How to Get Out of Debt and Build Wealth Quickly

Transform Your Financial Future

Contact UsMillions of Americans are stuck in the same trap: making minimum payments every month, watching interest accumulate, and wondering why their savings never move. According to Experian's 2025 consumer debt study, the average American carries $105,444 in total debt, with credit card balances averaging $6,768—and the Federal Reserve reports credit cards now carry an average 21.52% APR on accounts assessed interest.

The frustrating reality is that getting out of debt and building wealth feel like competing priorities. They don't have to be. There's a logical sequence: eliminate high-cost debt strategically, build a financial foundation, then accelerate wealth. This article lays out that roadmap.

Here's what you'll learn: how to inventory your debt, which payoff method fits your situation, when to start investing, and how to transition from surviving to genuinely building wealth.

Key Takeaways

- Not all debt is equal—high-interest consumer debt destroys wealth; asset-tied debt at lower rates can be managed strategically

- The debt avalanche saves the most money; the debt snowball builds the most momentum

- Capture your full employer 401(k) match and keep a $1,000–$3,000 emergency fund, even while paying off debt

- The first $100,000 in net worth is the hardest; compound growth accelerates significantly after that

- Increasing income is the most powerful lever available—expense cuts have a floor, income doesn't

Understanding Your Debt: The Foundation of Financial Freedom

Before choosing a payoff strategy, you need a complete picture of what you owe. Most people underestimate their total debt because they think in monthly payments, not balances.

Take Full Inventory First

Pull every account and list the following for each:

- Current balance

- Interest rate (APR)

- Minimum monthly payment

- Account status (current, past due, or in collections)

That last point matters. The action plan differs significantly depending on whether accounts are current or delinquent. Past-due and collections accounts require immediate attention—they accumulate fees, damage your credit score, and can stay on your credit report for up to seven years from the original delinquency date.

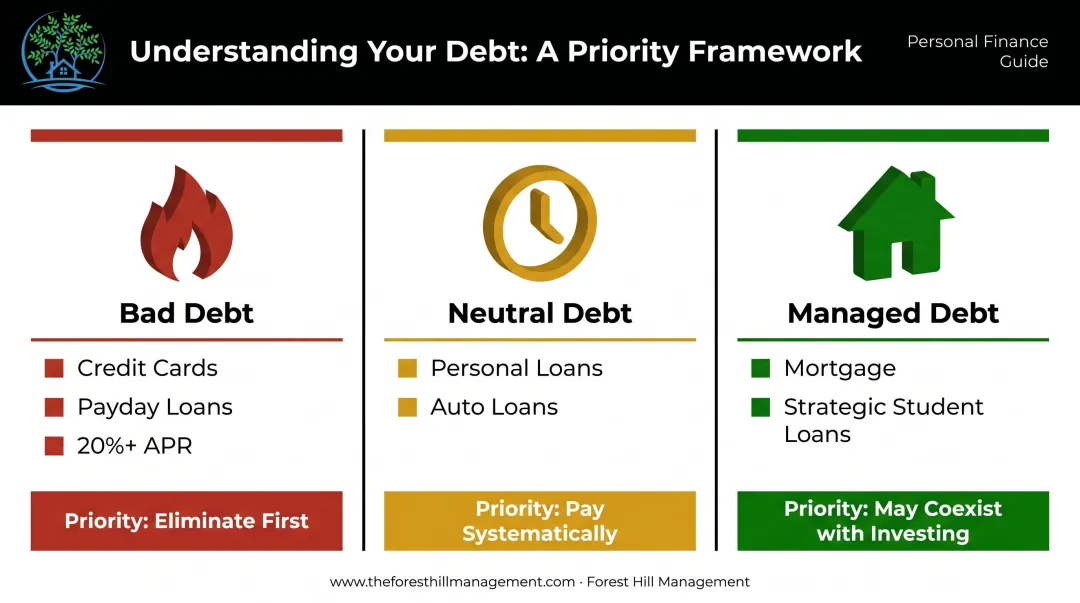

Good Debt vs. Bad Debt

Not all debt demands the same urgency. A useful framework:

High-interest consumer debt depletes wealth with certainty. A mortgage on an appreciating asset, or student loans that demonstrably increased earning power, can be managed differently. The distinction determines your entire payoff priority order.

If Accounts Are Already Past Due

Ignoring collection accounts lets fees and penalties compound while your credit score takes ongoing damage. The longer you wait, the fewer options you have.

