How to Manage Debt: Tips and Strategies for 2026

Transform Your Financial Future

Contact UsDebt has a way of making itself felt in every corner of daily life — the hesitation before swiping a card, the mental math at the grocery store, the low-grade anxiety that follows you into sleep. Whether it's credit card balances, student loans, auto loans, or past-due accounts sitting in collections, carrying debt affects financial confidence in ways that go beyond the numbers.

The scale is significant. Total US consumer credit outstanding reached nearly $5.1 trillion in 2025, according to Federal Reserve data — and 46% of credit card holders carried a balance at least once in 2024. That's not a niche problem. That's most American households navigating real financial pressure.

Debt itself isn't the enemy. A mortgage builds equity. A student loan can increase earning potential. The problem is unmanaged debt — debt that compounds quietly while minimum payments barely dent the principal. This guide walks through exactly how to change that in 2025: how to assess what you owe, choose a repayment strategy, reduce interest costs, protect your credit score, and recognize when professional help makes sense.

Key Takeaways

- Start with a full debt audit — every balance, interest rate, and minimum payment in one place

- Snowball and avalanche are both proven methods — pick the one that fits how you're wired, not just the numbers

- Cutting interest costs through consolidation or balance transfers can meaningfully shorten your payoff timeline

- On-time payments and low credit utilization protect your score while you pay down debt

- Seeking help from credit counselors or receivables management organizations is a smart, proactive step toward resolution

Understanding Your Debt: The First Step to Taking Control

Before choosing any repayment strategy, you need a clear picture of what you're dealing with. Most people underestimate their total debt because they think about each obligation separately — the car payment here, the credit card there. Viewing them together changes the picture entirely.

Start by listing every debt you carry:

- Creditor name

- Outstanding balance

- Interest rate (APR)

- Minimum monthly payment

- Type (credit card, auto loan, student loan, personal loan, medical bill)

Once you have this list, you can start making intentional choices about where to focus first.

Distinguishing Good Debt from Bad Debt

Not all debt carries the same urgency. Good debt — mortgages, student loans, small business loans — typically comes with lower interest rates and funds assets or earning potential that appreciate over time. Bad debt includes credit card balances carried month to month, payday loans, and high-interest personal loans used for discretionary purchases. These cost significantly more and fund things that lose value immediately.

With average credit card APRs sitting at 22.32% in 2025, according to Federal Reserve data, high-interest revolving debt deserves the most aggressive attention in any repayment plan. Knowing which debts fall into this category helps you prioritize — and that's where your debt-to-income ratio comes in.

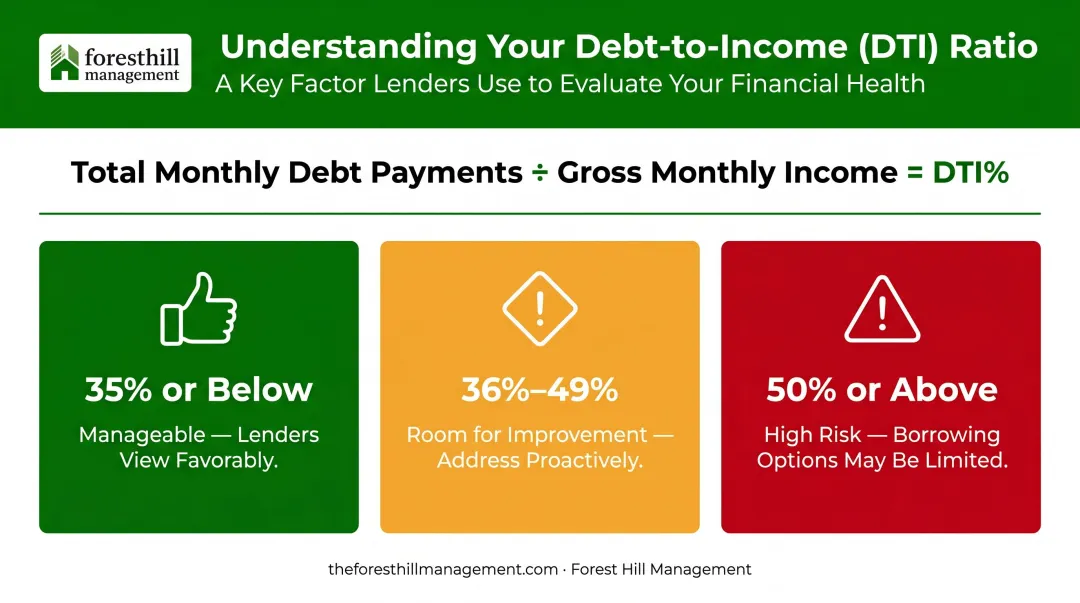

Calculating Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is simple to calculate: divide your total monthly minimum debt payments by your gross monthly income.

