Forest Hill Financial Guidance for Wealth Management

Transform Your Financial Future

Contact UsIntroduction

Most people assume wealth management is reserved for those who already have money — the investors, the high earners, the people who've never missed a payment. That assumption stops a lot of people from taking any financial steps at all.

The reality is different. Wealth management starts where you actually are — including if you're managing past-due accounts, working through debt, or rebuilding after financial setbacks.

According to the FINRA Foundation's 2025 National Financial Capability Study, 57% of U.S. adults had not tried to calculate how much they need to save for retirement, and only 46% had a rainy-day fund covering three months of expenses.

Those numbers point to a guidance problem, not a wealth problem.

This guide breaks down what financial health actually looks like for everyday consumers — where to start, what to prioritize, and how resolving past-due obligations fits into a longer-term strategy.

Key Takeaways

- Wealth management starts with resolving what's holding you back, regardless of your current financial position

- Payment history makes up 35% of your FICO Score, making past-due account resolution a financial priority

- A structured budget is your single most powerful tool for regaining financial control

- Forest Hill Management provides expert support and flexible payment options for resolving past-due accounts

- Rebuilding financial health takes consistent action over several months, and steady progress compounds quickly

What Is Wealth Management and Why Does It Matter?

What Wealth Management Actually Covers

Most people hear "wealth management" and picture brokerage accounts and retirement portfolios. That's part of it. The full picture also includes:

- Budgeting and cash flow management

- Debt resolution and account stabilization

- Long-term financial planning

- Protecting what you've already built

The CFP Board defines financial planning as a process that "helps maximize a client's potential for meeting life goals through financial advice that integrates relevant elements of the client's personal and financial circumstances." That applies whether you have $500 in savings or $500,000.

Wealth management is relevant at every income level and every financial stage. The goal isn't a specific dollar amount — it's control, stability, and forward momentum.

The Cost of Doing Nothing

Inaction has a price tag. The Federal Reserve reports that in 2025, 28% of adults struggled to pay their bills — either unable to pay in full or doing so with difficulty. Meanwhile, credit card interest rates averaged 21.22% in 2025. Let that compound for a year on an unpaid balance, and you'll feel it.

The CFPB found that consumers paid over $14 billion in credit card late fees in 2019 alone, with penalty fees representing a 24% annualized surcharge on top of already-high interest rates. Every dollar lost to fees and penalties is a dollar that can't go toward getting ahead.

Stability Before Accumulation

Those numbers point to something important: for many consumers, wealth management doesn't start with investment accounts. It starts with stopping the financial bleeding — resolving past-due accounts, getting current on obligations, and creating a stable foundation.

Accumulation follows stability. Until the foundation is solid, other financial moves are harder to sustain.

