How to Get Out of Mortgage Debt Strategies

Transform Your Financial Future

Contact UsMortgage debt becomes overwhelming faster than most homeowners expect. A job loss, a medical crisis, or a rate adjustment can turn a manageable payment into an impossible one — and the pressure compounds every month you wait.

According to the Mortgage Bankers Association's Q4 2024 National Delinquency Survey, 3.98% of residential mortgage loans were delinquent at year-end 2024, with FHA loans hitting 11.03%. That's millions of households navigating the same stress you may be facing right now.

The good news: there are legal, proven strategies to get out from under mortgage debt without losing everything. This guide walks through your options — from temporary relief like forbearance to permanent exits like short sales — and explains which strategy fits which situation.

Key Takeaways

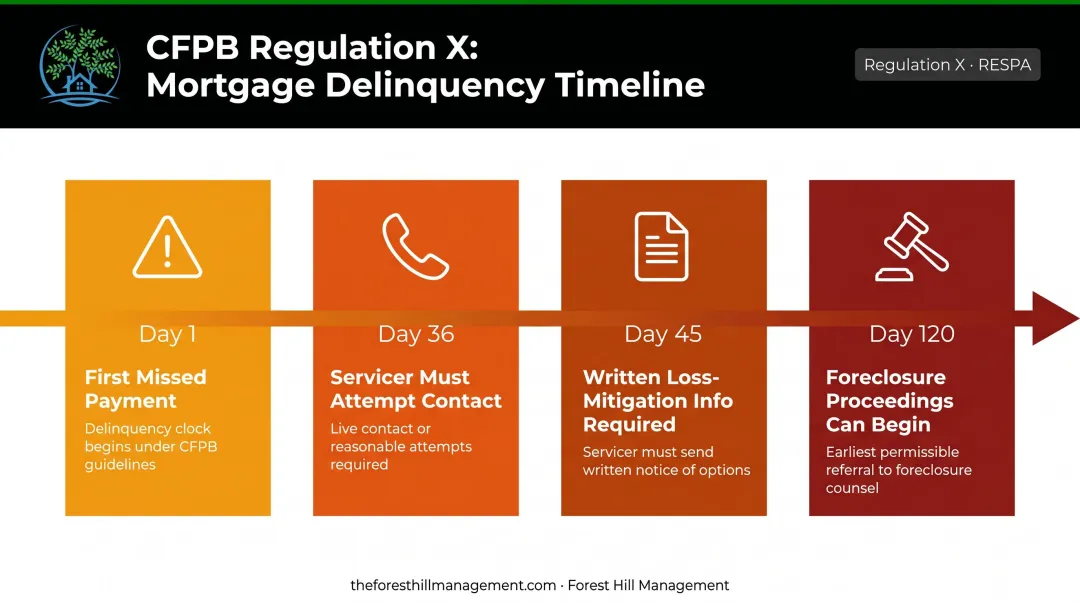

- Contact your mortgage servicer before day 120 of missed payments, when foreclosure proceedings can legally begin

- Forbearance pauses payments temporarily; loan modification changes them permanently — they solve different problems

- 47.7% of mortgaged U.S. homes were equity-rich in Q4 2024, meaning selling may be a realistic exit for many homeowners

