How to Dispute a Debt in California Successfully

Transform Your Financial Future

Contact UsGetting a debt collection notice in the mail is stressful — but California consumers have more legal ammunition than most realize. Between the federal Fair Debt Collection Practices Act (FDCPA) and California's own Rosenthal Fair Debt Collection Practices Act, you have real tools to challenge debts that are inaccurate, paid, or simply not yours.

The catch? Those tools only work if you use them correctly. Miss the 30-day window, dispute verbally instead of in writing, or skip documentation — and you forfeit protections that could have stopped collection entirely.

This guide walks through exactly how to dispute a debt in California, what affects your outcome, and what happens next.

Key Takeaways

- You have 30 days from receiving a debt validation notice to dispute in writing and trigger the collector's legal duty to pause collection

- Only written disputes activate FDCPA protections — verbal disputes do not trigger the cease-collection requirement

- California's Rosenthal Act extends FDCPA protections to original creditors, not just third-party collectors

- Disputing a debt pauses collection — it doesn't erase the debt, but forces verification before reporting or continued contact

- Report collector violations to the CFPB, California DFPI, or California Attorney General

How to Dispute a Debt in California Step by Step

Step 1: Review the Debt Validation Notice

When a debt collector first contacts you, they must send a written validation notice within 5 days of that initial communication (unless the information was already provided). Under CFPB Regulation F, effective November 30, 2021, that notice must include:

- The creditor's name and contact information

- Your account number

- The amount owed as of the itemization date

- An itemized breakdown of interest, fees, payments, and credits since that date

- The dispute deadline (your 30-day window)

Before anything else, compare every detail on that notice against your own records. Discrepancies in the amount, creditor name, or account number are grounds for dispute.

Step 2: Verify Whether the Debt Is Legitimate

Common valid reasons to dispute a debt in California include:

- The debt isn't yours (wrong person or identity theft)

- You already paid it, in full or in part

- The amount is incorrect

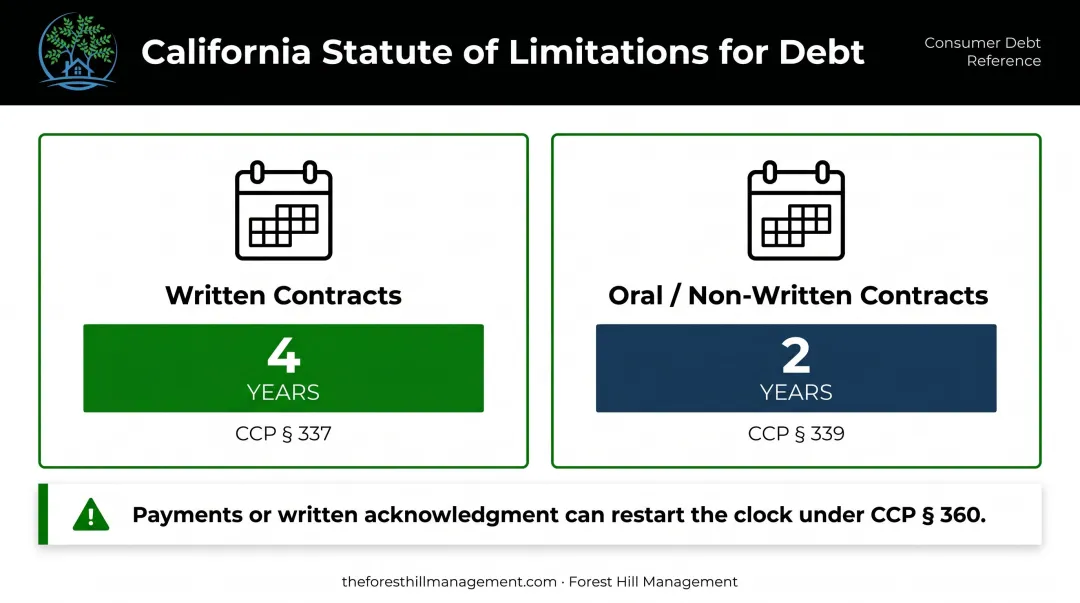

- The statute of limitations has expired (4 years for written contracts under California CCP § 337, or 2 years for oral contracts under CCP § 339)

- The debt resulted from fraud or unauthorized account opening

Pull your free credit report at AnnualCreditReport.com (free weekly reports are available from all three bureaus) to cross-reference any collection account against your credit history.

