Pay Recovery Guide: Resolve Debts Before They Escalate

Need Help Reviewing Your Account?

Contact UsMissed payments don’t fail loudly. They sit quietly in your day, pulling attention, shaping decisions, and creating a steady background tension you can’t fully switch off.

That strain is common, not personal failure. Data shows 42% of Americans feel worried about credit card debt, yet uncertainty about next steps keeps that worry unresolved.

This is where payment recovery enters, not as punishment, but as a structured response to bring order back into a stalled financial moment. It exists to replace guessing with process, so unresolved balances move forward instead of lingering in silence.

In this article, you’ll see how the payment recovery process works, the strategies behind it, and how early, informed action shapes better financial outcomes.

Key Takeaways

- Acting early gives you better control, helping reduce credit damage and avoid legal actions like wage garnishment.

- Creditors use various strategies, such as automated reminders and repayment options. Understanding these helps you respond more effectively.

- Propose payment plans or settlements early to secure better terms before debt escalates.

- Keep communication open with creditors to avoid misunderstandings and keep options flexible.

- Seeking professional advice can help you create a manageable plan, reducing stress and improving recovery outcomes.

What Payment Recovery Actually Means

Payment recovery is the system that creditors use to reclaim unpaid debts through structured methods. This includes automated reminders, direct contact, negotiation, and, when necessary, legal measures.

For creditors, it's about recovering what's owed while maintaining customer relationships. For you, it's a framework that turns financial ambiguity into clarity, even when that clarity feels uncomfortable.

Understanding what drives this process means you can manage it with intention rather than react to it in panic.

