Debt Collection Advice: Know Your Rights and Options

Need Help Reviewing Your Account?

Contact UsDebt collection rarely starts with numbers. It starts with a knot in your stomach when a name you don’t recognize keeps calling. You don’t ignore it because you don’t care. You ignore it because engaging feels risky, exposing, and harder than waiting.

That pause creates a power imbalance most people never notice. Debt collection advice exists to move control back into your hands before decisions get made for you.

This article explains how debt collection really works, how to respond without panic, and how to choose a path that protects your finances and your peace.

Key Takeaways

- Debt collection feels urgent by design, but most situations allow time to pause, verify information, and decide your next move calmly.

- You’re not expected to act or pay during the first contact; understanding the debt comes before agreeing to anything.

- Written records: validation letters, notes, and documented agreements are your strongest tools for staying in control.

- Not every debt requires the same response; your options depend on accuracy, affordability, and personal circumstances.

- Progress happens faster when you work with companies that respect consumer protections and communicate clearly, without pressure.

Your Basic Rights Under Federal Debt Collection Laws

Federal law doesn't just discourage bad behavior from collectors; it prohibits specific actions and grants you enforceable protections. The Fair Debt Collection Practices Act establishes boundaries that apply the moment a third-party collector contacts you about a debt.

Understanding these protections changes how you enter every conversation.

