Understanding Debt Validation Letters: How to Validate Debt

Need Help Reviewing Your Account?

Contact UsA debt validation letter doesn’t create pressure. It exposes it because you are forced to decide before you feel ready.

The moment it arrives, your mind jumps ahead. Is this accurate? Do you have to act immediately, and what happens if you wait?

Data shows why that hesitation is justified. More than half of debt collection complaints arise because consumers question whether the debt is even theirs, not because they refuse to pay.

That gap between notice and certainty is where proper debt validation matters. This article explores how to regain control during that window, assess your position calmly, learn your options clearly, and move forward without unnecessary pressure.

Key Takeaways

- A debt validation letter is your chance to pause, verify, and understand a claimed debt before taking action; don’t let urgency force a decision.

- Confirm the debt belongs to you by checking creditor details, balances, personal information, and whether the statute of limitations applies.

- Request formal verification if anything seems off; collectors must provide proof before continuing collection efforts.

- Based on verification, choose the right response: pay in full, negotiate a realistic plan, or dispute errors with documented evidence.

- Avoid common mistakes like partial payments, missed deadlines, or undocumented communication to protect your rights and credit.

What a Debt Validation Letter Tells You

A debt validation letter is a required notice meant to inform you of a claimed debt and your rights, not to convince you to pay. What it contains matters because those details determine how, and whether, you can respond effectively.