How the Payment Recovery Process Works

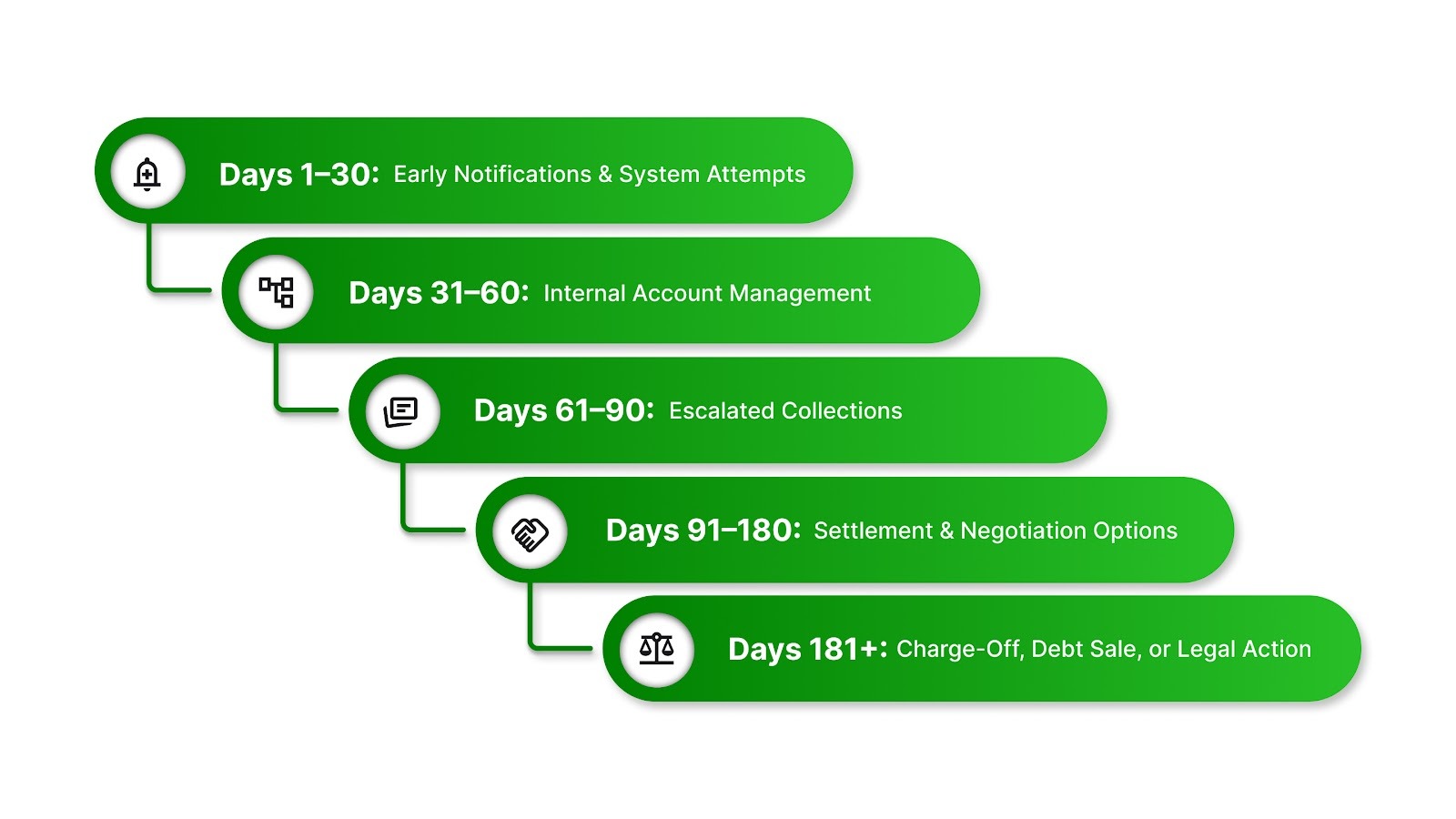

Payment recovery follows a predictable sequence, starting gently and escalating only when earlier steps fail. Each stage is designed to offer you a chance to resolve the debt before consequences intensify.

Days 1-30: Early Notifications and System Attempts

If a payment is missed, lenders usually send reminders and may retry automatic payments, but short-term delinquencies are rarely reported to credit bureaus immediately.

Days 31-60: Internal Account Management

Accounts may be flagged as delinquent, contact from the lender becomes more frequent, and options like payment plans or temporary relief may be offered; credit reporting can begin.

Days 61-90: Escalated Collections

Unpaid accounts may go to internal collections or external agencies, contact intensifies, and credit bureaus are usually notified if not already; collectors must follow legal rules.

Days 91-180: Settlement and Negotiation Options

Lenders may offer settlements or modified repayment terms; negotiation leverage increases with time, but non-response doesn’t automatically trigger legal action.

Days 181+: Charge-Off, Debt Sale, or Legal Action

Debts may be charged off or sold to third-party collectors, and legal action is possible but requires a court judgment; resolution can become more complex, but it isn’t guaranteed.

Also Read: 10 Successful Debt Collection Techniques for Maximizing Success

With this understanding of the recovery process, it’s important to recognize the strategies creditors use at each stage to move the process forward.

10 Common Payment Recovery Strategies Companies Use

Recovery teams follow data-driven tactics, focusing on response likelihood, cost efficiency, and legal risk. Their approach is systematic, not personal, helping you see debt collection as a set of predictable moves you can plan around.

Here’s a closer look at the common recovery strategies used by companies to encourage repayment.

1. Behavioral Nudges

Creditors schedule calls, emails, or letters when you’re most likely to notice, like early mornings or payday weeks. Frequent reminders are strategic, keeping the debt visible without crossing legal boundaries, subtly encouraging action.

2. Settlement Window Leverage

Settlement offers reflect calculated risk, not generosity. A 40-70% discount often appears when full repayment seems unlikely, framing the option as “saving money” to increase your acceptance.

3. Credit Reporting Enforcement

Reporting to credit bureaus costs little and works automatically. The impact on your score motivates repayment by creating real consequences in borrowing, renting, or financial opportunities.

4. Agency Outsourcing

When accounts are transferred or assigned to agencies, collection approaches may change depending on how the account is managed. While this can give you leverage in negotiations, agency tactics may feel more persistent.

5. Payment Plan Management

Installment plans convert uncertain debt into predictable income for creditors. Automatic payments reduce missed deadlines, and minor fee reductions cost little yet increase the chances of recovery, making it easier for you to stay on track.

6. Automated Reminders

Automation keeps recovery low-cost and unobtrusive. Emails, texts, or app notifications remind you of due payments, and systems can retry transactions automatically to catch moments when funds are available.

7. Multi-Channel Outreach

If automation fails, creditors expand across calls, letters, emails, and even social media. Persistent, multi-channel communication increases the chance you’ll respond without harassment.

8. Lump-Sum Settlement Discounts

Partial payment offers prioritize immediate recovery over chasing full amounts. Settling at a reduced rate clears your debt while still impacting your credit less severely than leaving it unpaid.

