How to Manage Debt While Investing for Future Growth

Transform Your Financial Future

Contact UsMany Americans find themselves stuck at the same crossroads: they know they should be investing, but carrying debt makes it feel irresponsible — or even impossible — to put money into the market. That tension is real, but it's based on a false choice.

The truth is that paying off debt and building wealth aren't mutually exclusive. For most people, the smartest path forward involves doing both at once — not waiting until every balance hits zero before opening a brokerage account. This guide walks through exactly how to think about that balance, when to lean one way versus the other, and how to build a strategy that works for your specific situation.

Key Takeaways

- Build at least a small emergency fund before aggressively attacking debt or investing

- Always capture your full employer 401(k) match — free money that instantly boosts your return

- High-interest debt (generally above 6%) should take priority over extra investing contributions

- Mortgages, federal student loans, and similar lower-rate debt can coexist with an active investment strategy

- Automate both: minimum debt payments and retirement contributions can run simultaneously

- The best financial plan is one you'll actually stick to — your stress tolerance matters as much as the math

Lay the Financial Foundation Before You Start

Before deciding how to split extra dollars between debt and investments, two foundational steps come first — and skipping either will undermine everything else.

Build a Starter Emergency Fund

Without a cash cushion, any unexpected expense forces you back into debt, erasing progress on both goals. Fidelity recommends starting with $1,000, then building toward 3–6 months of essential expenses. Vanguard uses the same 3–6 month benchmark for income shocks.

If you're carrying high-interest debt, don't wait until you have a full six-month reserve. A $1,000–$2,000 starter fund is enough to get moving.

Never Miss a Minimum Payment

This isn't optional. Missing payments triggers late fees, accelerates interest compounding at penalty rates, and damages your credit score — which then raises borrowing costs on everything else. According to the Federal Reserve's 2024 household finance report, 23% of U.S. adults had debt in collections as of 2024.

If you're among those with past-due accounts, resolving them is a financial priority. Organizations like Forest Hill Management can help set up structured payment plans that let you address outstanding balances without putting your other financial goals on hold. Getting those accounts current creates the stable footing you need before directing any extra dollars toward investing.

Capture Your Full Employer 401(k) Match

If your employer matches 401(k) contributions and you're not taking full advantage of it, you're leaving free money on the table. A 2015 Financial Engines study estimated that 1 in 4 employees missed their full match, leaving an average of $1,336 per year uncaptured. No debt payoff strategy delivers a guaranteed 50–100% immediate return — which is effectively what an employer match provides.

Contribute at least enough to capture the full match before directing any extra dollars toward debt payoff or additional investing.

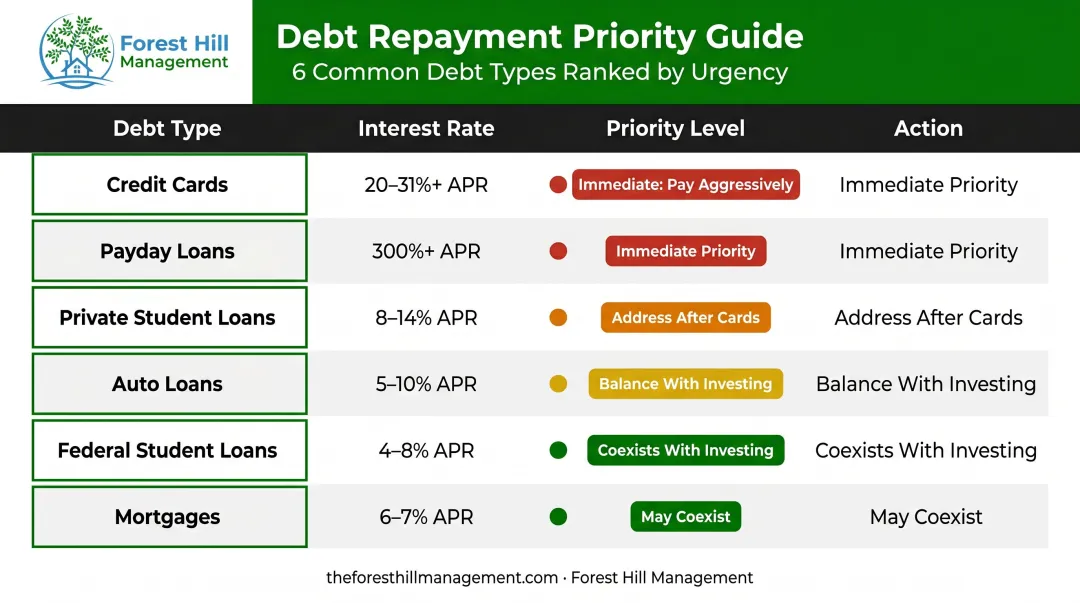

Not All Debt Is Equal: Understanding What You Owe

Debt type matters more than debt total. A $30,000 mortgage and a $30,000 credit card balance carry vastly different costs, risks, and repayment urgency.

