From Debt to Direction: Finance for Future Planning

Transform Your Financial Future

Contact UsFinding your financial footing after dealing with debt can feel overwhelming, but it is also one of the most powerful turning points in your life. According to the Fed’s Household Debt and Credit data, U.S. consumer debt recently reached $18.59 trillion (Q3 2025).

Yet behind every balance lies an opportunity to pause, plan, and build a future that feels stable and within reach. Moving from debt to direction is not about overnight change; it is about learning how to make clear, intentional financial choices that work for you.

With the right mindset, realistic goals, and a supportive plan, you can shift from reacting to confidently shaping your finances for the future. This guide will walk you through practical steps, strategies, and small wins to turn financial stress into steady progress.

Before we begin:

- Planning your finances gives you direction. It helps you move from short-term debt management to long-term stability by setting realistic goals that fit your current situation.

- Paying down debt consistently builds momentum. Each on-time payment reduces stress, improves your credit profile, and brings you closer to financial freedom.

- Small financial goals create lasting habits. Building an emergency fund, budgeting monthly, or saving modestly can strengthen your confidence and resilience over time.

- Mindset matters as much as money. Shifting from financial stress to planning helps you see debt as something manageable, not permanent.

- Progress is built on steady actions. Reviewing your finances, adjusting as needed, and staying patient with your plan make financial direction achievable for anyone.

Should You Really Plan for Your Financial Future?

“Americans are paying exponentially more to carry ... balances, with millions of cardholders paying hundreds or even thousands of dollars in extra interest each year.” (CBS News)

That reality might sound discouraging, but it is actually a reminder of why financial planning matters so deeply. When you have a plan, debt no longer feels like a permanent obstacle.

Everyone’s financial goals look different, but most fall into a few simple categories:

- Short-Term Goals: Paying off a small loan, setting aside an emergency fund, or catching up on overdue bills.

- Mid-Term Goals: Saving for a car, improving your credit score, or building a cushion for unexpected expenses.

- Long-Term Goals: Buying a home, planning for retirement, or reaching financial independence.

Each goal gives you something to aim for. A sense of progress that can feel deeply empowering, especially after periods of financial stress.

When you begin mapping your financial future, focus on direction rather than perfection. A plan does not need to be complicated or rigid; it just needs to help you move steadily toward stability and confidence.

In the following section, we look at the steps you can take to turn that plan into action.