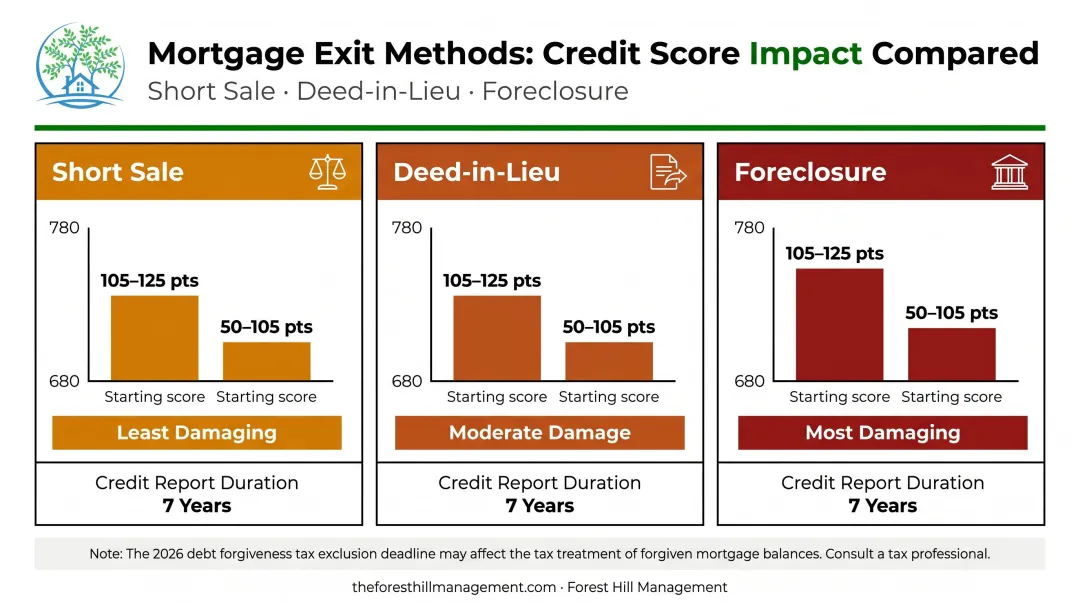

- Forgiven mortgage debt on a principal residence may be excluded from taxable income through January 1, 2026 (up to $750,000)

- Short sales and deed-in-lieu arrangements still damage credit; neither is a credit-neutral alternative to foreclosure

How to Get Out of Mortgage Debt: A Step-by-Step Approach

Step 1: Contact Your Mortgage Servicer Immediately

This is not optional advice — it's the single most consequential action you can take.

Under CFPB Regulation X (12 CFR 1024.41), servicers generally cannot initiate the first foreclosure notice or filing until a mortgage is more than 120 days delinquent. Many servicers are also required to attempt contact by day 36 and provide written loss-mitigation information by day 45. Acting early keeps every option on the table. Waiting shrinks them fast.

Before you call, prepare:

- Two recent pay stubs or current proof of income

- Two to three months of bank statements

- A clear description of your hardship — and whether it's temporary or permanent

- A full list of monthly expenses and liabilities

Be honest about your situation. Lenders distinguish between a short-term income gap and a permanent income reduction — the distinction directly affects which programs they'll offer you.

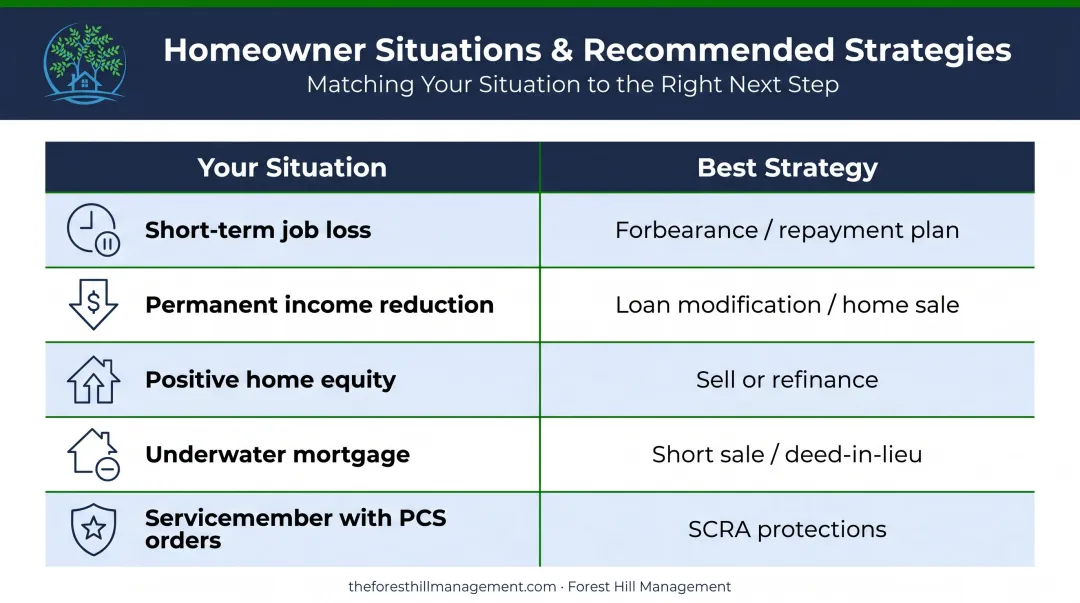

Servicemembers note: If you have PCS orders or are on active duty, the Servicemembers Civil Relief Act (SCRA) provides a 6% interest-rate cap on pre-service mortgage obligations and restricts nonjudicial foreclosure during service and for one year after. These are protections most civilian borrowers don't have access to — use them.