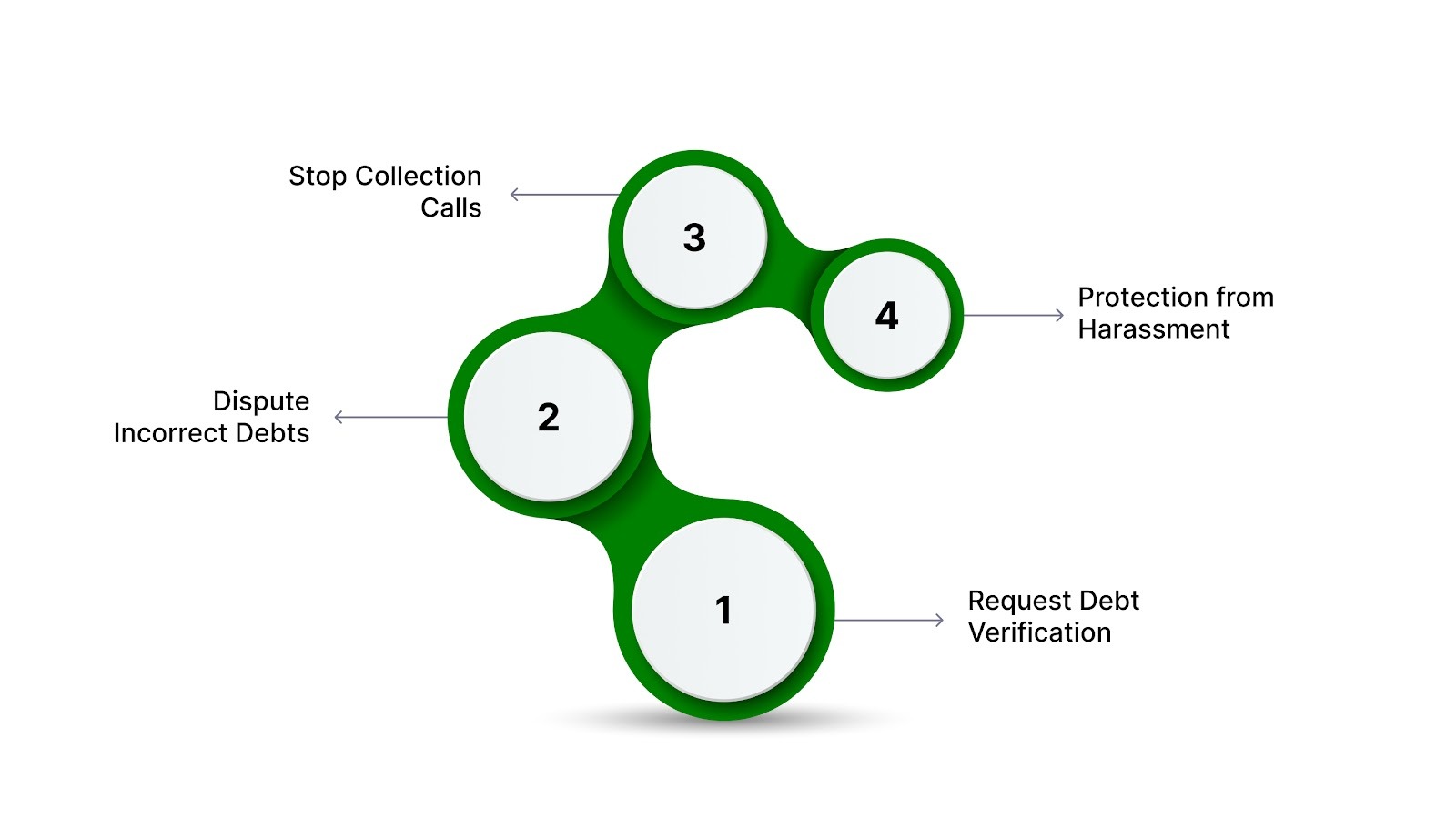

1. Request Written Verification of the Debt

A collector must send you written notice within five days of first contact. This notice includes the creditor's name, the amount owed, and your right to dispute. If anything feels wrong, you have 30 days to request validation in writing, and they must stop collection attempts until they provide proof.

2. Dispute Inaccurate or Unverified Debts

If the debt isn't yours, the amount is wrong, or the account has already been paid, you're not required to accept their word. Send a written dispute within 30 days. The collector must verify the debt with the original creditor before contacting you again.

3. Stop Collection Calls and Letters

A written request to cease communication forces the collector to stop calling and sending letters. They can only contact you once more to confirm they've stopped or to notify you of specific legal action. This doesn't erase the debt, but it does eliminate the noise if you need space to figure out next steps.

4. Protection From Harassment and Deception

Collectors cannot harass, threaten, or abuse you. They may not use profane language, make false threats of legal action, misrepresent themselves as attorneys, or lie about the debt. These rules are enforceable, and violations can be reported to the Federal Trade Commission (FTC) or your state attorney general.

Also Read: 10 Habits to Achieve Maximum Financial Freedom

Knowing your rights gives you the power to respond rather than react. With that foundation, it becomes easier to see exactly where collectors are allowed to act and where the law draws the line.

What Debt Collectors Can and Cannot Do

The law draws a clear line between legitimate collection activity and behavior designed to intimidate. Knowing where that line sits keeps you from reacting to pressure that has no legal weight.

Here's what's actually allowed and what crosses into violation territory:

The table shows power, but only when you recognize which column you're dealing with in real time. Knowing what's legal doesn't make the first call less stressful; it just changes how you handle what comes next.

How to Handle Debt Collection Contact Without Panic

The first conversation with a collector feels high-stakes because you don't know what happens if you say the wrong thing. In most cases, nothing you say in the initial call commits you to payment, but it’s still important to be cautious and avoid admitting liability. A few basic practices shift the dynamic immediately:

- Don't make promises or payments on the spot

Collectors are trained to secure commitment before you have time to think. In some situations and depending on state law, certain actions may affect how long a debt can be collected. You're not required to decide anything during the call.

- Request written validation before discussing payment

Until you've seen documentation that proves the debt is yours and the amount is correct, you're negotiating blind. Ask for validation in writing and end the conversation there. Federal law requires collectors to provide this information upon request.

- Take notes during every call

Write down the date, time, name of the person you spoke with, and what was said. If they make threats, promise specific outcomes, or contradict themselves later, your notes become evidence. Collectors know this, and documentation alone can change their tone.

- Know that you can negotiate

The first number they quote isn't final. Depending on the account and creditor, payment plans, timelines, or reduced payoff options may be discussed once the debt is verified. But negotiation only works when you understand what you owe and what you can actually afford.

Panic makes people agree to terms they can't sustain, which restarts the cycle a few months later when the first payment is missed.

Also Read: Exploring the Journal of Portfolio Management

Once you've handled the initial contact, the question becomes what you actually do with the information.

Your Options When a Debt Collector Contacts You

Contact from a collector doesn't lock you into one path. You have multiple ways to respond depending on whether the debt is accurate, whether you can afford to pay, and what outcome you're trying to protect. The choice you make should match your financial reality, not the urgency the collector tries to create.

1. Verify the Debt First

Validation is about confirming you owe what they say you owe before taking action. Request written proof within 30 days of their first contact. The documentation should include the original creditor's name, the amount, and an itemized breakdown if applicable.

If the numbers don't match your records or the debt isn't yours, you've just saved yourself from paying someone else's obligation.

2. Negotiate a Payment Plan or Settlement

If the debt is accurate but the full amount isn't feasible right now, propose terms that fit your budget. Collectors would rather receive partial payment over time than pursue legal action that may not result in collection.

