How to Deal with Debt Collectors When You're Unemployed

Transform Your Financial Future

Contact UsReceiving debt collection calls while unemployed is one of the more stressful financial experiences a person can face. There's no paycheck coming in, the bills aren't stopping, and the phone keeps ringing. That combination creates real anxiety — particularly when you're unsure what collectors can actually do to someone with no income.

This situation is more common than most people realize. According to a CFPB survey, roughly 32% of consumers with a credit record reported being contacted by a creditor or collector trying to collect a debt in the prior year.

Here's what most people don't know: unemployment doesn't erase what you owe, but it changes what collectors can legally and practically do — and you have considerably more rights and leverage than you might think.

This guide covers your legal protections under the FDCPA, a practical step-by-step strategy for responding to collectors, key factors that affect your vulnerability, and longer-term paths to resolving the underlying debt.

Key Takeaways

- Federal law protects you from abusive or deceptive collection practices regardless of employment status.

- Unemployment may make you temporarily "judgment-proof" — meaning collectors can win a court judgment but still have nothing they can legally seize.

- You can legally request debt validation within 30 days of first contact, which pauses collection activity.

- Documenting every collector interaction — dates, names, what was said — gives you leverage if disputes arise.

- You can negotiate payment arrangements or settlements even with little to no current income.

Know Your Rights Under the FDCPA Before You Respond

The Fair Debt Collection Practices Act (FDCPA) is the federal law that governs how third-party debt collectors — collection agencies, debt buyers, and collection attorneys — may communicate with consumers. It applies to you whether you're employed, unemployed, or somewhere in between.

What Collectors Cannot Do

Under the FDCPA, collectors are prohibited from:

- Calling before 8:00 a.m. or after 9:00 p.m. local time

- Using threatening, obscene, or abusive language

- Making false statements about the debt, its legal status, or consequences

- Contacting your employer if they know or should know your employer prohibits it

- Repeatedly calling with intent to harass or annoy

Violations can be reported to the CFPB and may entitle you to statutory damages up to $1,000 per individual action, plus attorney fees.

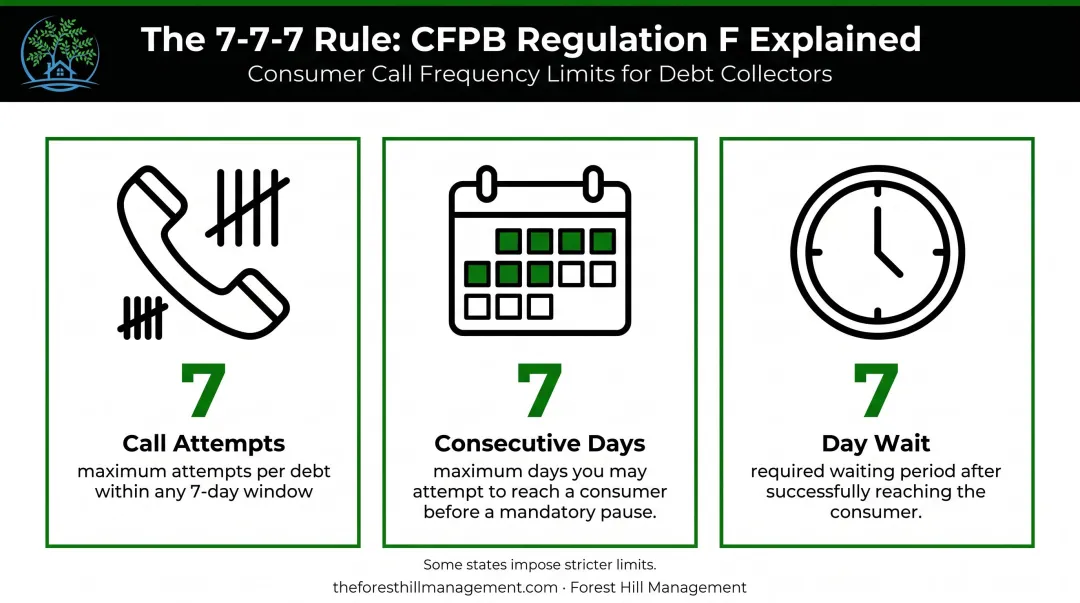

The 7-7-7 Rule (Regulation F)

CFPB's Regulation F, effective November 30, 2021, limits collectors to 7 phone call attempts within any 7 consecutive days for a specific debt. After reaching you by phone, they must wait 7 days before calling again. This is a federal ceiling — some states have stricter rules.