Understanding Your Financial Situation: The First Step to Wealth

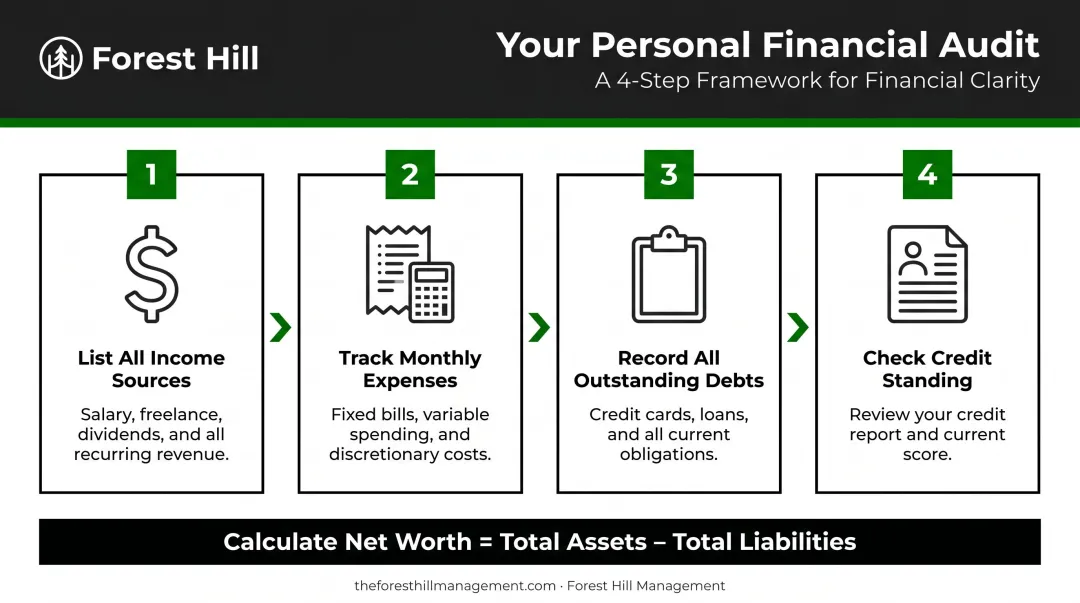

Running Your Personal Financial Audit

You cannot manage what you haven't measured. Before any strategy or plan makes sense, you need a clear picture of where you actually stand.

Start by documenting four things:

- List all income sources — every paycheck, side income, or benefit, after tax

- Track monthly expenses — fixed (rent, utilities, loan payments) and variable (groceries, transport, subscriptions)

- Record every outstanding debt — account name, current balance, and interest rate

- Check your credit standing — pull a free report at AnnualCreditReport.com

Once you have these numbers, calculate your net worth: total assets minus total liabilities. If you have $2,000 in savings and $8,000 in past-due accounts, your net worth is -$6,000. That's not a judgment — it's a starting point.

Identifying Problem Areas

Common financial pitfalls that block wealth building:

- Past-due accounts sitting in collections or accruing penalties

- Minimum payments that barely cover interest, trapping you in a debt cycle

- No emergency savings, turning every unexpected expense into new debt

- Paying debts randomly rather than following a structured repayment strategy

The numbers on delinquency are significant. The Urban Institute reports that 23% of Americans had debt in collections, with a median balance of $2,528. The New York Fed reported that in Q1 2025, 5.0% of consumers had a third-party collection account on their credit report.

The emotional weight compounds the problem. Research published in the Journal of Family and Economic Issues found that financial worry — not just objective debt levels — directly correlates with psychological distress. Many people avoid confronting their finances out of shame or overwhelm, which only deepens the hole.

Treating the audit as information, not judgment, is what breaks that cycle.

Setting a Baseline Financial Goal

Don't try to fix everything at once. Pick one achievable action:

- Resolve one past-due account

- Create your first monthly budget

- Contact a receivables management organization to discuss options

Small wins are not small. They break the cycle of avoidance and prove that forward movement is possible. One resolved account, one budget created — that's how recoveries actually begin.

Key Pillars of Financial Guidance for Wealth Management

Effective financial guidance rests on four interconnected pillars. Each one reinforces the others — and addressing them in sequence produces the most durable results.

Debt Resolution and Receivables Management

Resolving past-due accounts is one of the most overlooked pillars of wealth management. Outstanding obligations create ongoing financial drag — through penalties, interest, and credit score damage — that actively prevents wealth building.

Payment history makes up 35% of a FICO Score, making it the single largest scoring factor. Past-due accounts can remain on your credit report for up to seven years, though their impact diminishes as they age and as you establish consistent positive payment history.

Working with a receivables management organization changes the dynamic. Rather than navigating collections alone — without negotiating experience or knowledge of industry norms — consumers can access structured repayment plans, flexible terms, and expert guidance.

Forest Hill Management, for example, specializes in helping consumers resolve past-due accounts through customized payment plans. Their approach is collaborative: the goal is to "work together with you to identify the optimal solution to address and resolve your financial matter effectively." Consumers can explore options through their online portal or speak with a financial advisor directly at (888) 471-0109.

