-Being report), high APRs mean more of every payment goes toward interest — and the principal barely moves. At 21%, a $5,000 balance with minimum payments can take over a decade to pay off.

The Student Loan Wildcard

The most abrupt delinquency surge belongs to student loans. After years of federal forbearance that held default rates below historical norms, the Department of Education resumed collections on May 5, 2025. The results were immediate: 10.3% of student loan balances are now 90+ days delinquent, and the NY Fed's Liberty Street Economics analysis found the average borrower entering default after the pandemic pause was nearly 40 years old — not the recent college graduate most people picture.

These delinquencies ripple outward. Borrowers with scores in the 620–720 range are seeing significant credit score drops, which affects their ability to borrow for housing, vehicles, and emergencies.

Post-COVID Normalization

The current delinquency data also needs historical grounding. COVID-era stimulus — forbearance programs, economic impact payments, and near-zero interest rates — kept delinquency rates unusually low from 2020 through 2021. The current uptick partially reflects a return to pre-pandemic norms, not solely a new deterioration. Looking at delinquency rates against 2021 lows overstates the severity.

Delinquency Trends: Who Is Most at Risk

The Overall Rate

The delinquency rate on consumer loans at all commercial banks was 2.64% in Q1 2026 — above recent post-COVID lows, but near pre-pandemic historical norms. That average, though, obscures significant variation across borrower types and product categories.

Subprime Borrowers Bear the Heaviest Burden

Delinquency stress is concentrated among consumers with lower credit scores. The CFPB's 2025 credit card market report documented deteriorating card performance and rising charge-offs, with the pressure disproportionately hitting subprime borrowers.

Headline averages mask how badly this group is struggling. Aggregate delinquency rates are pulled down by the millions of borrowers who remain current — the distress at the bottom of the credit spectrum is far worse than the top-line figure suggests.

Mortgages: A Relative Bright Spot

The MBA reported a mortgage delinquency rate of 4.44% in Q1 2026 — elevated from post-pandemic lows, but the serious-delinquency transition flow sits at just 1.48%. The pandemic-era housing boom left most homeowners with substantial equity they didn't have before 2008. That equity gives borrowers the option to sell rather than default — a structural advantage that simply didn't exist before 2008, when negative equity trapped millions of homeowners with no exit.

What to Do If You're Struggling With Debt

Act Before the Account Goes to Collections

Most lenders — especially large banks and credit card issuers — have hardship programs, payment deferrals, or modified payment arrangements available. These options narrow significantly once an account charges off and moves to a collections stage. A single 30-day missed payment can drop a credit score by 60–110 points; waiting until 90+ days past due causes far greater damage and limits what any third party can do to help.

Call your lender before you miss a payment, not after.

Choose Your Repayment Strategy Based on Your Psychology

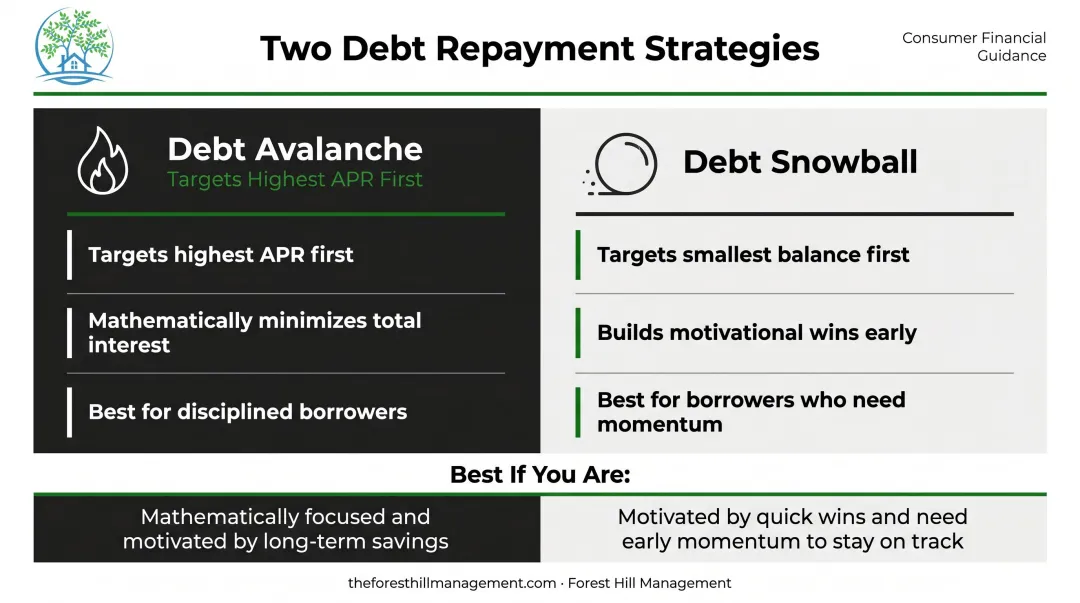

Two approaches dominate personal finance advice on debt repayment:

- Debt avalanche — Pay minimums on everything, then throw extra money at the highest-APR balance first. Mathematically optimal; minimizes total interest paid.

