How to Keep Your Debt Resolutions in 2025

Need Help Reviewing Your Account?

Contact UsJanuary does not expose a lack of discipline. It exposes how fragile financial plans become once real life resumes. 42% of Americans start the year intending to reduce debt, yet most already doubt they will hold the line.

That doubt comes from experience, not pessimism. Nearly 9 in 10 people fail at least one financial resolution, and over a third drop their money goals within three months because daily expenses do not pause for good intentions.

Debt resolutions fail when they depend on perfect months, steady cash flow, and uninterrupted focus. Without structure, one medical bill or missed paycheck turns progress into pressure, which is why structured repayment plans exist as systems rather than promises.

This article explores how to keep your debt resolutions intact through 2026 by replacing fragile goals with durable structures that work even when life does not cooperate.

Key Takeaways

- Debt resolutions often fail because life is unpredictable: unexpected expenses, income changes, and setbacks happen. Plans must be flexible.

- Break big debt goals into small, measurable actions tied to what you control, like a set extra payment each paycheck.

- Automate payments, track spending, and keep a small emergency buffer to prevent minor surprises from derailing progress.

- Pick a repayment strategy you can sustain: snowball, avalanche, or structured plans, and review monthly to adjust as needed.

- Seek professional help when debt becomes unmanageable or when account management overwhelms you; early support prevents bigger problems.

Why Most Debt Resolutions Fail by February

The problem starts with how resolutions are designed. They treat February as a continuation of January, which means they ignore what actually happens when rent is due, work hours fluctuate, and the car needs new tires.

Here's what breaks most debt plans before they gain traction:

