Forest Hills Settlement and Lawsuit Updates

Transform Your Financial Future

Contact UsIntroduction

If you searched "Forest Hills settlement" or "Forest Hills lawsuit" and ended up more confused than when you started, you're not alone.

Those searches pull up at least two completely unrelated stories — one about a Queens, New York homeowners' group and a stadium dispute, the other about a Florida debt collection case involving a company called "Forest Hill Account Management." Neither is straightforward to decode at first glance.

That confusion has real consequences if you've recently received a collection notice from Forest Hill Management. Stumbling onto lawsuit news tied to a similar name can be unsettling — and acting on the wrong information could lead to poor financial decisions.

Here's a clear breakdown of both stories, what the Florida case actually alleged, and what it means for your situation.

Key Takeaways

- The Queens "Forest Hills" lawsuit involved a homeowners' group and stadium policing — it has nothing to do with debt collection.

- A separate Florida case (Taylor v. Chebat) named "Forest Hill Account Management" over alleged FDCPA and FCRA violations tied to a payday loan.

- Forest Hill Management operates as a receivables management company under federal consumer protection law, including the FDCPA.

- You have the legal right to request written debt verification before making any payment — always do this first.

- Settling an account directly with Forest Hill Management through written communication creates a clear, documented record of resolution.

Clearing Up the Confusion: Two Very Different "Forest Hills" Stories

The Queens Stadium Case — Not a Debt Collector

The first result you'll often find when searching "Forest Hills settlement" is a 2026 news story about the Forest Hills Gardens Corporation, a civic and homeowners' organization in Queens, New York. That group sued New York City over how the NYPD handled street closures and crowd control around Forest Hills Stadium during concerts. According to the Queens Daily Eagle and the Queens Chronicle, the case — filed as Forest Hills Gardens Corporation v. The City of New York (Case No. 1:25-cv-05741) — settled for a reported $150,000 in March 2026.

This case involves real estate, policing, and municipal law. It has no connection to debt collection, consumer credit, or any company named Forest Hill Management.

The Florida Lawsuit — More Relevant, but Still Distinct

The second story is the one that matters if you've heard from Forest Hill Management. In March 2026, a Florida consumer named Antquan Taylor filed suit in the Middle District of Florida (Taylor v. Chebat et al, Case No. 8:26-cv-00734), naming "Forest Hill Account Management, Inc." as a defendant alongside another debt portfolio company.

As reported by BadCredit.org, the case involved a $700 payday loan from Plain Green that allegedly carried a 580% APR, with alleged violations of both the Fair Debt Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA).

That's the lawsuit consumers researching Forest Hill Management are actually finding. The two names — "Forest Hill Account Management, Inc." and "Forest Hill Management" — are similar, and their exact corporate relationship has not been publicly confirmed in available records.

Forest Hill Management's own website acknowledges the "Forest Hill Account Management Inc." name in consumer-facing content, and its SMS opt-in consent form references that name directly. This suggests a close relationship, but the precise legal structure isn't publicly documented.

If you received a notice from Forest Hill Management, here's what to take away:

- The Queens stadium case has no bearing on your situation — it's an unrelated municipal dispute

- The Florida lawsuit is worth understanding for context, but its outcome hasn't been publicly confirmed and doesn't determine whether any specific debt you owe is valid

What the Florida Lawsuit Actually Alleged

The Core of the Taylor v. Chebat Case

According to BadCredit.org's reporting, Antquan Taylor alleged he took out a $700 loan from Plain Green — a tribal lending entity — that carried a 580% APR. Florida law caps civil interest rates at 18% per annum under Florida Statute 687.03, and treats rates above 25% per annum as criminally usurious under Florida Statute 687.071. Taylor's lawsuit alleged the loan was void under Florida usury law, and that collecting on that void debt violated federal consumer protection law.

Forest Hill Account Management, Inc. was named because the charged-off balance was allegedly placed with it for collection. The FDCPA and FCRA claims weren't necessarily about the original loan terms — they were about what happened during the collection process.