If you've received communication from a receivables management organization like Forest Hill Management, start with three straightforward steps: verify the original creditor, confirm the debt is legitimate, and explore resolution options. Under the FDCPA, you have the right to request debt verification — which pauses collection activity while documentation is reviewed — and the right to dispute any account you believe is incorrect.

Forest Hill Management provides a self-service portal at pay.theforesthillmanagement.com and can be reached at (888) 471-0109 to discuss flexible payment arrangements. Clearing outstanding obligations before they escalate gives every other strategy in this guide a real foundation to build on.

Proven Strategies to Pay Off Debt Fast

Two frameworks dominate personal finance for debt elimination. Neither is universally superior—the right choice depends on what actually keeps you motivated.

Debt Avalanche Method

Best for: People who want to minimize total interest paid and can stay disciplined without quick wins.

How it works:

- List all debts from highest APR to lowest

- Make minimum payments on every account

- Direct every extra dollar to the highest-rate debt

- Once it's gone, roll that payment to the next highest rate

Why it works mathematically: At 21.52% APR (the current Federal Reserve average), credit card interest costs more than twice the S&P 500's historical average annual return of 9.90% since 1928. No investment reliably outpaces that drag. Paying off a 21% debt is a guaranteed 21% return.

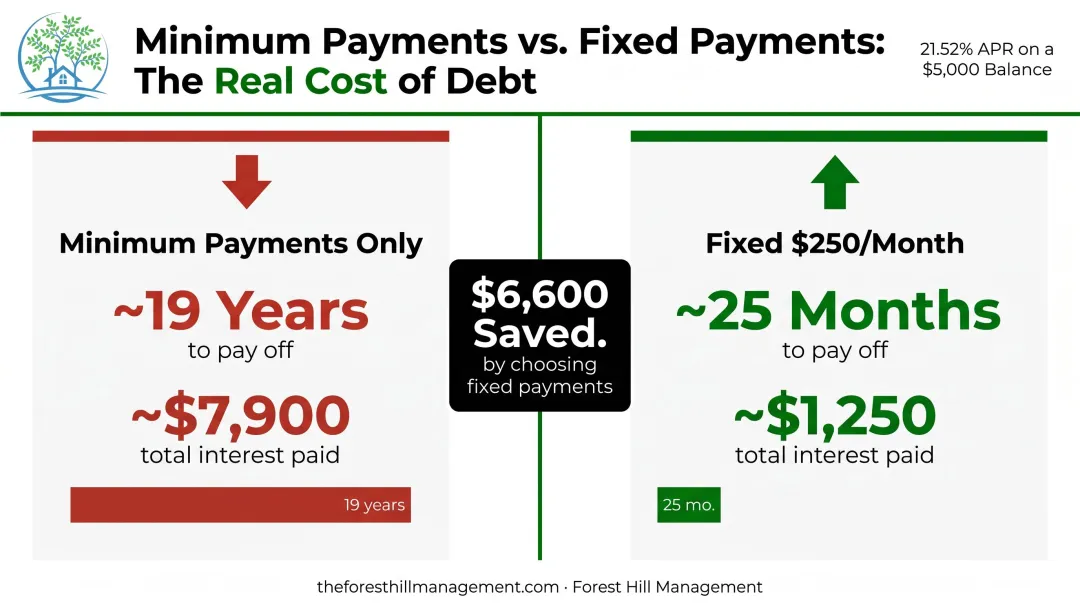

On a $5,000 balance at 21.52% APR, the difference between minimum payments and a fixed $250/month is stark:

That's over $6,600 saved by paying a fixed amount each month.

Debt Snowball Method

Best for: People who've tried and quit debt payoff plans before. Momentum matters more than math if you don't finish.

How it works:

- List debts from smallest balance to largest

- Eliminate the smallest first, regardless of interest rate

- Roll that freed-up payment to the next balance

The psychological wins from clearing accounts keep people consistent. If neither method fits perfectly, a hybrid works too: use the snowball to knock out one or two small balances for momentum, then switch to the avalanche for larger, high-interest debt.

Tactics to Accelerate Payoff

Beyond choosing a method, these tactics speed up the timeline:

- Switch to bi-weekly payments — You'll make 26 half-payments per year instead of 12 full ones, cutting interest and shaving months off your payoff date

- Direct windfalls entirely to principal — The IRS reported an average tax refund of $3,276, which could cut a typical credit card balance nearly in half

- Negotiate your interest rate: A LendingTree survey found 76% of cardholders who asked for a lower APR received one. Call your issuer, reference your payment history, and ask directly. It takes ten minutes and costs nothing.

