Master Consumer Portfolio Management for Debt Relief

Need Help Reviewing Your Account?

Contact UsDebt feels less confusing because of the balance and more because the name contacting you isn’t the one you borrowed from. When ownership shifts, clarity usually disappears first.

That confusion is common as average U.S. consumer debt reached $104,755 by mid-2025, with sharper increases among fair-credit borrowers and Gen Z. Rising balances make unfamiliar outreach harder to interpret.

When your debt moves into a portfolio, it doesn’t spiral by default. It enters a structured system called consumer portfolio management, where accounts are grouped, reviewed, and handled through defined processes.

That structure shapes how your account is reviewed, when you’re contacted, and which options appear first. This article explains how that system works and what it means for you as a borrower seeking resolution.

Key Takeaways

- Understanding how your debt is managed gives you leverage; portfolio companies often buy accounts at a discount, letting you negotiate settlements or repayment plans.

- Debt portfolios follow structured, data-driven processes; knowing timing, prioritization, and scoring models helps you respond strategically.

- Engaging early with portfolio managers prevents escalation, protects your credit, and keeps you in control of your finances.

- Forest Hill Management offers flexible repayment options, transparent account tracking, and personalized support, making debt resolution manageable.

- Knowing your rights, legal protections, and communication rules empowers you to interact confidently and rebuild financial stability.

What Is Consumer Portfolio Management?

Consumer portfolio management happens when companies buy past-due accounts from lenders and handle the debt collection. Creditors sell these accounts to get immediate cash and reduce risk, while the purchasing company focuses on recovering the owed amounts.

The debt itself doesn’t change; you still owe the same amount, but a new company manages the collection process.

Understanding how this process works in practice can help you see what happens once a debt is sold.

