How Installment Loans Work and Their Key Features

Need Help Reviewing Your Account?

Contact UsIntroduction

Are you tired of playing financial whack-a-mole, constantly juggling expenses? Let's make sense of installment loans and see if they can finally provide some relief from that pesky financial game!

Installment loans are a popular financial product that can empower individuals to finance large purchases or consolidate debt. By understanding how these loans work and their key features, you can take charge of your financial decisions. This comprehensive guide will walk you through the basics of installment loans, their benefits and drawbacks, alternatives, and tips for managing them effectively.

What are Installment Loans?

An installment loan is a type of loan that is repaid over time with a set number of scheduled payments. These loans are commonly used for significant expenses, such as personal loans, auto loans, and mortgages. For instance, a personal loan could be used to finance a wedding, an auto loan could be used to purchase a car, and a mortgage could be used to buy a house. Unlike payday loans, which typically require repayment in a single lump sum, installment loans offer fixed repayment terms and predictable monthly payments, making them easier to manage within a budget.

Installment loans differ from other types of loans primarily in their structure and terms. For example, payday loans typically require repayment in a single lump sum within a short period, usually two weeks. In contrast, installment loans spread the repayment over several months or even years. Similarly, revolving credit, such as credit cards, allows for ongoing borrowing up to a credit limit with variable monthly payments. This means that you can borrow and repay as much as you want within the credit limit, and your monthly payment will vary depending on your balance. In contrast, installment loans have a fixed repayment schedule, which means that your monthly payment will stay the same throughout the loan term.

Key Features of Installment Loans

Installment loans are a popular financing option that allows borrowers to repay a set amount over a predetermined period. These loans are characterized by their fixed monthly payments and structured terms, making them an appealing choice for many. Understanding the key features of installment loans can help you determine if they fit your financial needs. Here are the primary benefits and potential drawbacks to consider.

