How to Cancel a Debt Settlement Contract

Transform Your Financial Future

Contact UsYou enrolled in a debt settlement program expecting relief. Instead, you're watching fees stack up, your credit score slide, and creditors calling anyway — with no settlements in sight.

This situation is more common than you'd think. A 2025 FTC complaint against Accelerated Debt alleged consumers were harmed by approximately $100 million through illegal advance fees and false promises of 75%+ debt reductions. You have the right to exit. This guide covers exactly how to do it — and what to do next.

Key Takeaways

- You can cancel a debt settlement contract at any time — reputable companies must allow it without penalty under FTC rules

- The FTC's Telemarketing Sales Rule prohibits collecting fees before a debt is actually settled

- Cancellation requires written notice, stopping auto-drafts, and reclaiming any unearned escrow funds

- Unsettled debts remain your responsibility after cancellation, so have a repayment plan in place before you leave

What Is a Debt Settlement Contract?

A debt settlement contract is a formal agreement in which a for-profit company negotiates with your creditors to accept less than the full balance owed. You stop paying creditors directly and instead deposit money monthly into a dedicated savings account. Once enough funds build up, the company negotiates a lump-sum settlement.

These programs typically run 36 months or more, according to the CFPB. Under the FTC's Telemarketing Sales Rule, fees can only be charged after a debt is settled.

Why These Contracts Become Problems

The structure creates real risks:

- Interest and late fees keep accruing on unpaid accounts while you save

- Creditors may escalate to lawsuits, wage garnishment, or bank account freezes

- Your credit score deteriorates from missed payments while waiting for settlements

- Some companies charge fees that exceed what you save

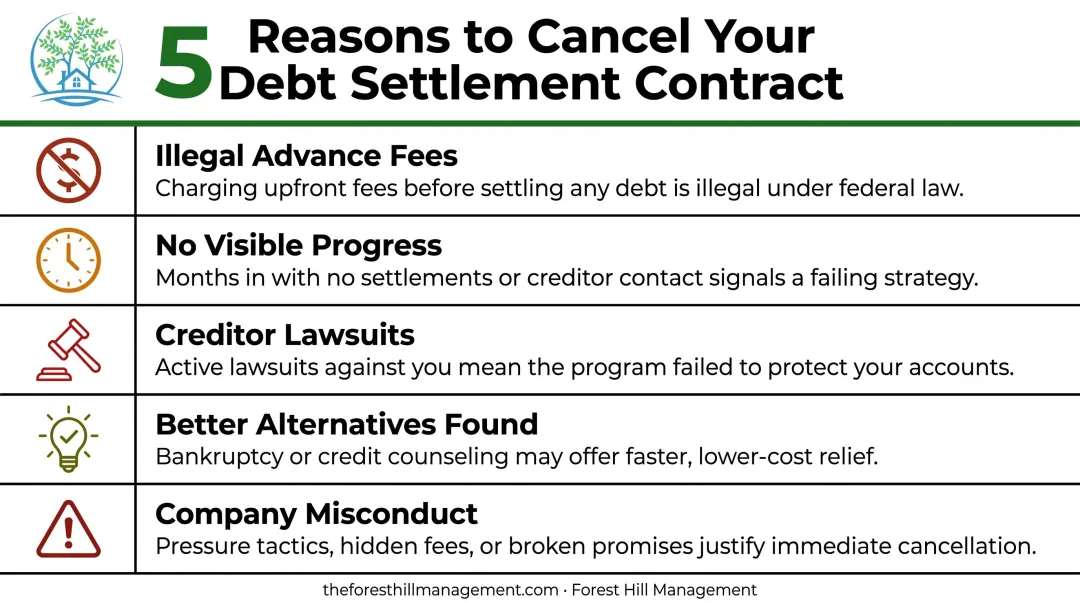

Common Reasons People Cancel

Consumer complaints about debt settlement companies follow consistent, documented patterns. A Maryland state study found 81 complaints alleging failure to provide promised services and 39 more citing improper billing or refusal to honor cancellation requests — and the reasons behind them are well-established.

- Illegal or excessive fees: The FTC's advance-fee ban — in effect since October 27, 2010 — prohibits collecting settlement fees before a debt is resolved. Being charged upfront is a clear violation.

- No visible progress: Programs can run for years with no actual settlements, while accounts fall deeper into delinquency.

- Creditor lawsuits: Stopping payments can prompt legal action. The CFPB confirms this risk directly: collections, lawsuits, and judgments that allow wage garnishment are all possible outcomes.

- Better alternatives emerged: You may have qualified for bankruptcy, found a nonprofit credit counseling program, or received a financial windfall that makes paying off debt directly viable.

- Company misconduct: Undisclosed fees, guaranteed outcomes, impersonation of banks or government agencies — these are documented FTC violation patterns. If you've spotted them, cancel the contract and file a complaint with the FTC.