How Consumer Portfolio Management Works

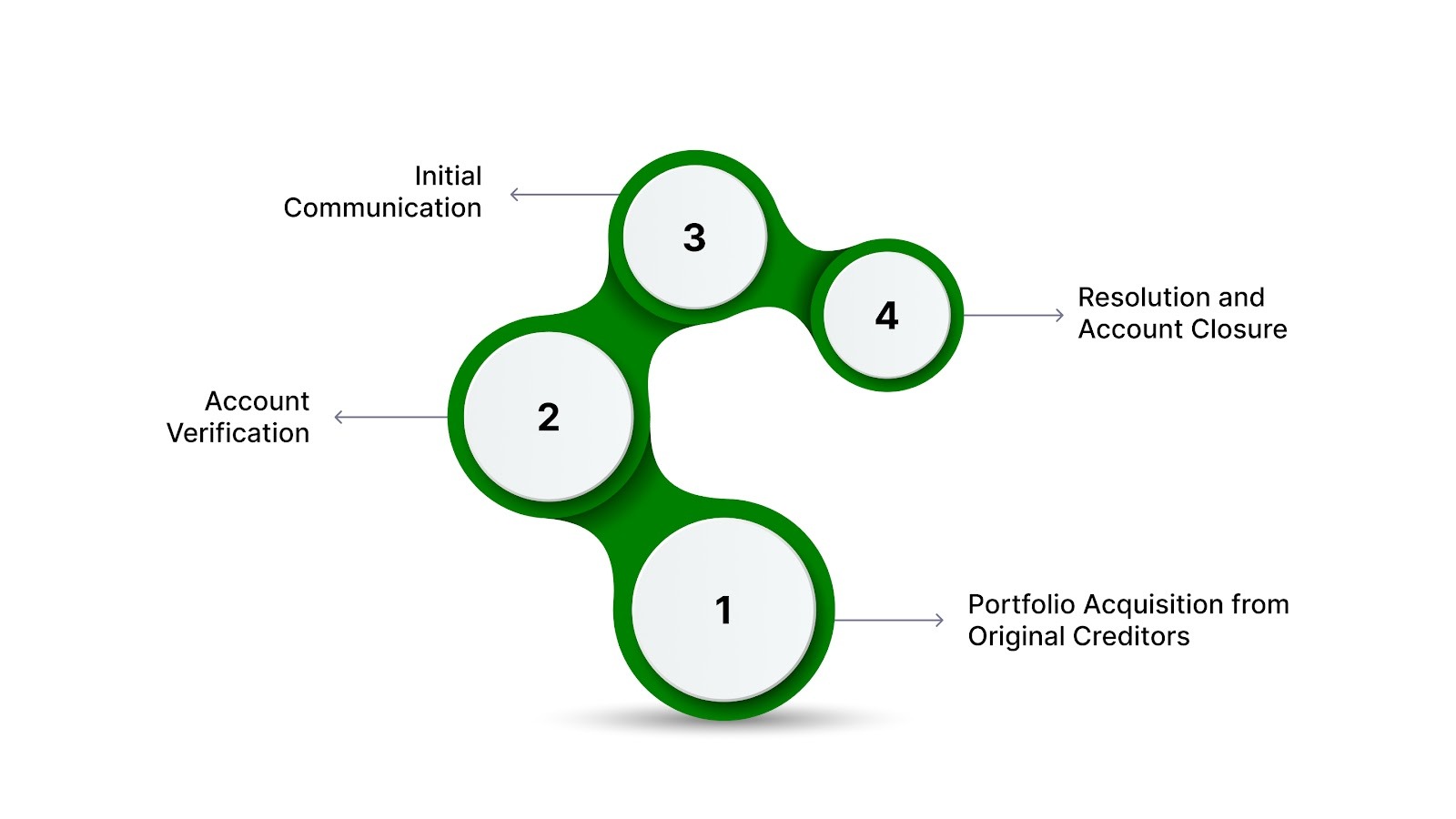

When a debt portfolio changes hands, your account goes through a clear process to verify it, communicate with you, and work toward a resolution. Here’s a step-by-step look at how the process unfolds:

1. Portfolio Acquisition from Original Creditors

Debt buyers purchase past-due accounts from banks or lenders, usually at a fraction of what’s owed. This allows room for repayment options. Records generally include your balance and contact info, though details may sometimes be incomplete.

2. Account Verification

Before reaching out, the company checks that the debt and your information are correct. If anything looks off, the account is reviewed further to avoid mistakes.

3. Initial Communication

The company must tell you how much you owe, who the original creditor was, and your right to dispute the debt within 30 days. This is the start of a conversation about repayment, not random harassment.

4. Resolution and Account Closure

Once payments are made or a settlement is reached, the account is marked resolved, and collection activities stop. The resolution is reported to credit bureaus, updating your credit file while ending uncertainty.

Also Read: Understanding Consumer Debt and Its Impact on Your Credit Score

With the process clear, let’s look at the strategies that make debt resolution possible.

Strategies Portfolio Managers Use to Support Debt Resolution

Portfolio managers aim to recover debts while helping you manage repayment responsibly. Key strategies include:

- Flexible Repayment Plans: Monthly installments provide a structured path without causing undue financial strain.

- Settlement Offers: In some cases, managers accept a reduced one-time payment to close the account efficiently.

- Clear, Ongoing Communication: You receive updates through phone, mail, email, or online portals to track balances and payments.

- Compliance With Debt Collection Laws: All actions follow federal regulations, including the FDCPA, ensuring legal and ethical treatment.

Building on these strategies, portfolio managers also prioritize accounts to ensure efficient resolution while balancing fairness and risk management.

