Debt Collection Oversight: Consumer Advice and Management

Need Help Reviewing Your Account?

Contact UsWhen a collector calls, the imbalance is immediate. You hold uncertainty, while the caller controls timing, language, and pressure, which explains why 70 million Americans face collection contact yearly.

That imbalance worsens when information stays unclear. Federal data shows 27% of contacted consumers feel threatened, often because details feel incomplete, disputed, or delivered without context you can trust.

Debt account oversight exists to correct that imbalance before it escalates into unnecessary stress or confusion. It sets boundaries on how collection accounts are handled, ensuring accuracy, restraint, and accountability instead of leaving outcomes to persistence or intimidation.

This article explains how debt account oversight works, how it affects your interactions, and how you can manage collection accounts with confidence instead of confusion.

Key Takeaways

- Debt collectors must follow federal and state rules; knowing these limits helps you recognize harassment or illegal pressure.

- Always verify a debt before paying: request written validation, confirm the original creditor, and check all amounts and fees.

- You have enforceable rights: dispute errors, stop unwanted contact, and report violations without fear of retaliation.

- Patterns matter: repeated calls, threats, or refusal to provide documentation are clear red flags.

- Working with compliant, transparent companies makes managing debt less stressful, with clear communication, fair repayment options, and secure account access.

Who Oversees Debt Collectors and Why It Matters to You

The Consumer Financial Protection Bureau sets and enforces the rules collectors must follow nationwide. Think of them as the referee keeping the game fair. They investigate complaints, penalize companies that break the law, and update protections as tactics evolve.

States add another layer. Most have consumer protection offices or attorney general oversight, sometimes with stricter rules, interest caps on old debts, or licensing requirements before collectors can contact you.

Oversight doesn’t stop collection. It prevents abuse. Debt collection rewards speed and volume, which can tempt misconduct. Clear rules and real consequences keep most companies compliant; the rest are removed. Knowing who’s watching shows where to turn when something feels wrong and that these protections exist for you.

What Debt Collectors Can and Cannot Do Under Federal Law

Federal law draws a bright line between legitimate collection activity and behavior that crosses into harm. Collectors operate within specific boundaries designed to let them do their job without trampling your dignity or rights.

The distinction matters because what feels aggressive isn't always illegal, and what seems polite might still violate the law.

Here's what the rules allow and prohibit:

These boundaries are designed to make the process more balanced and predictable. You can't be worn down by 3 AM calls. You can't be tricked into paying debts you don't owe. You can't be publicly shamed at your workplace.

The rules don't make the debt disappear, but they do ensure the process respects your basic humanity.

Also Read: 10 Successful Debt Collection Techniques for Maximizing Success

Even with clear rules in place, some collectors still test the edges or ignore them entirely.

Signs a Collector May Be Crossing the Line

When a collector violates federal law, your gut usually knows before your brain catches up. The conversation feels wrong: too intense, too invasive, or deliberately confusing. Those instincts are data. Trust them, then look for the specific patterns that confirm a line's been crossed.