What the FDCPA and FCRA Actually Protect

Both federal laws give consumers specific, enforceable rights during the collection process:

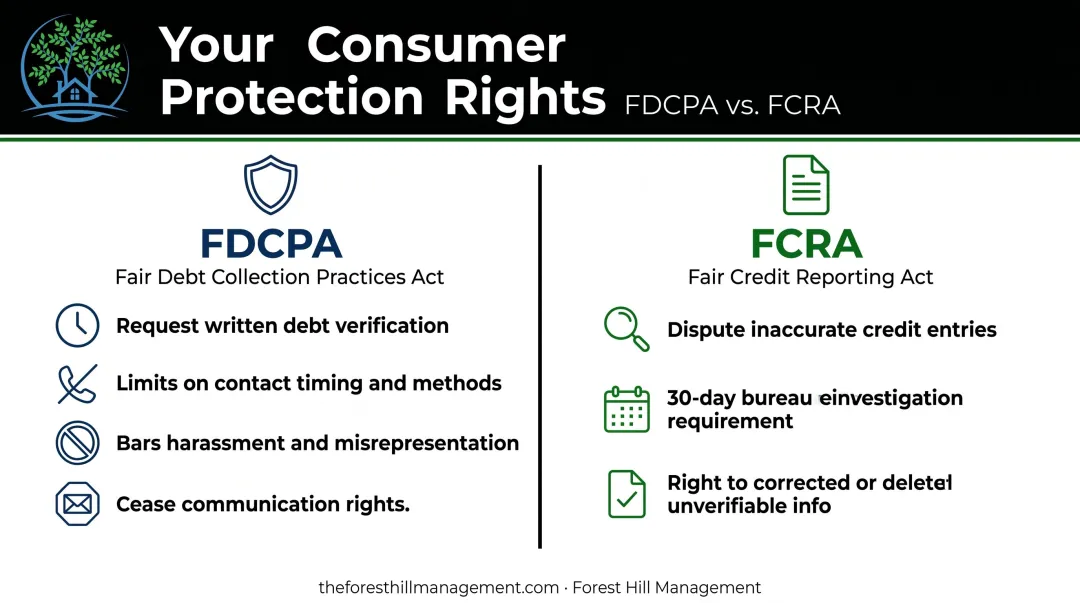

- FDCPA (15 U.S.C. § 1692 et seq.): Prohibits unfair, deceptive, or abusive collection practices. Gives consumers the right to request written verification of a debt, limits when and how collectors can contact you, and bars harassment, misrepresentation, and false statements.

- FCRA (15 U.S.C. § 1681 et seq.): Governs how debt information is reported on your credit file. Gives you the right to dispute inaccurate entries, which credit bureaus must investigate within 30 days.

Why Cases Like This Matter

High-profile FDCPA lawsuits have a real effect on consumer protections across the industry. The CFPB's 2025 FDCPA Annual Report reported that consumers filed approximately 207,800 debt collection complaints in 2024 — with the most common issues being attempts to collect debts not owed, insufficient verification, and continued contact after stop requests. Those numbers reflect why cases that test the boundaries of tribal lending and third-party collection have drawn sustained attention from regulators and consumer advocates alike.

It's worth noting that the outcome of Taylor v. Chebat has not been publicly confirmed. No final judgment or settlement has been verified in available sources, so the case details are best treated as context rather than confirmed precedent — and should not be read as reflecting current practices at Forest Hill Management.

Is Forest Hill Management a Legitimate Debt Collector?

Yes. Forest Hill Management (theforesthillmanagement.com) is a receivables management company operating under FDCPA regulations.

Its communications include the required "mini-Miranda" disclosure — "This is an attempt to collect a debt. Any information obtained will be used for that purpose" — a legally mandated indicator that the company is operating as a covered debt collector under federal law.

How to Verify a Debt Collector's Legitimacy

When you receive any collection notice, check for these indicators:

- Mini-Miranda language in the written communication (required by 15 U.S.C. § 1692e(11))

- Original creditor identification — Forest Hill Management's correspondence identifies the original creditor for the account

- Verifiable contact information — phone (888) 471-0109, email info@foresthillmanagement.com, website theforesthillmanagement.com

- Governing law disclosure — Forest Hill Management operates under New York State law per its Terms & Conditions

How Debt Collection Actually Works

Forest Hill Management operates under both a servicing model (managing accounts on behalf of original creditors) and a debt buyer model (purchasing charged-off portfolios outright). The CFPB describes this in its debt collection guidance: debt buyers purchase delinquent accounts at a fraction of the debt's face value and then collect on their own behalf.

Receiving a notice does not mean you must pay immediately. Verifying the debt first — in writing — is the recommended first step before any payment or negotiation.