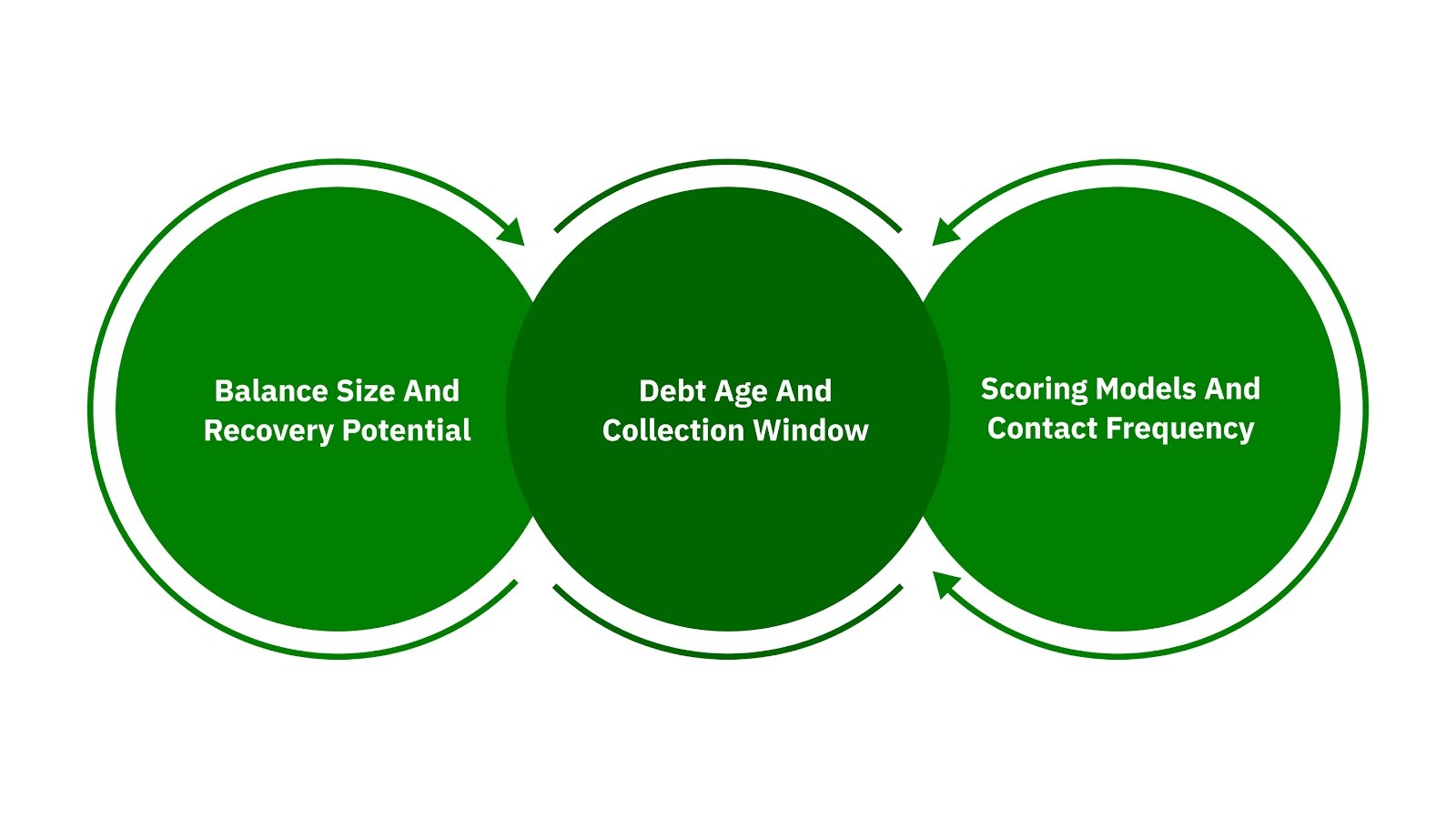

How Accounts Are Prioritized in Consumer Portfolios

Not every account receives the same level of attention at the same time. Portfolio managers use data-driven systems to decide which accounts to contact first, how often to follow up, and what offers to extend.

Here's what drives those decisions:

1. Balance Size and Recovery Potential

Larger balances naturally attract more focus because the potential recovery justifies the time investment. An account with a $15,000 balance gets more resources than one with $500, simply because the financial return is higher.

Recovery potential also factors in. Accounts where the debtor has a stable income or a history of partial payments are prioritized over those with no recent engagement.

2. Debt Age and Collection Window

Older debts are usually harder to collect. Memories fade, circumstances change, and laws may limit legal collection options. Portfolio managers focus on accounts that are still within active collection periods, which vary by jurisdiction and debt type.

Newer accounts often receive immediate attention, as the borrower’s financial situation is more likely to support repayment.