Your Right to Debt Validation

Within 30 days of first contact, you can send a written request asking the collector to verify the debt. Once they receive it, all collection activity must pause until they provide written verification. Your letter should include:

- Your name and address

- The account number referenced in their notice

- A clear statement that you dispute the debt and request verification

Send the letter via certified mail with return receipt so you have documented proof of delivery.

Your Right to Stop Contact

A written cease-and-desist letter legally requires the collector to stop contacting you, with two narrow exceptions: confirming they'll stop, or notifying you of a specific legal action. This legally ends contact — but use it deliberately. Stopping contact doesn't stop a lawsuit, and in some cases it accelerates one.

The FDCPA sets a federal floor, but many states go further. New York, for example, reduced its consumer debt collection statute of limitations to three years and bars revival through later payments. Check your state's specific laws before responding to any collector.

How to Deal with Debt Collectors When You're Unemployed: A Step-by-Step Approach

Step 1: Verify the Debt Before Responding

Don't engage until you know exactly what you're dealing with.

- Confirm the basics: Check the collector's name, original creditor, account number, and claimed balance against your own records.

- Check the statute of limitations: Most states allow between three and six years to sue on consumer debts, though some extend longer. If the debt is "time-barred," collectors may still attempt to collect — but they cannot legally sue you to enforce it.

- Send a validation request if anything is unclear: Do this within 30 days of first contact. Collectors must pause collection until they provide verification.

Companies like Forest Hill Management have formal debt verification processes in place — consumers can request account documentation directly through their online portal or by contacting their team.

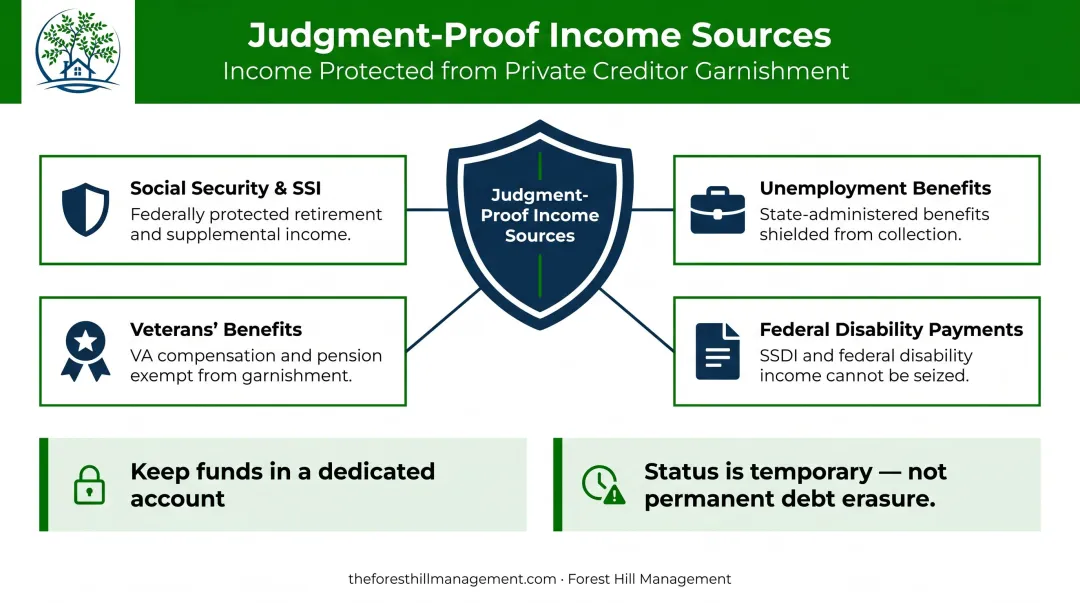

Step 2: Assess Your "Judgment-Proof" Status

Being judgment-proof means a collector who wins a lawsuit may still be unable to collect from you because your income and assets are legally exempt from garnishment.

