Effective Debt Management Tips and Strategies

Transform Your Financial Future

Contact UsIf you're juggling credit cards, student loans, car payments, and medical bills simultaneously, you're not alone — and you're not without options. U.S. household debt reached $18.8 trillion in Q1 2026, with the average consumer carrying $105,444 in total debt. That weight is real, but it doesn't have to be permanent.

This guide walks through everything you need to take control: understanding what you actually owe, choosing a repayment strategy that fits your personality, building a budget that sticks, protecting yourself from new debt, and knowing when to call in professional help.

Key Takeaways

- Distinguishing good debt from bad debt helps you prioritize which balances to attack first.

- A debt audit — listing every balance, rate, and minimum payment — is the non-negotiable first step.

- The snowball and avalanche methods are both proven — choose based on your motivation style.

- A budget and a starter emergency fund are your two strongest defenses against spiraling deeper.

- Past-due accounts are a solvable financial situation — Forest Hill Management can help you work through them.

Understanding Good Debt vs. Bad Debt

Not all debt costs the same or works the same. The distinction matters because it shapes where you direct your repayment energy.

Good debt — mortgages, federal student loans, small business loans — typically carries lower interest rates and finances something with return potential. As of June 2026, the average 30-year fixed mortgage sits at 6.47%, and federal undergraduate Direct Loans are fixed at 6.39% for the 2025–2026 year.

Bad debt — primarily high-interest credit cards and payday loans — drains money without building anything. Credit card accounts averaged 21.00% APR in Q1 2026, according to Federal Reserve G.19 data. That's more than three times the cost of a mortgage.

That contrast matters, but the categories aren't absolute. Too much "good" debt can still become unmanageable if the monthly payments stretch your cash flow too thin — and that's exactly what your debt-to-income ratio measures.

Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is the clearest single measure of whether your debt load is sustainable. Calculate it like this:

- Add up all minimum monthly debt payments

- Divide by your gross monthly income

- Multiply by 100

What the numbers mean:

- Below 36% — Generally healthy; most lenders are comfortable here

- 36–50% — Caution zone; limited financial flexibility

- Above 50% — Serious concern requiring immediate action

Fannie Mae guidelines allow DTIs up to 45%, and up to 50% with compensating factors — but those are lender maximums, not personal finance targets. If your DTI is climbing toward 50%, the practical response is to prioritize paying down high-interest balances first and review any recurring obligations that can be reduced or eliminated.

Conduct a Debt Audit: Know Exactly What You Owe

Most people have a rough sense of their debt — but a rough sense isn't enough to build a plan. Vague awareness leads to vague decisions. A full debt inventory replaces that uncertainty with specific, actionable numbers you can actually work with.

What to Include in Your Debt Inventory

For every debt you carry, record these four data points:

- Creditor name: the lender, servicer, or collection agency holding the account

- Total balance: the current amount outstanding, not the original loan amount

- Minimum monthly payment: what keeps the account current each billing cycle

- Interest rate (APR): what each debt is actually costing you over time

That combination creates a complete debt snapshot. Once it's on paper (or a spreadsheet), you can rank debts by cost and build a plan.

Pull your free credit report from AnnualCreditReport.com — the only federally authorized source — before finalizing your list. This surfaces any past-due or collection accounts you may have lost track of. 23% of Americans had debt in collections as of August 2025, with a median collection balance of $2,528. If you're in that group, seeing it clearly on your report is better than discovering it later.

Calculate Your Debt-to-Income Ratio

Once you have your inventory, run your DTI calculation using the steps above. The Federal Reserve's household debt service ratio sat at 11.16% in Q1 2026 — a population-level benchmark, not a personal target, but useful context for where American households collectively stand.

Proven Strategies to Pay Off Debt Faster

With a complete debt picture in hand, you can choose a repayment strategy. Three approaches work well for most people: the snowball method, the avalanche method, and consolidation. Consistency matters more than which method you pick — so start with the one that fits how you're wired.