3. Scoring Models and Contact Frequency

Portfolio companies use predictive scoring models to rank accounts by likelihood of repayment. These models analyze payment patterns, income indicators, and past interactions to assign a score.

High-scoring accounts trigger more frequent contact attempts and better settlement offers because the data suggests a higher chance of resolution. Low-scoring accounts may receive less attention or be placed in a lower-priority queue.

Also Read: Consumer Impact Recovery and Debt Collection Guide

The way accounts are prioritized shapes the timing and nature of communications, which in turn affects the repayment options and support available to you as a borrower.

What This Means for You as a Borrower

Understanding how consumer portfolio management operates shifts your position from reactive to informed. You're not just receiving calls or letters; you're participating in a process that has structure, rules, and room for negotiation.

That knowledge changes how you approach the situation:

- Negotiate from a stronger position: Portfolio companies buy debt at a discount, giving them room to accept less than the full balance. Use that leverage to propose settlements or payment plans that fit your budget instead of accepting the first offer.

- Engage to prevent escalation: Ignoring the account doesn’t make it disappear; it can lead to legal action, credit damage, or more aggressive collection. Responding early, even if you can’t pay immediately, keeps options open and shows a willingness to resolve the debt.

- Know your rights: Federal law protects you from abusive practices, ensures accurate information, and requires documentation. If something is wrong, you can formally dispute it, avoiding agreements that don’t serve your interests.

- Restore control: Resolving an account, even through a negotiated settlement, removes the weight of unresolved debt and allows you to rebuild credit and financial stability without constant collection activity.

Also Read: What Happens If You Miss a Payment on Consumer Easy Credit?

With this understanding, here’s how Forest Hill Management supports borrowers with clear, flexible, and fair solutions.

How Forest Hill Management Approaches Consumer Portfolio Management

When your account is managed by a portfolio company like Forest Hill Management, you're working with a team that prioritizes resolution over pressure. We understand that everyone's financial situation is different, which is why we've built our approach around flexibility and support. Here's what you can expect when working with us:

- Make secure payments online 24/7 through our user-friendly platform with no hidden fees

- Work with financial advisors to create a repayment plan that fits your current budget and income

- Access your account details anytime for full transparency on balances, payments, and progress

- Receive personalized support from a team that understands financial hardship without judgment

Our approach ensures you’re never managing your debt alone. Every payment, plan, and update is designed to make your path to resolution clear and manageable.

Conclusion

Debt can feel like a maze, but understanding the system behind portfolio management transforms uncertainty into perspective. When you recognize that every account is part of a structured process, you gain the power to respond thoughtfully, make informed decisions, and regain control over your financial journey.

This isn’t just about paying balances; it’s about reclaiming confidence, building clarity around your obligations, and choosing steps that work for your life. Forest Hill Management stands ready to help you manage these choices, offering guidance and tools to turn complexity into a clear path forward.

Take the first step toward financial freedom today - make a payment online or contact our advisors to create a personalized plan.

FAQs

1. Can a consumer portfolio manager contact me at work or on social media?

Portfolio companies typically follow strict regulations about communication channels. While federal law allows them to reach you, contacting you at work or on social media is generally restricted to protect your privacy and prevent harassment.

2. How does debt in a portfolio affect co-signers or authorized users?

If someone co-signed your debt, portfolio ownership can also impact them. The portfolio manager may reach out to co-signers for repayment or negotiation discussions, but authorized users on the account without liability are usually not contacted.

3. Are there tax implications when settling a debt through a portfolio manager?

Yes, forgiven debt might be considered taxable income. If you settle for less than the full balance, the IRS could require you to report the forgiven amount. It’s wise to consult a tax professional when negotiating settlements.

4. Can portfolio-managed debt be included in bankruptcy proceedings?

Debts held by portfolio companies are still legally enforceable and can be included in bankruptcy filings. The fact that a portfolio company manages the account does not exempt it from discharge rules or repayment requirements under bankruptcy law.

5. What happens if a portfolio company sells my account again?

Accounts can change hands multiple times. Each new owner must re-verify the debt and notify you of the transfer. Your obligations remain the same, but you may need to update payment instructions and confirm balances with the new company.