Protected income sources include:

- Social Security and SSI (protected under federal law from virtually all private creditor garnishment)

- Unemployment benefits (federal guidance generally prohibits interception for private debts; most state laws concur)

- Veterans' benefits and federal disability payments

Two caveats worth knowing:

- Keep protected funds in a dedicated bank account — mixing them with other deposits can complicate your ability to claim the exemption if a levy is attempted.

- Judgment-proof status is temporary. It doesn't erase the debt; collectors can resume enforcement once your financial situation improves.

Certain government debts — federal student loans, IRS tax obligations — may be treated differently, so verify your state's rules if those apply to you.

Step 3: Communicate Strategically and Document Everything

How you handle collector conversations matters legally. A few rules:

What NOT to do:

- Don't admit the debt is yours outright

- Don't provide detailed personal financial information beyond what's necessary

- Don't agree to a payment plan you cannot actually maintain

- Don't make any payment on a time-barred debt — it can restart the statute of limitations in many states

What TO do:

- Keep a log of every contact: date, time, representative's name, what was said, and the number they called from

- Briefly state you are currently unemployed and ask whether any hardship accommodations are available

- Get anything they promise in writing before acting on it

A detailed record is what gives you leverage. If a collector calls at prohibited hours, uses threatening language, or misrepresents what they can do, you can report those violations — and may be entitled to damages as a result.

Step 4: Negotiate a Hardship Arrangement or Settlement

Many collectors — particularly on unsecured debts like credit cards or medical bills — are open to negotiation. Options include:

- Lump-sum settlement: Offer a reduced amount to fully resolve the balance. Debt buyers, who often purchase accounts for a fraction of face value (an FTC study found large debt buyers paid an average of 4 cents per dollar of face value), have more room to negotiate than original creditors.

- Temporary hardship deferral: Some collectors will pause collection activity for a defined period when a consumer demonstrates genuine financial hardship.

- Structured payment plan: A lower monthly payment based on what you can realistically afford.

Before agreeing to anything, get the terms in writing. Confirm whether the debt will be reported as "settled" or "paid in full" — these are treated differently on your credit report, and the distinction matters.

Tax implication: If a creditor forgives $600 or more, they may send a 1099-C form. Forgiven debt is considered taxable income unless an exclusion applies. Consult a tax professional if this is relevant to your situation.

Key Factors That Affect Your Vulnerability as an Unemployed Debtor

Not every unemployed consumer faces the same risk from collectors. Several variables determine how much leverage they actually have over you.