- Debt snowball — Pay minimums on everything, then attack the smallest balance first. Generates early wins that research published in the Journal of Marketing Research shows sustains motivation and improves follow-through.

Neither method works if you quit. For people who struggle with consistency, the snowball's psychological momentum often outperforms the avalanche's math. For people who are disciplined, the avalanche saves more money. Pick the one you'll actually stick with.

Work With a Receivables Management Organization for Past-Due Accounts

If your accounts are already past due or in collections, your priority shifts from optimization to damage control — stopping further credit score deterioration, avoiding wage garnishment, and getting onto a structured path forward.

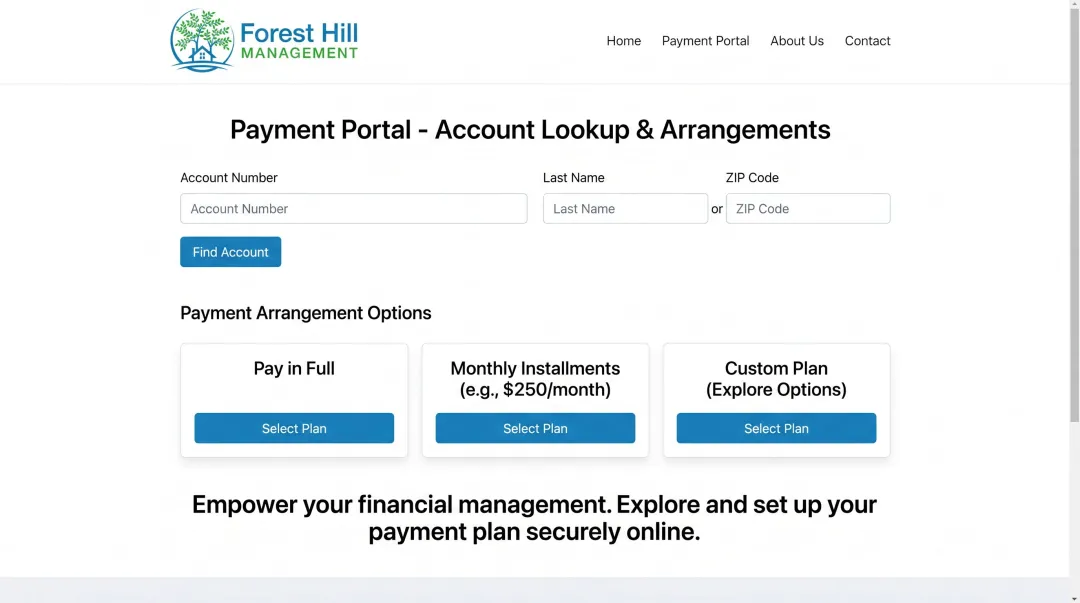

Forest Hill Management is a receivables management organization that specializes in helping consumers resolve past-due accounts. They work with you to verify the account, explain your options, and build a payment plan matched to your actual budget. Their online portal at pay.theforesthillmanagement.com lets you explore payment arrangements on your own schedule, and their team is reachable at (888) 471-0109 if you prefer to talk through your options directly.

They've assisted thousands of consumers in resolving obligations since 2020, and they operate under FDCPA and CFPB compliance frameworks — meaning you have formal dispute rights throughout the process.

Frequently Asked Questions

What kills credit scores fastest?

Late or missed payments — especially those 30+ days past due — cause the sharpest score drops, since payment history accounts for 35% of a FICO Score. High credit utilization, accounts entering collections, and loan defaults compound the damage quickly. Even one missed payment on an otherwise clean file can cause a significant drop.

What happens after 7 years of not paying debt?

Most negative information — late payments, charge-offs, collection accounts — falls off your credit report after 7 years under the Fair Credit Reporting Act. The underlying debt may still be legally owed depending on your state's statute of limitations, and federal student loans have no equivalent reporting time limit.

Is $40,000 in credit card debt a lot?

Experian reported the average U.S. credit card balance at $6,768 as of September 2025 — making $40,000 nearly six times that figure. At current APRs above 21%, the monthly interest alone exceeds $700, making structured repayment essential.

What's the difference between consumer debt and household debt?

Consumer debt covers non-real-estate borrowing: credit cards, auto loans, personal loans. Household debt is the broader category that adds mortgages and student loans. Most alarming "record debt" headlines refer to total household debt — a figure dominated by mortgage balances, which behave very differently from revolving consumer credit.

How do rising interest rates affect my existing debt?

Variable-rate debt — including most credit cards and some auto loans — reprices as rates rise. That means more of every payment goes toward interest and less reduces your principal. A rate increase from 18% to 21% can add hundreds of dollars in annual interest costs without any new spending.

What should I do if I can't make my minimum payments?

Contact your creditor immediately — most have hardship options that disappear once an account charges off. If your accounts are already past due, reaching out to a reputable receivables management organization like Forest Hill Management or a nonprofit credit counselor can help you map out a structured resolution path before the situation deteriorates further.