Your Rights Under the FDCPA and FCRA

Debt Validation: Your Right to Verify

Under 15 U.S.C. § 1692g, you have the right to send a written debt validation request within 30 days of receiving a collector's first written communication. Once you send that request, the collector must pause collection activity until they provide written verification of:

- The amount owed

- The name of the original creditor

- Your right to dispute the debt

How to exercise this right:

- Send the request via certified mail with return receipt

- Keep copies of everything

- Do not share personal financial details in your initial communication

- Do not make any payment until validation is complete

Prohibited Collector Behaviors Under the FDCPA

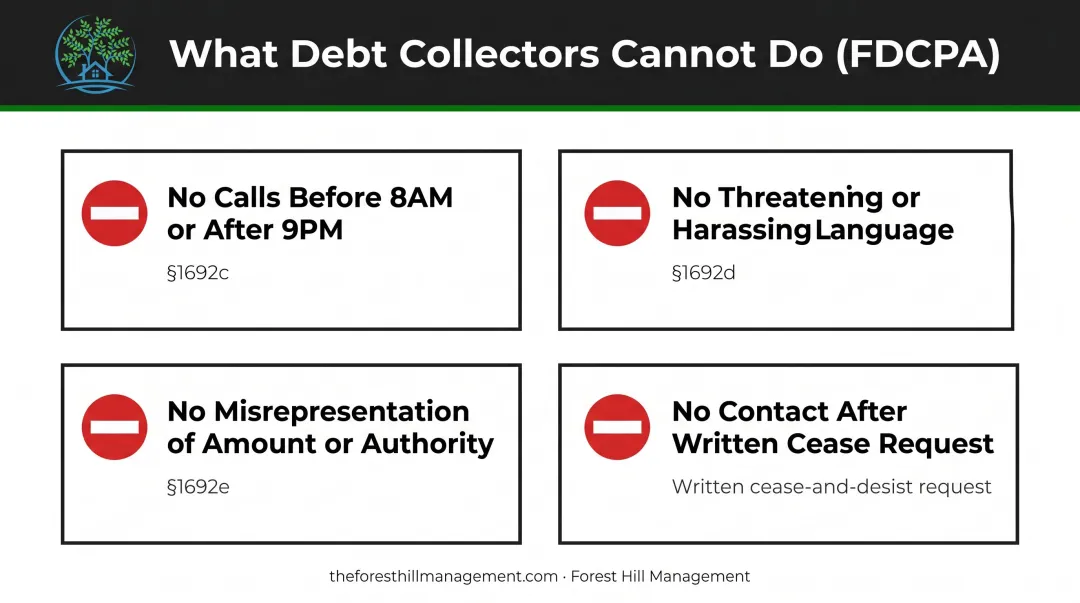

Debt collectors cannot legally:

- Call before 8 a.m. or after 9 p.m. local time (15 U.S.C. § 1692c)

- Use threatening or harassing language (15 U.S.C. § 1692d)

- Misrepresent the amount owed or their legal authority (15 U.S.C. § 1692e)

- Continue contact after a written cease communication request

If a collector violates these rules, you can file a complaint with the CFPB, the FTC, or your state attorney general's office. Under 15 U.S.C. § 1692k, successful individual actions can recover actual damages plus up to $1,000 in statutory damages and attorney's fees.

Credit Reporting Rights Under the FCRA

The FDCPA governs collector conduct, but a separate law covers what gets reported to the credit bureaus. If Forest Hill Management has reported an account, check your free credit reports at AnnualCreditReport.com to check for any reported accounts. Under 15 U.S.C. § 1681i, credit bureaus must reinvestigate disputed information within 30 days and correct or delete anything that can't be verified.

Dispute inaccuracies in writing directly with the credit bureau reporting the error, not solely with the collector. Both steps may be necessary to fully resolve the issue.