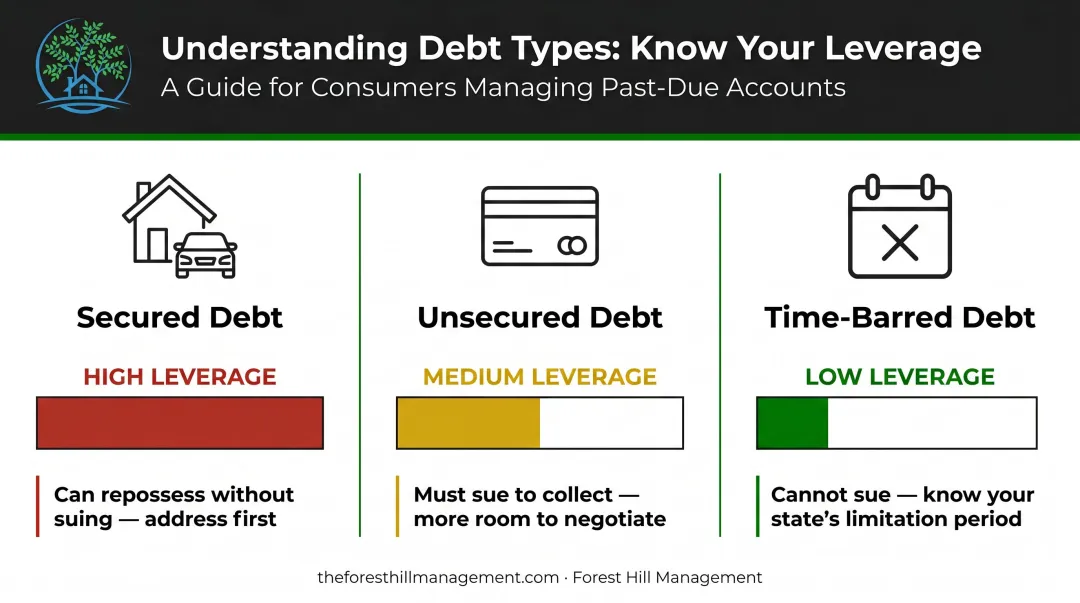

Type and Age of the Debt

Unsecured debts give collectors far less practical leverage than secured ones. Prioritize which debts you address based on what a creditor can actually do if you don't pay.

Your Income Sources and State Exemptions

How you hold protected income is just as important as whether it's protected. Key steps to reduce your exposure:

- Keep unemployment benefits, Social Security, and disability payments in a dedicated separate account to reduce the risk of wrongful garnishment or an account freeze

- Look up your state's exemption laws, which protect certain amounts of bank balances, personal property, and home equity from collection enforcement

- Never assume you're fully covered — exemption amounts vary significantly by state and directly affect how much collectors can reach

Original Creditor vs. Debt Buyer

This distinction matters for negotiation:

- Original creditors are generally not covered by the FDCPA and may have less flexibility to reduce principal balances.

- Third-party collectors and debt buyers are covered by the FDCPA and — especially if they purchased the account at a discount — often have more room to settle below the full balance.

Check any collection letter you receive for an "Original Creditor" field. This tells you whether you're dealing with the original lender or a third-party buyer — and that distinction directly affects your negotiating position and legal protections.

Common Mistakes to Avoid

- Don't ignore a debt lawsuit. Silence doesn't make debt disappear. The CFPB warns that a default judgment can trigger wage garnishment once you're re-employed, bank levies, or property liens.

- Avoid making any payment on a time-barred debt without first checking your state's rules. Even a minimal payment can restart the statute of limitations, giving the collector renewed standing to sue.

- Don't commit to payment terms you can't sustain. Collectors are trained negotiators, and defaulting on a plan you agreed to gives them additional grounds for legal action. It's better to say nothing than to promise something unworkable.

- Document every FDCPA violation. Prohibited-hour calls, threatening language, and misrepresentation of the debt are all reportable to the CFPB and FTC — and may entitle you to statutory damages.

Longer-Term Debt Relief Options to Consider

Fielding collector calls one at a time is a short-term tactic. At some point, a longer-term resolution strategy becomes necessary, particularly if your financial situation shifts and your judgment-proof status changes.

Hardship Programs and Nonprofit Credit Counseling

Many original creditors have financial hardship programs that can lower interest rates, reduce minimum payments, or temporarily pause collection. The CFPB notes that many credit card companies are willing to work with consumers facing financial emergencies — but these options typically must be accessed before the account is sold to a third-party collector.

Nonprofit credit counseling agencies affiliated with the NFCC can help structure Debt Management Plans (DMPs) — consolidating eligible unsecured debts into a single monthly payment with potentially reduced interest rates.

Debt Settlement and Professional Receivables Management

Debt settlement — negotiating to pay a reduced lump sum to resolve a balance — is most effective with delinquent, unsecured accounts that have been sold to third-party collectors. The gap between what the collector paid for the debt and the full balance creates negotiating room that benefits both parties.

Forest Hill Management works with consumers to find resolution paths that fit their actual situation, including payment plans based on what they can realistically afford. You can explore options through the online account portal at pay.theforesthillmanagement.com or speak directly with a representative at (888) 471-0109 about what arrangements are available for your account.

