Forest Management and Ecology Collection

Transform Your Financial Future

Contact UsYou open your mail and find a notice from a company called Forest Hill Management. Or maybe you missed a call and found a voicemail asking you to get in touch about a past-due account. Either way, the first reaction for most people is the same: confusion, followed by a spike of anxiety. Who are these people? Is this legitimate? What happens if I ignore it?

Those are fair questions, and you deserve clear answers. This post covers exactly who Forest Hill Management is, what rights federal law gives you when any debt collector contacts you, and the practical steps you can take to resolve your account without unnecessary stress.

Key Takeaways

- Forest Hill Management is a legitimate third-party receivables management organization, not a scam

- Federal law gives you 30 days to dispute a debt in writing after first contact

- Debt collectors cannot call before 8 a.m. or after 9 p.m. your local time

- Delinquent accounts can stay on your credit report for up to 7 years per CFPB guidelines

- Responding to a notice — by paying, disputing, or negotiating a plan — consistently leads to better outcomes than ignoring it

Who Is Forest Hill Management?

Forest Hill Management is a receivables management organization based in the United States, operating since 2020. The company specializes in managing past-due accounts that original creditors assign to them for resolution. Since founding, they've helped thousands of consumers work through outstanding financial obligations.

First-Party vs. Third-Party: What the Distinction Means for You

Forest Hill Management is a third-party receivables management organization — meaning they're not the original lender or creditor. What that means for you:

- Your original creditor (a bank, lender, or service provider) was unable to collect payment on your account

- That creditor assigned the account to Forest Hill Management to manage the resolution process

- Forest Hill Management is now authorized to contact you on the original creditor's behalf

- Every communication from Forest Hill Management will include an "Original Creditor" section identifying who you originally borrowed from

This is why many consumers don't recognize the name at first. You didn't borrow from Forest Hill Management — but they're now the point of contact for resolving that account.

Is Forest Hill Management Legitimate?

Forest Hill Management operates under documented contact infrastructure, formal legal policies governed by New York state law, and a structured consumer dispute process. Their website at theforesthillmanagement.com includes a payment portal, FAQ section, and educational resources about your rights.

Their homepage carries the standard FDCPA disclosure: "This communication is from a debt collector. This is an attempt to collect a debt and any information obtained will be used for that purpose." That's a required disclosure, and its presence confirms the company is operating within regulatory guidelines.

If you want independent confirmation, request written debt validation (explained in the next section). It's a reliable first step any time an unfamiliar collector contacts you.

Your Rights Under the FDCPA When Contacted by a Debt Collector

The Fair Debt Collection Practices Act (FDCPA) is the federal law that governs how third-party debt collectors — including Forest Hill Management — may communicate with you. Knowing what it requires gives you a clear framework for responding — and for pushing back if a collector crosses a line.

The 30-Day Validation Window

Under 15 U.S.C. § 1692g, a debt collector must send you a written validation notice within 5 days of first contact. That notice must include:

- The amount of the debt

- The name of the original creditor

- A statement that you have 30 days to dispute the debt in writing

- Notice that the collector will provide verification if you dispute within that window

If you send a written dispute within those 30 days, the collector must stop collection activity until they mail you verification of the debt. Don't dispute verbally — put it in writing and keep a copy.