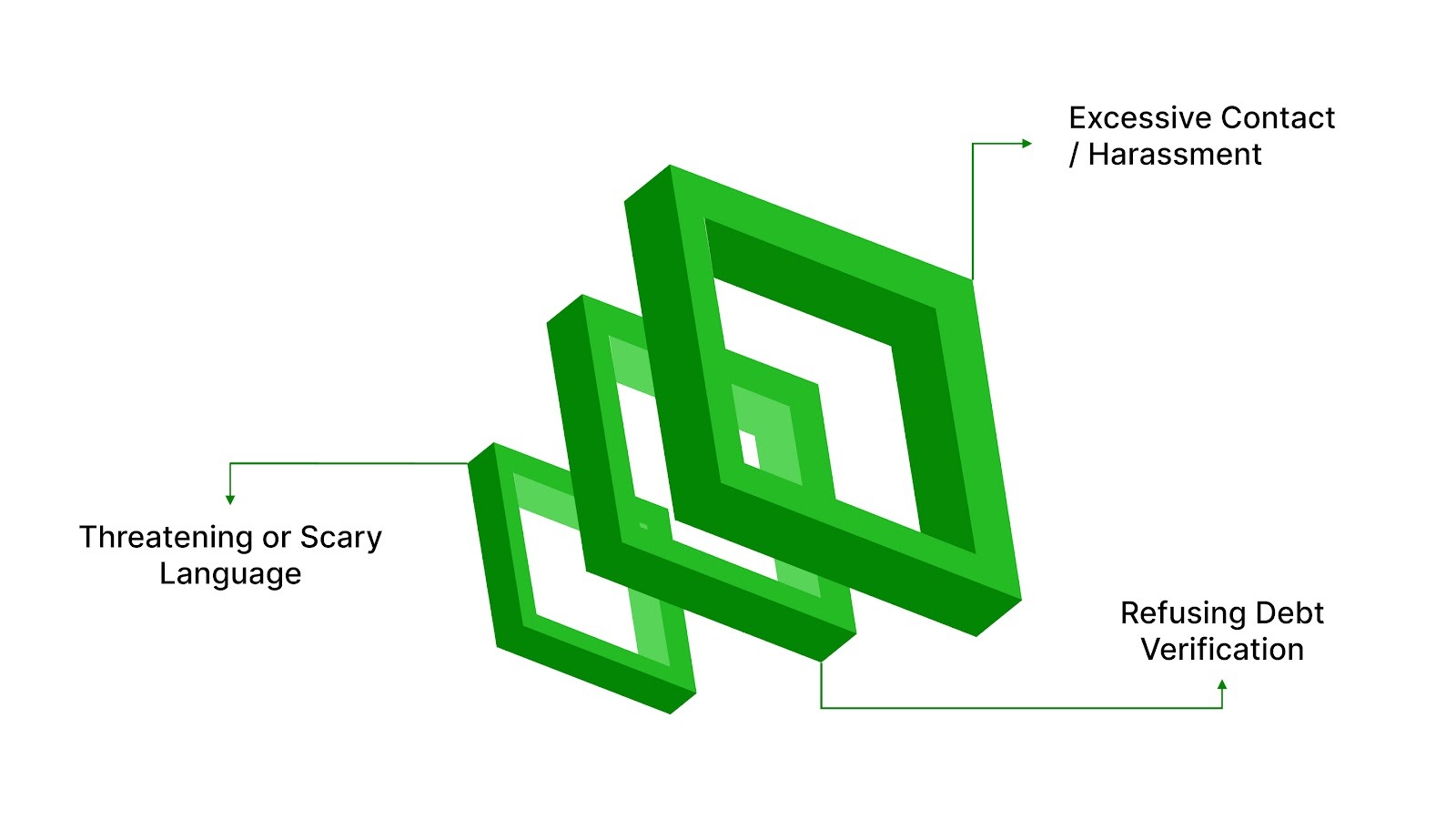

1. Excessive Contact / Harassment

If your phone rings eight, ten, or twelve times in a single day from the same collector, that's not persistence. It's harassment. The law doesn't set an exact number, but judges and regulators recognize a pattern designed to exhaust you into compliance. The goal is to make you answer just to stop the noise.

Some collectors call your workplace repeatedly even after you've told them not to. Others contact relatives or neighbors, ostensibly to "locate" you, but really to embarrass you into responding. This pressure may be intentional, and in many cases, it violates federal law.

2. Threatening or Scary Language

Profanity, insults, or threats don't belong in a business conversation, yet some collectors use them anyway. You might hear threats of arrest, jail time, or criminal charges. All fabrications, since unpaid consumer debt isn't a crime.

Others claim they'll seize your house, freeze your bank account, or garnish wages without a court order. These statements create panic, which is the point. Fear can push people toward rushed decisions without full information. But courts have been clear: collectors can't weaponize false consequences to force payment.

3. Refusing Debt Verification

When you ask who the original creditor was or request written proof of what you owe, a legitimate collector provides it within a reasonable time. A non-compliant one deflects, delays, or demands payment first. This opacity isn’t confusion. It’s a tactic to keep you off-balance and discourage questions.

Also Read: How to Win Debt Collection Disputes: A Complete Step-by-Step Guide

Recognizing violations is step one. Confirming the debt itself is legitimate comes next.

How to Verify Your Debt Is Being Managed Properly

Just because someone says you owe money doesn't make it true. Debts get sold, transferred, and misrecorded constantly. Amounts get inflated with fees that weren't authorized. Sometimes accounts that were already paid resurface under a different collector's name. Verification closes the gap between what they claim and what's actually owed.

