Ethical Debt Collection Practices and Strategies

Need Help Reviewing Your Account?

Contact UsYou’re not reacting to debt alone; you’re reacting to how it was handled. In 2024, the Consumer Financial Protection Bureau (CFPB) logged 207,800 debt collection complaints, largely tied to unclear claims and disputed balances.

When information stays vague and contact feels relentless, uncertainty turns into stress. CFPB findings show one in four consumers felt threatened, often because communication lacked clarity.

That gap reveals a deeper issue. Collection becomes harmful when pressure replaces explanation, even though debt resolution works best when expectations stay clear and respectful. Ethical debt collection operates on this difference, not by denying debt, but by changing how it’s addressed.

This article shows what ethical debt collection looks like, how it contrasts with aggressive tactics, and how it helps you resolve debt clearly and calmly.

Key Takeaways

- Debt stress grows when collection is unclear or aggressive; clear, transparent communication reduces confusion and anxiety.

- Ethical collection protects both you and collectors from legal consequences and financial pitfalls.

- Written validation and accurate account information give you leverage and prevent unfair pressure or mistakes.

- Predictable contact and flexible, realistic payment options support long-term financial stability and recovery.

- Aggressive threats, harassment, and false claims backfire, slowing and complicating resolution.

What Defines Ethical Debt Collection?

Ethical collection operates from a simple premise: debt exists, but how it gets resolved determines whether the process damages you further or creates an actual path forward. The difference shows up in every phone call, letter, and payment conversation you have.

When a collector follows ethical standards, they're bound by more than courtesy. Federal laws like the Fair Debt Collection Practices Act (FDCPA) and state-level consumer protections establish minimum behavior requirements. Ethical companies treat these as baselines, not loopholes to navigate around.

What this looks like in practice:

- Every claim about what you owe gets backed by documentation you can verify

- Your rights as a consumer get explained upfront, not buried in fine print or ignored entirely

- Payment discussions focus on realistic repayment structures rather than scripted demands designed to extract the largest amount fastest

- Your financial circumstances receive acknowledgment, not as excuses, but as factors that shape realistic solutions

- Contact follows predictable patterns within legal limits, so you're not ambushed at work or during dinner

Understanding what separates lawful collection from boundary-crossing behavior starts with knowing what protections already exist.

Core Components of Lawful Collection Practices

Lawful debt collection ensures you get accurate information, fair contact, and secure handling of your personal data. Here’s how these protections work in practice:

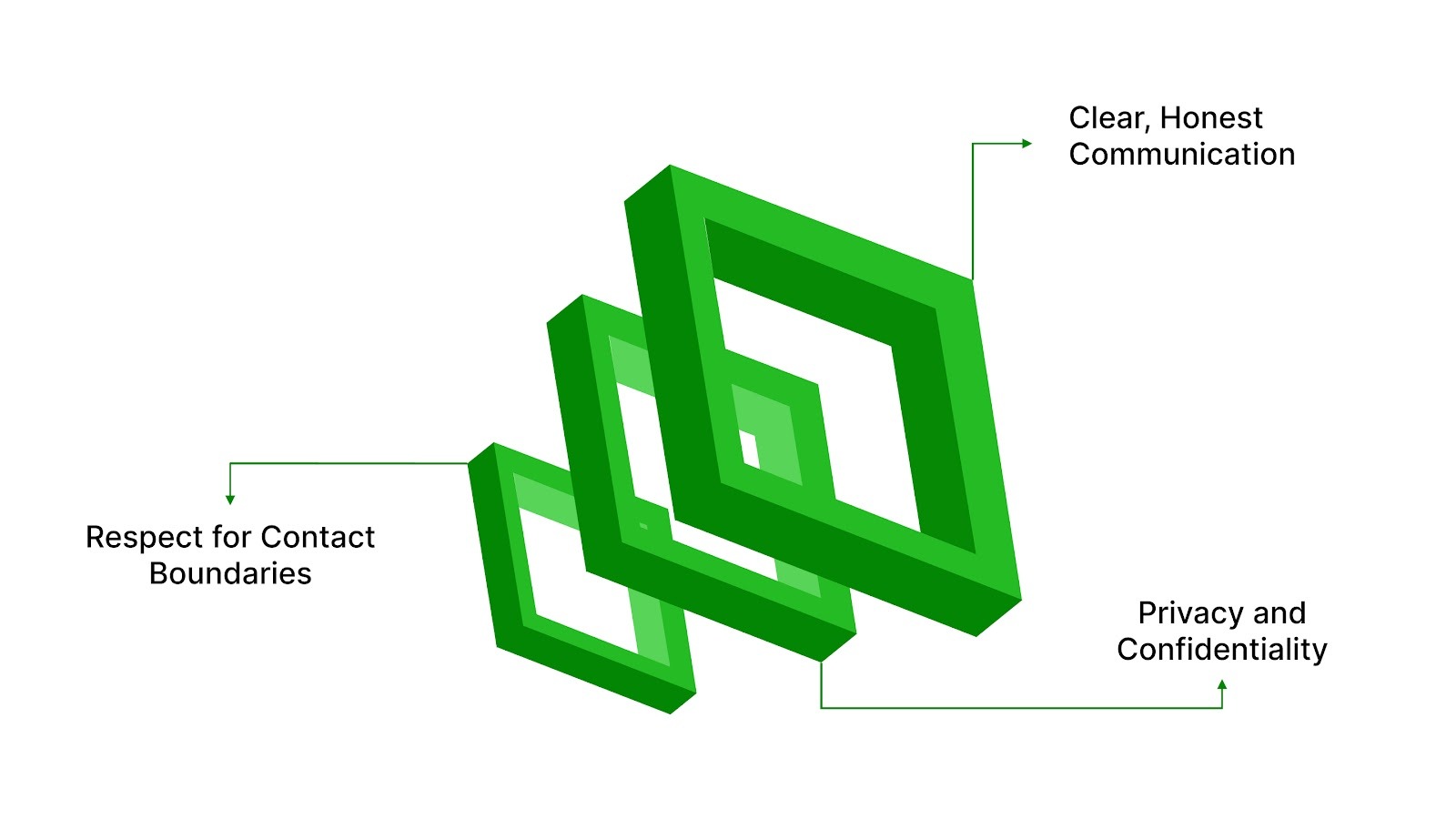

1. Clear, Honest Communication

From the very first contact, you have the right to know exactly what’s being claimed and who is claiming it. Ethical collectors provide full account details right away, and misrepresentation goes beyond lying about the amount. Written validation is your legal right, not a courtesy. Specifically:

- Full account disclosure: Original creditor, current balance, date of last payment, and calculation of the debt.

- Avoiding misrepresentation: No overstating authority, implying false legal consequences, or creating fake urgency (e.g., threats of wage garnishment or arrest without court involvement).

- Written validation notice within five days: Collectors must send a written notice outlining debt details and your right to dispute.

2. Respect for Contact Boundaries

Collectors must keep communication within legal hours and avoid overwhelming or persistent contact. Written requests to stop communication also have strict rules. Here’s what respecting contact boundaries looks like in debt collection:

- Legal contact hours: Calls must be between 8 AM and 9 PM in your time zone; outside this is harassment.

- Reasonable frequency: Repeated or excessive contact intended to harass or pressure may violate FDCPA standards.

- Cease contact requests: Once submitted in writing, collectors can only confirm receipt or notify you of legal actions; they cannot call or send letters to pressure you to reconsider.

3. Privacy and Confidentiality

Collectors must keep your debt information private and handle your personal data securely. Key points to note here:

- Limited disclosure: Your account can only be discussed with you, your spouse, or your attorney.

- Third-party contact: Others can be contacted solely to locate you; collectors cannot reveal that you owe money.

- Data security: Account details and sensitive info like payment information or Social Security numbers are stored securely with restricted access.

Also Read: How to Win Debt Collection Disputes: A Complete Step-by-Step Guide

The line between following these standards and exploiting their absence becomes obvious when you compare practices side by side.

How Ethical Practices Differ From Aggressive Tactics

The gap between lawful collection and pressure-driven tactics isn't subtle. It shows up in language, timing, and whether the collector treats resolution as mutual problem-solving or a zero-sum extraction.

Here’s a side-by-side look at how ethical collection practices differ from aggressive tactics:

Tone and transparency reveal a collector’s intent. Ethical collectors provide clear explanations and options, while aggressive ones use fear and vague claims to pressure you. Full disclosure, like the debt’s origin, account details, and interest calculations, is a hallmark of lawful, professional practices.

Also Read: Integrating Compliance Management Systems with Debt Collection Platforms

These distinctions matter beyond individual interactions. They shape whether the collection process becomes a source of lasting harm or a manageable path forward.

Why Ethical Collection Protects You Long-Term

Debt collection is stressful, but unlawful tactics, like threats of lawsuits, arrests, or wage garnishments, carry legal risks for collectors and provide grounds to challenge the debt.