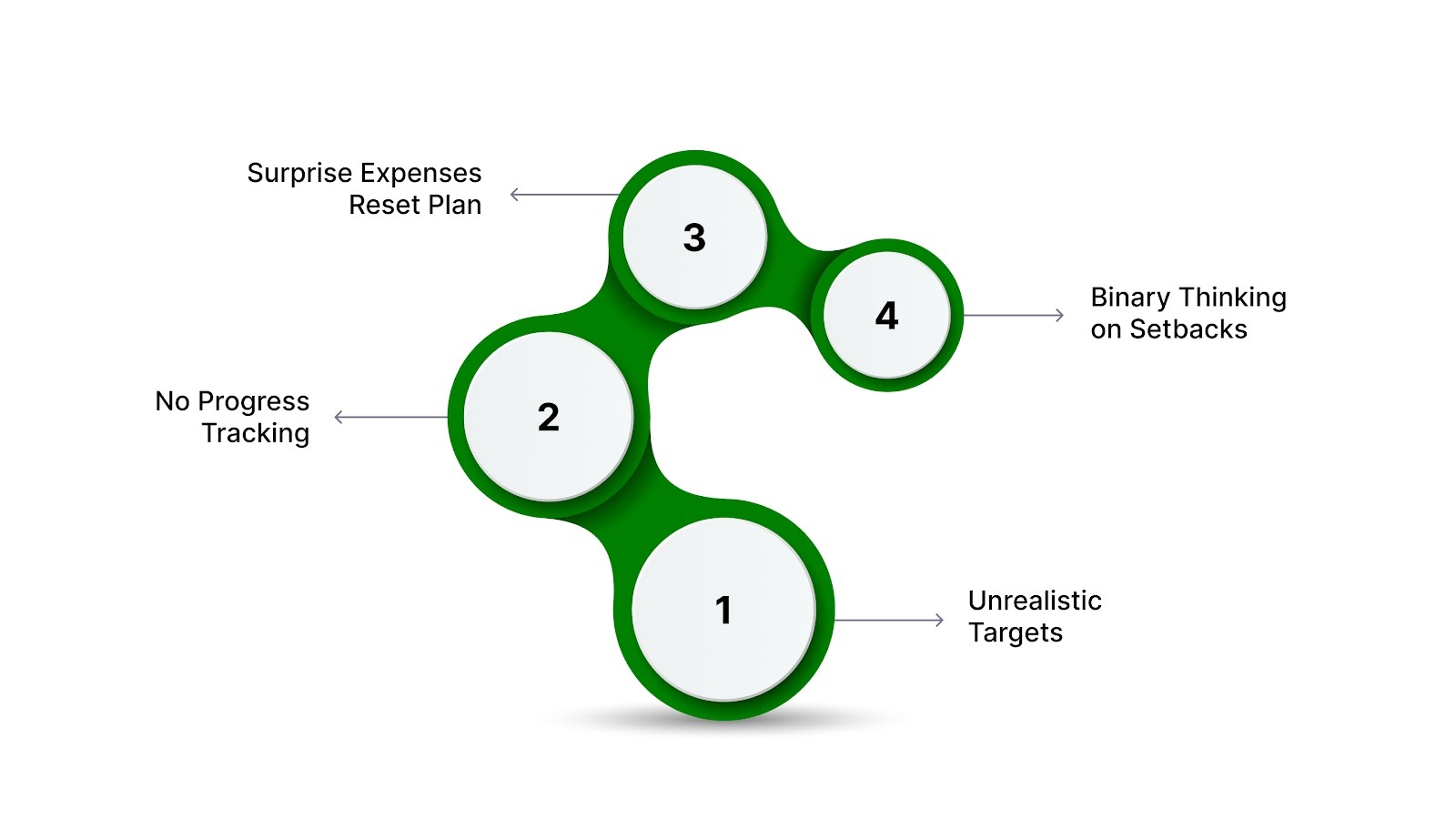

- Targets that ignore your actual income: Planning to eliminate $20,000 in six months on a $40,000 salary leaves no room for utilities, groceries, or anything unexpected.

- No system to see if you're on track: Without a way to measure progress weekly or monthly, you're guessing whether the plan still works or has quietly fallen apart.

- A single surprise expense becomes a full reset: When an unplanned $400 cost hits and there's no buffer, the entire resolution feels ruined instead of just requiring adjustment.

- Binary thinking turns setbacks into failures: Missing one payment or falling short one month convinces you the whole effort was pointless, so you stop entirely instead of resuming.

Understanding why resolutions collapse helps you design ones that last. Let’s start by turning vague intentions into clear, measurable goals.

Set Specific, Achievable Debt Goals

Vague intentions don't survive contact with your actual schedule and spending. You need targets specific enough to track and small enough to hit consistently.

Here's how to structure goals that hold up under pressure:

- Pick one concrete outcome: Instead of "pay down debt," choose "pay off the $1,200 credit card by June" or "reduce total balances by $2,400 this year."

- Divide annual targets into monthly checkpoints: A $2,400 reduction becomes $200 per month, which is easier to evaluate and adjust as income shifts.

- Anchor goals to what you control: "Make an extra $50 payment every paycheck" is more reliable than "pay off 30% this year," because the second depends on variables outside your influence.

These adjustments turn abstract resolutions into trackable behavior.

Also Read: How to Analyze a Debt Portfolio Effectively

Once your goals are clear, the next step is building habits that make sticking to them automatic, not a constant struggle.

Build Financial Habits That Support Your Debt Resolution

Resolutions collapse when they require constant decision-making. The mental effort of choosing what to pay, when to pay it, and how much to send drains motivation faster than the debt itself.

Here's how to remove friction from the process:

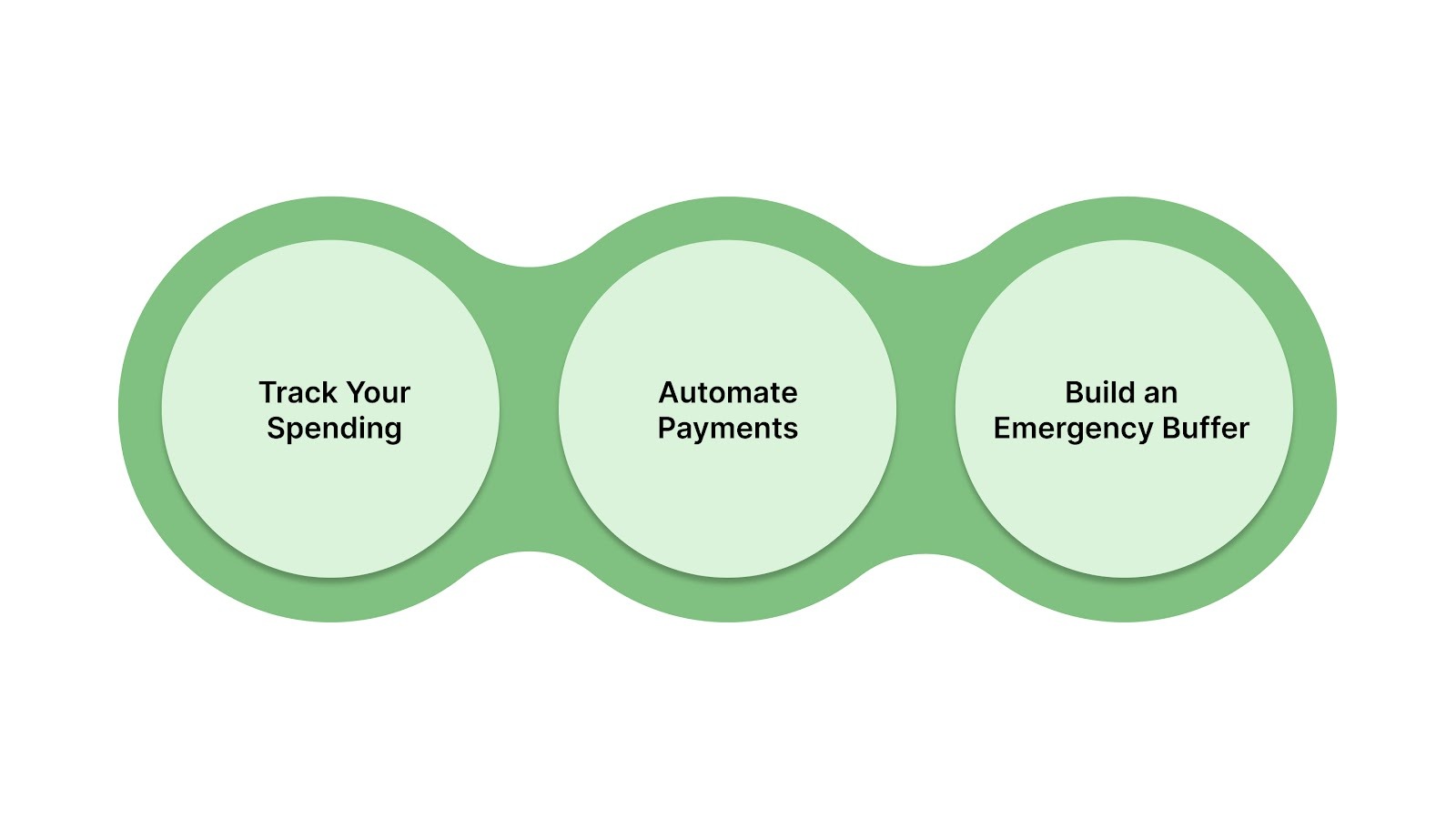

1. Track Every Dollar Coming In and Going Out

You don't need a perfect system. It helps to understand where money actually goes, not where you think it goes. Two weeks of tracking reveal patterns: subscriptions you forgot, small purchases that add up, categories where spending exceeds estimates.

Once you see the leaks, you can redirect money toward debt without feeling like you're cutting essentials.

2. Automate Payments

Setting up recurring payments for minimum balances plus an extra amount eliminates the daily question of whether to pay now or wait. The payment happens whether you remember it or not.

This prevents the "I'll handle it tomorrow" spiral that turns into missed due dates and late fees. Automation doesn't require motivation, which is why it works when willpower doesn't.

3. Create a Small Emergency Buffer

Even $500 sitting in a separate account stops minor emergencies from becoming new debt. When the water heater breaks or the prescription costs more than expected, you cover it without reaching for a card.

Small wins like this compound, not just financially, but psychologically. Handling a surprise without derailing your plan proves the system works, which keeps you engaged.

Also Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2026 Update)

With supportive habits in place, the next step is picking a repayment strategy that matches your goals and lifestyle, so your plan is sustainable.

Choose a Debt Repayment Strategy You Can Stick With

The method you pick matters less than whether you'll actually use it for months without stopping. Different approaches work for different people, depending on whether you need quick psychological wins or want to minimize total interest paid.