How to Cancel a Debt Settlement Contract

Stopping payments is not the same as canceling. Following the correct process protects you from ongoing fees, unresolved debts, and disputes over your escrow funds.

Step 1: Review Your Contract

Find the cancellation clause. Look for:

- Required notice method (written letter, email, certified mail)

- Notice periods (typically 30 days or less for reputable companies)

- Any stated cancellation fees

If your contract doesn't allow penalty-free cancellation, that's a red flag on its own.

Step 2: Send Written Notice

Even if the company accepts phone cancellations, always follow up in writing. Your notice should include:

- Your full name and account number

- The date

- A clear statement that you are terminating the agreement

- A request for written confirmation of cancellation

Send via certified mail with return receipt, and keep copies of everything.

Step 3: Stop Automatic Bank Drafts

Contact your bank immediately after sending your cancellation notice. Revoke authorization for any automatic debits to the debt settlement company. If the company continues withdrawing funds after cancellation:

- Ask your bank to block those specific transactions

- As a last resort, consider closing the linked account to cut off access entirely

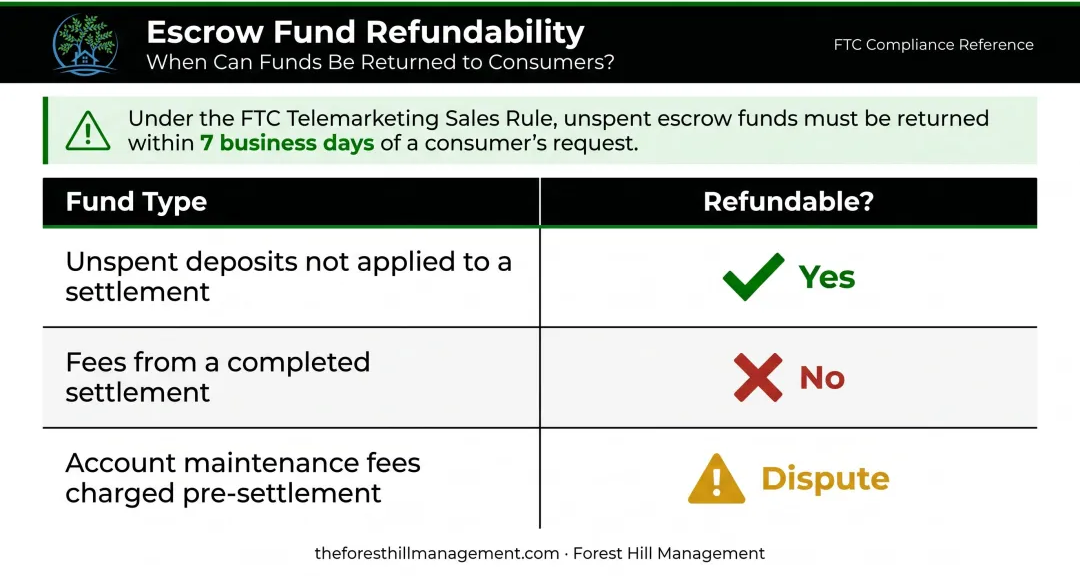

Step 4: Reclaim Your Escrow Funds

The money in your dedicated savings account is legally yours. Under the FTC's Telemarketing Sales Rule, the company must return all unearned funds within 7 business days of your withdrawal.

What's refundable vs. what isn't:

If the company refuses to return your funds, file a complaint with the FTC, your state attorney general, or consult a consumer law attorney.

Step 5: Notify Your Creditors Directly

Contact each creditor and let them know:

- You are no longer represented by a debt settlement company

- You want to discuss your account directly

- You'd like an updated balance including accrued interest and fees

This prevents collection efforts from escalating due to silence — and puts you back in direct control of negotiating your own terms.

What Happens After You Cancel

Cancellation ends your relationship with the debt settlement company — not your obligation to the debts themselves. Any debts successfully settled before you canceled remain settled. Everything else is still owed, plus accrued interest and fees.

Creditors will likely resume or escalate contact once negotiations stop. Knowing your options before that happens puts you in a stronger position.