For instance, in December 2024, the FTC refunded over $540,000 to consumers threatened with debts they may not have owed. Courts have also awarded damages or penalties when rights were violated.

Ethical practices eliminate that risk by keeping every step defensible. Realistic resolution paths only exist when collectors acknowledge your actual circumstances. Here's why that matters:

- Payment plans structured around your income don't collapse after two months, forcing you back into default

- Accurate information about your balance prevents surprise charges or interest calculations you never agreed to

- Documented agreements create accountability, so terms don't shift midway through repayment

- Respectful engagement makes it possible to ask questions, request adjustments, or raise concerns without retaliation

Long-term financial recovery depends on stable, predictable interactions. Ethical collection provides that foundation. Aggressive tactics destabilize it, often making the original debt worse through added fees, damaged credit from inaccurate reporting, or legal complications that could have been avoided.

Recognizing when a collector has abandoned ethical standards helps you identify situations where you need to act, not just comply.

Red Flags That Signal Unethical Collection Behavior

Not every violation announces itself clearly, but certain patterns indicate a collector has stopped following legal requirements. Knowing what to watch for helps you distinguish between firm-but-fair practices and outright misconduct.

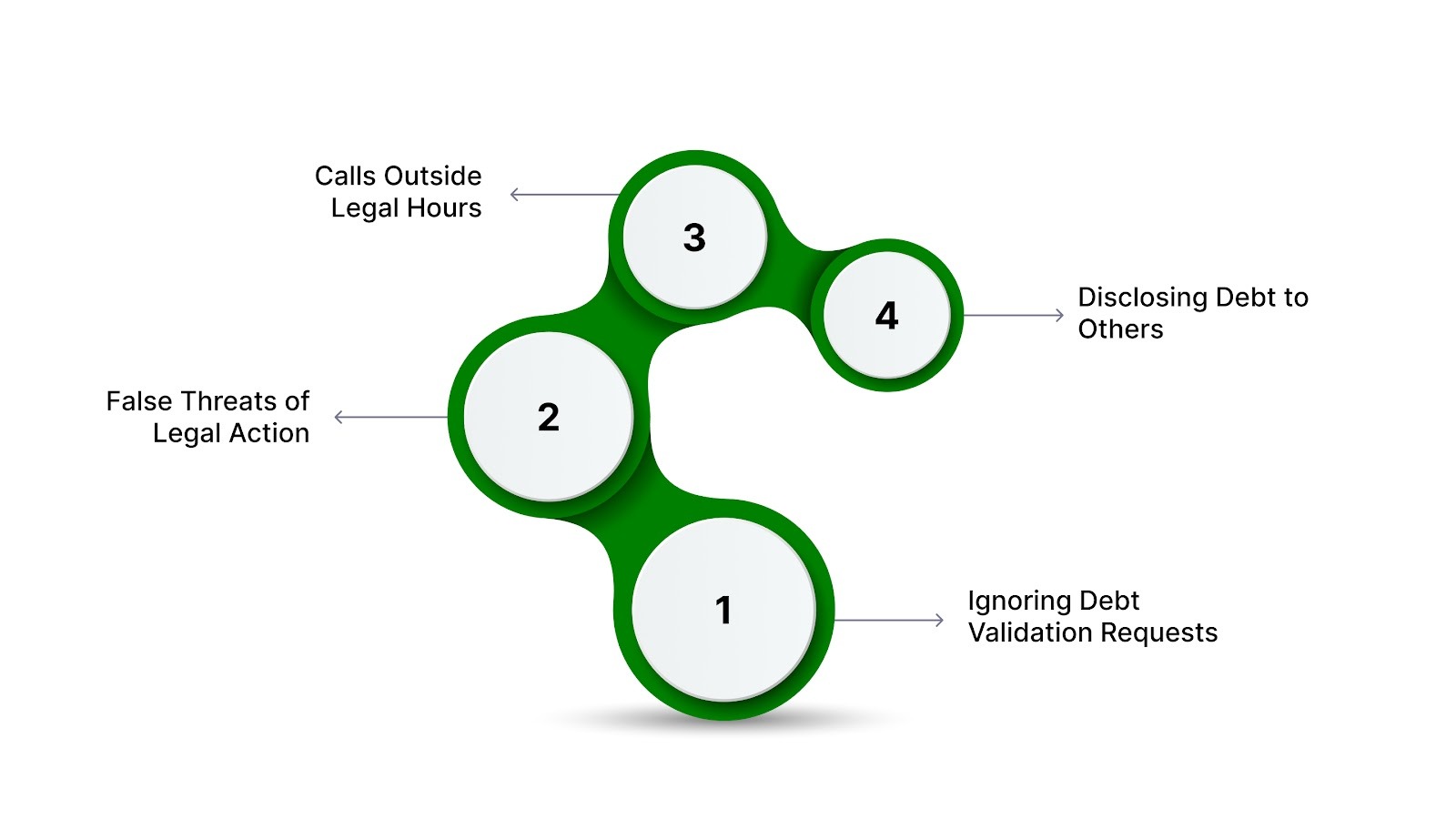

1. Ignoring Debt Validation Requests

If you ask for written proof of the debt and the collector stalls, redirects, or insists you pay first, something's wrong. Validation is a legal right.

Once a written dispute is submitted, collectors must pause collection activity until verification is provided. Any attempt to bypass this process signals they either don't have proper records or they're hoping you won't push back.

2. False Threats of Legal Action

Consumer debt isn't a criminal matter. You cannot be arrested for unpaid credit cards, medical bills, or personal loans. Collectors who claim otherwise are lying to scare you into payment.

The same applies to threats about seizing property without a court judgment or filing criminal charges for non-payment. These tactics are illegal, full stop.

3. Calls Outside Legal Hours

One early-morning call might be a mistake. A pattern of calls before 8 AM or after 9 PM isn't. If you've told the collector your time zone and they continue calling outside legal hours, they're either ignoring the law or testing whether you'll tolerate it. Either way, it's a violation.

4. Disclosing Debt to Others

The moment a collector tells someone else about your debt, they've broken federal law. This includes leaving voicemails that reveal why they're calling, sending letters to your workplace that mention payment, or discussing your account with anyone who isn't legally authorized.

Also Read: How Fintech is Transforming Debt Collection Practices

Understanding these warning signs makes it clear why ethical practices matter, and why choosing the right account manager can make all the difference.

How Forest Hill Management Prioritizes Ethical Account Management