Here's what each strategy offers:

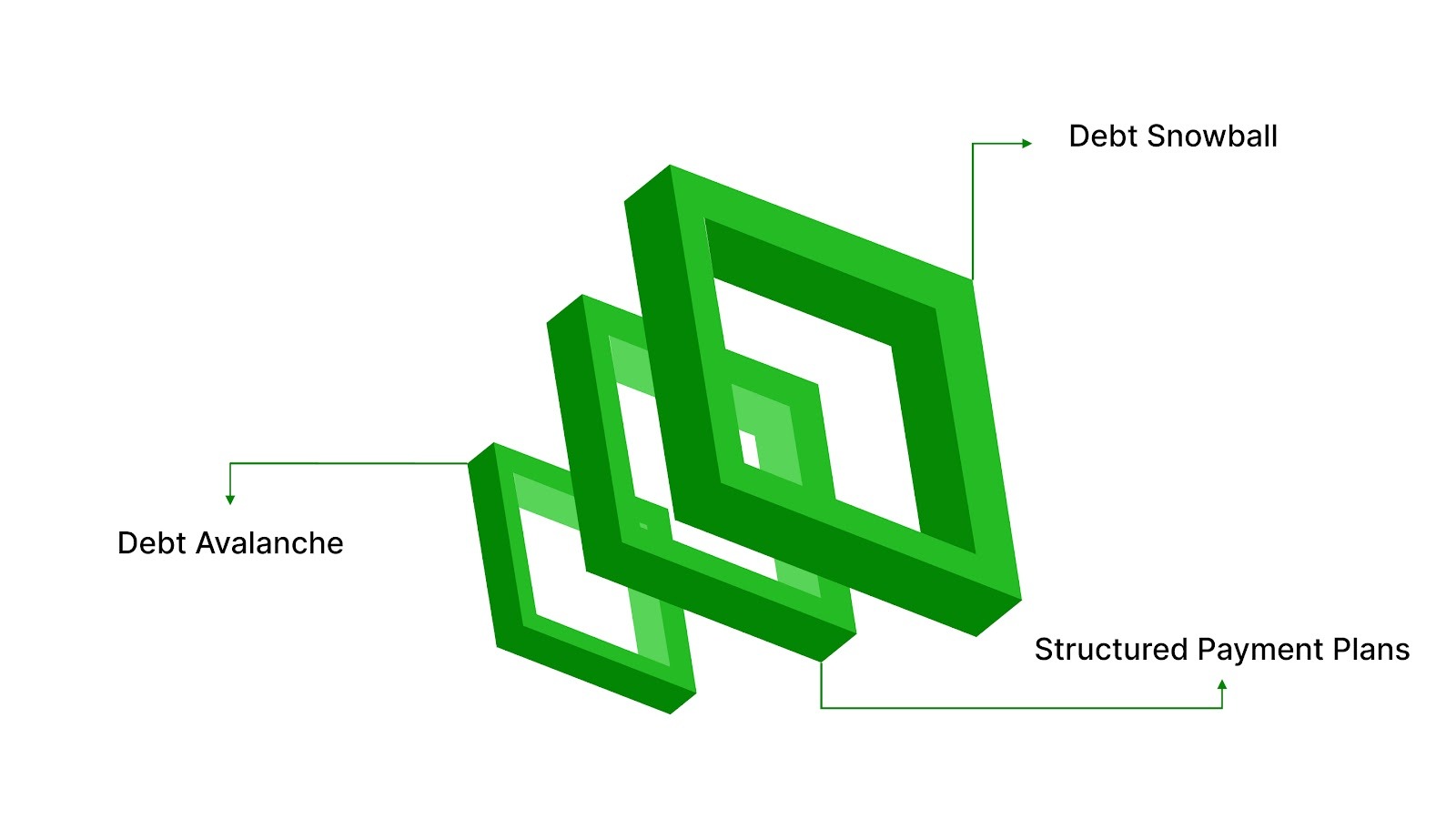

1. Debt Snowball

This approach targets your smallest debt first, regardless of interest rate. You make minimum payments on everything else and put extra money toward the smallest balance until it's gone. Then you move to the next smallest, rolling that freed-up payment into the next target.

2. Debt Avalanche

This strategy prioritizes the debt with the highest interest rate. You pay minimums everywhere else and direct extra payments toward the most expensive balance first. Once that's eliminated, you tackle the next highest rate. Mathematically, this saves the most money over time because you stop the fastest-growing balances first.

3. Structured Payment Plans

Instead of managing multiple accounts, due dates, and varying interest rates, you work within a structured repayment arrangement that simplifies payments into a single, manageable schedule. The terms are negotiated in advance, the amount is fixed, and you deal with one entity instead of juggling several.