Suggested Read: Essential Personal Finance Tips for Beginners

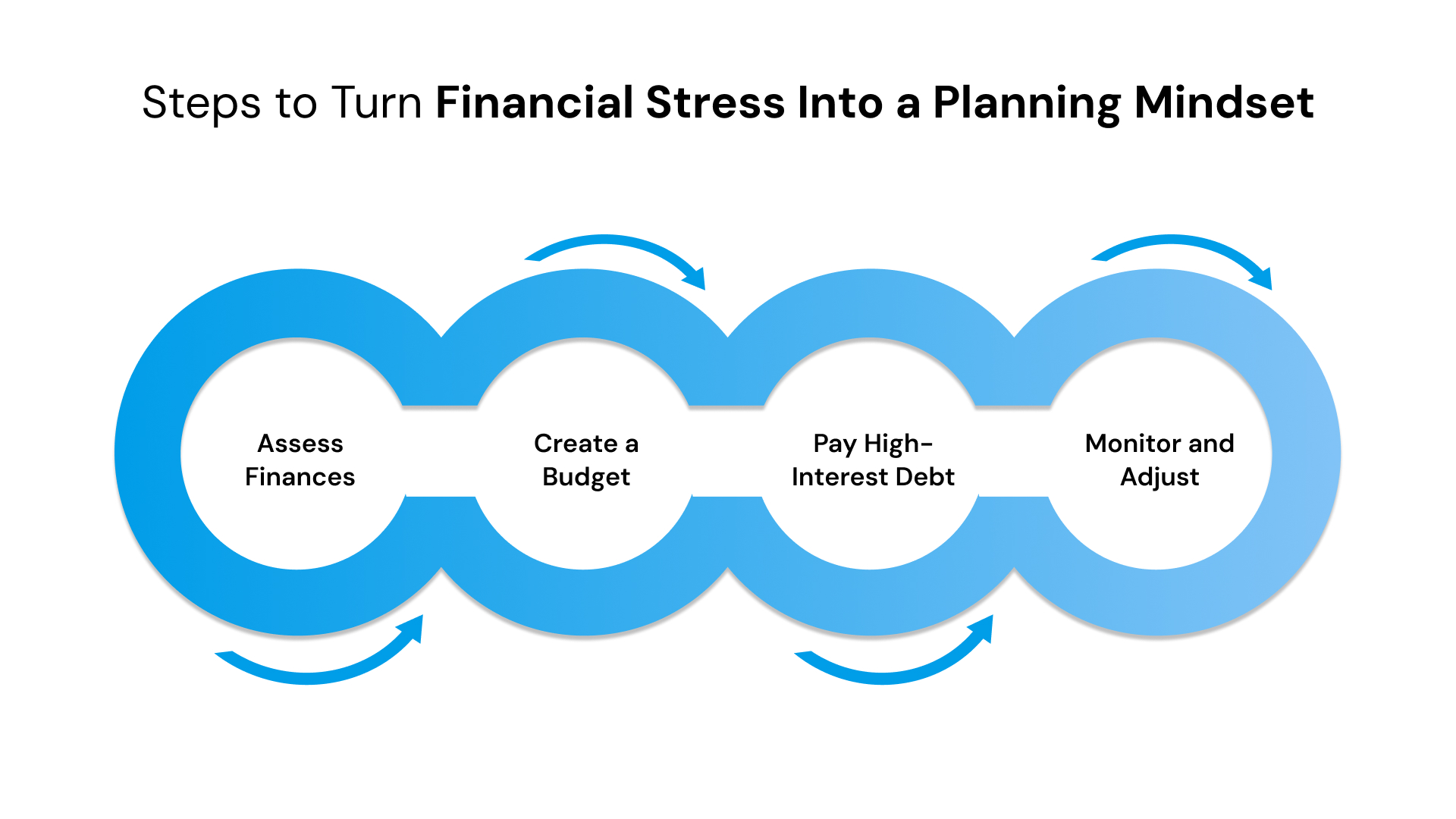

Steps to Turn Financial Stress Into a Planning Mindset

“You don’t have to see the whole staircase, just take the first step.” — Martin Luther King Jr.

When debt has weighed you down, shifting into a planning mindset is not about doing everything at once. It is about taking meaningful, consistent steps that give you control again.

With the right approach, you can reduce debt, rebuild confidence, and move from simply managing money to shaping your financial direction with purpose.

Step 1: Assess Your Current Finances Honestly

Before you plan what comes next, take a moment to understand where you stand. This step is all about gaining clarity and acknowledging your starting point.

Here is what you need to do:

- Write down all debt balances and interest rates so you know exactly what you owe.

- Track monthly income and expenses to see where your money truly goes.

- Identify any recurring expenses or subscriptions you can reduce or pause.

- Accept that you cannot change everything overnight — progress begins with awareness.

Step 2: Create a Simple, Realistic Budget

A budget is your foundation, not a restriction. It is a plan that helps you make thoughtful financial decisions.

This is what you need to do:

- Prioritize spending on essentials first, then repay debt, followed by savings or small goals.

- Set aside even a small amount for an emergency fund. Consistency matters more than size.

- Automate payments to avoid missed due dates and reduce stress.

- Review your budget monthly to see what worked and where you can adjust.

Step 3: Prioritize Paying Down High-Interest Debt

Debt reduction begins with focus. You need to target the right balance first to help you gain momentum more quickly.

Key points:

- Pay off debts with the highest interest rates first to save money over time.

- Continue paying minimums on other accounts to avoid penalties.

- Redirect money from cleared debts toward the next one — the “snowball” method builds motivation.

- Celebrate small wins since each cleared balance is proof that your plan is working.

Step 4: Monitor Progress and Adapt When Needed

Financial progress is rarely linear, but monitoring your journey helps you stay motivated and accountable.

This is what you need to focus on:

- At the month’s end, compare your actual spending and payments with your plan.

- Note what went well and what needs adjustment. This is how long-term habits form.

- Do not let setbacks discourage you; they are part of the process, not the end of it.

- Recognize progress often — small improvements are still forward motion.

The financial advisors at Forest Hill Management can help you stay organized and feel more in control. We offer secure online payments, flexible repayment options, and personalized communication to help you manage your balance confidently and without unnecessary stress. Speak to us today.

These steps can move you in the right direction, but there are also practical approaches you can use to strengthen your financial foundation even further.

Suggested Read: How to Diversify Your Income Streams Successfully

Smart Financial Strategies to Move Forward

The U.S. personal saving rate recently stood at approximately 4.6% of disposable income, indicating that many Americans are not saving enough for their future goals.

When you are ready to move from just making ends meet to building toward your goals, these strategies provide real-world, manageable steps.

These are a few effective strategies you can put in place:

- Automate Savings and Payments

Set up recurring transfers from your checking account to your savings, and automate debt payments so you never miss a due date. Automation removes stress and maintains consistent progress without requiring constant effort.

- Use the 50/30/20 Rule (or an Adjusted Model)

Allocate 50% of your income to essentials, 30% to discretionary wants, and 20% (or whatever amount fits your situation) toward savings or debt reduction. The percentages can flex. It is the habit that matters.

- Build an Emergency Fund First

Even a small cushion, like $500 to $1,000, can protect you from turning to credit cards or loans when unexpected expenses arise. Having that safety net gives you peace of mind.

- Redirect Windfalls Wisely

When you receive extra income such as a tax refund, bonus, or gift, use part of it to pay down debt or grow your savings instead of spending it all. Every dollar directed toward your goals shortens your path to stability.

