Latest Consumer Debt Insights and Strategies

Need Help Reviewing Your Account?

Contact UsHousehold debt in the U.S. now exceeds $18.6 trillion, yet reading that figure doesn’t immediately tell you what it means for your day‑to‑day decisions. Credit card balances alone surpass $1.23 trillion, highlighting pressures that go beyond numbers and touch how people live, spend, and plan.

Understanding these trends changes how you act. You see, debt isn’t just a line on a statement. It shapes choices about essentials, opportunities, and future security. With clarity, you gain perspective instead of reacting to alarming headlines.

Understanding consumer debt trends can turn abstract statistics into actionable insight. They translate balances, repayment timelines, and interest realities into steps you can take, giving you control over situations that might otherwise feel unmanageable. This isn’t about theory; it’s about decisions you can make today that ripple into tomorrow.

In this article, you’ll explore how consumer debt trends affect your finances and learn strategies to regain control with confidence.

Key Takeaways

- Rising costs and stagnant wages are widening the gap, making it harder to keep up with debt, especially when unexpected emergencies arise.

- Debt collection tactics are shifting from aggressive calls to digital reminders, giving consumers more control over how they're contacted.

- Focus on high-interest debts first, like credit cards, to cut down on interest and pay off debt faster.

- Addressing debt early and using digital tools for tracking can prevent further complications and costly fees.

- Forest Hill Management offers flexible, transparent solutions customized to your financial needs, guiding you towards better debt management.

Current State of Consumer Debt in the United States

Credit card interest rates are at historically high levels, with average APRs exceeding 20%, making balances more expensive to carry. U.S. households often manage multiple forms of revolving debt, including credit cards, personal loans, and medical bills.

This creates a fragile financial ecosystem where missed payments can ripple across accounts. Delinquency rates have risen from pandemic lows, reflecting growing financial stress, though precise age-specific trends are less clear.

These pressures affect how Americans manage credit today:

- Higher interest burden: More of each payment goes toward interest, slowing debt repayment even for consistent payers.

- Tighter credit conditions: Some lenders have reduced credit limits or tightened access, increasing utilization ratios.

- Rising costs of missteps: Late fees, over-limit charges, and returned payment fees can add up quickly, compounding financial strain.

Even households making a consistent effort to stay current are feeling the effects, highlighting the importance of clear budgeting, realistic repayment strategies, and careful debt management.

Why More Consumers Are Falling Behind on Payments

When income stays flat but everything else rises, the math stops working. You’re not spending recklessly; everyday expenses have increased by roughly 15-18% over the past three years. Let’s break down the main reasons this gap keeps growing:

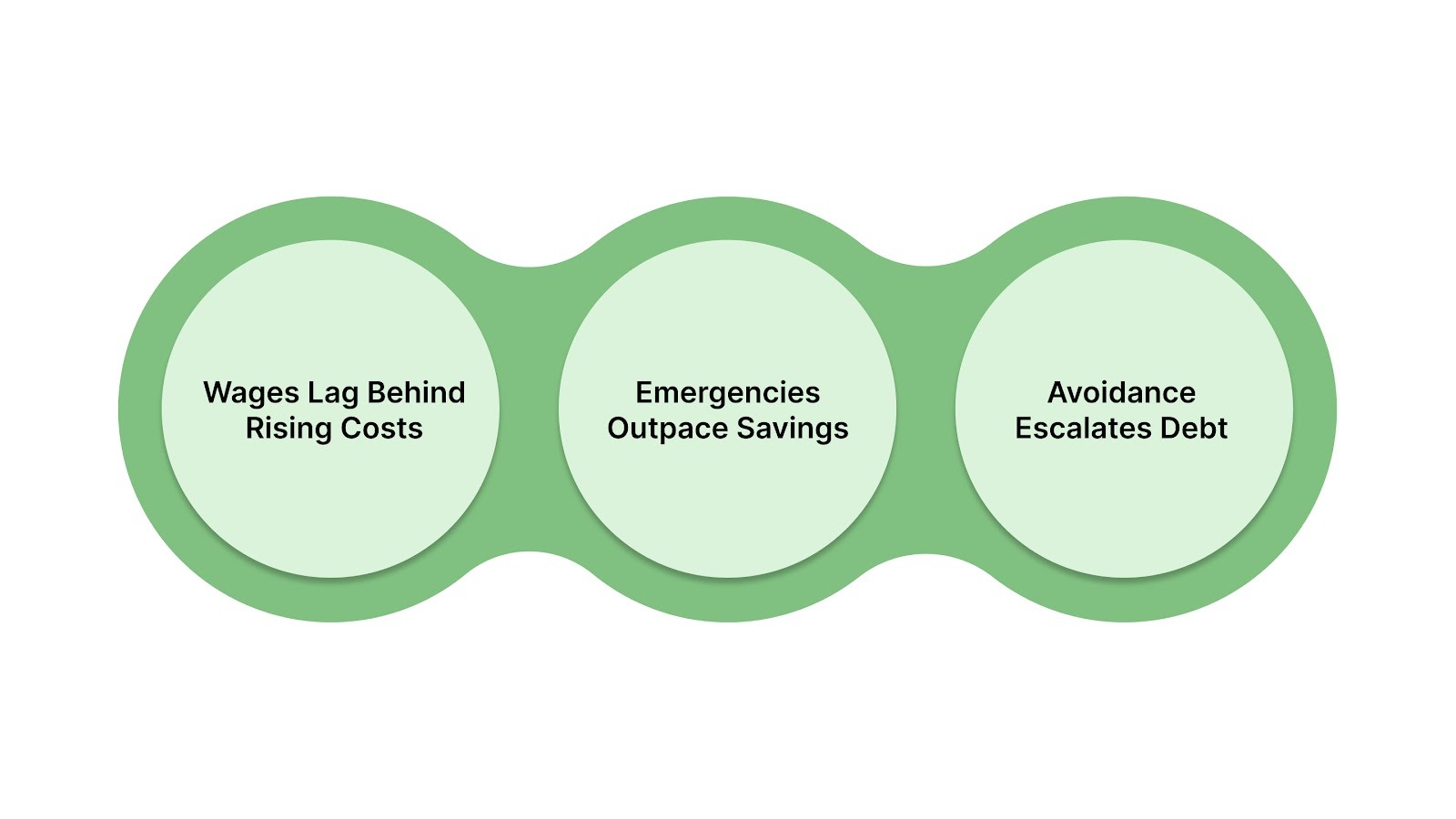

1. Wages Lag Behind Rising Costs

Rent, groceries, utilities, and insurance have all increased faster than most people's paychecks. A salary that felt sufficient in 2021 may now require difficult trade-offs between prescriptions and car repairs, or a broken appliance and a full credit card payment. The gap appears in your checking account balance every month.

2. Emergencies Outpace Savings

A transmission failure. A root canal. A layoff that lasts three months instead of three weeks. Most households (nearly 7 in 10) operate with less than $1,000 in accessible savings, which means any unexpected expense immediately becomes debt.

Once you're using credit cards for emergencies instead of discretionary purchases, the balance grows faster than you can pay it down, even when things stabilize.

3. Avoidance Escalates Debt

When opening mail or checking balances triggers anxiety, it's easier to just stop looking. You know ignoring the problem doesn't fix it, but the mental weight of confronting mounting numbers feels unbearable in the moment.

Also Read: Understanding Consumer Debt and Its Impact on Your Credit Score

This pattern is common and understandable, but it also means accounts escalate from late to seriously delinquent while you're still telling yourself you'll handle it next month.

How Collection Practices Are Evolving

The way creditors and account managers communicate with consumers has fundamentally changed, driven by both regulation and recognition that outdated tactics don't produce results.

You're less likely to receive aggressive phone calls and more likely to interact through digital channels that give you time to think and respond on your terms.

Here's what that shift looks like in practice:

- Text and email reminders replace repeated calls: Many companies now send payment reminders and account updates digitally, reducing the pressure of unexpected calls during work or family time.

- Online portals provide 24/7 account access: You can check balances, review payment history, and make arrangements anytime without waiting on hold or explaining your situation repeatedly to different representatives.

- Regulations limit contact frequency and methods: The CFPB's 2021 Debt Collection Rule caps calls at seven per week and requires creditors to honor your communication preferences. This gives you more control over how and when you're contacted.