Here's what the numbers mean in practice, using Wells Fargo's DTI classifications:

Keeping DTI in check isn't just about debt repayment — it directly affects your ability to qualify for future loans, mortgages, and better rates.

Recognizing the Warning Signs of Debt Distress

Some patterns signal that debt has moved from manageable to problematic. Watch for these:

- Using credit cards to cover everyday expenses like groceries or utilities

- Making only minimum payments every month — a pattern that's more common than most realize, with over 11% of large-bank credit card accounts making just the minimum payment as of late 2024

- Delaying one bill payment to cover another

- Drawing down savings to pay regular monthly obligations

- Taking on new debt to pay existing debt

If two or more of these apply to you, the repayment strategies in the next section give you a concrete place to start.

Choose the Right Debt Repayment Strategy for 2025

There's no universally "best" repayment method. The best strategy is the one you'll actually stick with for months or years. Two approaches dominate — and they're built around very different motivations.

The Debt Snowball Method

The snowball method works like this:

- List all debts from smallest balance to largest

- Make minimum payments on every debt

- Direct all extra money toward the smallest balance until it's gone

- Roll that freed-up payment into the next smallest debt

The appeal is psychological. Each eliminated account feels like a win, and those wins build momentum. Research summarized by the Kellogg School of Management found that consumers who tackled smaller balances first were more likely to eliminate debt overall — precisely because small victories sustain motivation.

One downside worth knowing: you may pay more total interest over time, since you're not targeting the highest-cost debt first.

The Debt Avalanche Method

The avalanche method prioritizes math over motivation:

- List all debts from highest interest rate to lowest

- Make minimum payments on everything

- Direct extra funds toward the highest-rate debt first

- Once eliminated, move to the next highest rate

This is the mathematically superior approach — it minimizes total interest paid over the life of your debt. In a high-rate environment where credit card APRs are hovering above 22%, the interest savings can be substantial, especially for anyone carrying large balances at those rates.

The challenge is patience. If your highest-rate debt also carries a large balance, it can take months before you see that first account eliminated — and staying the course without visible wins requires real discipline.

How to Choose the Right Method for You

A simple decision framework:

- Motivated by visible progress? Snowball is more sustainable for you

- Focused on minimizing total cost? Avalanche is more efficient

- Both? A hybrid works — clear one or two small debts for momentum, then switch to avalanche for the rest

If you're still unsure, start with the snowball. Getting one account to zero builds confidence — and confidence is often what separates people who finish from people who stall.

Build a Budget That Supports Debt Repayment

A repayment strategy without a supporting budget is just a plan on paper. The budget is what converts intention into actual extra payments.

The basic calculation:

Net income − fixed expenses − variable expenses = available cash flow for debt

Fixed expenses include rent, utilities, insurance premiums, and minimum loan payments. Variable expenses cover groceries, transportation, dining, and discretionary spending. Whatever remains is what you direct toward faster debt payoff.

The 50/30/20 rule provides a practical starting framework: 50% of take-home pay toward needs, 30% toward wants, 20% toward savings and debt repayment. For anyone in active debt paydown mode, leaning the 20% heavier toward debt (and lighter toward discretionary spending) accelerates the timeline.

One non-negotiable addition: build a small emergency fund of $500–$1,000 before throwing every dollar at debt. Without that buffer, one car repair or medical copay puts you right back on credit cards, undoing weeks of progress. A small cushion prevents one unexpected expense from erasing your progress entirely.

Practical tools that help:

- Budgeting apps like YNAB or Mint to track spending in real time

- Automated minimum payments to eliminate the risk of late fees

- Monthly budget reviews — income and expenses shift, and your plan should shift with them

With a budget in place, you have a clear picture of how much you can realistically put toward debt each month — and a foundation for choosing the right repayment strategy.

Reduce Interest Costs and Avoid Accumulating New Debt

Every dollar saved on interest goes directly toward reducing principal. That's why targeting interest costs is worth pursuing aggressively alongside your repayment strategy.

Debt Consolidation

Debt consolidation combines multiple high-interest debts into a single loan with a lower rate and one monthly payment. The Federal Reserve reported average 24-month personal loan rates at 11.51% in 2025 — meaningfully lower than the 22%+ credit card rates most people are carrying.

A few honest caveats:

- Compare total interest paid across the loan's full term, not just the monthly payment — a lower payment stretched over more years can cost more overall

- Home equity loans offer lower rates but put your home at risk if you default. As the CFPB notes, failure to repay a home equity loan can result in foreclosure

Balance Transfer Credit Cards

The 0% introductory APR balance transfer is a highly effective short-term interest-reduction strategy. Moving a high-rate credit card balance to a card with a 0% promotional period — typically 12 to 21 months — means every payment goes entirely toward principal during that window.