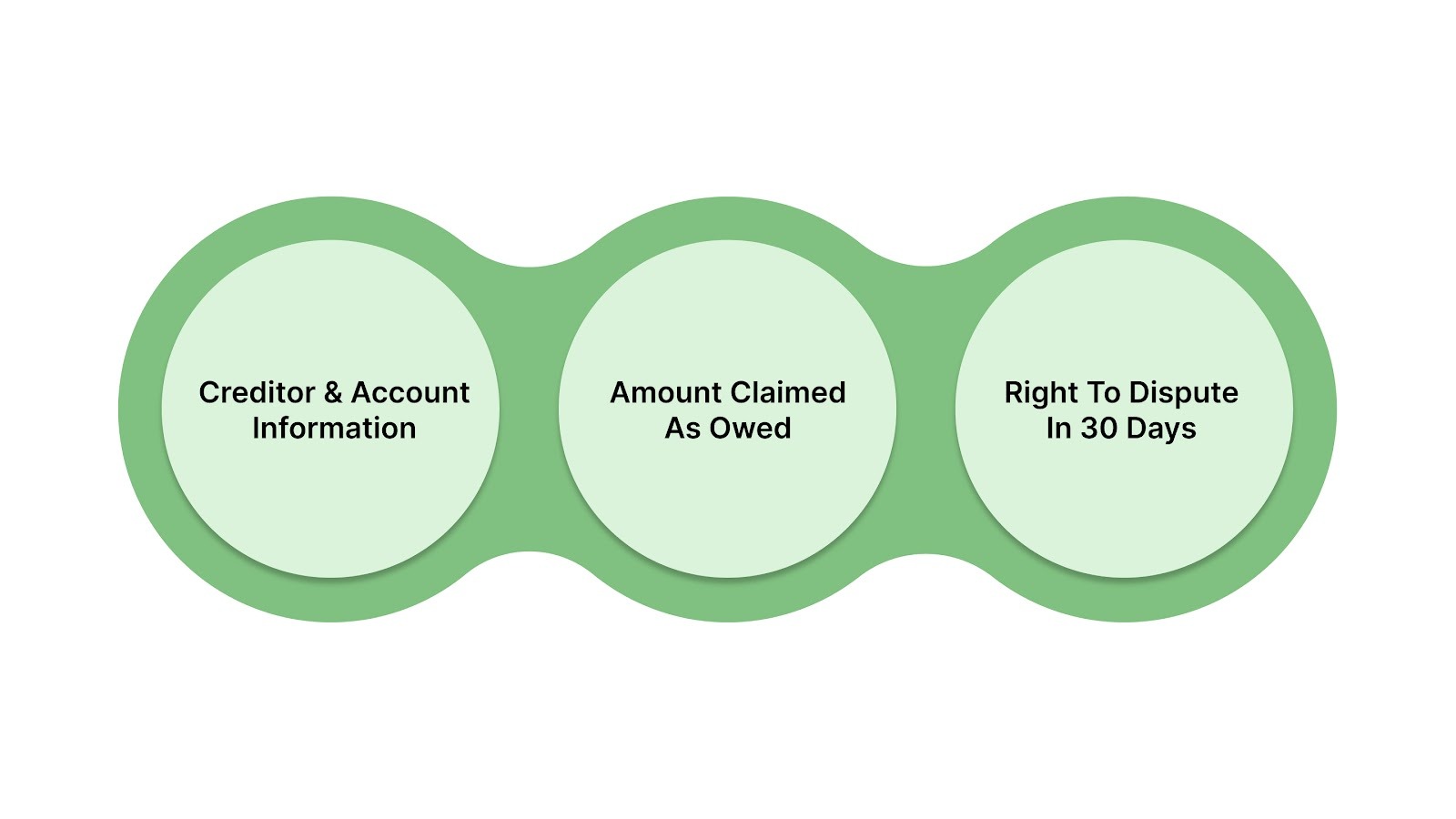

- Creditor and account information: The letter identifies the current creditor and usually names the original creditor, along with an account reference. This allows you to determine whether the debt corresponds to an account you recognize.

- Amount claimed as owed: It states the total amount the collector claims is due at the time of the notice. This figure may include interest or fees and may differ from what you remember owing.

- Your right to dispute within 30 days: Federal law gives you 30 days from receipt of the notice to dispute the debt in writing. If you do so within that period, the collector must pause collection activity until it provides verification of the debt.

Why This Matters

Disputing the debt within the 30-day window triggers legal obligations for the collector. If you do not dispute within that timeframe, the collector may assume the debt is valid for collection purposes and may continue collection efforts, subject to other legal limits.

Also Read: How to Manage Your Debt: Tips and Strategies

With the key details of a debt validation letter in mind, it’s time to confirm whether the debt is accurate and truly yours.

Steps to Confirm and Validate Your Debt

The steps below walk you through how to confirm the claim, request proof when needed, and choose a response that protects your financial position.