High-Interest vs. Low-Interest Debt

The CFPB's 2024 credit card market report found that average APRs hit 25.2% for general-purpose cards and 31.3% for private-label cards. At those rates, minimum payments barely dent the principal.

The Real Cost of Minimum Payments

Using the CFPB's 25.2% average APR, a $5,000 credit card balance paid with minimums only looks like this:

Minimum payments are not a payoff plan.

The Tax Deductibility Factor

Some debt is partially tax-deductible, which effectively lowers its true cost:

- Mortgage interest: Deductible on up to $750,000 of qualifying debt (2025 limits)

- Student loan interest: Up to $2,500 deductible, phasing out at $85,000–$100,000 MAGI for single filers

Tax deductibility changes the math. On a 6% deductible mortgage, the after-tax cost may drop closer to 4.5%, which often makes investing the better financial move over prepaying. Consult a tax professional for your specific situation.

How to Decide: When to Prioritize Debt Payoff vs. Investing

The core decision-making framework comes down to one question: does your debt cost more than your investments could reasonably earn?

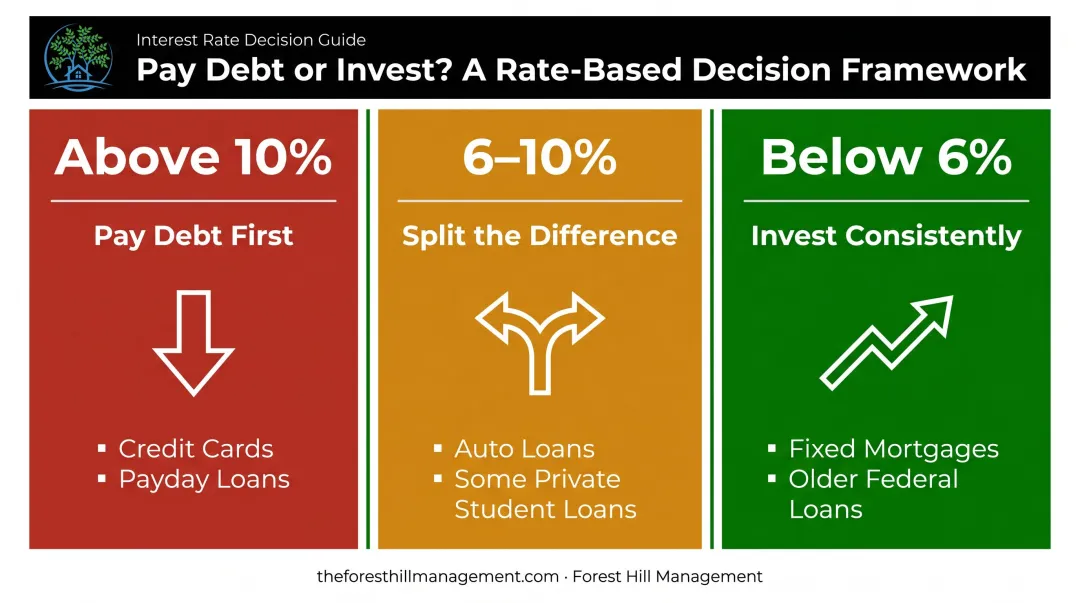

The 6% Threshold Rule

Fidelity uses 6% as the key benchmark: if a debt's interest rate exceeds 6%, directing extra dollars toward payoff typically beats investing more. If the rate falls below 6%, investing may produce better long-term outcomes.

Think of it as a practical sorting tool, not a hard rule. Apply it to extra dollars only — after minimums are paid, your emergency fund is established, and any employer match is captured.

Three-Scenario Decision Model

High-rate debt first (above 10%): Credit cards, payday loans, high-rate private debt. No investment return reliably beats eliminating these.

Invest consistently (below 6%): A 3% fixed mortgage or older federal student loans at 4–5%. The math favors keeping steady investment contributions.

Split the difference (6–10%): Moderate auto loans or some private student loans. Divide extra dollars between accelerated payoff and investing based on your risk tolerance and time horizon.

These scenarios give you a starting point. Where the decision gets more nuanced is when time itself becomes part of the equation.

Why Starting Early Matters So Much

Time horizon changes everything. Fidelity estimates that saving 15% annually starting at age 25 should be enough to fund retirement, but waiting until age 30 raises the required savings rate to 18%. A five-year delay costs you meaningfully — both in compounding growth and in the higher savings rate needed to compensate.

A 35-year-old has 30 years of compounding ahead. That length of runway makes early investing extremely powerful, even alongside moderate-rate debt.

How to Manage Debt and Invest at the Same Time

Running both strategies in parallel is not only possible — it's often the smarter move than waiting until debt is fully paid off.

