What Is Portfolio Analysis? How It Helps You Understand and Manage Your Debt

Transform Your Financial Future

Contact UsJuggling multiple debts can start to feel confusing when balances, due dates, and interest rates blur together without a clear picture. When money feels tight, uncertainty often creates more stress than the numbers themselves.

Portfolio analysis isn’t just an investment term; it’s a way to step back and understand how all your debts work together. Looking at your full debt picture helps you see where pressure builds, what truly costs you the most, and where change is possible.

In this article, you’ll learn what portfolio analysis means in a personal finance context, how it applies to your debts, and how it can guide smarter repayment decisions. With clarity, you can replace guesswork with structure and move forward with more confidence.

Let’s start by breaking down what portfolio analysis really means in simple, everyday terms.

Key Takeaways

- Portfolio analysis helps you understand all your debts together, not just one at a time

- Reviewing balances, interest rates, and payments reveals what drives financial pressure

- Clarity makes repayment decisions more intentional and manageable

- Flexible repayment options support consistency without added stress

- Guidance and secure online payments help turn insight into steady progress

What Portfolio Analysis Means for Your Debt Situation

When money feels tight, managing debts one by one can hide the real problem. Portfolio analysis means stepping back and looking at all your debts together to understand how they affect your budget as a whole.

For financially stressed individuals, this approach answers a key concern: Why does it feel like you’re paying every month but not moving forward? Seeing the full picture shows where interest, timing, and balances create the most pressure.

A simple debt portfolio review focuses on:

- Total balances across all accounts

- Interest rates and payment terms

- Monthly payment obligations

- How much of your income goes to debt

You don’t need advanced tools to start. Organizing this information helps you identify which debts deserve attention first and where flexibility could ease strain. Secure online payment tools and structured repayment support can then help you follow through consistently.

Once you understand what portfolio analysis means, the next step is seeing why reviewing your debts together matters more than addressing them one at a time.

Why Looking at Your Debt All at Once Matters

Focusing on one bill at a time can make it feel like progress is happening, even when the overall pressure stays the same. Looking at your full debt picture helps you understand what’s truly driving the stress behind your monthly payments.

When debts are reviewed together, patterns become easier to spot. You can see which balances cost you the most over time and which payment schedules compete with essential expenses. That clarity makes it easier to choose smarter next steps.

Here’s what reviewing your debts as a group can reveal:

- Which accounts carry the highest interest

- How overlapping due dates strain your cash flow

- Where minimum payments slow real progress

- Which debts create the most long-term risk

This perspective helps you move from reacting to bills toward planning with intention. When repayment decisions are based on the full picture, flexible payment options and secure online tools become more effective and easier to manage.

With that understanding, the next step is identifying the specific components you should review when analyzing your personal debt portfolio.

Key Components of Your Personal Debt Analysis

A useful debt portfolio analysis focuses on a few clear details that shape how manageable your situation feels month to month. You don’t need to track everything—just the information that influences cost, timing, and stress.