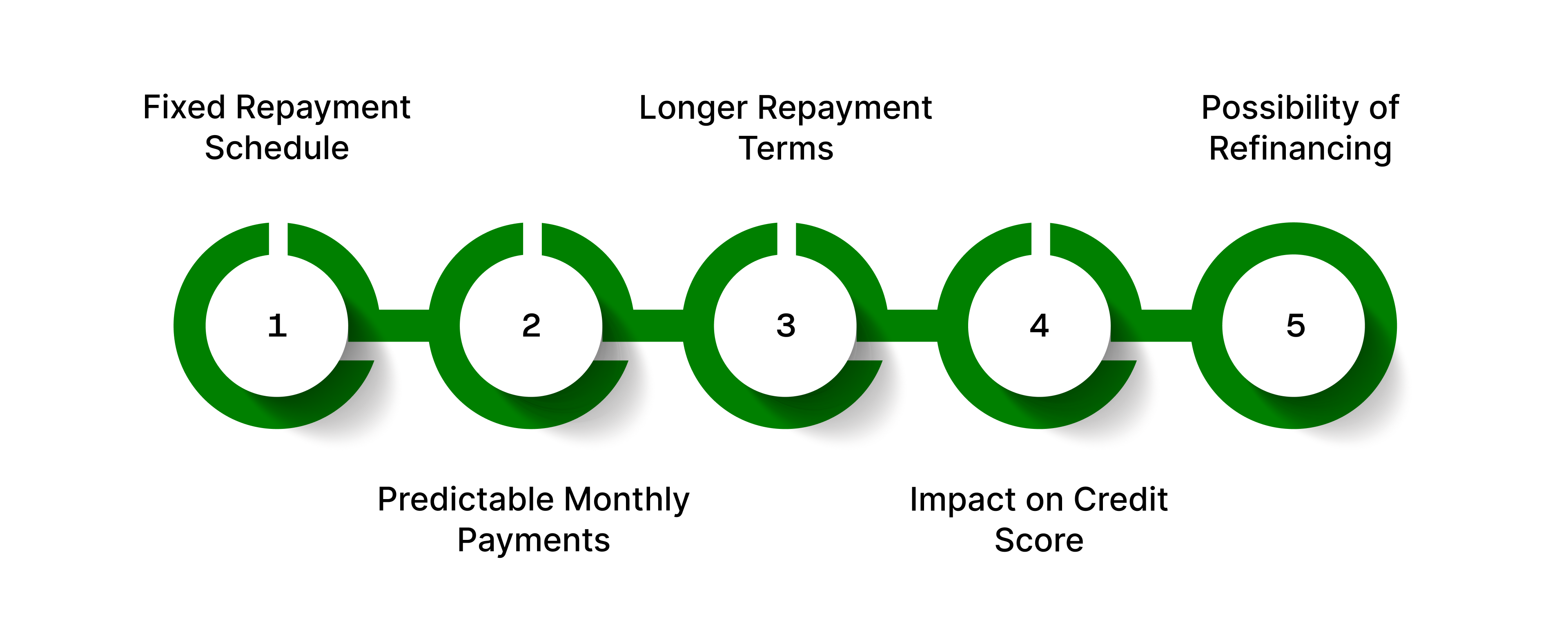

- Fixed Repayment Schedule

One of the primary features of installment loans is the fixed repayment schedule. Borrowers know exactly when payments are due and how much they will be, aiding in budgeting. This fixed schedule contrasts with the variable payments on revolving credit accounts like credit cards.

- Predictable Monthly Payments

Fixed payments make it easier to manage finances without unexpected fluctuations. This predictability is particularly beneficial for those on a tight budget or with fixed monthly expenses.

- Longer Repayment Terms

These loans often have more extended repayment periods than other loan types, spreading the cost over several years. This can make large purchases more affordable by breaking them into manageable monthly payments.

- Impact on Credit Score

Installment loans can impact your credit score in several ways:

Suppose you need help to keep up with payments. In that case, consulting with debt management professionals in Forest Hill can mitigate these risks and help protect your credit score.

- Possibility of Refinancing

Borrowers can refinance their installment loans if better terms become available. Refinancing involves taking out a new loan to pay off the existing one. This can lower your interest rate, reduce your monthly payment, or shorten your loan term. However, it's essential to consider any fees or penalties associated with refinancing, as these can affect the overall cost of the loan. Refinancing can be a beneficial strategy if it helps you save money or pay off your loan faster.

Types Of Installment Loans

Installment loans come in various forms, each designed to meet specific financial needs. Understanding the different types can help you choose the right loan. Here, we'll explore the most common types of installment loans and their key features and differences.

Secured vs. Unsecured Loans

Secured Loans Secured loans require collateral—an asset the lender can seize if you fail to repay the loan. Common types of collateral include homes, cars, and savings accounts. Because the risk to the lender is lower, secured loans often have lower interest rates and more favorable terms.

Examples:

- Auto Loans are used to purchase vehicles, with the car as collateral.

- Mortgages: Loans for buying property, with the home serving as collateral.

Unsecured Loans Unsecured loans do not require collateral, making them riskier for lenders. As a result, they typically come with higher interest rates and stricter approval criteria. These loans rely on your creditworthiness and ability to repay the loan based on your income and credit history.

Examples:

- Personal Loans: Can be used for various purposes, such as debt consolidation, home improvements, or medical expenses.

- Credit Cards: While not installment loans, credit cards are a form of unsecured credit with revolving terms.

Now that we have covered the different types of installment loans, let's examine how these loans actually work.

How Do Installment Loans Work?

Installment loans are a common form of borrowing that allows individuals to finance large purchases or consolidate debt through fixed monthly payments over a specified period. Understanding how these loans work can help you make informed decisions and manage your finances effectively.

This section will explore the mechanics of installment loans, from application and approval to repayment and potential impacts on your financial health.