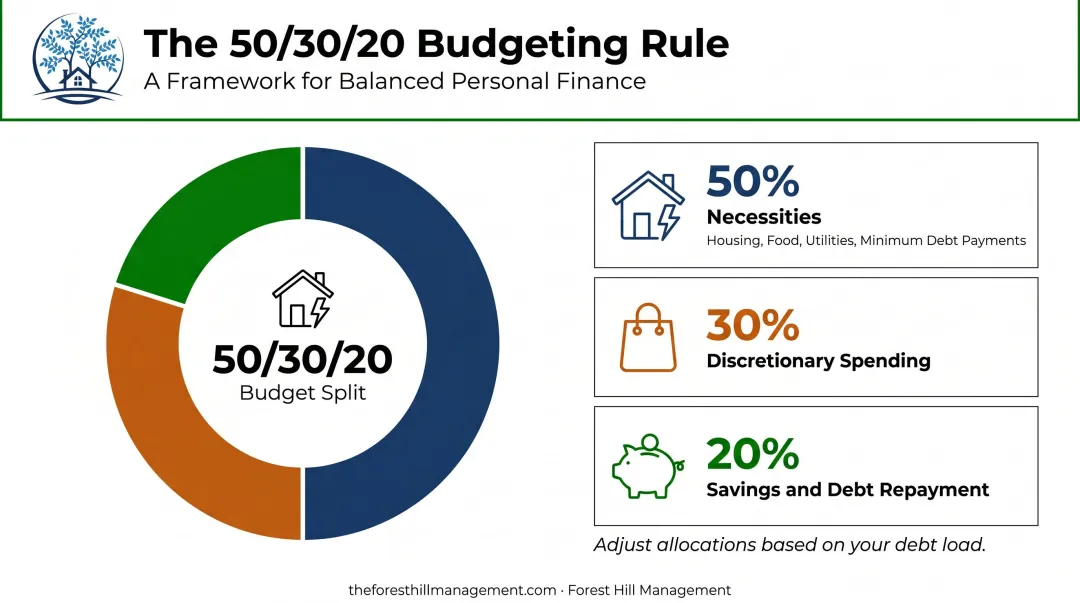

Budgeting and Cash Flow Management

A monthly budget is the backbone of financial control. Without one, money disappears without purpose.

The 50/30/20 rule is a practical starting framework:

- 50% of after-tax income toward necessities (housing, food, utilities, minimum debt payments)

- 30% toward discretionary spending

- 20% toward savings and additional debt repayment

Adjust the percentages based on your situation — if you're carrying significant debt, you may shift more toward the 20% bucket temporarily. What matters most is building the habit of tracking and allocating with intention, not which framework you start with.

Portfolio and Savings Planning

Once obligations are stabilized, the next pillar is building. Even small, consistent contributions compound meaningfully over time.

The CFPB found that consumers with at least one month of income saved had an average financial well-being score of 61, compared to 40 for those with no emergency savings. Having any buffer at all — even a modest one — shifts both the financial reality and the sense of control that comes with it.

Fidelity's research on compounding illustrates the timing effect clearly: starting $6,000 in annual contributions at age 25 versus 35, at a 7% annual return, produces dramatically different outcomes over decades. The earlier you begin, the less total contribution you need to reach the same endpoint.

Once emergency savings are established, consistent contributions to a retirement account — even small ones — capture years of compounding growth that no future contribution increase can fully replace.

Ongoing Financial Education and Accountability

Wealth management isn't a one-time decision. Income shifts, expenses arise, and goals evolve — which means your plan needs to evolve too. A trusted guidance partner provides the education, check-ins, and plan adjustments that keep your finances moving forward.

Forest Hill Management supports this through an extensive library of financial education resources, freely accessible on their website. Topics covered include:

- Debt repayment strategies and account resolution options

- Budgeting techniques for different income situations

- Understanding credit reports and consumer rights under the FDCPA

- How to communicate effectively with creditors and collection agencies

How to Resolve Past-Due Accounts and Rebuild Your Financial Health

Step 1: Acknowledge and Inventory Your Obligations

List every past-due account with:

- Creditor name (original and current)

- Amount owed

- Days past due

- Any written communications received

A complete inventory prevents surprise escalations — new collection contacts, legal notices, or credit report changes that catch you off guard. Knowing what you owe and to whom puts you in control of the conversation.