Step 2: Request Forbearance or a Loan Modification

These two options serve different purposes.

Forbearance is a temporary pause or reduction in payments. The debt isn't erased; it's deferred, typically added to the end of the loan or repaid through a repayment plan. It's the right tool for short-term hardship: a layoff, a medical leave, a gap between jobs.

COVID-era data from the Urban Institute shows that of 8.8 million borrowers who entered forbearance, 47% were performing and 38% had fully paid off their loans by February 2024. Forbearance works when it's the right fit.

Loan modification is a permanent restructuring of your mortgage terms. The lender may reduce your interest rate, extend your repayment period, or in some cases reduce the principal. This is appropriate for permanent income reduction or chronic unaffordability. Lenders typically require:

- A completed mortgage assistance application (Fannie Mae and Freddie Mac use Form 710)

- Documentation of financial hardship and income/expenses

- Evidence that you cannot sustain current payments long-term

Neither option erases the debt. Both require lender approval. And both can have credit implications depending on how your servicer reports the arrangement.

Step 3: Refinance or Sell the Home

When forbearance and modification aren't the right fit — or when you're ready to move on — refinancing and selling are the next tier of options.

Refinancing makes sense when you have equity and stable (but changed) finances. The goal is a lower monthly payment or shorter payoff term. Fannie Mae's minimum representative credit score for delivered loans is 620, with LTV ratios up to 97% for a 1-unit principal residence limited cash-out refinance. FHA Streamline options exist for borrowers with existing FHA loans, with credit-qualifying and non-credit-qualifying paths available.

Borrowers with very low credit scores and no equity will typically not qualify for refinancing. In those cases, selling or renting may be the more realistic path.

Selling the home is the cleanest exit when your property has sufficient equity to cover:

- The outstanding mortgage balance

- Agent commissions and closing costs (Zillow estimates sellers typically pay 8%–10% of sale price in total costs)

- Any remaining liens

When the math works, proceeds satisfy the loan in full. No lingering debt, no credit damage from default.

Renting the home is worth considering if rental income can cover the mortgage payment and you can relocate affordably. It's not a long-term solution for everyone, but it buys time while property values recover.

Step 4: Pursue Short Sale, Deed-in-Lieu, or Formal Debt Forgiveness

When the home is worth less than you owe and other options have failed, these are your paths out.

Short sale: The lender agrees to accept less than the full mortgage balance as payment in full. This requires lender approval, and state laws determine whether you're still liable for the remaining deficiency.

Several states (including California, Arizona, Oregon, and Washington) offer meaningful anti-deficiency protections for purchase-money mortgages, but rules vary by foreclosure method, property type, and whether the loan was refinanced. Verify your state's specific statute before proceeding.

Deed-in-lieu of foreclosure: You voluntarily transfer ownership to the lender in exchange for release from the mortgage obligation. Fannie Mae's requirements include a completed hardship evaluation, property valuation, clear and marketable title, and subordinate lien releases. If your non-retirement cash reserves exceed $10,000, a cash contribution may be required.

Tax implications: IRS Publication 4681 confirms that under the Mortgage Forgiveness Debt Relief Act, qualified principal residence indebtedness can be excluded from taxable income for discharges before January 1, 2026, up to $750,000 (or $375,000 if married filing separately). The debt must have been used to buy, build, or substantially improve your main home. This exclusion does not apply to second homes or investment properties. Consult a tax professional before finalizing any forgiveness arrangement, particularly given the 2026 expiration date.

When Each Strategy Makes Sense

No single approach works for every homeowner. Your best option depends on the severity and duration of your hardship and whether your goal is to stay in the home or exit cleanly.

The table below matches common situations to their most effective strategy:

One critical distinction to understand before choosing a path: recourse vs. non-recourse loans. In non-recourse states, lenders can generally only seize the home as collateral — they can't pursue your other assets after a short sale or foreclosure. In recourse states, lenders can pursue a deficiency judgment against you. Rules vary by state, loan type, and foreclosure method. Confirm your state's deficiency laws with a licensed attorney before committing to any liquidation strategy.