- Payment plan discussions increasingly happen earlier: Rather than waiting for accounts to reach legal stages, many organizations now offer structured repayment options while accounts are still recent, preventing escalation before it starts

Also Read: Best Finance Advisory Service Providers for Debt Management

These changes don't eliminate the stress of owing money, but they create pathways that feel less confrontational and more focused on finding solutions.

Practical Strategies for Managing Debt in Today's Environment

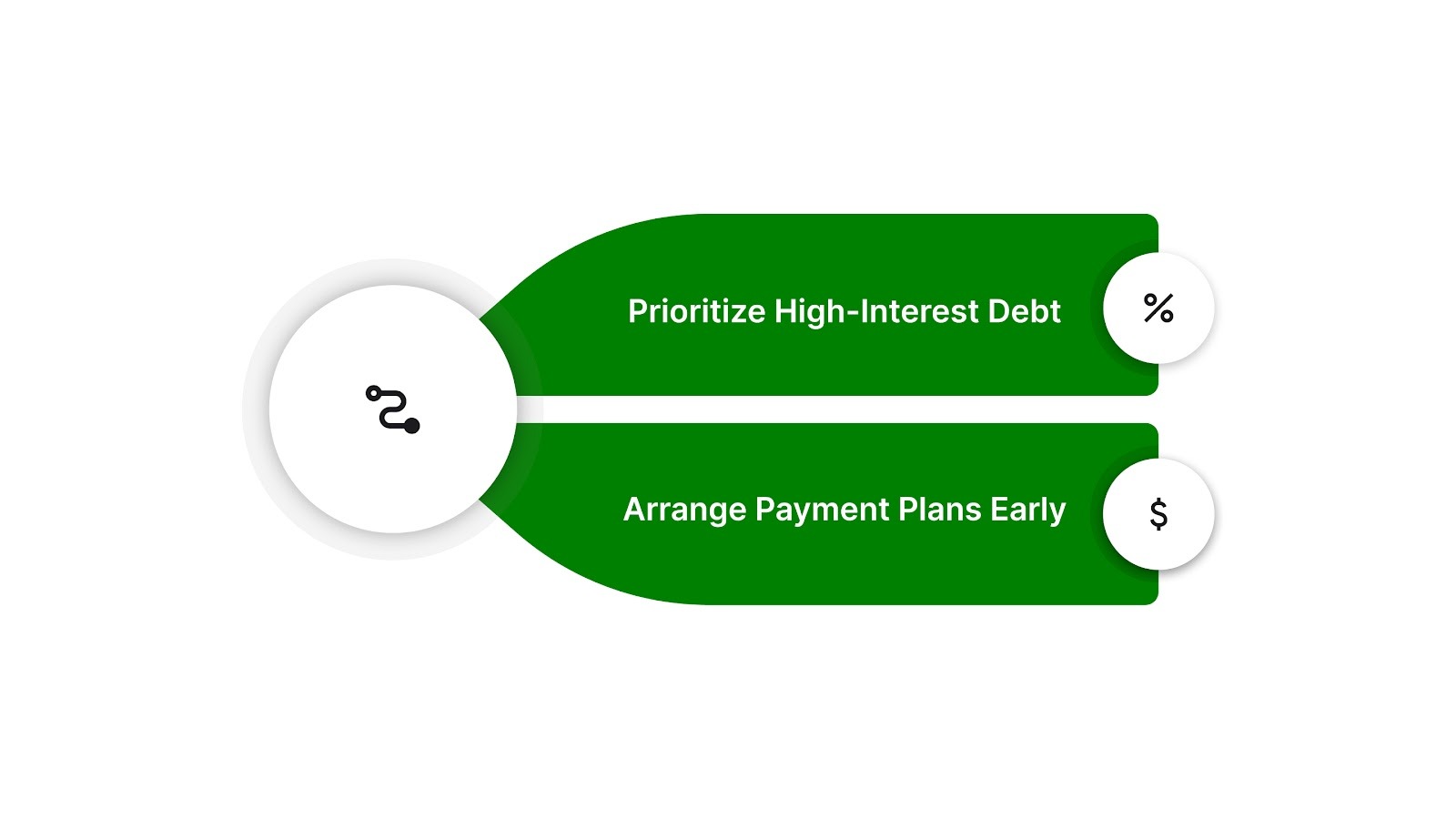

Effectively managing debt today involves prioritizing high-interest debts, arranging early payment plans, and using digital tools to track progress. Here's how to put these strategies into action.