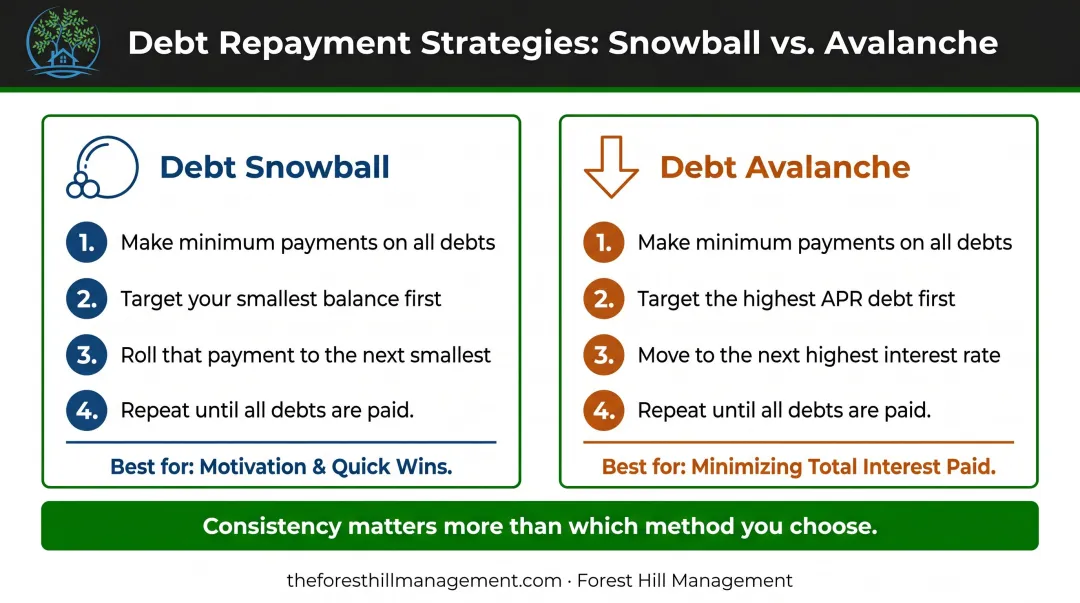

The Debt Snowball Method

The snowball method focuses on smallest balance first:

- Make minimum payments on all debts

- Direct every extra dollar toward your smallest balance

- Once it's paid off, roll that payment into the next smallest

- Repeat until all debts are gone

Research published in the Journal of Consumer Research found that concentrated repayment — focusing on small accounts — increases motivation and leads consumers to pay more aggressively over time. The psychological wins of clearing accounts matter. If motivation is your main obstacle, snowball is your method.

The Debt Avalanche Method

The avalanche method focuses on highest interest rate first:

- Make minimum payments on all debts

- Direct all extra funds toward the highest-APR balance

- Once eliminated, move to the next highest rate

- Continue until all debts are cleared

This approach saves the most money in interest over time — mathematically, it's the superior choice. The tradeoff is patience. If your highest-rate debt also carries a large balance, you may not see a "win" for months. That's manageable for some people; for others, it erodes momentum.

Debt Consolidation and Refinancing

Debt consolidation combines multiple debts into a single loan at a lower interest rate, simplifying payments and reducing total interest paid. It works best for borrowers with good credit and multiple high-rate accounts.

Two related tools worth knowing:

- Balance transfer cards with 0% introductory APRs let you temporarily eliminate interest on credit card debt. These introductory periods typically run 12 to 21 months, with transfer fees of 3–5% and good credit generally required to qualify.

- Refinancing replaces a high-rate loan with one carrying better terms — useful when interest rates have dropped or your credit score has improved since you originally borrowed.

Both options require discipline: if you consolidate and then run up new balances, you've made your situation worse.

Additional Tactics to Accelerate Repayment

Two underused moves that can meaningfully speed things up:

- Apply windfalls directly to debt — Tax refunds, work bonuses, and unexpected income should go straight to your highest-priority balance before they get absorbed by daily spending.

- Negotiate your interest rate — A LendingTree survey found that 76% of cardholders who asked for a lower APR in the past year were successful, with an average reduction of 6.3 percentage points. One phone call costs nothing.

Build a Budget That Works for Debt Repayment

A budget is the mechanism that turns repayment intentions into actual payments. Without one, there's no reliable way to know how much you can realistically put toward debt each month.

A 2023 NerdWallet survey found that 74% of Americans have a monthly budget, but 84% of those budgeters sometimes exceed it — meaning the real work isn't creating a budget, it's following through on one.