How to Resolve Your Account with Forest Hill Management

Start Before You Call

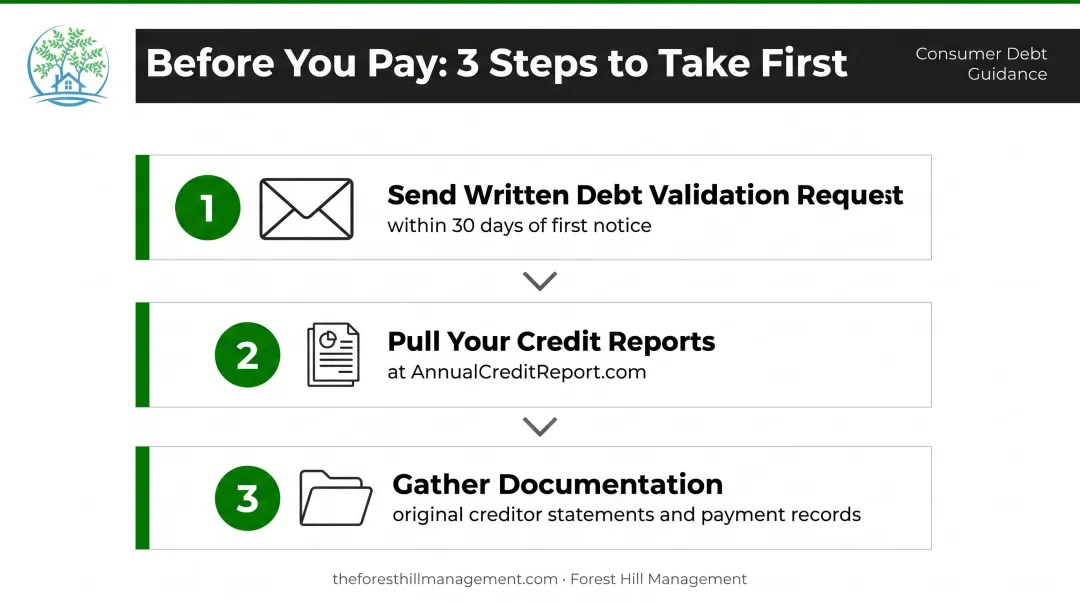

Before making any payment or entering any agreement, take these steps:

- Send a written debt validation request within 30 days of your first notice

- Pull your credit reports at AnnualCreditReport.com to see how the account is reported

- Gather documentation — any original creditor statements or prior payment records you have

Resolution Options

You have three ways to contact Forest Hill Management and explore your options:

- Visit pay.theforesthillmanagement.com to review your account and explore payment options at any time

- Call (888) 471-0109 to speak with a representative about a repayment arrangement

- Email info@foresthillmanagement.com to submit inquiries or request account documentation

Once you've identified a path forward, protect yourself before committing to anything.

Before You Pay Anything

Whatever arrangement you reach, get it in writing first. The written agreement should confirm:

- The total amount to be paid

- The payment schedule (if installments)

- Confirmation that it satisfies the account

Keep copies of all documentation. Once the account is resolved, Forest Hill Management will provide written confirmation of the settlement upon request. Include your name and account number when you reach out.

Frequently Asked Questions

Is Forest Hill Management a legitimate debt collector?

Yes. Forest Hill Management is a receivables management company operating under FDCPA regulations since 2020. Their notices include the required mini-Miranda disclosure, and consumers can verify the company's identity through its website (theforesthillmanagement.com), confirmed contact information, and New York State governing law disclosed in its Terms & Conditions.

What should I do if I receive a notice from Forest Hill Management?

Send a written debt validation request within 30 days via certified mail — this pauses collection activity while the debt is verified. Separately, pull your credit reports at AnnualCreditReport.com to confirm what's being reported, and avoid making any payment until you receive written verification of the debt.

Can Forest Hill Management sue me over an unpaid debt?

Collectors can pursue legal action to recover valid debts, but whether that happens depends on factors like the balance, account age, and your state's statute of limitations. The CFPB notes that most states have limitations periods of three to six years. Responding to notices and requesting validation early gives you the most options before any legal action is initiated.

How can I dispute a debt that Forest Hill Management is collecting?

If you believe the debt is inaccurate or not yours, send a written dispute within 30 days under the FDCPA (15 U.S.C. § 1692g) — this requires the collector to stop collection until the debt is verified. For errors already appearing on your credit report, file a separate written dispute directly with the relevant credit bureau under the FCRA.

Will settling with Forest Hill Management hurt my credit score?

A settled account is reported as "settled for less than full balance," which is less favorable than "paid in full" — per Experian, the latter carries more weight with lenders. When negotiating, ask whether paying the full balance is an option to get the stronger designation on your report.

How do I contact Forest Hill Management to resolve my account?

Call (888) 471-0109, email info@foresthillmanagement.com, or log in to the secure payment portal at pay.theforesthillmanagement.com to review your account and discuss resolution options directly with an advisor.