Within five days of first contacting you, collectors must send a written notice containing specific details: the creditor's name, the amount owed, and a statement of your right to dispute. You have 30 days from the date you receive that notice to request validation.

Send your request in writing via certified mail with a return receipt so you have proof. During that window, the collector must pause collection activity until they provide documentation proving the debt is yours, accurate, and legally collectible.

Proper documentation looks specific, not vague. It includes:

- Original creditor's name and account number

- Itemized breakdown showing principal, interest, and any added fees

- Date of last payment or account activity

- Clear statement of your dispute and verification rights

Red flags appear when details don't line up. Verification is about ensuring the process starts from truth rather than assumptions.

Once you know the debt is real, understanding your rights determines how much control you actually have.

Your Rights When Dealing With Collection Oversight

You're not a passive participant in this process. Federal law grants you specific rights that collectors must honor, regardless of how much you owe or how long the debt's been outstanding.

To make sure your rights are protected, keep these points in mind:

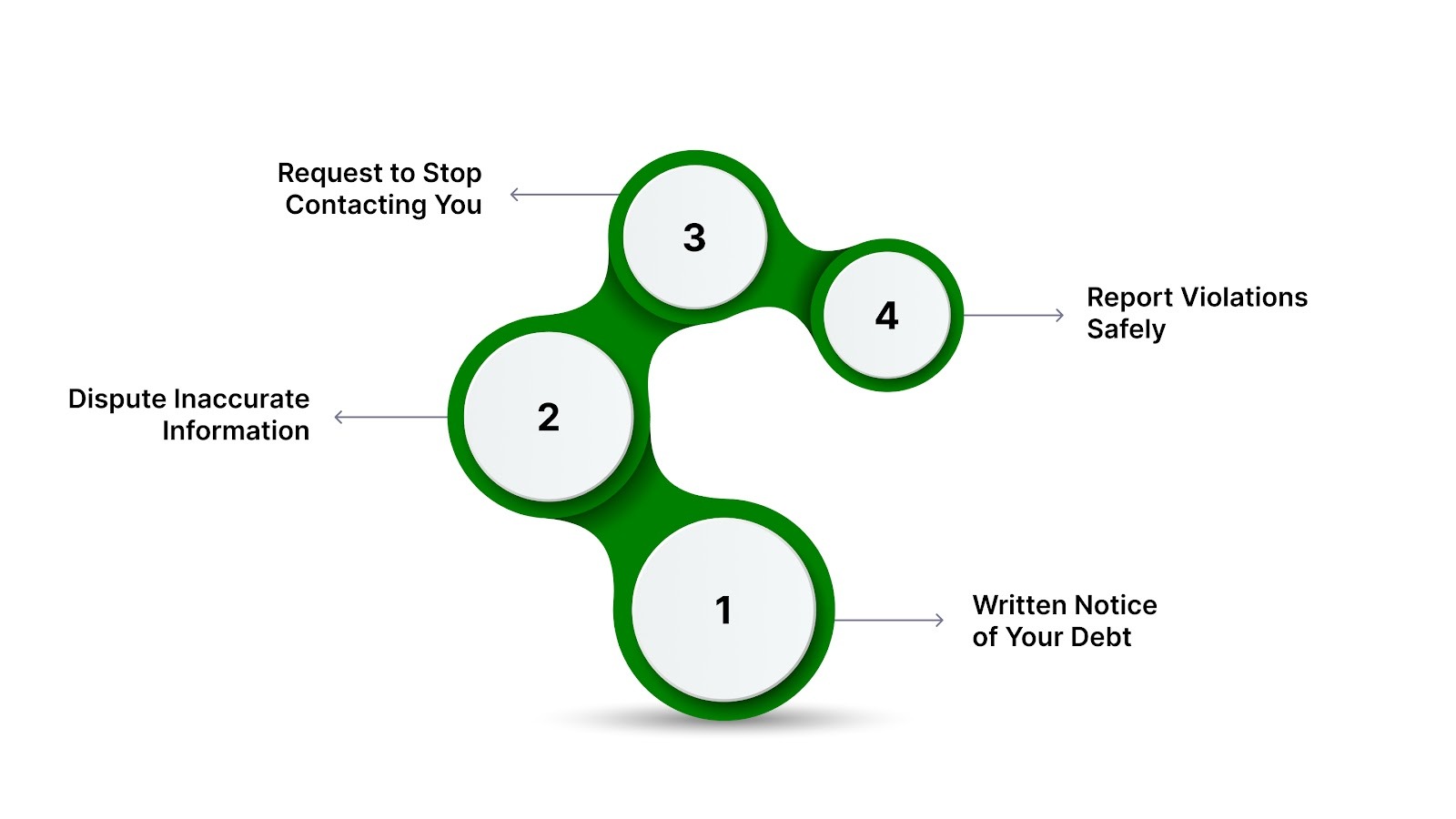

1. Written Notice of Your Debt

Every collection attempt must include or be followed by a written validation notice. That notice isn't optional, and it's not just a courtesy. It's your legal documentation showing what's being claimed, by whom, and under what terms. Without it, you're operating blind. With it, you can fact-check every assertion before deciding how to respond.

2. Dispute Inaccurate Information

If the debt amount is wrong, if it's not your account, or if you already settled it, you can dispute in writing within 30 days. Once you do, the collection activity must stop until the collector investigates and responds with proof.

This right exists because errors are common. One study found nearly 20% of credit reports contain mistakes that could impact collections.

3. Request to Stop Contacting You

You can send a written cease-and-desist letter to a collector telling them to stop calling, texting, or emailing. Once they receive it, contact must end. This doesn't erase the debt, but it does silence the noise while you figure out the next steps.

4. Report Violations Safely

If a collector breaks the law, you can file a complaint with the CFPB, your state attorney general, or pursue legal action. Collectors can't punish you for exercising this right. Complaints create a documented trail that regulators use to identify patterns and take enforcement action. Your report might protect the next person they contact.

Also Read: Best Debt Payment Gateways and How They Work

Rights matter, but they mean more when the company you're dealing with already operates within them by default.

How Forest Hill Management Approaches Compliant Account Management