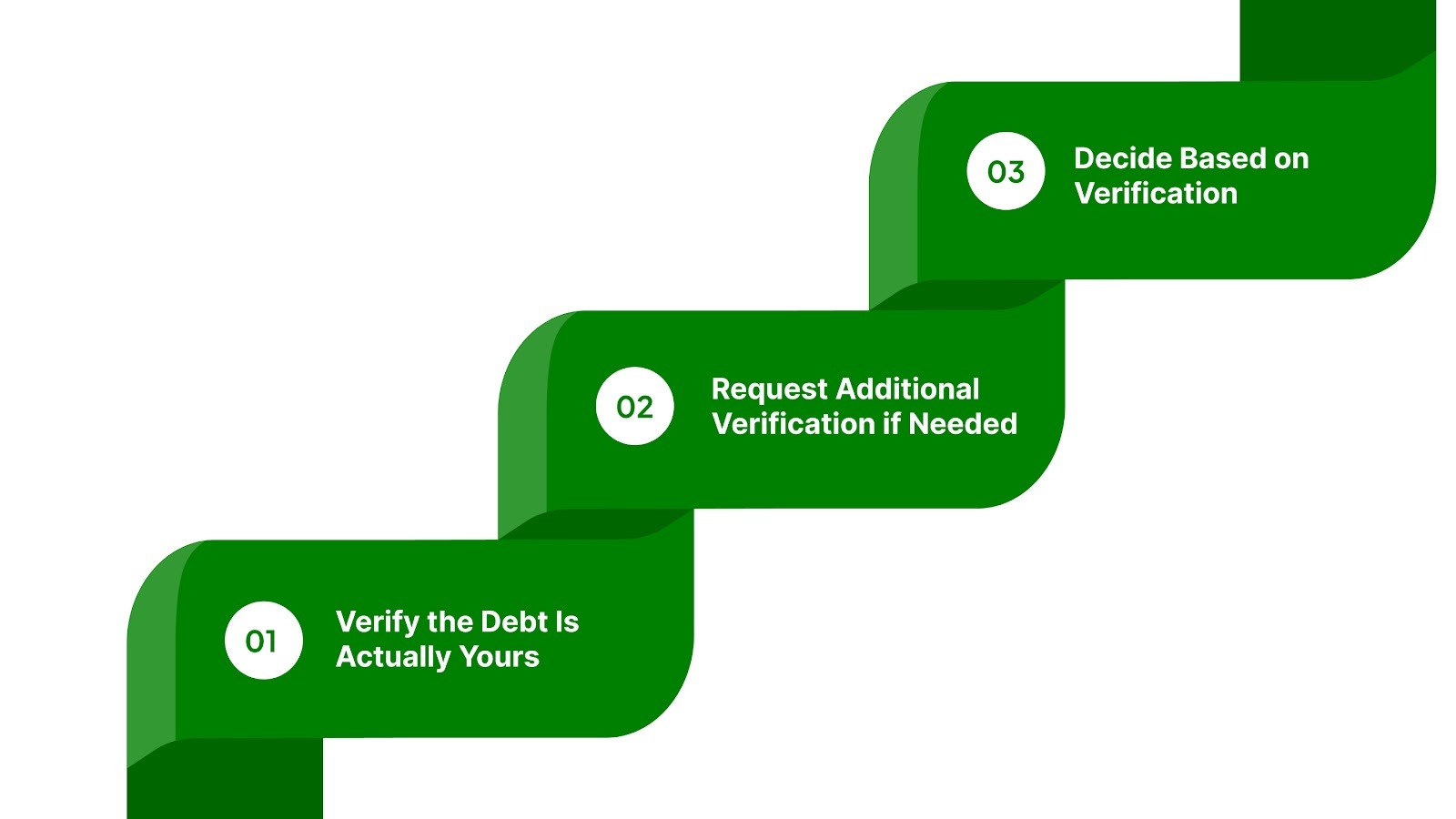

Step 1: Verify the Debt Is Actually Yours

Cross-check the claim before you commit to anything. Paying a debt that isn’t yours has lasting consequences. It legitimizes an account that doesn’t belong on your credit file, wastes money, and signals that you’ll accept claims without scrutiny. Verification isn’t skepticism; it’s a basic step in protecting your financial position.

Start by confirming the fundamentals:

- Original creditor: Does the creditor name match a company you recognize? Debts are often sold multiple times, and the current collector’s name alone doesn’t matter; the source does.

- Amount claimed: Compare the balance to your own records. The total may have increased, but the underlying figure should connect to something you remember owing.

- Personal details: Check your name, address, and account number carefully. Errors here can indicate the debt was mismatched to you, especially if you have a common name or recently moved.

- Statute of limitations: Determine whether the debt is time-barred under your state’s law. Once that window expires, the debt still exists, but the creditor’s ability to sue does not. In some states, even a small payment can restart that clock.

Step 2: Request Additional Verification if Needed

The initial letter provides a snapshot, not proof. If anything doesn’t align, you have the right to request documentation that shows the debt legitimately belongs to you. This step is about confirming that the claim is supported before you decide how to respond.

Focus your request on concrete records:

- Original agreement: A copy of the signed contract or account agreement that created the debt.

- Payment history: A complete record showing what was paid, when, and how the balance changed over time.

- Balance breakdown: An itemized explanation of interest, fees, or charges that make up the current amount claimed.

Send your request in writing, preferably by certified mail with a return receipt, so you have proof of delivery and timing. Once the collector receives your request, federal law requires them to pause collection activity until they provide adequate verification.

That pause gives you space to evaluate what comes back; and whether the claim actually holds up.

Step 3: Decide Your Next Move Based on Verification

Once verification comes back, or doesn't, you're no longer guessing. The path forward depends on what the documentation proves and what your financial position allows.

If the Debt Is Accurate and You Can Afford to Pay

Paying in full closes the account and stops collection activity, but negotiation may still be an option. In some situations, collectors may accept a reduced lump-sum amount, depending on the account and its age.

Before making any payment, confirm the terms in writing:

- Resolution amount: The exact payment that satisfies the account.

- Reporting status: Whether the debt will be reported as “paid in full” or “settled.”

- Finality: Written confirmation that no balance will remain after payment clears.

Without this documentation, you risk disputes later over what was agreed to.

If the Debt Is Accurate but You Can't Pay in Full

A structured repayment plan breaks the balance into smaller, predictable amounts designed to be manageable over time. Many collectors are willing to consider this approach if you can show consistency and follow-through. The key is proposing terms you can actually maintain.

When putting a plan forward:

- Base payments on your real budget: Offer a monthly amount you can sustain, not what the collector initially asks for.

- Be realistic: Committing to $200 a month when you can only afford $75 increases the risk of default.

Payment plans aren't guaranteed. The collector can reject your proposal. But offering something concrete shows intent to resolve the account, which often works in your favor.