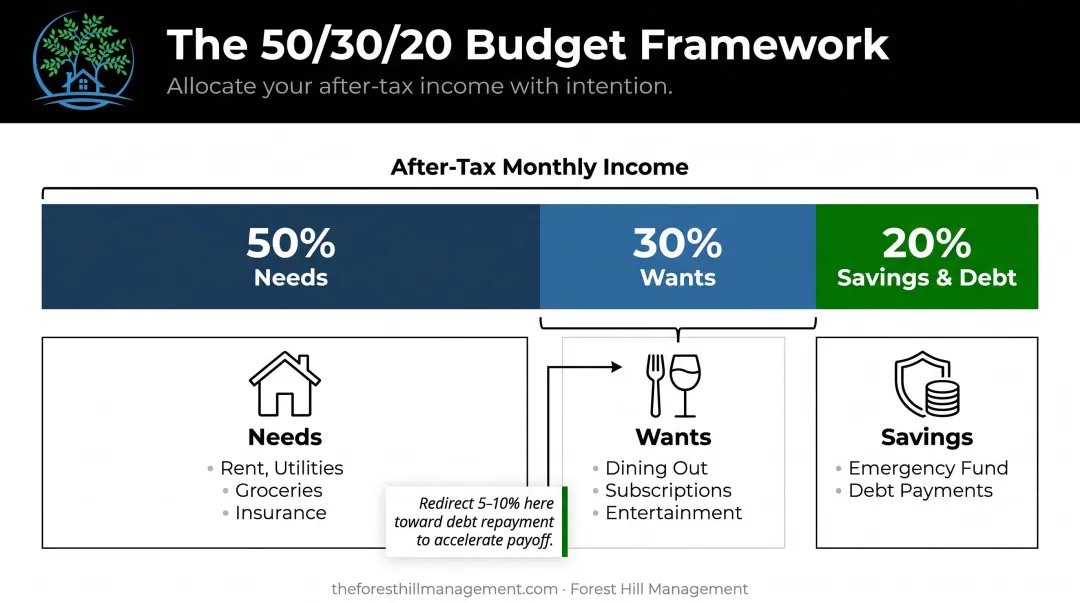

The 50/30/20 Framework as a Starting Point

The 50/30/20 rule (introduced by Elizabeth Warren and Amelia Warren Tyagi in All Your Worth) allocates after-tax income this way:

If you're carrying significant high-interest debt, consider temporarily shifting your "wants" allocation — pulling 5–10% from that bucket and redirecting it to debt repayment until balances are under control.

Quick wins for freeing up extra cash:

- Audit and cancel unused subscriptions

- Reduce discretionary dining to a fixed weekly amount

- Review recurring charges on bank and credit card statements

Automate Payments to Stay Consistent

Once your budget is mapped out, automation keeps it running without relying on memory or willpower. Set up automatic minimum payments on every account — this prevents late fees, protects your credit score through consistent on-time payment history, and removes the temptation to skip a payment during a tight month.

Federal student loan borrowers enrolled in autopay receive at least a 0.25% interest rate reduction — and as of June 2026, the U.S. Department of Education announced a temporary 1% reduction for eligible borrowers in autopay. Confirm with your loan servicer whether that reduction applies to your account.

Build Your Financial Safety Net

Start with a Small Emergency Fund

Here's the trap many people fall into: they focus entirely on debt repayment, leave no cash buffer, and the first unexpected expense — a car repair, a medical bill, a temporary job loss — goes straight on a credit card, wiping out weeks of progress.

The Federal Reserve's 2025 household survey found that only 63% of adults could cover a $400 emergency using cash or equivalent, and 12% could not cover it by any means. An emergency fund isn't optional; it's structural protection.

You don't need three to six months saved before you start attacking debt. Start with one month of essential expenses. That buffer alone breaks the cycle of emergency-to-credit-card.

Once that buffer is in place, the next priority is making sure you're not adding new debt while paying down the old.

Avoid Accumulating New Debt

While repaying existing balances:

- Freeze or lock credit cards rather than closing them — this preserves your credit utilization ratio and account history

- Stick to your budget for discretionary spending

- Avoid financing new purchases during the repayment period

When it comes to balancing debt repayment with investing, start by capturing any employer 401(k) match — that matched contribution doubles your money before market returns even factor in. Beyond that, Fidelity guidance suggests that debt with interest rates of 6% or higher generally warrants paying down before investing additional unmatched dollars.