Time-barred debt warning: A collector can still attempt to collect a debt past its statute of limitations, but cannot sue to enforce it. According to the California Attorney General's office, collectors may still contact you about old debts.

Proceed with caution: making a payment or providing a signed written acknowledgment can restart the clock under CCP § 360.

Step 3: Gather Supporting Documentation

Collect everything relevant before drafting your dispute letter:

- The debt validation notice itself

- Payment receipts, bank statements, or cancelled checks

- Account agreements or prior correspondence

- Police report or FTC identity theft report (if fraud is involved)

- Any prior communications from the original creditor

Send copies only (never originals). The FTC advises keeping original supporting documents in your possession. For the dispute letter itself, the CFPB recommends keeping a copy and sending the original letter to the collector.

Step 4: Send a Written Dispute Letter Before the 30-Day Deadline

Under FDCPA 15 U.S.C. 1692g(b), a written dispute sent within 30 days of receiving the validation notice legally requires the collector to stop all collection activity. They cannot resume until the debt is verified and mailed back to you.

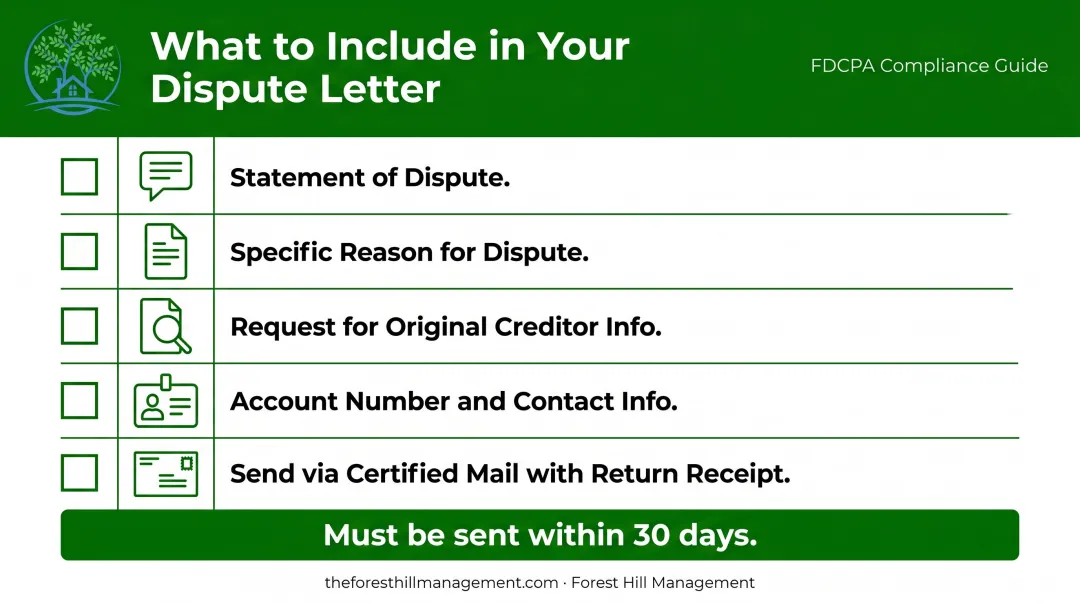

Your dispute letter should include:

- A clear statement that you dispute the debt (all or part of it)

- The specific reason: "this debt was already paid," "this is not my debt," or "the amount is incorrect"

- A request for the original creditor's name and address if dealing with a third-party collector

- Your account number and contact information

- Certified mail with return receipt requested (that timestamp is your proof of timely submission)

The CFPB offers sample dispute letter templates you can use as a starting point.