With a strategy in place, the key is to review and adjust your plan each month to stay on track.

Review and Adjust Your Plan Every Month

A plan that worked in January might not work in April. Income changes, expenses shift, and priorities evolve. Static plans break because they assume next month will look like this month.

Here's how monthly reviews keep your resolution functional:

- Match the plan to current reality: If your hours got cut or childcare costs went up, adjust payment amounts before you miss deadlines, not after.

- Catch small issues before they escalate: A $50 shortfall one month is fixable. Three months of ignored shortfalls turn into collections calls.

- Acknowledge forward movement regardless of pace: Paying $1,800 this year instead of the planned $2,400 is still $1,800 less debt than you had. Slower progress isn't failed progress.

Monthly check-ins take 20 minutes but prevent the kind of drift that kills resolutions silently.

Also Read: Can a Debt Collector Take My Car? Understanding Your Rights

Even with careful tracking and adjustments, some challenges may exceed what you can handle on your own. Knowing when to ask for help keeps your resolution on track.

When to Ask for Help With Your Debt Resolution

There's a difference between temporary difficulty and a structural problem you can't solve alone. Ignoring that difference wastes time and deepens the hole.

You're past the point of solo effort when:

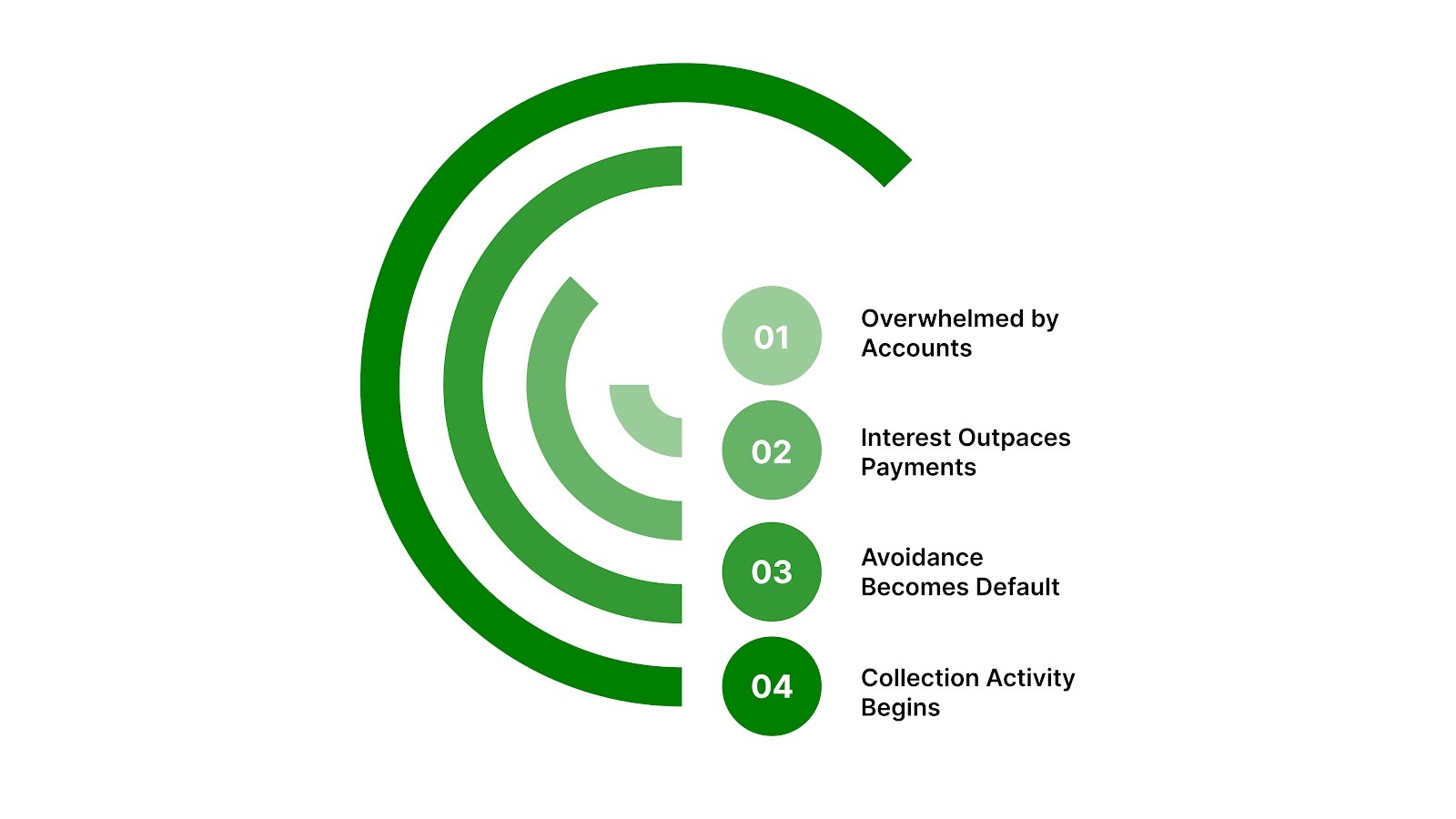

- The number of accounts overwhelms you: When you're managing five or more creditors with different due dates, minimum payments, and interest rates, the administrative burden alone prevents progress.

- Interest accrues faster than payments reduce principal: If your monthly payments barely cover interest charges, the debt isn't shrinking. You're running in place, and that compounds both financially and emotionally.

- Avoidance has become the default response: When you stop opening mail, ignore account balances, or feel paralyzed at the thought of logging in, the psychological weight is blocking action entirely.

- Collection activity has started: Once collection activity begins, timelines often become more structured, making early support more helpful. Professional support becomes less about preference and more about protecting options before they narrow further.

Asking for help isn't admitting defeat. It's recognizing when the problem exceeds the tools you currently have.

When managing debt becomes overwhelming or unmanageable on your own, professional guidance can help turn a fragile plan into a sustainable resolution.

How Forest Hill Management Supports Sustainable Debt Resolutions

Keeping a debt resolution isn’t about perfection; it’s about having a plan flexible enough to adapt to your life while still helping you move forward. Forest Hill Management doesn’t ask you to choose between paying debt and managing everyday expenses. We help structure repayment options that consider both your obligations and everyday expenses.