Ethical collection isn't about following a checklist to avoid lawsuits. It's about recognizing that people dealing with debt are already under stress, and adding confusion or pressure only makes resolution harder for everyone involved.

Forest Hill Management operates on the principle that transparency and respect aren't optional extras. They're how account management should work from the beginning.

What that means for you:

- Compliance isn't negotiable: Every process follows federal consumer protection laws, no exceptions or gray areas.

- Clear, honest communication: You receive accurate information about your account from the first contact, not vague threats or misleading claims.

- Respect for your situation: Payment plans structured using the information you choose to share, not arbitrary demands that ignore your reality.

- Secure, transparent systems: Your financial data is protected, and your privacy is maintained throughout the process.

- Support, not pressure: Our support teams provide clear account assistance without intimidation, manipulation, or scripted sales tactics.

If you're ready to work with a company that values transparency and lawful practices, make a payment online or call (888) 471-0109 for respectful, compliant support.

Conclusion

Facing debt can feel isolating, but understanding the value of respectful and responsible resolution gives you a sense of control and confidence in your next steps. By choosing approaches that prioritize clarity and fairness, you equip yourself to navigate challenges with calm and purpose.

Taking action, no matter how small, creates momentum toward regaining stability. When you’re ready to move forward, Forest Hill Management is here to guide you with approachable, supportive assistance every step of the way.

Take the first step toward resolving your account with support you can trust - contact our advisors today.

FAQs

1. How can ethical debt collectors support long-term financial literacy?

Beyond resolving debts, some ethical collectors provide education on budgeting, credit score impact, and repayment planning. This guidance helps consumers understand interest accumulation, avoid future pitfalls, and make informed financial decisions beyond the current account.

2. Can ethical debt collection improve credit reporting accuracy?

Yes. Collectors who maintain documentation and report payments responsibly help ensure credit bureaus reflect accurate balances, payment history, and dispute outcomes. This prevents erroneous entries that could harm your credit score.

3. How do ethical collections handle partial payments or negotiation requests differently?

Ethical collectors clearly explain available repayment arrangements, document any agreed terms, and avoid proposing options that create unsustainable commitments.

4. Are there industry standards for training debt collectors in ethical practices?

Yes. Leading companies provide training on communication, dispute handling, empathy, and compliance. Staff are taught to identify vulnerable consumers, avoid coercion, and prioritize problem-solving over profit.

5. How do ethical practices influence dispute resolution outside of court?

By documenting interactions and providing clear records, ethical collection firms facilitate faster, fairer dispute resolution. Consumers and creditors can resolve disagreements directly, reducing the need for formal legal intervention.