9. Flexible Repayment Plans

Installment options help you pay over time with reduced interest or fees. Structured plans increase the likelihood that creditors recover the full balance, while giving you breathing room to manage payments within your budget.

10. Credit Bureau Motivation

The threat of damage to credit scores is a powerful motivator. Reporting delinquent accounts nudges you to act before borrowing, housing, or employment opportunities are affected, increasing urgency without direct pressure.

Also Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2026 Update)

Now that you understand how recovery teams operate, the next step is to learn how to respond effectively to regain control of your payments.

Effective Strategies for Managing Payment Recovery

Even in recovery, taking action gives you more control than waiting. Successful strategies focus on engagement, not avoidance, and aim to resolve debt while limiting further impact. Let’s explore how you can take control of the recovery process:

- Verify the Debt: Always confirm the debt is accurate before paying. Request written validation within 30 days to protect yourself from errors or already-paid balances.

- Communicate Proactively: Respond to calls or letters, even briefly. Engaging shows responsibility, keeps negotiation doors open, and reduces the chance of aggressive action.

- Engage Early: Ask about available repayment arrangements before the account escalates.

- Use Secure Online Payments: Web portals allow one-time or recurring payments, provide digital records, and simplify disputes, giving you control and security over transactions.

- Seek Support When Needed: Qualified professionals can help explain options and processes related to managing overdue accounts.

Following these strategies is important, yet the difference between stress and progress often comes down to timing.