If the Debt Contains Errors or Isn't Yours

When a claim is incorrect, your response should be formal and specific. A written dispute forces the collector to justify the debt rather than relying on an assumption, and it creates a record of your challenge.

In your dispute:

- Identify the exact issue: State whether the amount is wrong, the account isn’t yours, or the balance includes unauthorized charges.

- Include supporting evidence: Attach any documents that back up your position.

- Keep it in writing: This ensures the dispute triggers the required review process.

Once submitted, the dispute requires the collector to investigate. They must either correct the error or verify the debt as accurate. If the debt can’t be verified or is found to be invalid, it should no longer be reported as collectible and may be removed from your credit report. If it is verified, collection activity may resume.

Also Read: Best Debt Payment Gateways and How They Work

After verification and response, the next phase begins. Knowing what happens after a dispute helps you stay in control and avoid surprises.

What Happens After You Dispute the Debt

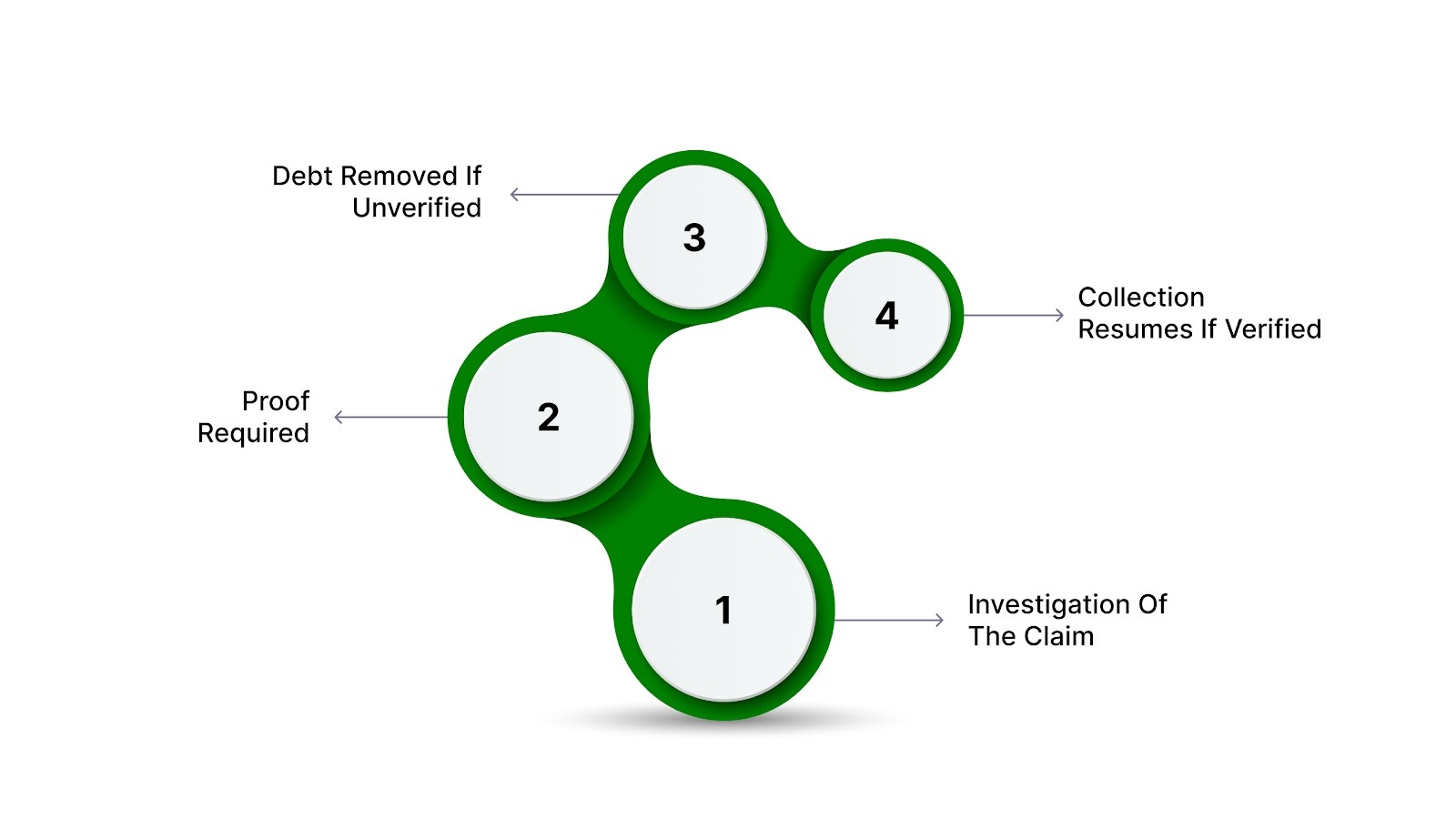

Filing a dispute doesn't just challenge the collector's claim. It activates a specific sequence of actions they're required to follow.