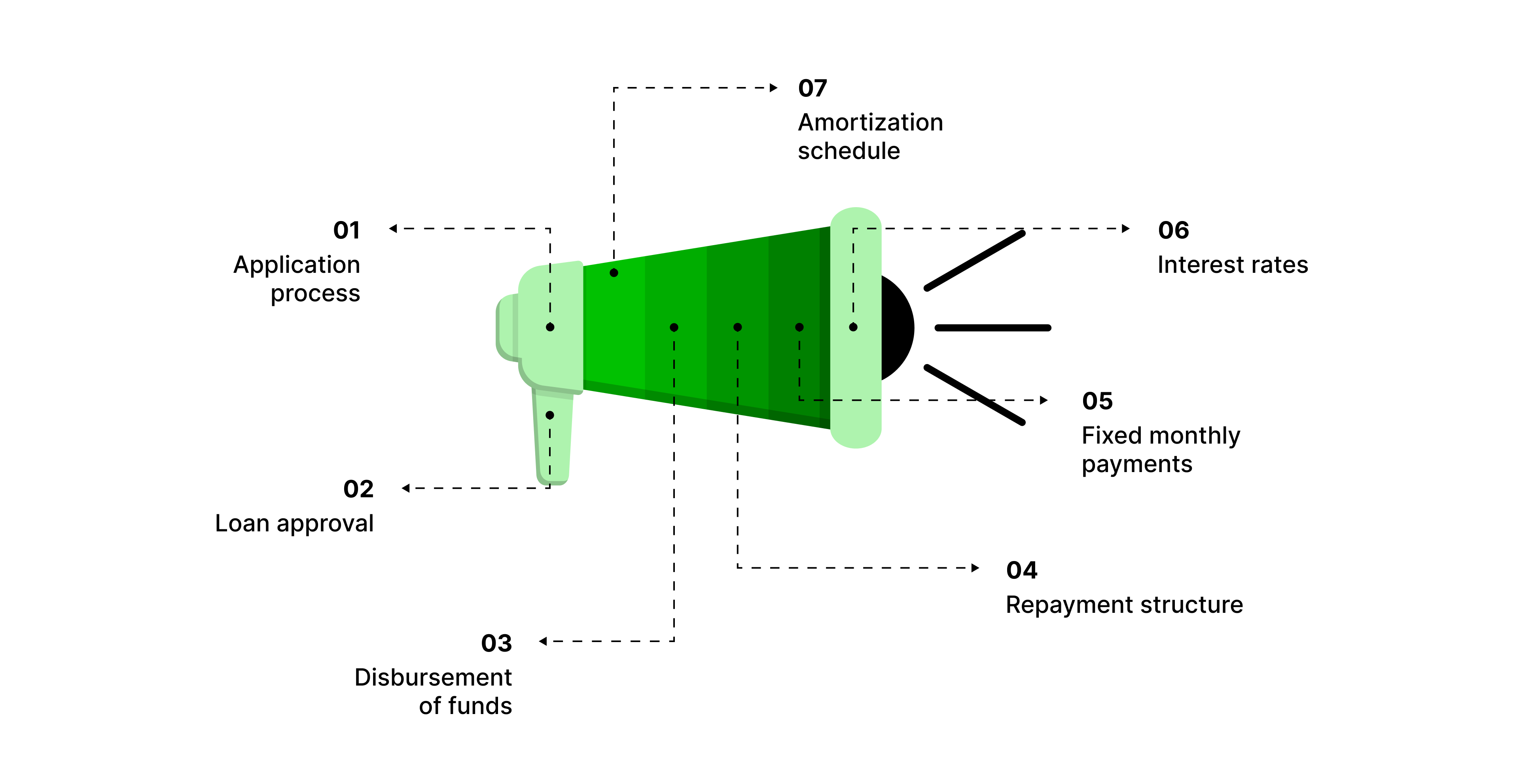

1. Application process

Potential borrowers need to meet eligibility criteria and provide necessary documentation, such as proof of income, employment, and credit history. The application process typically involves filling out an application form, providing the required documents, and waiting for the lender's decision. Depending on the lender, the application process can be done online, in person, or over the phone. It's important to be prepared and have all the necessary documents ready to speed up the process.

2. Loan approval

Lenders evaluate the applicant's creditworthiness through credit checks and determine loan terms based on their findings. A good credit score can lead to better interest rates and loan terms. A poor credit score may result in higher interest rates or loan application denial.

3. Disbursement of funds

Once approved, the loan amount is disbursed to the borrower directly or to the entity receiving payment (e.g., a car dealership). The disbursement method and timeline can vary based on the lender and the type of loan.

4. Repayment structure

Borrowers repay the loan through fixed monthly payments, including principal and interest. The interest rate can be fixed or variable, impacting the total repayment amount over time. The repayment schedule is typically outlined in an amortization schedule, showing how each payment is divided between interest and principal.

5. Fixed monthly payments

One key feature of installment loans is fixed monthly payments. This means the borrower pays the same amount each month until the loan is fully repaid. This predictability helps with budgeting and financial planning.

6. Interest rates

Interest rates on installment loans can be fixed or variable. Fixed interest rates remain unchanged throughout the loan term, providing stability and predictability. Variable interest rates can change over time based on market conditions, leading to fluctuations in monthly payments.

7. Amortization schedule

An amortization schedule is a table that shows the breakdown of each loan payment into principal and interest and the remaining balance after each payment. This schedule helps borrowers understand how their fees are applied and how much they still owe over the life of the loan.

Understanding the mechanics of installment loans, it's time to weigh their benefits and drawbacks to see if they align with your financial goals.

Benefits And Drawbacks Of Installment Loans

When considering installment loans, weighing their advantages and disadvantages is essential. This section provides a clear overview of the benefits and drawbacks of installment loans, presented in a tabular format. Understanding these factors lets you decide whether an installment loan suits your financial situation.