Step 5: Document Every Interaction Going Forward

Keep a dedicated file from day one. If your dispute is challenged or ignored, documentation is what gives you leverage:

- Copies of every letter sent and received, with dates

- Notes on any phone calls (date, time, name of representative, what was said)

- Certified mail receipts and return receipt confirmations

If the dispute moves to a credit bureau complaint, a regulatory filing, or a legal claim against the collector, this record is your foundation.

Key Factors That Affect the Outcome of Your Dispute

Not all disputes succeed equally. Several variables determine whether your dispute results in debt verification, removal, or resumed collection.

Timing: The 30-Day Window

Disputing within 30 days triggers the FDCPA's cease-collection requirement automatically. After 30 days, that automatic protection disappears. The collector can legally keep contacting you even if you dispute later. You can still dispute after 30 days, but your leverage decreases significantly.

Written vs. Verbal Communication

Calling the collector to dispute doesn't trigger FDCPA 1692g(b)'s protections. Only a written dispute does. No matter how clear the conversation seems, verbal disputes don't create a legal obligation for the collector to pause and verify. Always put it in writing.

California-Specific Protections

California adds two layers beyond the federal FDCPA:

- Rosenthal Fair Debt Collection Practices Act (California Civil Code §§ 1788.2 and 1788.17): The Rosenthal Act applies FDCPA protections to original creditors collecting their own debts — not just third-party collectors covered by federal law. That coverage gap doesn't exist under California law.

- Debt Collection Licensing Act (SB 908): Under California Financial Code § 100001, no person may conduct debt collection in California without a license from the DFPI. The DFPI began accepting applications on September 1, 2021. You can verify a collector's license status through the DFPI's licensing page.

Statute of Limitations

A collector cannot sue on time-barred debt, but they can still attempt to collect informally. Knowing where your debt falls on this timeline tells you how much legal exposure you actually face.

Common Mistakes That Can Derail Your Dispute

Disputing Verbally or Waiting Too Long

These two errors are the most frequent — and the most costly. Calling instead of writing, or missing the 30-day window, both result in losing the automatic cease-collection protection. Once you've received the validation notice, the clock starts immediately.

Paying Without Verifying

Never pay any amount on a disputed debt before the collector verifies it. Even a small partial payment can be interpreted as acknowledgment of the debt. Under California CCP § 360, payments on principal or interest owed on a promissory note can constitute sufficient acknowledgment to restart the statute of limitations. Verification protects both your legal rights and your timeline — skipping it can cost you both.

Failing to Keep Records

Without certified mail receipts and copies of your correspondence, you have no proof your dispute was received. That documentation matters in two specific scenarios: if the collector continues collection activity after receiving your dispute, or if they never respond at all. Either situation may support a regulatory complaint or an FDCPA claim — but only if you have the paper trail to back it up.

What Happens After You Dispute a Debt in California

Once a collector receives your written dispute, FDCPA 1692g(b) requires them to stop all collection activity — including calls and credit bureau reporting — until they obtain and mail verification to you.