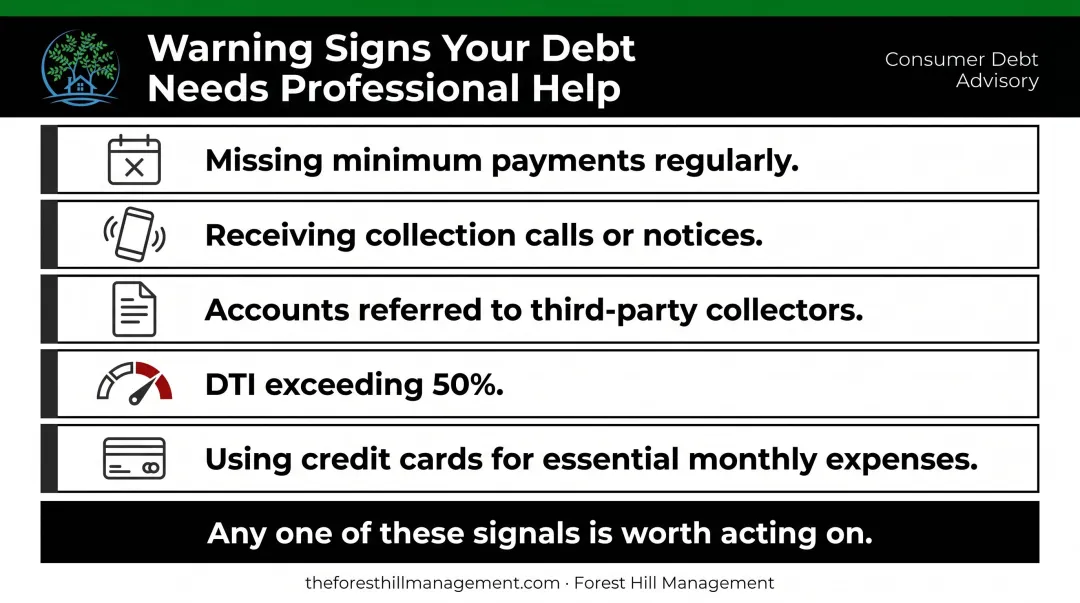

When to Seek Professional Help for Past-Due Accounts

Warning signs that debt has moved beyond self-management:

- Missing minimum payments regularly

- Receiving collection calls or notices

- Accounts being referred to third-party collectors

- DTI exceeding 50%

- Using credit cards to cover essential monthly expenses

Reaching this point isn't a personal failure — it's a signal that the situation calls for structured support rather than solo effort.

Forest Hill Management works with consumers who have past-due accounts, helping them understand their options, set up flexible payment plans, and move through the resolution process with clear guidance. Consumers can reach them by phone at (888) 471-0109, by email at info@foresthillmanagement.com, or through the online payment portal at pay.theforesthillmanagement.com.

Timing also has a direct impact on credit recovery. The CFPB notes that negative payment information can remain on a credit report for up to seven years, and payment history accounts for 35% of a FICO Score — which means addressing a past-due account sooner shortens the path back to financial stability.

Frequently Asked Questions

What is a good way to manage debt?

Start with a full debt audit listing every balance, rate, and minimum payment. Then choose a repayment strategy — snowball or avalanche — build a budget, and automate payments. Avoid taking on new high-interest debt while working through existing balances.

What is the difference between the snowball and avalanche debt repayment methods?

The snowball method pays the smallest balances first for motivational quick wins, while the avalanche method targets the highest-interest debt first to minimize total interest paid. Both work. If early wins help you stay consistent, start with snowball. If you want to minimize what you pay overall, go avalanche.

How do I know if my debt has become unmanageable?

Key signals include consistently missing minimum payments, receiving collection notices, carrying a DTI above 50%, or relying on credit cards to cover basic monthly expenses. Any one of these warrants a closer look and potentially professional help.

Should I pay off debt or build an emergency fund first?

Build a small starter fund — one month of essential expenses — before aggressively attacking debt. Without that buffer, any unexpected expense sends you back to the credit card, undoing progress. Once the buffer exists, focus on high-interest debt.

What happens if I have past-due accounts?

Past-due accounts can trigger collection activity, credit score damage, and additional fees. They can be resolved by contacting the creditor directly or working with a debt management company like Forest Hill Management to negotiate a payment arrangement and settle the obligation.

How does debt consolidation work?

Debt consolidation combines multiple debts into a single loan, ideally at a lower interest rate, simplifying payments and potentially reducing total interest paid. It typically requires a fair-to-good credit score (typically 620 or higher) to qualify for favorable terms and works best when paired with a plan to avoid accumulating new balances.