1. Prioritize High-Interest Debt

A $5,000 credit card balance at 24% APR generates $100 in interest every month before you've paid down a single dollar of what you actually borrowed. That's $1,200 a year just maintaining the debt.

Compare that to a car loan at 6% or a medical bill at 0%, and the difference becomes clear: the highest interest rates drain your financial capacity fastest.

Directing extra payments toward these accounts first, even $50 or $100 beyond the minimum, reduces the total interest you'll pay and shortens the timeline to being debt-free.

2. Explore Payment Plan Options Early When Available

Contact creditors while your account is still in the early stages of delinquency. Most are willing to offer flexible payment plans before legal actions or collections, which could save you money and stress.

Track Progress with Secure Tools

Use digital tools to monitor your payments and balances in real time. Having that information readily available removes the guesswork and lets you plan with confidence instead of constantly wondering where you stand.

Also Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2026 Update)

Given the evolving challenges consumers face, it's essential to work with companies that recognize these shifts and adapt accordingly.

How Forest Hill Management Adapts to Changing Consumer Needs

We understand that today’s financial pressures, like higher living costs and rising interest rates, are making it harder to keep up with obligations. At Forest Hill Management, we know that traditional, high-pressure collection tactics add to the stress rather than solve the problem.

That’s why we’ve built systems that reflect what consumers really need right now:

- Technology that removes barriers: Secure online payments, real-time balance tracking, and account visibility so you're never guessing where you stand.

- Flexible plans that match your reality: Repayment structures designed around your current financial situation, not what we wish you could afford.

- Compliance-first approach: We follow evolving regulations to ensure your rights are protected as laws change.

- Transparency at every step: No hidden fees, no surprise escalations, no confusing language that requires a lawyer to decode.

- Human support when you need it: Account support teams available to answer questions and review plan adjustments.

Whether you’re just starting to address an outstanding balance or need to adjust your plan as life changes, we’re here to make the process easier.

Conclusion

Consumer debt in the U.S. has grown into a complex challenge, but with the right strategies, it’s possible to regain control and build a path forward. Small steps, like managing rising interest rates, handling emergencies, and addressing debt early, can have a big impact on your financial future.

As you move forward, remember that tackling debt is not about perfection; it’s about progress. No matter where you are in your journey, taking the first step toward understanding your options can lead to lasting relief and control.

At Forest Hill Management, we’re here to support that journey. Our approach is to find solutions that fit your life, providing you with the tools and guidance you need to manage this challenging landscape. Together, we can help you take the next step toward financial peace of mind.

Take the next step toward managing your debt more clearly by contacting our support team for personalized assistance.

FAQs

1. How does revolving credit differ from installment debt in risk and repayment?

Revolving credit, like credit cards, allows ongoing borrowing up to a limit, so balances can fluctuate and interest compounds monthly. Installment debt, like personal or auto loans, has fixed payments and a set payoff date, creating predictable timelines and a lower risk of runaway interest if managed properly.

2. Can macroeconomic factors affect my debt repayment even if my income is stable?

Yes. Inflation, rising interest rates, and changes in lending policies can increase your minimum payments, reduce available credit, or accelerate penalties. Even a steady income may not keep pace with these external pressures, impacting your ability to repay on schedule.

3. What psychological effects can mounting debt have on decision-making?

High debt levels often trigger stress, avoidance behavior, and short-term thinking. People may delay payments, ignore statements, or make impulsive financial choices to cope emotionally, which paradoxically worsens the debt situation over time.

4. How do structured repayment plans affect long-term financial stability?

Structured repayment plans provide predictable payments and clear timelines, which can reduce stress and help consumers stay consistent without taking on new debt.

5. Are there tax implications for settling debts for less than the full amount owed?

Yes. Forgiven debt may be considered taxable income by the IRS, meaning if a creditor accepts a reduced payment, the forgiven portion could trigger a tax liability unless specific exemptions (like insolvency) apply. Proper planning is needed to avoid unexpected financial consequences.