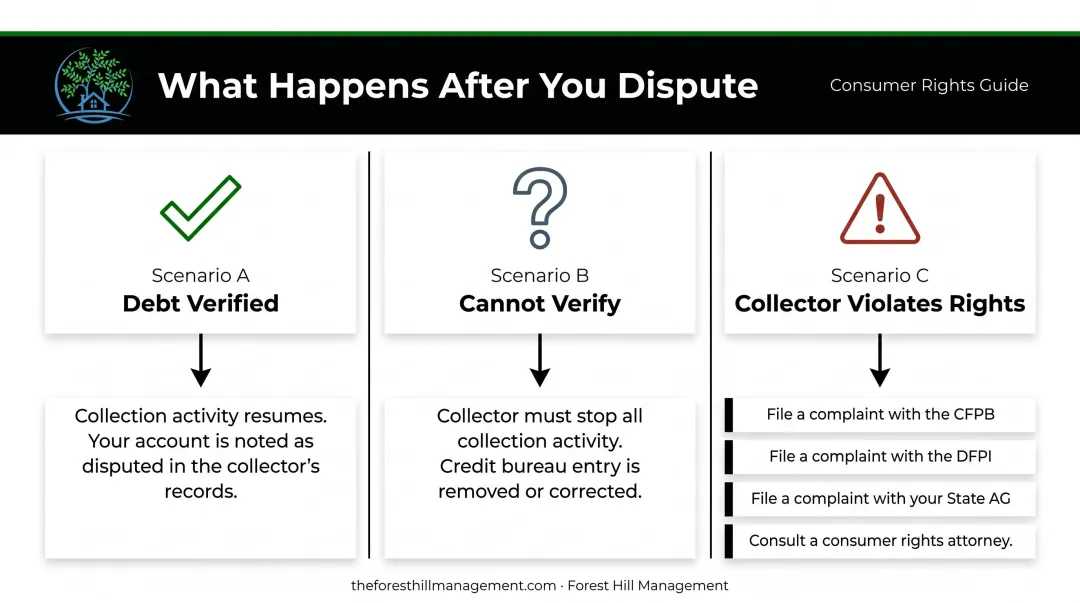

Scenario A — Collector Verifies the Debt

The collector provides documentation proving the debt is valid. Collection may resume, but any credit reporting must note the debt as disputed under FDCPA 1692e(8).

Your options at this stage include negotiating a settlement, setting up a payment plan, or working directly with the collector on an arrangement outside of court. If your account is held by Forest Hill Management, you can manage repayment through their online payment portal or contact them to discuss a payment plan that fits your situation.

Scenario B — Collector Cannot Verify the Debt

If the collector can't provide adequate verification, they must stop all collection activity and cannot report the debt to credit bureaus. Any existing negative entry tied to that account may need to be removed.

Scenario C — Collector Violates Your Rights

Violations include continuing to call after receiving your written dispute, reporting unverified debt, or using deceptive or threatening language. These actions violate FDCPA sections 1692d, 1692e, and 1692f. Your options:

- File a complaint with the CFPB

- File a complaint with the California DFPI

- File a complaint with the California Attorney General

- Consult a consumer protection attorney — FDCPA 1692k allows successful plaintiffs to recover actual damages, up to $1,000 in additional damages, and attorney's fees

Credit Bureau Disputes as a Parallel Step

If the disputed debt already appears on your credit report, file a separate dispute directly with the relevant bureaus. Under FCRA § 1681i, each bureau must complete a reinvestigation within 30 days (extendable by 15 days if you provide additional information) and must delete or correct information that is inaccurate, incomplete, or unverifiable.

Frequently Asked Questions

What are valid reasons to dispute a debt?

The main grounds are: the debt isn't yours, you already paid it, the amount is wrong, the statute of limitations has expired (4 years for written contracts in California), or the debt resulted from identity theft or fraud.

How do I dispute a debt that isn't mine?

Send a written dispute letter stating clearly the debt doesn't belong to you, include supporting ID or fraud documentation, and request verification or cessation of collection. Identity theft victims should also file a report with the FTC at IdentityTheft.gov.

Is it worth disputing a debt?

When there's a genuine basis, yes. A successful dispute stops collection activity, protects your credit report, and can result in the debt being removed entirely if the collector can't verify it.

How long does a debt dispute take in California?

After receiving your written dispute, the collector must cease collection until they mail verification — there's no fixed FDCPA deadline for how long that takes. Credit bureau reinvestigations must generally be completed within 30 days under FCRA § 1681i.

Can disputing a debt hurt my credit score?

Filing a dispute itself does not affect your score. Both Experian and TransUnion confirm that initiating a dispute has no score impact — though subsequent changes to your credit file (additions or removals) may affect it.

What if the debt collector doesn't respond to my dispute?

If a collector fails to provide verification, they must cease all collection activity under FDCPA 1692g(b). File a complaint with the CFPB or California DFPI, and consult a consumer protection attorney if violations persist.