Failing to make payments can lead to default, negatively impacting your credit score and financial stability. Engaging with a debt management service like Forest Hill can help introduce you to tailored solutions that help avoid such outcomes.

Alternatives To Installment Loans

While installment loans can be a helpful financial tool, they may not be the best fit for everyone. Exploring alternative financing options can help you find a solution that suits your needs and circumstances better. Before opting for an installment loan, consider these alternatives:

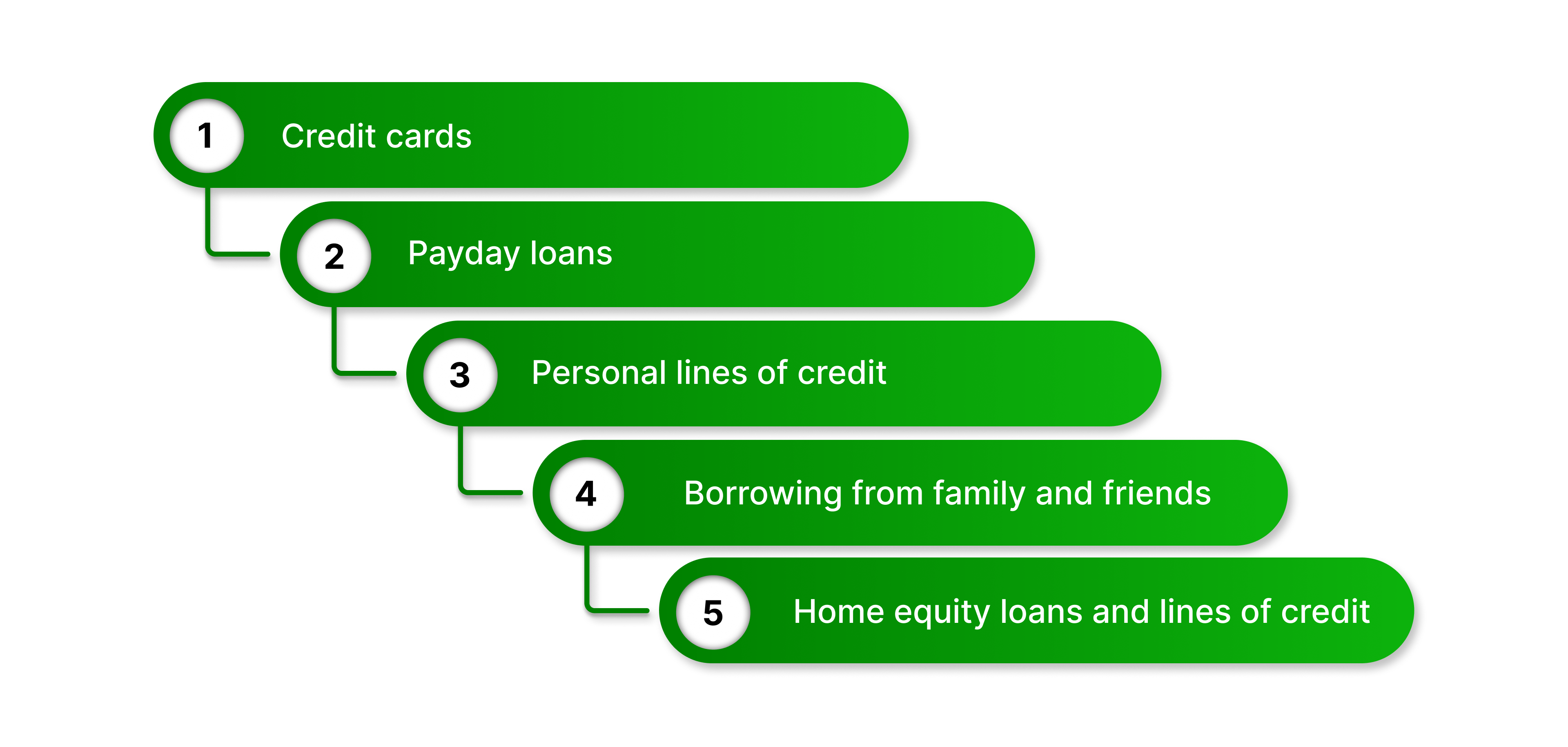

1. Credit cards

Credit cards can be helpful for more minor expenses and offer revolving credit with variable monthly payments. However, they often have higher interest rates than installment loans.