Communication Rules Collectors Must Follow

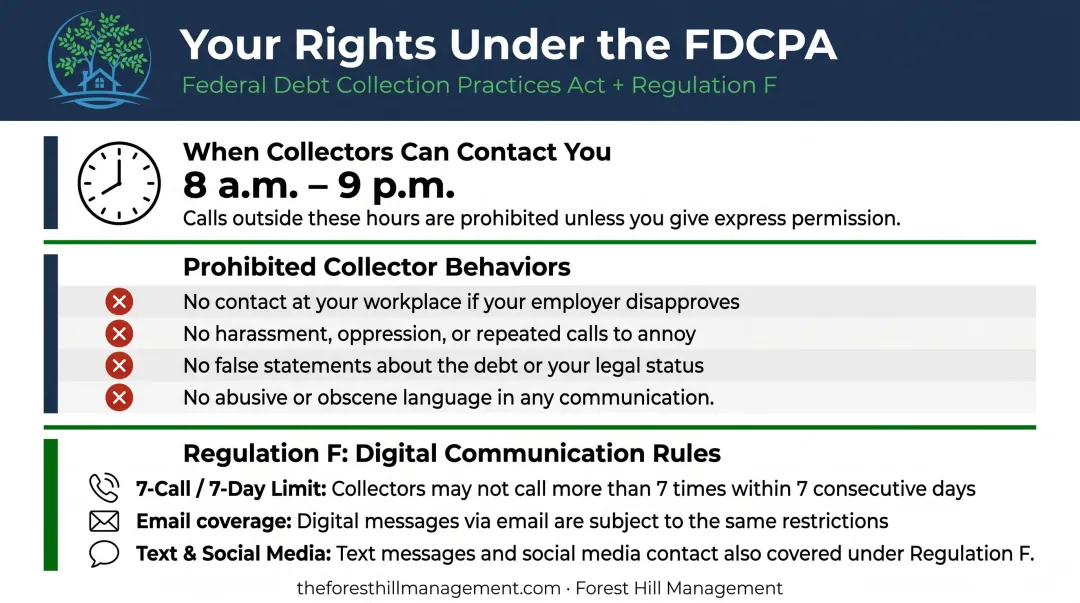

The FDCPA sets clear boundaries on how and when collectors can reach you. Under 15 U.S.C. § 1692c and FTC guidance:

- No calls before 8 a.m. or after 9 p.m. local time

- No workplace contact once you've told them your employer prohibits it

- No harassment, threats, or abusive language of any kind

- No false or misleading statements about the debt or its legal status

Regulation F, which took effect November 30, 2021, extended these rules to email, text, and social media — including a framework limiting collectors to roughly 7 calls per 7 consecutive days about a specific debt.

Your Right to Stop Contact

If the communication rules above aren't enough, you can go further. Send a written "cease communication" letter at any time, and the collector must stop — with only three narrow exceptions:

- To confirm they are stopping collection efforts

- To notify you that they may invoke a specific legal remedy

- To inform you that a specific remedy will be invoked

Sending a cease letter doesn't eliminate the debt. It only limits how the collector can contact you going forward.

Statute of Limitations on Lawsuits

Each state sets a separate window during which a collector can sue to collect — independent of how long the debt stays on your credit report. According to the CFPB, most states set this at 3 to 6 years, though some run longer. This is a different clock from the FCRA's 7-year credit reporting window — the two don't reset each other.

If you're uncertain about your state's specific period, check with a financial professional or consumer law resource before making any decisions about an older debt.

What to Expect When Forest Hill Management Contacts You

Here's how contact typically unfolds — and what you should do at each stage.

The First Contact

Forest Hill Management reaches out by letter, email, phone, or SMS. Written communications will include:

- The outstanding balance

- The original creditor's name

- Your account or reference number

- A statement of your right to dispute

If the initial contact is by phone and the validation information wasn't included in that call, they're required to send you a written notice within 5 days.

What to Do Before You Respond

Before calling back or making any payment:

- Gather original account documents — statements, agreements, or correspondence from the original creditor

- Confirm the creditor name matches what's listed in Forest Hill Management's notice

- Keep a running log — write down dates, times, and representative names for every call or correspondence

Disputing vs. Resolving

Once those steps are done, you'll have a clear picture of where you stand — and two distinct paths forward:

If you believe the debt is incorrect or not yours:Send a written dispute within 30 days of first contact. Include your name, account number, and a clear statement that you're disputing the debt. Forest Hill Management provides an online dispute form, and their blog article "How To Submit A Written Dispute To The Forest Hill Management" walks through exactly what to include.