Once a written dispute is received, collection activity is required to pause while the claim is reviewed. They can't call, send additional letters, or report the debt to credit bureaus while the investigation is underway. That pause protects you from escalating pressure while they review the account.

Here's what the process looks like:

- They investigate the claim: The collector reviews their records, contacts the original creditor if necessary, and gathers documentation to support or refute the dispute

- They must provide proof: If the debt is legitimate, they're required to send you evidence: original contract, payment history, or account statements that verify your responsibility

- If they can't verify, the debt is removed: Lack of proof means the account must be closed and erased from your credit file

- If they verify, collection resumes: Once substantiated, they can continue pursuing payment, but you'll have clarity about the legitimacy of the claim

Disputes don't always succeed. But they force a checkpoint that separates valid debts from errors or mismatches that shouldn't be your problem.

Knowing what happens after a dispute is only half the equation. Just as important is avoiding the mistakes that can undermine your position during the validation process.

Common Pitfalls to Avoid During the Validation Process

Mistakes during validation don't just slow things down. They can restart legal timelines, weaken your position, or lock you into obligations you could have avoided.

The validation window is short, and certain actions carry consequences that aren't immediately obvious. Understanding where people commonly trip up helps you sidestep those same missteps.

Also Read: How Debt Stacking Can Accelerate Your Journey to Financial Freedom

Now that you know what not to do, the next step is understanding how to handle validation correctly, without risking your rights or your time.

How Forest Hill Management Supports the Validation and Resolution Process

Validation should bring clarity, not more stress. When you’re already dealing with uncertainty around an account, the last thing you need is confusion about what information you’re entitled to or what steps come next.

At Forest Hill Management, the validation process is handled with transparency and care. Our goal is to make sure you understand the account, your options, and how to move forward, without pressure or unnecessary complexity.

What this means for you:

- Clear validation information

You receive the details required under U.S. consumer protection laws, with additional documentation provided upon request if you need further verification.

- Straightforward dispute support

If something doesn’t look right, you’re given clear, reasonable steps to raise concerns and have them reviewed properly.

- Flexible repayment options once verified

When an account is confirmed, you can explore structured payment solutions designed to fit your financial situation.

- Secure online account access

View balances, payment history, and next steps through a protected online portal, so you always know where you stand.

- Access to real support

Knowledgeable advisors are available to help explain your options and answer questions, so you’re not navigating the process alone.

If you’re ready to take the next step, you can make a payment online or contact Forest Hill Management at (888) 471-0109 for clear, supportive guidance.

Conclusion

Debt validation isn’t about confrontation or delay. It’s about creating a moment of clarity before a financial decision becomes permanent. When you understand what’s being claimed, what’s required, and what’s optional, pressure loses its power, and choices become yours again.

If you’re ready to move forward, whether that means resolving an account or simply understanding where you stand, support should make the process feel steadier. Forest Hill Management exists to help you take that next step with clarity, respect, and a path that fits your real situation.

Take the next step when you’re ready - make a secure payment online or contact Forest Hill Management for clear, compliant support.

FAQs

1. Can a debt collector contact me in states where they are not licensed?

Collectors must be licensed in many states to legally collect. If they aren’t, their actions may violate state rules. You can report unlicensed collectors, which may strengthen your legal position.

2. How does the sale of debt to another collector affect my rights?

A new owner of your debt doesn’t automatically inherit prior errors. Clear documentation of ownership is required, and knowing who owns the debt affects your ability to challenge or negotiate it.

3. Can a debt validation dispute affect interest accrual or penalties?

In some cases, interest or penalties may continue to accrue under the original agreement, depending on the account terms. Understanding this helps you plan negotiations and estimate what you may owe.

4. Are there consequences if a debt collector reports your dispute to credit bureaus incorrectly?

Collectors must report disputes accurately. Misreporting, like marking a disputed debt delinquent, can harm your credit, and you can request corrections to prevent long-term damage.