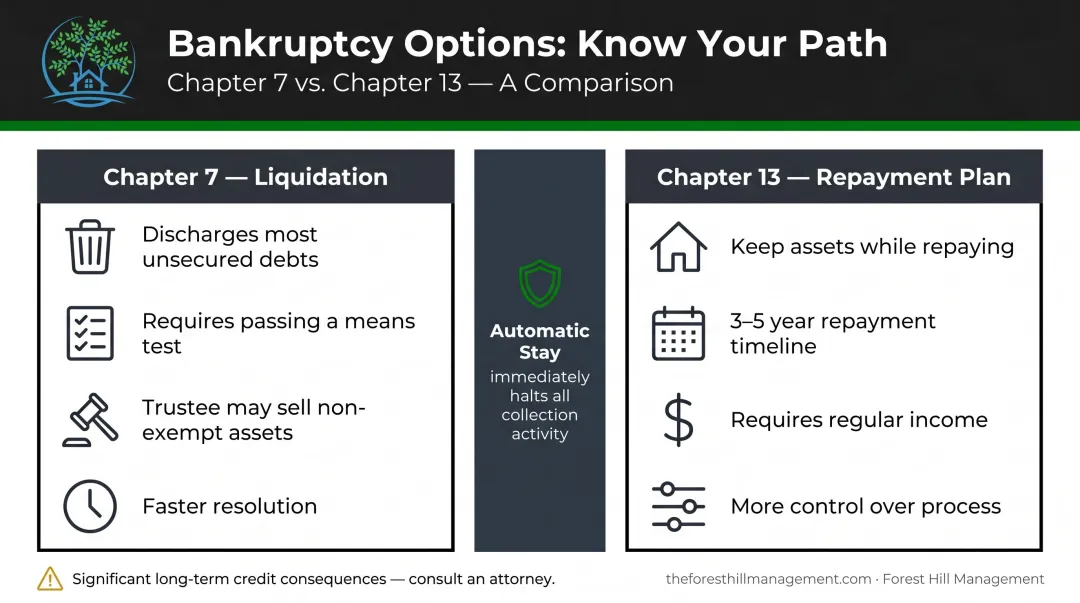

Bankruptcy as a Last Resort

Two primary options exist:

- Chapter 7 (Liquidation): Discharges most unsecured debts after a means test. A trustee may sell non-exempt assets.

- Chapter 13 (Repayment Plan): Allows you to keep assets while repaying creditors over three to five years, requiring regular income.

Both trigger an automatic stay that immediately halts all collection activity. The trade-off is significant long-term credit consequences. Consult a bankruptcy attorney before pursuing either route — the decision has implications that extend well beyond stopping collector calls.

Frequently Asked Questions

Can a debt collector sue you if you are unemployed?

Yes, but collectors can sue regardless of employment status. However, if you're unemployed with no garnishable wages or non-exempt assets, you may be "judgment-proof," meaning a court judgment may be unenforceable until your financial situation changes.

What is the 7-7-7 rule for debt collectors?

Under CFPB's Regulation F, collectors are limited to 7 call attempts within any 7-day period for a specific debt, and must wait 7 days after reaching you before calling again. This is a federal minimum; some states impose stricter limits.

Can debt collectors garnish unemployment benefits?

Federal guidance generally prohibits intercepting unemployment benefits for private debts, and most state laws agree. Exceptions may apply for certain government obligations like child support or tax debt. Verify your state's specific rules.

What should I say to a debt collector when I have no income?

Confirm you're speaking with the correct collector, avoid admitting the debt outright, and state that you are currently unemployed and unable to make payments. Ask about hardship options and document every detail of the conversation afterward.

How do I get a debt collector to stop calling me?

Send a written cease-and-desist letter via certified mail. Once received, the collector may only contact you to confirm they'll stop or to notify you of a specific legal action. This does not erase the debt and may prompt a lawsuit, so use it deliberately.

What happens if I ignore debt collectors while unemployed?

Ignoring collectors risks a default court judgment, which can later trigger wage garnishment once you're re-employed, bank account levies, or property liens. Even if you can't pay, communicating proactively puts you in a far stronger position than going silent.