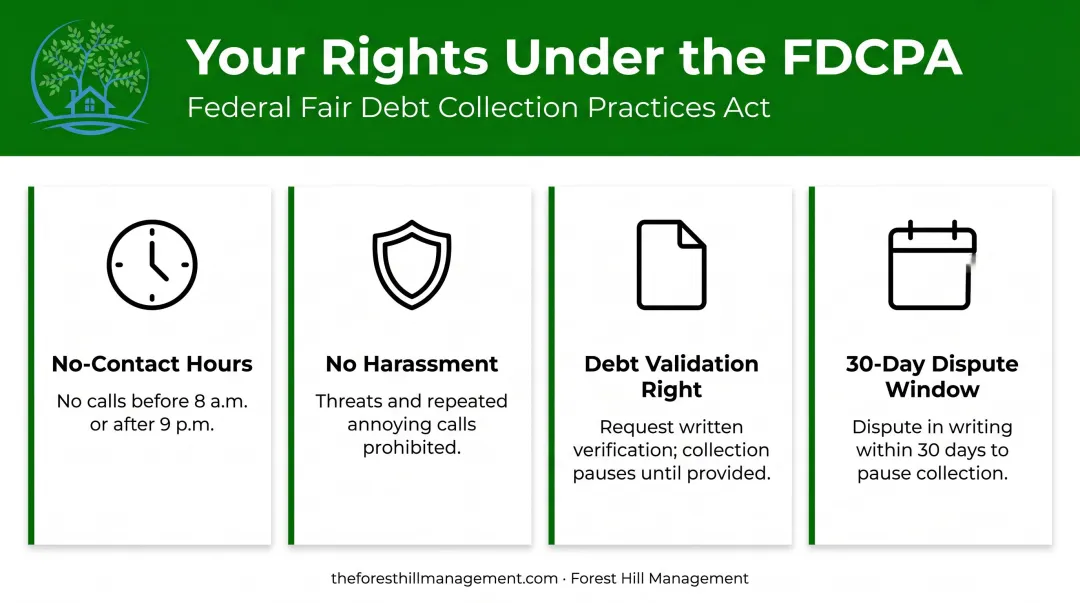

Step 2: Understand Your Rights as a Consumer

The Fair Debt Collection Practices Act (FDCPA), enacted in 1977, establishes clear protections for consumers dealing with debt collectors. Key rights include:

- Collectors cannot contact you before 8 a.m. or after 9 p.m.

- Harassment, threats, and repeated calls intended to annoy are prohibited

- You can request written debt validation — and the collector must stop collection activities until they provide verification

- If you dispute the debt in writing within 30 days, collection must pause until the debt is verified

The CFPB's Debt Collection Rule (Regulation F), effective November 2021, further clarifies communication standards. Knowing these protections means you can engage from an informed position rather than a reactive one.

Step 3: Work With a Financial Guidance Organization

Negotiating past-due accounts independently — without knowledge of industry norms, typical settlement terms, or legal frameworks — puts consumers at a disadvantage. Professional support changes that dynamic.

Forest Hill Management works directly with consumers to manage and resolve transferred receivables. Services include:

- Flexible, customized payment plans tailored to individual financial circumstances

- Expert negotiation and account management support

- Secure online portal access at pay.theforesthillmanagement.com for self-directed repayment

- Written settlement confirmation once an account is fully resolved

To explore your options, call (888) 471-0109 or log into your account at pay.theforesthillmanagement.com.

Step 4: Build Back Your Financial Foundation

Once your account is resolved, the next priority is making sure that resolution works in your favor. The rebuilding steps are straightforward:

- Monitor your credit reports — check that resolved accounts are accurately reflected

- Establish consistent payment habits — on-time payments are the fastest way to demonstrate creditworthiness under any scoring model

- Build a savings buffer — even $500 to $1,000 changes your ability to handle unexpected expenses without creating new debt

- Set short-term financial milestones — 90-day goals are more motivating than 5-year plans

According to FICO, late payments are evaluated by recency, severity, and frequency. A 90-day late payment is treated more harshly than a 30-day one, but both diminish in influence as time passes and positive payment history accumulates. Credit scores are not permanent — they respond to current behavior.