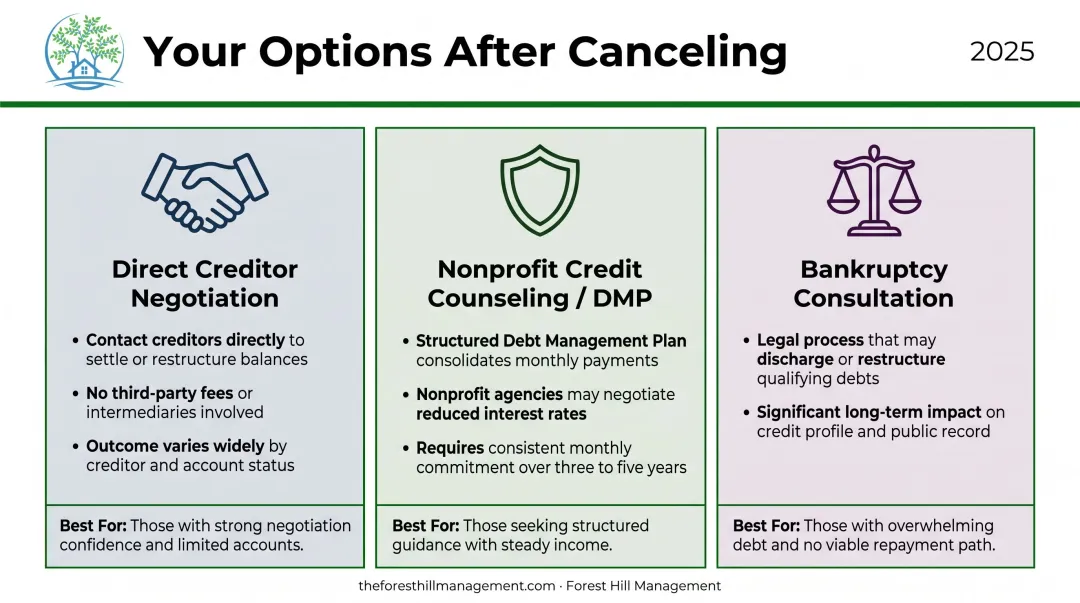

Your Three Main Paths Forward

- Negotiate directly with creditors — Many creditors prefer this. If you can demonstrate financial hardship and a concrete repayment intention, they may offer a reduced balance or structured payment plan.

- Enroll in a nonprofit credit counseling program — A debt management plan through a nonprofit agency typically involves no debt reduction but consolidates payments at reduced interest rates, without the credit damage of stopped payments.

- Consult a bankruptcy attorney — If the debt load is genuinely unmanageable, Chapter 7 or Chapter 13 may provide more complete relief than debt settlement ever could.

If your account has been transferred to Forest Hill Management, contacting them directly at (888) 471-0109 can clarify exactly what you owe and what structured repayment options are available.

The Credit Reality

Canceling a debt settlement program doesn't repair credit immediately. Missed payments, charge-offs, and collections already reported stay on your file. Payment history makes up 35% of your FICO score, per FICO — so the fastest path to recovery is consistent on-time payments going forward, even small ones. Settled accounts and late payments generally remain on credit reports for 7 years from the original delinquency date.

Should You Cancel or Stay?

Not every situation calls for cancellation. Use this framework:

Cancel if:

- The company charged fees before settling any debt (a direct FTC violation that justifies both exiting the contract and filing a complaint)

- No settlements have occurred after a reasonable period, and accounts are deepening into delinquency

- A creditor has filed or is threatening a lawsuit

- Bankruptcy or a debt management plan would better address your situation

Stay (or renegotiate) if:

- At least some debts have been settled as agreed

- The program is progressing and fees were clearly disclosed upfront

- Your hardship is temporary with no better alternative available

If you're leaning toward leaving, consider one more step first. Most debt settlement companies will negotiate a modified payment schedule or a temporary pause in contributions — it's worth asking before you walk away.

Conclusion

Canceling a debt settlement contract is your legal right. Done correctly — written notice, stopped auto-drafts, recovered escrow funds, and creditors notified — the process protects you from further financial harm and opens the door to an approach that actually fits your situation.

Cancellation is a course correction, not a defeat. From here, options like direct negotiation with creditors or enrolling in a debt management plan give you a structured path forward — one where you stay in control of the outcome.

Frequently Asked Questions

Can I back out of a debt settlement agreement?

Yes. Consumers can exit a debt settlement agreement at any time. Under FTC rules, reputable companies must allow cancellation without penalty. The process typically involves written notice and retrieval of any unearned escrow funds, which must be returned within 7 business days.

Is it better to settle or be dismissed?

A settled debt means the creditor accepted less than the full balance; the account closes with credit and potential tax implications, but the obligation is resolved. A lawsuit dismissal drops the case, though the underlying debt may still be owed — leaving the issue unresolved.

What two debts cannot be erased?

Child support and alimony obligations cannot be discharged through bankruptcy and are not eligible for debt settlement. Most student loans, certain tax debts, and criminal fines also carry significant restrictions under federal bankruptcy law (11 U.S.C. § 523).

What are the 11 words to stop a debt collector?

The phrase is: "Please cease and desist all calls and contact with me immediately." Sending this in writing invokes your rights under the Fair Debt Collection Practices Act, requiring the collector to stop contacting you. The debt itself, however, remains owed.

What happens to my escrow funds if I cancel?

Unearned deposits belong to you and must be returned within 7 business days under the FTC's Telemarketing Sales Rule. Fees already earned from previously completed settlements are not refundable. If the company refuses to return eligible funds, file a complaint with the FTC or your state attorney general.

Can I negotiate with my creditors directly after canceling?

Yes. Creditors often prefer direct communication and may offer a payment plan or reduced settlement, especially when you can demonstrate financial hardship and a clear intention to repay. Contact each creditor proactively rather than waiting for them to escalate.