Choose Your Debt Payoff Method

Two proven approaches dominate the debt payoff conversation:

Debt Avalanche: Pay minimums on all balances, then direct extra cash to the highest-interest debt first. This minimizes total interest paid over time. It works best for disciplined savers who want the mathematically optimal outcome.

Debt Snowball: Pay minimums everywhere, then target the smallest balance first. Kellogg School of Management research found that consumers who attacked small balances first were more likely to eliminate their overall debt — visible progress improves follow-through. It works best for anyone juggling multiple small accounts or who needs motivational wins.

Either method pairs well with an active investing strategy.

Automate Everything

Automation removes the decision friction that causes people to neglect one goal or the other. Set up:

- Automatic minimum (or above-minimum) payments on all debts

- Automatic contributions to your 401(k) or IRA each paycheck

Research from Chicago Booth found that automatic savings escalation raised retirement savings rates from 3.5% to 13.6% over 40 months. When the process runs in the background, both goals stay on track without relying on monthly willpower.

Use Tax-Advantaged Accounts While Paying Debt

Contributing to retirement accounts while carrying debt is often the strategically sound move. For 2025:

- 401(k) elective deferral limit: $23,500

- Traditional/Roth IRA combined limit: $7,000 ($8,000 if age 50+)

A $5,000 Traditional 401(k) contribution reduces your taxable income by $5,000 — translating to $1,100 in federal tax savings at a 22% marginal rate or $1,200 at 24%. That tax reduction effectively lowers the cost of investing, making it more competitive with debt payoff even at moderately high interest rates.

Handle Windfalls Strategically

Tax refunds, bonuses, and unexpected income are high-leverage moments. Rather than sending 100% to debt or 100% to investments, consider a split:

- Allocate 60–70% toward high-interest debt

- Direct the remainder into your investment account

This keeps momentum on both goals without forcing you to treat them as competing priorities.

The Psychological Side of Debt and Investing

Personal finance is emotional, not just mathematical. A 2025 Bankrate survey found that 43% of U.S. adults say money negatively affects their mental health at least occasionally. Debt is a significant driver of that stress.

When the Suboptimal Math Is Still the Right Choice

Sometimes paying off a low-interest loan ahead of schedule — even when the numbers favor investing — is still the right decision. If carrying a balance causes enough anxiety to disrupt your sleep, relationships, or overall decision-making, eliminating it frees up mental energy that can be redirected toward building wealth. The best financial plan is the one you can stick to for 20 years, not the one that looks best on a spreadsheet.

Build Momentum With Milestones

Small wins reinforce the behaviors that lead to long-term success. When you:

- Pay off a single credit card balance

- Hit a specific savings threshold

- Reach a positive net worth for the first time

Acknowledge it. These moments aren't just psychological boosts. They're proof that the strategy works, which builds the discipline needed to push through the longer, slower stretches between wins.

For consumers managing past-due accounts alongside these goals, that clarity matters even more. Forest Hill Management offers flexible payment plans and structured account resolution to help reduce financial stress and create a more manageable path forward.

Frequently Asked Questions

Should I pay off debt before investing for retirement?

You don't need to be completely debt-free before investing for retirement. Capture any employer match immediately, then prioritize high-interest debt (above ~6%) over extra investing. Lower-rate debt can typically coexist with consistent retirement contributions.

What is the 7-5-3-1 rule in investing?

The 7-5-3-1 rule originates from Indian mutual fund (SIP) contexts and has no recognized U.S. regulatory or major brokerage equivalent. For U.S. investors, it's best treated as a loose framework rather than an authoritative guideline.

What are the 5 C's of credit?

The 5 C's are Character (repayment history), Capacity (ability to repay), Capital (assets or reserves), Collateral (pledged assets), and Conditions (loan purpose and broader circumstances). Lenders use these to assess creditworthiness — understanding them helps you see how carrying and resolving debt affects your future borrowing terms.

What is the 7-7-7 rule for debt collectors?

Under CFPB Regulation F (effective November 2021), a debt collector is presumed to violate the law if it calls a consumer more than 7 times within 7 consecutive days about a particular debt, or calls within 7 days after a phone conversation about that debt. Knowing this rule helps you recognize when contact frequency may be improper.

How do I invest while paying off student loans?

Federal student loans typically carry lower interest rates, making it reasonable to invest simultaneously — especially in a 401(k) or Roth IRA. Income-driven repayment (IDR) plans can lower monthly payments based on income and family size, freeing up additional cash flow for investing while keeping loan payments current.

What is the difference between the debt avalanche and debt snowball method?

The avalanche targets the highest-interest balance first, minimizing total interest paid. The snowball targets the smallest balance first, generating faster psychological wins. Both can run in parallel with an investment strategy. The right choice depends on whether your bigger challenge is math optimization or staying motivated.