Can You Build Wealth While Still in Debt?

Yes—but selectively. The rule of thumb: if an investment's expected return reliably exceeds the debt's interest rate, doing both simultaneously makes sense. The problem is that most debt rates make this math unfavorable.

The Two Parallel Priorities

While paying down debt, two financial moves should happen regardless:

1. Build a starter emergency fund ($1,000–$3,000)

Bankrate's 2026 emergency savings report found that 53% of Americans couldn't cover a $1,000 emergency from savings. Without a cushion, any unexpected expense—car repair, medical bill, appliance replacement—goes straight back onto a credit card, resetting months of progress. A small buffer breaks that cycle.

2. Capture your full employer 401(k) match

An employer match is an immediate 50–100% return on your contribution. No debt payoff strategy competes with that. Vanguard's data shows 22% of employees don't participate in their matched plans and another 24% contribute below the match threshold—leaving significant compensation on the table. Contribute enough to capture the full match, then direct everything else to high-interest debt.

When to Invest More Aggressively

Once you've handled those two priorities and only lower-rate debt remains—a mortgage under 4–5%, for example—it makes sense to shift more money toward investing. The S&P 500's 9.90% historical geometric annualized return (1928–2025) exceeds the cost of low-rate debt over a long time horizon.

The math flips completely with high-rate debt. A 22% APR credit card erases the gains from virtually any investment strategy. If you're earning 10% in the market while paying 22% on a credit card balance, you're losing 12% net. Investing aggressively under those conditions doesn't build wealth—it just offsets the damage.

From Debt-Free to Wealthy: Building Long-Term Wealth

Once high-interest debt is gone, the money that went to creditors every month is now yours to deploy. The critical mistake is letting lifestyle inflation absorb it instead.

The First $100,000 Milestone

Commonly attributed to Charlie Munger, the idea that the first $100,000 is the hardest holds up mathematically. Investopedia describes this threshold as the point where compound growth shifts from incremental to meaningful.

At $1,000 per month invested at a 7% average annual return, going from $0 to $100,000 takes roughly 79 months. Going from $100,000 to $200,000 takes about 54 months—25 months faster, with identical contributions. The math keeps accelerating from there. Reaching that first $100K as quickly as possible is the highest-leverage move in the early wealth-building phase.

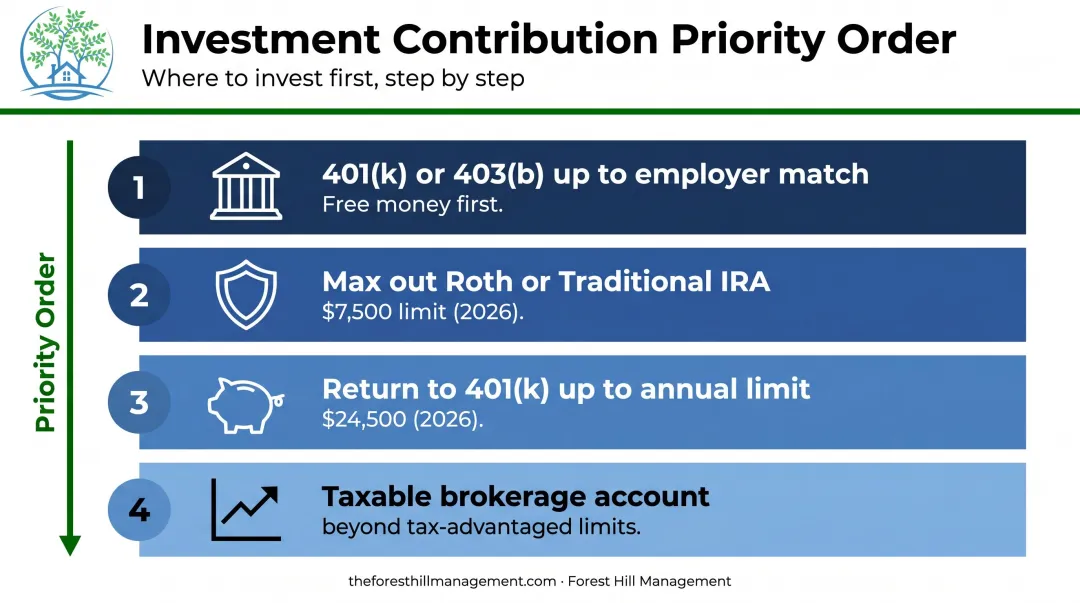

Maximizing Tax-Advantaged Accounts

Follow this priority stack:

- 401(k) or 403(b) up to employer match — Free money first, always

- Max out Roth or Traditional IRA — The 2026 limit is $7,500

- Return to 401(k) up to the annual limit — $24,500 in 2026

- Taxable brokerage account — For savings beyond tax-advantaged limits

Tax-deferred and tax-free growth compounds dramatically over decades. Fidelity illustrates that a $250,000 bond-fund investment in a Roth IRA can produce nearly $270,000 more after 20 years than the same investment in a taxable account, at a 35.8% marginal tax rate.

Automate contributions. Treat retirement investing like a non-negotiable bill. When the money moves before you see it, it stops feeling like a sacrifice.

Increasing Income as a Wealth Accelerator

Expense cuts have a hard limit. Income growth doesn't. The Federal Reserve's 2023 Survey of Consumer Finances found that real mean family income rose 15% from 2019 to 2022, with the largest gains concentrated at higher income levels. Pew Research Center data shows upper-income households carry median net worth 33 times higher than lower-income households.

Practical paths to income growth:

- Career advancement — Negotiate raises proactively; job-switching typically yields larger increases than annual reviews

- Skills development — Certifications, courses, and new competencies that increase market value

- Side income — Freelancing, consulting, or gig work that adds $500–$1,500 per month can shave years off debt payoff timelines

- Strategic job changes — Lateral moves to higher-paying employers often outperform within-company raises

What matters is keeping your savings rate steady as income rises. The gap between earnings and spending is what actually builds wealth over time.

Mistakes That Keep People Stuck in the Debt Cycle

Most debt payoff plans fail for predictable reasons. Here are three patterns that quietly derail even motivated people.

Ignoring past-due accounts. Collection accounts don't go dormant — they accumulate fees, damage credit scores, and can stay on your credit report for up to seven years. That poor credit then locks you out of better financial products: lower mortgage rates, reasonable car loan terms, and cards with rewards instead of penalty APRs. Resolving them is Step 1, not optional.

Making only minimum payments. On a $5,000 balance at 21.52% APR, minimum payments stretch payoff to roughly 19 years with nearly $7,900 in total interest — the original balance more than doubles. Fixed payments of $250 per month clear the same debt in 25 months. Minimum payments are structured to keep balances profitable for the issuer, not to help you pay them down.

Skipping the emergency fund. Without a financial cushion, a $600 car repair or a $400 medical copay goes straight back onto the credit card. Months of payoff progress evaporate in a single day. Building even a small buffer — $500 to $1,000 — is what keeps debt payoff from restarting at zero every few months.

Frequently Asked Questions

Can you build wealth while in debt?

Yes, but selectively. Capture any employer 401(k) match—that's an immediate 50–100% return—and build a $1,000–$3,000 emergency fund. Beyond that, aggressive investing should wait until high-interest debt is cleared, since a 21%+ APR reliably outpaces most investment strategies.

What creates 90% of millionaires?

That statistic is frequently misquoted. What the data actually shows is that consistent long-term investing, home equity, and income growth all contribute meaningfully to wealth. Pew Research confirms homeownership "looms large," while the Federal Reserve's Survey of Consumer Finances shows retirement accounts and financial assets play equally significant roles.

What is the 7-in-7 rule for money?

In consumer finance, the 7-in-7 rule is a CFPB debt collection regulation: collectors cannot call more than seven times about a debt within seven consecutive days, or within seven days after a phone conversation. No widely recognized personal finance wealth-building framework uses this name.

What is the fastest way to pay off debt?

The debt avalanche method—targeting the highest APR balance first—saves the most money and clears debt fastest mathematically. Combine it with income increases (side work, windfalls directed entirely to principal) and cuts to discretionary spending to accelerate the timeline further.

How much should I save before I start investing?

Start with a $1,000–$3,000 emergency fund, then focus on eliminating high-interest debt. Once that's cleared, expand your fund to 3–6 months of expenses and shift toward aggressive investment contributions. Always capture any employer 401(k) match from the start—it's free money.

What is the difference between good debt and bad debt?

Good debt is tied to appreciating assets or income growth—mortgages, strategic student loans—where the expected return justifies the cost. Bad debt carries high interest rates with no asset value in return: credit cards, payday loans, retail financing. The distinction determines your payoff priority order.