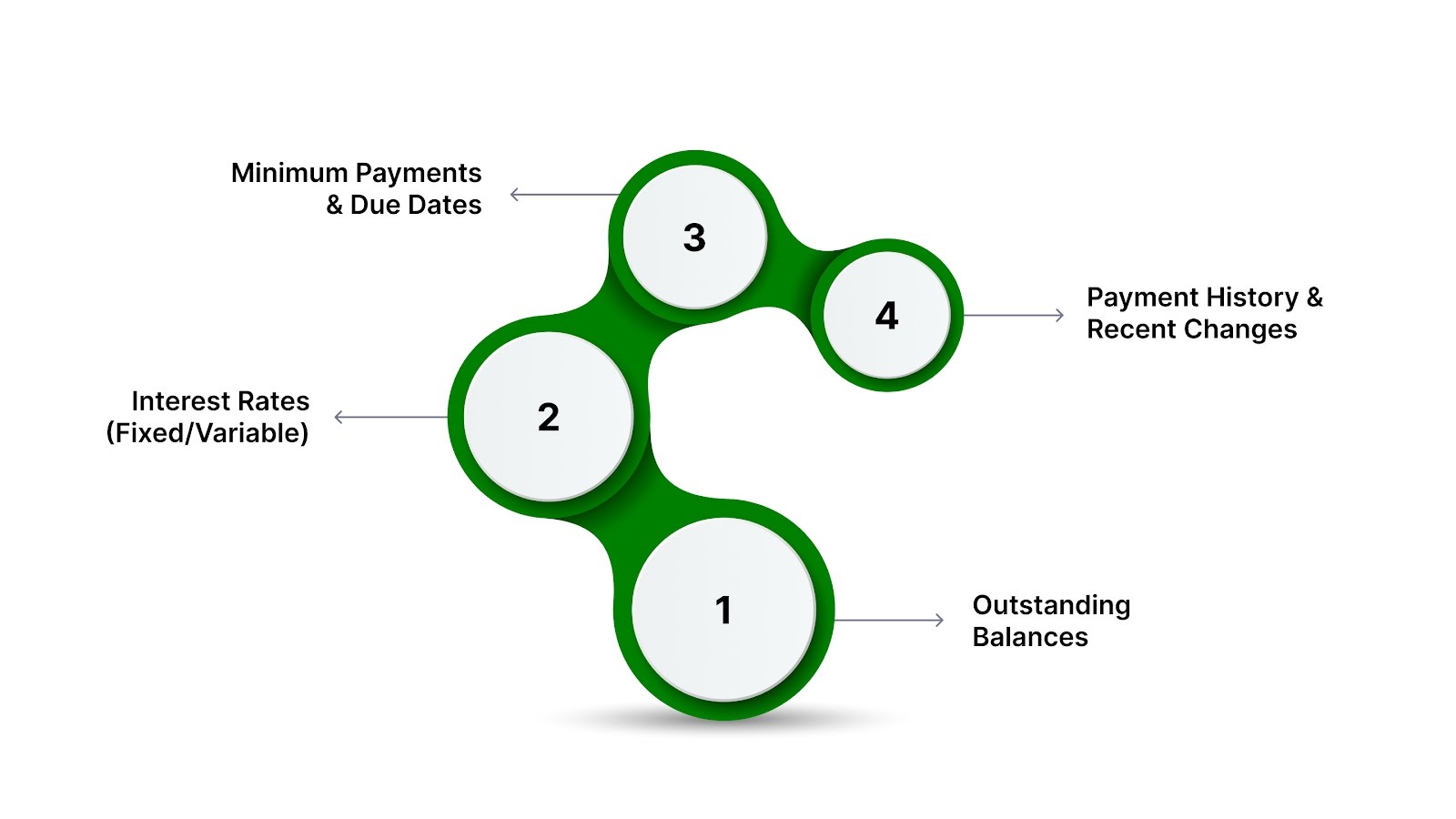

Start by gathering these core components:

- Outstanding balances on each account.

- Interest rates and whether they’re fixed or variable.

- Minimum payments and due dates.

- Payment history and any recent changes.

Looking at these elements together helps you see which debts drain the most money and which create scheduling conflicts. This clarity makes it easier to prioritize without guessing or reacting under pressure.

As patterns emerge, you can begin thinking about adjustments that bring relief, such as restructuring payments or choosing tools that simplify tracking and follow-through. Consistent organization and secure online payment access help keep that momentum steady.

Once these components are clear, the next step is learning how to review your debt portfolio in a simple, step-by-step way without feeling overwhelmed.

How to Do Your Own Debt Portfolio Review

Once you’ve identified the key details, reviewing your debt portfolio becomes a practical exercise, not an emotional one. The goal isn’t perfection, it’s clarity that helps you make steadier decisions.

You can start with a simple, structured review:

- List each debt with its balance, interest rate, and due date.

- Note how much you pay monthly and how often payments overlap.

- Identify which debts cost the most over time.

- Flag any accounts that feel hardest to keep up with.

As you review, avoid the urge to judge past decisions. This step is about understanding where you are today so you can choose what works moving forward. Small adjustments often matter more than drastic changes.

Staying organized makes follow-through easier. Secure online payment tools and flexible repayment options can help you manage multiple accounts without missing payments or adding stress.

With a clearer review complete, the next step is understanding how this analysis can guide smarter repayment choices that support long-term stability.

How This Analysis Can Guide Your Next Steps

Once you understand how your debts interact, decisions stop feeling random and start feeling intentional. Portfolio analysis gives you a framework to choose actions that reduce stress instead of shifting it elsewhere.