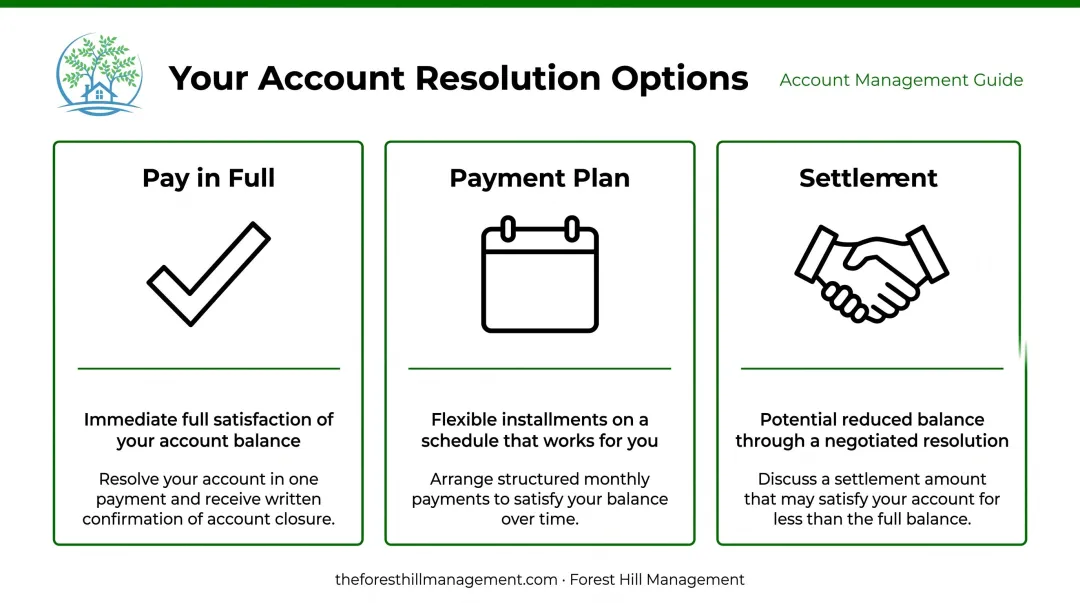

If you recognize the debt:Contact Forest Hill Management to discuss options. Resolution doesn't have to mean paying everything at once — payment plans, settlements, and reduced payoff options are available.

How to Resolve Your Account with Forest Hill Management

Three main resolution paths exist:

Forest Hill Management works directly with consumers to build arrangements that fit individual circumstances. No single rigid structure applies to everyone — each plan reflects your specific situation.

How to Get Started

- Log in at pay.theforesthillmanagement.com to explore options and make payments online

- Call (888) 471-0109 to speak with someone directly about building a payment plan

- Email info@foresthillmanagement.com for written confirmation requests or specific account inquiries

One Non-Negotiable Step

Before making any payment — especially for a settlement or payment plan — get the agreement in writing. The document should confirm the agreed-upon amount, the payment schedule, and what happens to the account once you complete the arrangement. Request this confirmation proactively; Forest Hill Management can provide it via email or mail.

What Happens If You Ignore a Debt Collection Notice?

The short answer: things get worse, not better.

Credit Reporting Impact

A delinquent collection account can appear on your credit report for up to 7 years from the date of the first missed payment that triggered the delinquency — a timeline set by the Fair Credit Reporting Act. The account's presence on your report can affect your ability to borrow, rent, or in some cases, get hired.

Per myFICO, collection accounts do affect FICO Scores, though the impact lessens as the information ages. FICO Score 9 and the FICO Score 10 suite disregard collections reported as paid in full — one concrete reason why resolving an account matters.

The Escalation Path

If you don't engage, the process can escalate:

- The account may be referred to an attorney

- A civil lawsuit may be filed against you

- If the collector obtains a court judgment, wage garnishment or a bank account order may follow, depending on your state's laws

None of those outcomes are inevitable. But they all become possible when a legitimate notice goes unanswered.

The Case for Proactive Engagement

The earlier you respond, the more options remain available. Reaching out to Forest Hill Management before the process escalates gives you access to payment plans, dispute rights, and negotiated timelines that typically disappear once a lawsuit is filed. Even a partial resolution stops the escalation clock and demonstrates good-faith effort.

Frequently Asked Questions

Is Forest Hill Management a legitimate debt collector?

Yes. Forest Hill Management is a legitimate receivables management organization operating in the United States since 2020. You can verify its legitimacy by requesting written debt validation under the FDCPA, reviewing its legal documentation at theforesthillmanagement.com, or contacting the company directly at (888) 471-0109.

What happens if I just ignore a debt collector?

Ignoring a legitimate collection notice does not make the debt disappear. The account may continue to affect your credit report for up to 7 years, and the collector can escalate to a lawsuit, court judgment, and potential wage garnishment. Calling (888) 471-0109 early gives you the most options for resolution.

Can Forest Hill Management sue me for a debt?

A debt collector can pursue legal action, but lawsuits are typically a last resort — used when other resolution attempts have failed. The likelihood depends on the debt amount, its age, and your state's statute of limitations. Reaching out before an account escalates gives you the best chance to negotiate a workable resolution.

How do I verify that a debt Forest Hill Management is collecting is mine?

Send a written validation request within 30 days of first contact, asking for the original creditor name, account number, and amount owed. Collection activity must pause until verification is provided. Forest Hill Management also offers an online dispute form at theforesthillmanagement.com for inaccurate debts.

Can I negotiate a payment plan instead of paying all at once?

Yes. Forest Hill Management offers flexible, customized payment arrangements based on your individual financial situation. Log in to the portal at pay.theforesthillmanagement.com to see available options, or call (888) 471-0109 to work through a plan directly with their team.