Pros

- Flexibility in spending and repayment

- Rewards and cashback programs

- No fixed repayment term

Cons

- Higher interest rates

- Risk of accumulating high-interest debt

2. Payday loans

Payday loans are short-term loans with very high interest rates and are suitable for emergencies only. They typically require repayment by the borrower's next payday.

Pros

- Quick access to cash

- Minimal credit checks

Cons

- Extremely high-interest rates

- Short repayment period leading to potential debt cycles

3. Personal lines of credit

A personal line of credit offers flexible borrowing with variable interest rates, typically provided by banks. Borrowers can draw on the credit line up to a predetermined limit as needed.

Pros

- Flexible borrowing and repayment

- Interest only on the amount borrowed

Cons

- Variable interest rates

- Potential for overspending

4. Borrowing from family and friends

This can be a low-cost option, but it can strain personal relationships. To avoid misunderstandings, it's essential to set clear terms and expectations.

Pros

- Low or no interest rates

- Flexible repayment terms

Cons

- Risk of damaging personal relationships

- Lack of formal agreement protections

5. Home equity loans and lines of credit

These use your home as collateral and often offer lower interest rates. They can be a good option for significant expenses but carry the risk of losing your home if you default.

Pros

- Lower interest rates

- Potential tax benefits

Cons

- Risk of foreclosure

- Requires sufficient home equity

How To Choose The Right Installment Loan?

Selecting the right installment loan is crucial for managing your finances effectively and meeting your financial goals. With various loan options available, it's essential to understand the key factors that can influence your decision, such as interest rates, loan terms, and your credit score. The steps involved in this process include:

- Assessing Your Financial Situation

Determine how much you need to borrow and what you can afford in monthly payments. Consider your income, expenses, and financial goals to ensure the loan fits your budget.

- Comparing Loan Offers

Shop around to compare lenders' interest rates, terms, and fees. Look for reputable lenders with positive reviews and transparent terms.

- Understanding Loan Terms

Read the fine print to understand the loan's terms and conditions thoroughly. Pay attention to interest rates, fees, repayment terms, and any penalties for early repayment or missed payments.

- Calculating Total Loan Cost

Factor in both the interest and any additional fees to determine the actual cost of the loan. Use online calculators or consult a financial advisor to get an accurate picture of your total repayment amount.

Tips For Managing Installment Loans

Effectively managing installment loans is crucial for maintaining financial health and avoiding potential pitfalls. Whether you're new to installment loans or looking to improve your current loan management, these insights will guide you towards smarter financial decisions. To manage your installment loan effectively:

Create a Repayment Plan

Plan your budget around your loan payments to ensure you can meet your obligations. Consider setting up a dedicated account for loan payments to keep your finances organized.

Automate Payments

Set up automatic payments to avoid missing due dates. Many lenders offer autopay options that simplify repayment and prevent late fees.

Communicate with Lenders

If you face financial difficulties, talk to your lender about possible solutions. They may offer payment deferral, loan modification, or other assistance to help you stay on track.

Monitor Your Credit Score

Track your credit score to understand how the loan affects your financial health. Regularly review your credit report for accuracy and address any issues promptly.

Personalized debt management services like Forest Hill can also help you find the best solutions tailored to your financial needs.

Before we wrap things up, let's address some of the most frequently asked questions about installment loans.

Frequently Asked Questions (FAQs)

1. What happens if I miss a payment?

Missing a payment can result in late fees and negatively impact your credit score. If you anticipate difficulty making a payment, it's crucial to communicate with your lender. They may offer solutions such as payment extensions or revised payment plans.

2. Can I pay off my loan early?

Some lenders allow early repayment without penalties, while others may charge a fee. Check your loan agreement for specific terms and conditions regarding early repayment.

3. How do installment loans affect my credit score?

Timely payments can improve your credit score by demonstrating responsible debt management. Conversely, missed payments can lower your credit score. Additionally, installment loans can diversify your credit mix, which benefits your credit profile.

4. What should I do if I can't make a payment?

Contact your lender immediately to discuss your options. They may offer payment deferral, loan modification, or other assistance to help you manage your payments. Ignoring the issue can lead to default, legal actions, and severe credit damage.

Conclusion

Understanding installment loans and their features is crucial for making informed financial decisions. These loans offer benefits such as predictable payments, lower interest rates, and flexible terms, making them ideal for large purchases and debt consolidation. However, potential drawbacks include high interest rates for those with poor credit and long-term financial commitments. Being well-informed about installment loans and managing them wisely can help you achieve your financial objectives and maintain stability.