What You Need Before Pursuing Any Strategy

Preparation directly affects how quickly lenders respond and which programs they'll offer. Missing documentation delays relief — sometimes long enough to close off options entirely.

Financial Documents to Gather

- Two recent pay stubs or alternative proof of income

- Two to three months of bank statements

- Two years of tax returns

- A complete list of monthly expenses and outstanding liabilities

Hardship Letter Requirements

A vague hardship letter gets deprioritized or rejected. An effective letter:

- States the specific cause of financial difficulty (job loss, illness, divorce, disability)

- Provides a clear timeline of when the hardship began

- Details steps already taken to manage the situation

- Explains whether the hardship is temporary or permanent

Professional Guidance

Don't navigate this alone. HUD-approved housing counselors provide free assistance to homeowners with mortgage payment problems — you can find one through HUD's official counselor directory or by calling 800-569-4287.

Mortgage relief is only part of the picture. If you also have past-due accounts — credit cards, medical bills, personal loans — those affect your debt-to-income ratio and can directly limit your eligibility for a loan modification or refinance. If any of those accounts are already being managed by a receivables company like Forest Hill Management, resolving them proactively gives you a stronger profile when approaching your mortgage servicer.

Common Mistakes When Trying to Exit Mortgage Debt

Waiting Too Long to Act

Foreclosure proceedings can legally begin 120 days after a missed payment. The earlier you contact your servicer, the more options remain available. ATTOM data shows properties in foreclosure in Q2 2024 had been in the process an average of 815 days — but that clock starts with an initial missed payment you may still be able to address.

That urgency also makes homeowners a target. When you're desperate for a solution, predatory "relief" services step in — which is why knowing the red flags matters.

Falling for Mortgage Relief Scams

Red flags to watch for:

- Upfront fees demanded before any help is provided

- Guarantees of loan modification approval

- Instructions to stop paying your servicer and send payments elsewhere

- Requests to sign over your property title to a third party

HUD-approved counseling is free. Legitimate lenders and servicers will never ask you to transfer your title. Report suspected scams to the CFPB at consumerfinance.gov/complaint.

Ignoring Tax and Credit Consequences

- Tax risk: Forgiven debt may be taxable, particularly if the current exclusion isn't extended past January 1, 2026. Speak with a tax professional before accepting any forgiveness arrangement.

- Credit damage: Short sales and deed-in-lieu arrangements can reduce a 780 credit score by 105–125 points and a 680 score by 50–105 points according to FICO research. These events typically remain on credit reports for 7 years. They're less damaging than foreclosure overall, but expect significant credit impact either way.

Frequently Asked Questions

Can mortgage debt be forgiven?

Yes. Lenders may forgive partial or full balances through loan modifications, short sales, or deed-in-lieu arrangements. Under current IRS rules, up to $750,000 of forgiven debt on a principal residence can be excluded from taxable income for discharges before January 1, 2026. Consult a tax professional before relying on this exclusion.

What happens if I stop paying my mortgage?

Missed payments trigger late fees, credit score damage, and eventually foreclosure proceedings, which can begin as early as 120 days after the first missed payment. In recourse states, lenders may also pursue a deficiency judgment for any remaining balance after the home sells.

How does loan modification work?

A loan modification permanently restructures your mortgage terms, such as reducing the interest rate, extending the loan term, or cutting the principal balance. It requires lender approval, financial documentation, and proof of hardship.

Is refinancing a good way to reduce mortgage debt burden?

Refinancing can lower monthly payments or secure a shorter payoff period, but it requires qualifying for a new loan. That means sufficient credit score (Fannie Mae's minimum is 620), income stability, and home equity. Severely distressed borrowers typically won't qualify.

What is the difference between forbearance and a loan modification?

Forbearance temporarily pauses or reduces payments; the full debt remains and is typically added to the end of the loan. A loan modification permanently restructures the loan's terms. Forbearance addresses short-term gaps, while modification addresses long-term unaffordability.

Will getting out of my mortgage hurt my credit score?

It depends on the method. Selling with sufficient equity and no missed payments has minimal impact. Short sales, deed-in-lieu, and foreclosure can significantly damage your score and remain on your credit report for seven or more years, with any deficiency balance compounding the damage.