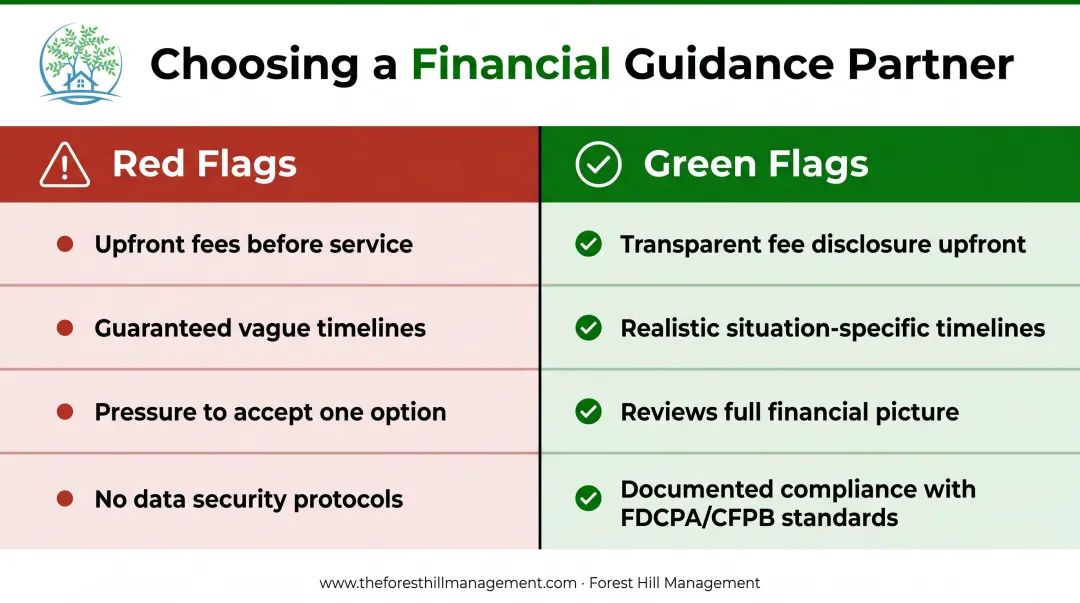

How to Choose the Right Financial Guidance Partner

Not all financial guidance organizations operate the same way. The wrong choice can deepen financial problems rather than resolve them.

What to Look For

- Know exactly what you're agreeing to before any services begin — fee structures and processes should be documented upfront

- Verify that the organization references and adheres to FDCPA and CFPB standards

- Expect a plan built around your specific situation, not a generic template applied to everyone

- Confirm how often you'll receive updates, what support channels are available, and whether milestones are documented

The NFCC recommends verifying national affiliation, independent accreditation, counselor certification, and checking for unresolved complaints with your state's Attorney General or Better Business Bureau.

Red Flags to Watch For

With those verification steps in mind, watch for warning signs that signal a poor fit:

- Upfront fees demanded before any service is rendered — the FTC's Telemarketing Sales Rule prohibits for-profit debt relief companies from charging fees before settling or reducing a consumer's debt

- Guaranteed or vague timelines — real resolution depends on your specific situation, not a blanket promise

- Pressure to accept one option without reviewing your full financial picture

- No documented data security protocols

What a Strong Partnership Looks Like

A strong working relationship means regular communication, documented milestones, and a team that engages with your actual financial picture. Forest Hill Management structures its service around this: account managers reachable by phone, a secure online portal for self-directed account access, and compliance practices built around FDCPA and CFPB standards — so you know exactly where your account stands at every stage.

Frequently Asked Questions

What services does Forest Hill Management offer?

Forest Hill Management is a receivables management organization offering past-due account resolution, flexible payment plans, portfolio management, and debt verification services. A secure online payment portal makes it straightforward for consumers to manage and resolve outstanding obligations.

Is Forest Hill Management independently owned?

Forest Hill Management is a dedicated receivables management organization focused on direct, personalized client relationships. For specific details about its ownership structure, contact the team at (888) 471-0109 or info@foresthillmanagement.com.

What is the average fee for a financial advisor?

According to NerdWallet's 2026 data, financial advisors typically charge 0.25% to 2% of assets under management annually (median around 1%), $200 to $400 per hour, or $2,500 to $9,200 annually on retainer. Fees vary significantly by service type, scope, and provider — always ask for transparent fee disclosure before engaging any advisor.

How can I start managing my finances if I have past-due accounts?

Start by auditing all outstanding obligations — creditor, balance, and days past due — then contact a reputable receivables management organization to discuss resolution options. Resolving past-due accounts is the first step toward wealth management, not a barrier to it. Forest Hill Management can be reached at (888) 471-0109 to explore your options.

What is receivables management and how does it help consumers?

Receivables management involves the professional handling and resolution of past-due accounts — helping consumers settle obligations through structured, often more affordable arrangements than navigating collections independently. It reduces ongoing financial penalties, clears credit report drag, and creates a foundation for rebuilding financial health.

How long does it take to rebuild financial health after resolving debt?

Timelines vary by individual circumstances, but with consistent on-time payments, active budgeting, and professional guidance, many consumers see meaningful credit score and financial stability improvements within one to two years of beginning a structured resolution plan. FICO factors in recency and consistency — current behavior matters more than past history as time passes.