Key details:

- Balance transfer fees typically run 3% to 5% of the transferred amount

- The strategy only works if you pay off the balance before the promotional period ends — after that, standard rates apply

- Have a concrete payoff plan in place before transferring

Negotiating Directly with Creditors

Many consumers don't realize they can contact creditors directly — before an account reaches collections — to request hardship programs, reduced interest rates, or modified payment arrangements. Creditors generally prefer a negotiated resolution to a default. Keep written records of any agreement made; verbal commitments aren't enough.

Stopping the Cycle: Avoiding New Debt

Reducing existing interest costs only works if new debt isn't replacing what you pay down. These habits keep the cycle from restarting:

- Use credit cards only for purchases you can pay in full that month

- Switch to debit or cash for discretionary spending categories

- Resist financing non-essential purchases — if the emergency fund isn't there yet, that purchase can wait

Protect Your Credit Score While Paying Down Debt

Paying down debt and maintaining a healthy credit score aren't competing goals — but they require some coordination.

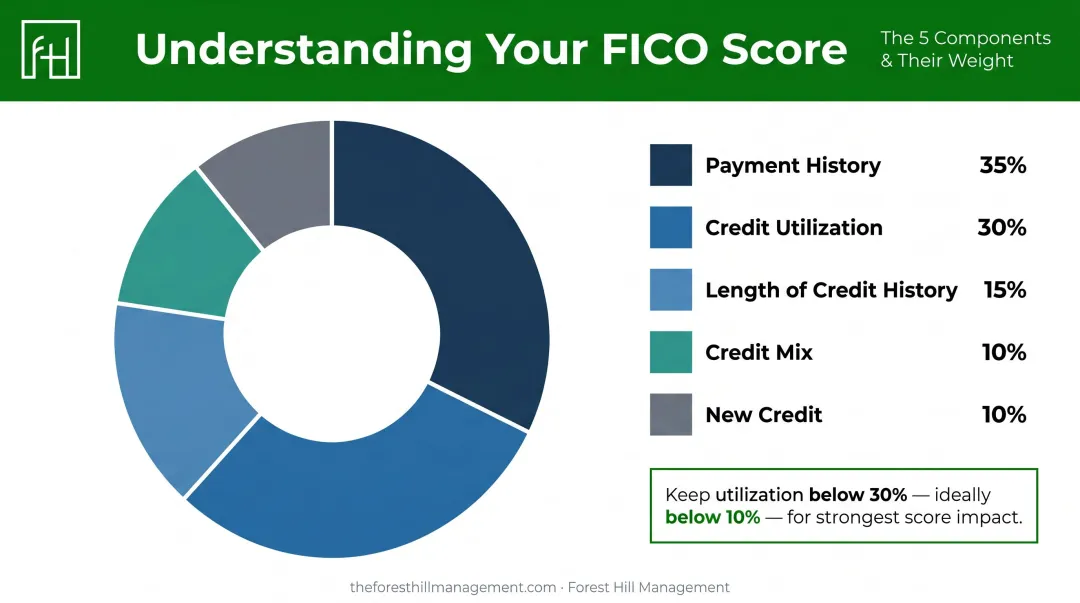

Payment history accounts for 35% of a FICO score, according to myFICO. That makes on-time minimum payments non-negotiable, even on debts that aren't your current payoff priority. A single missed payment can take months to repair — damage that far outweighs the few dollars saved by skipping it.

Credit utilization — the ratio of your credit card balances to your credit limits — is the second major factor (30% of FICO). The guidance: keep utilization below 30%, and ideally below 10% for the strongest score impact. As you pay down card balances, your utilization naturally improves.

Closing paid-off credit cards immediately after eliminating a balance is a common mistake. It reduces your total available credit, which can spike utilization across your remaining cards overnight. Keep paid accounts open unless there's a compelling reason — like an annual fee with no benefit — to close them.

Monitor your credit reports regularly — consumers can access free reports through AnnualCreditReport.com. A 2024 Consumer Reports study found that nearly half of participants discovered errors, and more than a quarter found serious mistakes.

Inaccurate negative information can drag down a score unfairly. Disputing errors costs nothing and takes minutes online.

Here's a quick summary of the key credit-protection habits:

- Pay at least the minimum on every account, every month — no exceptions

- Keep credit card utilization below 30% (below 10% for the best results)

- Leave paid-off accounts open to preserve your available credit

- Check your credit reports annually for errors and dispute any you find

When to Seek Professional Help

Self-managed debt repayment works well for many people — but not every situation. Consider professional help when:

- Balances across multiple creditors feel overwhelming

- Accounts are already past due or in collections

- You're receiving threats of legal action

- You consistently can't make minimum payments, even after budgeting

The earlier you act, the more options you have. Two of the most common professional routes — credit counseling and receivables management — serve different situations.