- Review and Rebalance Regularly

Every few months, review your income, expenses, and savings progress. Adjust your budget or payment plans as life changes. Staying adaptable keeps you moving forward without feeling restricted.

These strategies can help you build a stronger foundation for your future. But even the best plan can face challenges. Let's discuss some common setbacks and how to stay on track when life throws you off balance.

Suggested Read: Effective Strategies For Credit Score Improvement

Common Setbacks and How to Stay on Track

“Thinking about the financial aspects of retirement can be overwhelming, so many people put it off.” — American Psychological Association

That is the first mistake people make — waiting too long to start. It is completely human to feel hesitant or unsure, especially when money already feels tight.

But financial stability does not come from having everything figured out; it comes from taking small, thoughtful actions even when it feels uncomfortable.

Here are a few other common setbacks that can quietly stall your progress:

- Avoiding Your Finances Altogether: It is easy to delay checking balances or opening statements when you are anxious about what you might find. But awareness is the first step toward change and not something to fear.

- Trying to Fix Everything at Once: When you attempt to pay off all debt, save, and invest simultaneously, burnout happens fast. Focusing on one realistic goal at a time keeps you moving steadily forward.

- Not Having a Safety Net: Without even a small emergency fund, one unexpected expense, such as a car repair or a medical bill, can undo months of progress. Building a small cushion protects you from that spiral.

- Comparing Yourself to Others: Everyone’s financial story looks different. Comparing your journey to someone else’s can lead to discouragement instead of motivation.

- Thinking Small Wins Do Not Matter: Paying off one credit card, saving $50, or sticking to your budget for a month are all milestones. Over time, these small wins compound into lasting financial strength.

The best way to stay on track is to treat your financial progress like a long walk, not a sprint. Check in with yourself regularly. Adjust when life changes. And most importantly, be patient. Progress built on consistency will always last longer than progress built on pressure. You are not falling behind; you are simply finding your pace.

Forest Hill Management supports that same steady progress. We help you manage your current accounts while staying focused on your financial future.

Suggested Read: Top 12 Proven Steps to Becoming Financially Stable

Forest Hill Management Can Help You Take the Next Steps

At Forest Hill Management, we understand that financial challenges can feel overwhelming — but you do not have to face them alone. We are a professional financial services organization that works with individuals to help them pay their debts.

Our approach combines personalized financial guidance, secure online repayment options, and a human touch that prioritizes respect, clarity, and progress over pressure.

Our advisors will take the time to understand your unique situation, then help you create a plan that works within your reality — one that balances repayment with planning.

Here is how we can help:

- Personalized Financial Advisory Support: Our team helps you review your repayment plan, identify the most manageable approach, and guide you through the process with compassion and transparency.

- Flexible Repayment Arrangements: We work with you to set up a payment schedule that aligns with your income and responsibilities, reducing stress and improving consistency.

- Secure Online Payment Options: Our digital platform allows you to make payments safely, quickly, and conveniently from wherever you are.

- Clear and Respectful Communication: You always know where your account stands — no confusion, no pressure, just open and honest updates.

- Commitment to Your Financial Confidence: Beyond account management, we help you develop stronger financial habits that support your long-term goals.

At Forest Hill Management, we believe financial recovery is about building direction, discipline, and confidence for the future. With every payment made and every step forward, you are creating space for the financial life you deserve.

Conclusion

Planning is one of the most freeing financial choices you can make. When you take time to organize your finances and pay your debts on time, you build a good credit history. Each consistent payment is a step toward financial independence, proving that stability grows through steady, intentional effort.

At Forest Hill Management, we help make that effort easier. Our team provides personalized financial advisory support, secure online payments, and flexible repayment options, allowing you to manage your debt with confidence. We focus on helping you move from financial stress to long-term direction — one practical step at a time.

Make a secure online payment or review your repayment options with our team. Contact us today.

Frequently Asked Questions

1. How Often Should I Review My Financial Plan?

It is best to review your financial plan at least every six months, or sooner if your income, expenses, or goals change. Regular check-ins help you stay aligned with your priorities and adjust before small issues grow into larger ones.

2. Can Paying Off One Debt Improve My Credit Score?

Yes. Paying off even one account reduces your credit utilization and strengthens your payment history — two major factors in your credit score. Over time, consistent payments across all accounts build lasting credit improvement.

3. What Should I Do If I Miss a Payment?

If you miss a payment, make it as soon as possible to minimize the impact. Contact your lender or servicer — including Forest Hill Management, if your account is placed with us — to discuss flexible repayment options that help you get back on track without unnecessary stress.

4. How Can I Stay Motivated When Progress Feels Slow?

Financial recovery takes time, and it is normal to feel discouraged along the way. Try tracking small wins — such as reducing a balance or sticking to your budget for a month — and remind yourself that steady progress is far more powerful than quick fixes.

5. What Resources Can Help Me Learn More About Managing Debt?

Trusted sources like the Consumer Financial Protection Bureau (CFPB), Experian, and Investopedia offer free educational tools and credit management guides. These resources can help you better understand how debt repayment, credit scores, and financial planning work together over time.