Oversight exists because not all companies follow the rules. Forest Hill Management was built to operate inside those rules from day one. Not because we have to, but because it's the only way to treat people fairly when they're already dealing with financial stress.

What that looks like in practice:

- Clear communication from the start: You receive a written notice with all required debt details, not vague or misleading claims.

- Respect for your time and privacy: Contact happens within legal hours, and your personal information stays protected.

- Validation you can trust: We provide documentation that confirms the debt, the original creditor, and the amount owed.

- Flexible, structured repayment options based on your financial situation: Structured plans designed around your situation, not pressure tactics.

- Secure online access: Manage payments, view balances, and track progress through a safe, transparent platform.

Forest Hill Management is committed to ensuring every interaction follows applicable consumer protection laws, provides accurate documentation, and offers structured solutions, so you can manage your accounts with certainty and peace of mind.

Conclusion

Oversight doesn’t erase your obligations, but it can make managing them clear and manageable. You now understand your rights, what collectors can and can’t do, and how to spot when something isn’t right. That knowledge shifts the balance from confusion and stress to informed, confident action.

Taking the next step starts with knowing you have options. Whether it’s requesting validation, disputing errors, or exploring a structured repayment plan, you can move forward at your own pace, without pressure or guesswork.

Working with a company like Forest Hill Management, which respects your rights and provides clear, compliant support, removes one more barrier on your path to financial stability.

Contact our advisors for personalized guidance and transparent support designed around your situation.

FAQs

1. Can debt collection practices differ for different types of accounts?

Yes. Credit cards, medical bills, student loans, and utilities have distinct rules, privacy requirements, and reporting standards. Knowing your debt type helps you understand which oversight protections apply.

2. How do technological tools influence debt collection compliance?

AI, automated calls, and data analytics improve efficiency but raise compliance concerns. Regulators monitor these tools to ensure they don’t misrepresent debts or violate timing and communication rules.

3. What role do third-party collection agencies play versus original creditors?

Third-party agencies manage or buy debts from original creditors. Errors can multiply in transfers, so both parties must maintain accurate documentation and comply with oversight standards.

4. How does debt collection affect credit reporting beyond simple payment records?

Collectors’ reports can affect credit scores through timing, partial payments, or disputes. Oversight ensures reporting is accurate and not misleading, protecting your credit history.