Here’s how we make resolutions achievable:

- Flexible payment plans: Designed around what you can afford right now, with room to adjust as circumstances change, not rigid terms that ignore your reality.

- Clear progress tracking: See exactly where you stand with secure online account access, so you're never guessing whether you're on track.

- One simple monthly payment: No juggling multiple creditors, confusing due dates, or mental math about which account to pay first.

- Support when life happens: Our advisors help you adjust plans when unexpected expenses arise, not penalize you for being human.

- Compliance and transparency: No hidden fees, no surprise escalations, just clear next steps that don't change without your knowledge.

Every small step counts toward creating stability. When your approach is realistic, adaptable, and transparent, managing debt becomes a process you can handle with confidence.

Conclusion

Financial challenges don’t define your ability to move forward; they highlight the choices you can make in the moment. Each decision, no matter how small, shapes the path ahead and builds a foundation for steadier progress over time.

Forest Hill Management is part of that journey, helping you manage the steps with transparency and respect for your circumstances. This way, managing your obligations feels more manageable and less overwhelming.

Take the first step toward financial freedom or make a payment online today.

FAQs

1. Can lifestyle changes accelerate or derail a debt resolution?

Yes. Major life shifts, like moving cities, starting a new job, or having a child, can alter income, expenses, and priorities. Planning ahead for potential transitions allows you to adjust targets without feeling like failure when circumstances shift.

2. How do psychological biases affect debt repayment decisions?

Cognitive biases, such as overconfidence, loss aversion, or optimism bias, can lead you to underestimate expenses, overestimate repayment ability, or ignore looming debts.

3. Can debt repayment strategies interact with tax or legal obligations?

Certain repayments, like paying off student loans or medical collections, may affect tax deductions, garnishments, or legal protections.

4. How does debt type influence the speed of resolution?

Not all debt behaves the same. Secured debts (like auto loans) and installment loans have predictable schedules, while revolving credit or variable-rate debt can fluctuate.

5. Is there a role for behavioral incentives in sustaining debt resolutions?

Yes. Rewarding yourself for milestones, like paying off a certain percentage of debt or sticking to a budget for three months, can reinforce consistent behavior. Incentives don’t need to be large; even symbolic recognition strengthens adherence to your plan.