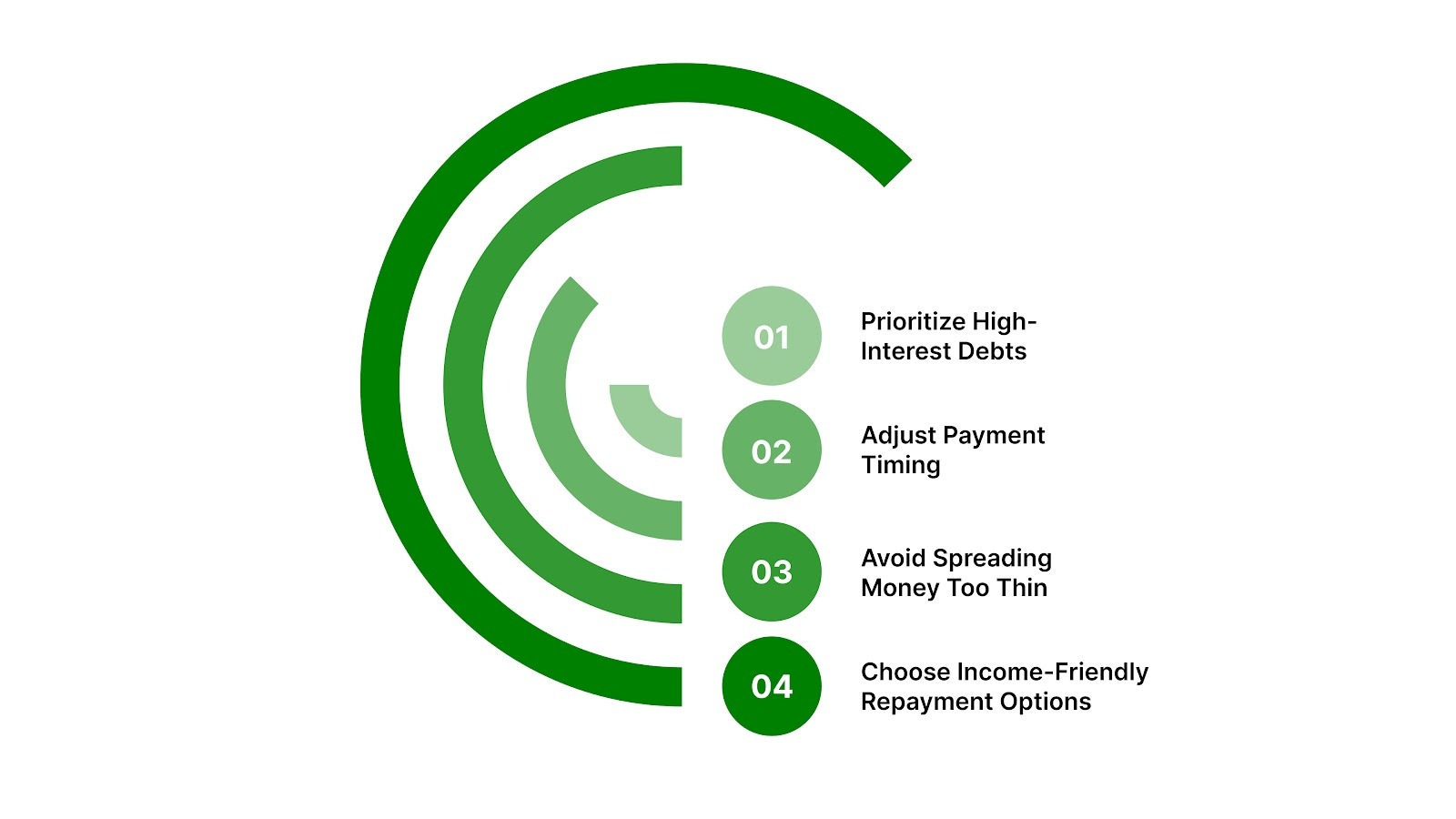

With a clear debt picture, you can:

- Prioritize debts that cost the most in interest.

- Adjust payment timing to protect essential expenses.

- Avoid spreading money too thin across every balance.

- Choose repayment options that fit your income rhythm.

This insight helps you move away from short-term fixes and toward consistency. Flexible repayment options make it easier to stay committed, while secure online payments help you track progress without added complexity.

When your plan aligns with your financial reality, follow-through becomes more manageable and less draining. That’s when momentum starts to build.

If reviewing and adjusting your plan still feels uncertain, the next step is knowing when to ask for support instead of navigating these choices alone.

When to Ask for Help With Your Debt Evaluation

There’s a point where reviewing numbers on your own stops being productive and starts adding pressure. If uncertainty remains after your analysis, asking for guidance can help you move forward with clarity instead of second-guessing.

Support can be helpful if you notice any of the following:

- You’re unsure which debts to prioritize

- Payments feel unmanageable even after reviewing your budget

- You worry about making a decision that sets you back

- You need structure to stay consistent month to month

Getting help doesn’t mean you’ve failed at managing your finances. It means you’re choosing to make informed decisions with the right context and support. Personalized guidance can help translate your analysis into a realistic plan you can maintain.

With clear direction, flexible repayment options, and secure online tools, it becomes easier to turn insight into action.

Now that you’ve seen how portfolio analysis fits into your situation, it’s time to bring everything together and decide how you want to move forward with confidence.

Conclusion

Understanding your full debt picture can change how you approach every financial decision from this point forward.

You’ve learned what portfolio analysis means for your debt, why reviewing everything together matters, and how to use that insight to guide smarter repayment choices. Instead of reacting to bills as they arrive, you now have a way to plan with clarity and intention.

Taking action doesn’t require drastic moves or perfect timing. It starts with organizing what you owe, choosing manageable next steps, and staying consistent with a plan that fits your financial reality.

When you’re ready to move forward, contact our advisors to review your debt portfolio or make a payment online today using secure tools designed to support steady progress.

Frequently Asked Questions

1. Is portfolio analysis only for investments, or does it apply to debt?

Portfolio analysis also applies to personal debt. It helps you understand how all your balances, payments, and interest rates work together.

2. Do I need special tools to analyze my debt portfolio?

No. A basic list of balances, interest rates, and due dates is enough to start gaining clarity and direction.

3. How often should I review my debt portfolio?

Reviewing it every few months or after a financial change helps you stay aligned with your budget and priorities.

4. Can portfolio analysis help lower my financial stress?

Yes. Seeing the full picture often reduces uncertainty and helps you make calmer, more confident decisions.

5. What if my analysis shows I can’t keep up with payments?

That’s a signal to explore flexible repayment options or seek guidance before stress turns into missed payments.