Nonprofit credit counseling agencies offer a structured path for managing active, high-interest debt. Through a Debt Management Plan (DMP), a certified counselor reviews your finances, negotiates with creditors for reduced or waived interest charges, and creates a single consolidated monthly payment. DMPs typically run up to five years and require closing enrolled credit accounts during the plan — a real tradeoff, but often worth it for someone buried in revolving debt.

Before engaging any agency, verify accreditation and confirm transparent fee disclosures. The FTC recommends checking with your state attorney general's office for complaints.

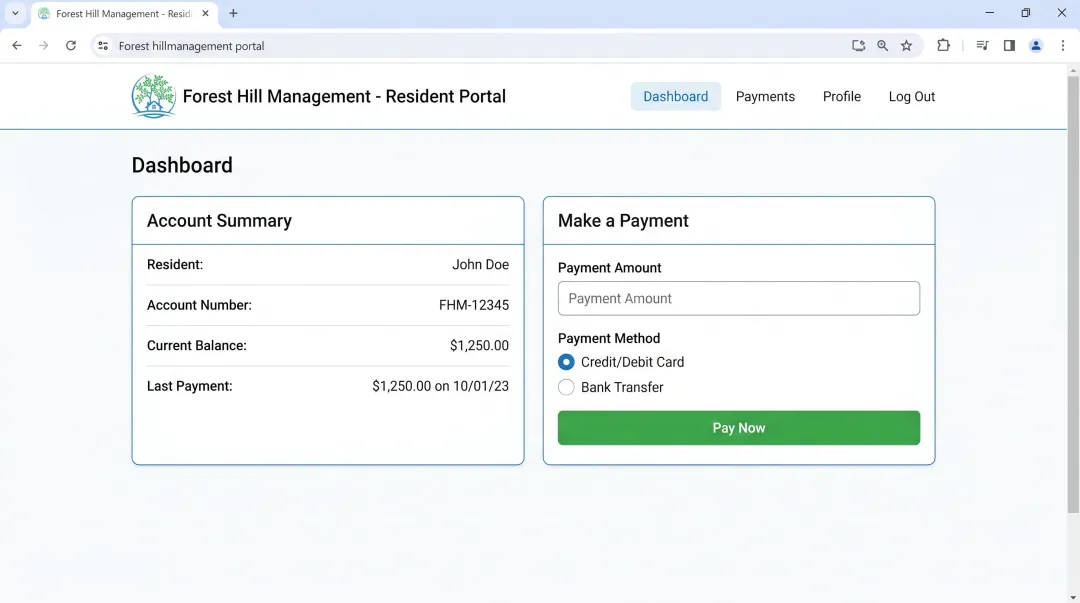

For accounts already past due or in collections, Forest Hill Management works directly with consumers to understand their circumstances, set up flexible payment arrangements, and create a clear path to resolving outstanding balances. You can reach their team at (888) 471-0109 or info@foresthillmanagement.com. Their online payment portal at pay.theforesthillmanagement.com lets you review your account and make payments directly.

Frequently Asked Questions

How do I manage debt effectively?

Start by auditing every debt you carry — balances, interest rates, and minimums. Choose a structured repayment method (snowball or avalanche), build a budget that frees up extra cash, reduce interest costs where possible, and make on-time minimum payments consistently throughout.

What are the 5 C's of debt?

The 5 C's of credit — Character, Capacity, Capital, Collateral, and Conditions — are the framework lenders use to evaluate creditworthiness. They assess your credit history, income-to-debt ratio, assets, loan security, and broader economic factors like interest rates.

What is the difference between the debt snowball and debt avalanche method?

The snowball targets the smallest balance first to generate motivational wins through quick account closures. The avalanche targets the highest-interest debt first, minimizing total interest paid over time. Choose snowball if you need early momentum — choose avalanche if cutting total interest cost is the priority.

Is it better to pay off debt or save money?

Build a small emergency fund ($500–$1,000) first, then prioritize high-interest debt. Keep contributing to any employer-matched retirement account — that match is an immediate 50–100% return. Once high-interest debt is cleared, redirect that cash toward long-term savings.

What is a good debt-to-income ratio?

A DTI below 35% is generally considered manageable by most lenders. Above 50% signals significant financial strain and can limit access to new credit or favorable loan terms.

How does debt affect your credit score?

High balances relative to credit limits, missed payments, and accounts sent to collections all damage a credit score. Consistent on-time payments and steadily lowering your credit utilization are the most reliable ways to improve your score over time.