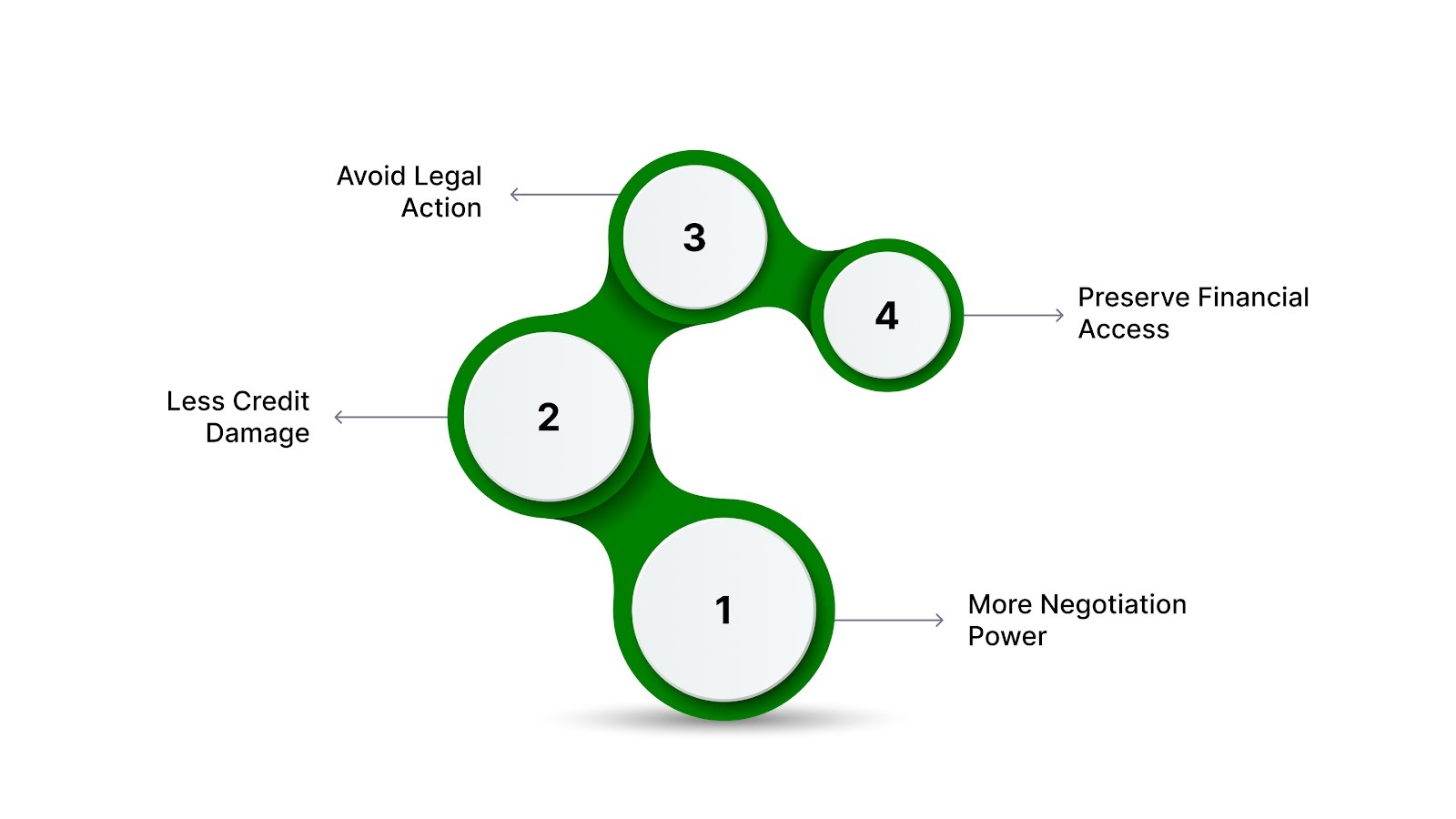

Why Early Action Leads to Better Outcomes

Timing is critical in payment recovery. Acting early, before your debt reaches 90-120 days, gives you more control, better options, and less damage. The longer you wait, the more expensive and complex the resolution becomes.

Here's how acting early can help:

- More negotiation power: Original creditors offer more flexibility within the first 60 days. After that, you're a recovery target.

- Less credit damage: A 30-day late payment can be fixed; delays past 90 days hurt your score significantly.

- Avoid legal action: Engaging early prevents lawsuits, garnishments, and extra legal fees.

- Preserve financial access: Unresolved debts block credit, housing, and job opportunities.

Also Read: Consumer Impact Recovery and Debt Collection Guide

Now that you understand the importance of acting early, let’s explore how Forest Hill Management can assist you in managing the recovery process with clarity, flexibility, and support.

How Forest Hill Management Supports Payment Recovery

If you're ready to address an overdue balance, Forest Hill Management makes the recovery process more manageable. We know that missing payments doesn't mean you want to avoid responsibility; it often means you need a plan that actually works.

Here's how we help you move forward:

- Use our secure online platform to make payments instantly from anywhere, at any time that fits your schedule

- Work with our support team to understand and manage available repayment arrangements

- Taking timely action helps clarify options and reduce uncertainty around next steps.

- Get clear answers about your account, payment history, and next steps without confusing jargon or runaround

By addressing overdue balances early, you can avoid complications, restore financial stability, and regain peace of mind, all without the usual hassle.

Conclusion

The road to resolving overdue balances doesn’t need to be daunting. Early action is your most powerful tool in regaining control, allowing you to reduce stress, explore options, and take meaningful steps forward. Proactively managing your debt means fewer surprises and more opportunities to shape your financial future on your terms.

At Forest Hill Management, we understand the weight that comes with overdue payments. That's why we offer clear, structured account management to help you navigate these challenges, providing clarity and support when you need it most. Let’s work together to transform uncertainty into a plan that fits your life.

Take the first step toward resolving your debt today. Contact Forest Hill Management to explore flexible repayment options and find a plan that works for you.

FAQs

1. Can cancelled or settled debt trigger income tax liability?

Yes. Forgiven debt is generally taxable in the U.S., reported on Form 1099‑C, unless you qualify for exclusions like bankruptcy or insolvency.

2. Are payment recovery processes different for medical versus credit card debt?

Yes. While credit card debts often follow structured escalation and legal channels, medical debts may involve additional protections, such as insurance negotiations, charity care, or state-specific billing regulations.

3. How do debt settlement companies differ from creditor-initiated recovery?

Debt settlement companies negotiate on your behalf for a fee, whereas creditor-initiated recovery is managed internally or through collection agencies.

4. Can bankruptcy stop payment recovery actions immediately?

Filing for bankruptcy triggers an automatic stay, which temporarily halts most collection activities, including legal actions and wage garnishments. However, certain debts (like taxes or secured loans) may not be fully protected, and the long-term credit impact of bankruptcy is significant.

5. How do state laws influence payment recovery tactics?

Each state has specific regulations on how and when creditors can contact you, the maximum allowable interest rates, statute of limitations on debt collection, and legal remedies. Understanding your state’s laws can help you recognize your rights and spot illegal collection practices.