In some cases, especially with older accounts, collectors may consider resolving a balance for less than the full amount, depending on the circumstances. Whatever you agree to, get the terms in writing before you send money. Verbal agreements aren't enforceable, and partial payments without documentation can complicate disputes later.

3. Dispute the Debt If It's Wrong

Errors happen, accounts get misreported, balances get inflated, and payments don't get credited. If you believe the debt is inaccurate, file a formal written dispute within 30 days. Include any documentation that supports your claim: bank statements, receipts, or correspondence from the original creditor.

4. Request They Stop Contacting You

If you need the calls and letters to stop while you figure out your next move, send a written cease contact request. This is your legal right under the Fair Debt Collection Practices Act (FDCPA).

Once they receive it, they can only contact you one more time to confirm they've stopped or to inform you of specific legal action. This does not erase the debt, and legal options may still exist depending on the account and applicable laws.

There are moments when managing debt solo becomes less effective, and seeking guidance is the smarter choice.

When to Seek Professional Guidance

Many people handle debt collection alone until it outpaces their ability to respond. Reaching the point where professional input can change the outcome isn’t failure; it’s smart planning.

Here’s when professional guidance can make a difference:

- You can’t afford any payment: If income barely covers essentials and even a reduced plan isn’t realistic, a financial advisor or credit counselor can explore bankruptcy, hardship programs, or negotiation options.

- Legal action is threatened: Mentions of lawsuits, wage garnishments, or court proceedings compress timelines. An attorney specializing in consumer debt can verify threats and guide your response.

- Multiple collectors are contacting you: When several agencies are involved, prioritizing payments matters. Professionals help triage based on legal risk, statutes of limitations, and financial impact.

- You need a structured repayment plan: Expert guidance ensures your resources are allocated effectively, avoiding mistakes that prolong the problem.

Also Read: Can a Debt Collector Take My Car? Understanding Your Rights

Professional help is about entering a high-stakes situation with someone who knows the rules better than you do. Knowing your rights and options only matters if you're working with a company that respects both without forcing you to demand them first.

How Forest Hill Management Supports Clear, Compliant Account Resolution

Understanding your rights is important. Working with a company that communicates clearly and follows consumer protection standards can make the process feel far more manageable.

Forest Hill Management approaches account resolution with an emphasis on transparency, lawful communication, and respect for your situation. The goal is to help you understand your account, review available options, and take practical steps forward at a pace that makes sense for you.

What this looks like in practice:

- Clear account information: You receive written details about the account, including the original creditor and balance, so you know exactly what you’re being contacted about.

- Professional, respectful communication: Outreach is intended to be straightforward and informative, not overwhelming or confusing.

- Flexible repayment options: Payment arrangements are structured around your individual circumstances to help reduce pressure and avoid unnecessary escalation.

- Secure online account access: You can review balances, make payments, and manage your account through a secure, user-friendly online platform.

- Support when you need it: If you have questions or need help understanding your next steps, Forest Hill Management’s team is available by phone to assist you.

Financial challenges can feel isolating, but you don’t have to manage them without clarity or support. By focusing on compliant processes and clear communication, Forest Hill Management works to make resolving your account more straightforward and less stressful.

Conclusion

Debt collection feels overwhelming largely because it introduces urgency before understanding. Once you know the rules, the process becomes something you can navigate instead of something that happens to you.

You now understand how federal protections work, what collectors are allowed to do, and how to respond in a way that fits your situation and financial reality.

When you’re ready to move forward, working with a company that operates within those boundaries matters. Forest Hill Management exists to support resolution through clear communication, compliant processes, and practical repayment paths, without adding pressure or confusion.

You can make a payment online or contact our advisors for personalized support to explore options that fit where you are right now.

FAQs

1. How can timing of payments affect debt collection strategy?

Paying debts at certain times, like right before a creditor sells the account, can influence how aggressive collection becomes. Strategic timing may reduce fees, prevent additional interest, or improve negotiating leverage if the account is nearing transfer.

2. Can communication style impact collector responses?

Yes. The way you communicate: calm, concise, fact-based versus emotional or reactive, can change a collector’s behavior. Clear documentation, polite firmness, and structured questions often yield faster responses and fewer errors in account handling.

3. How do debt collection policies vary by industry?

Debt collection practices differ depending on the type of debt. Medical, student, utility, and credit card debts have unique rules, reporting practices, and statute of limitations.

4. Are there risks to co-signed or joint accounts in collections?

Co-signers or joint account holders may be pursued even if only one party defaulted. Understanding the shared liability, potential impact on credit, and who can negotiate is critical to prevent unexpected financial responsibility.