What Investment Portfolio Management Means for Managing Debt Over Time

Need Help Reviewing Your Account?

Contact UsWhen you’re juggling multiple debts, it can feel like every month brings a new decision without a clear sense of long-term direction. You may be making payments consistently, yet still wondering whether your approach is actually improving your situation.

Investment portfolio management is usually discussed in the context of assets and growth, but the core idea is broader than that. At its heart, it’s about managing multiple financial obligations over time with structure, review, and adjustment, principles that matter just as much when you’re managing debt.

In this article, you’ll learn how investment portfolio management concepts apply to personal debt, how debts move through predictable stages, and how different management approaches affect long-term stability. With this understanding, you can move away from reacting month to month and toward a plan that supports consistency.

To start, let’s look at what investment portfolio management really means when it’s applied to real-life debt, not investments or institutions.

Key Takeaways

- Investment portfolio management principles can apply to debt, helping you manage multiple balances as a connected system rather than isolated bills.

- Debt changes over time, and managing it without structure often leads to rising interest pressure and competing payment demands.

- Different management approaches exist, from self-directed efforts to structured and guided plans that adapt as circumstances change.

- Using the right tools consistently matters, including secure online payments and flexible repayment options that adjust with your budget.

- Personalized guidance helps turn uncertainty into a workable plan, supporting steady progress instead of reactive decisions.

What Portfolio Lifecycle Management Means in Personal Finance

Investment portfolio management typically refers to overseeing multiple financial assets in a coordinated way. In personal finance, the same principles apply when you’re managing multiple debts that compete for limited income.

For overwhelmed debtors, this answers an important question: Why does handling debt feel harder over time, even when payments are being made? Without structure, debts interact in ways that quietly increase pressure.

When applied to debt, investment portfolio management principles help you:

- View all debts as part of one financial picture

- Understand how interest, timing, and balances interact

- Adjust your approach as circumstances change

- Avoid reactive decisions that create future strain

Instead of focusing only on the next due date, this approach emphasizes ongoing review, planning, and adjustment. That perspective makes it easier to choose repayment options that fit your income and remain sustainable.

With that foundation in place, it’s important to understand why this structured approach matters even more when you’re carrying multiple debts at once.

Also Read: Simple Money Management Techniques for Personal Finances

Common Investment Portfolio Management Approaches

When managing multiple financial obligations, people naturally fall into different management styles. These approaches mirror traditional investment portfolio management types, but apply directly to debt.

Self-Directed Management

You manage each debt independently, often prioritizing what feels most urgent.

- Decisions are reactive and time-driven.

- Long-term structure is often missing.

Structured Management

Payments follow a defined plan aligned with income and essentials.

- Timing and amounts are planned.

- Consistency matters more than speed.

Guided Management

You receive support in interpreting your full financial picture.

- Decisions are informed and proactive.

- Adjustments happen before stress escalates.

Adaptive Management

Your approach evolves as debts move through different stages.

- Plans adjust when income or expenses change.

- Progress continues despite setbacks.

Understanding which approach you’re using helps explain why progress feels steady, or strained, and sets up the next step of recognizing how debt naturally moves through its lifecycle.

Also Read:

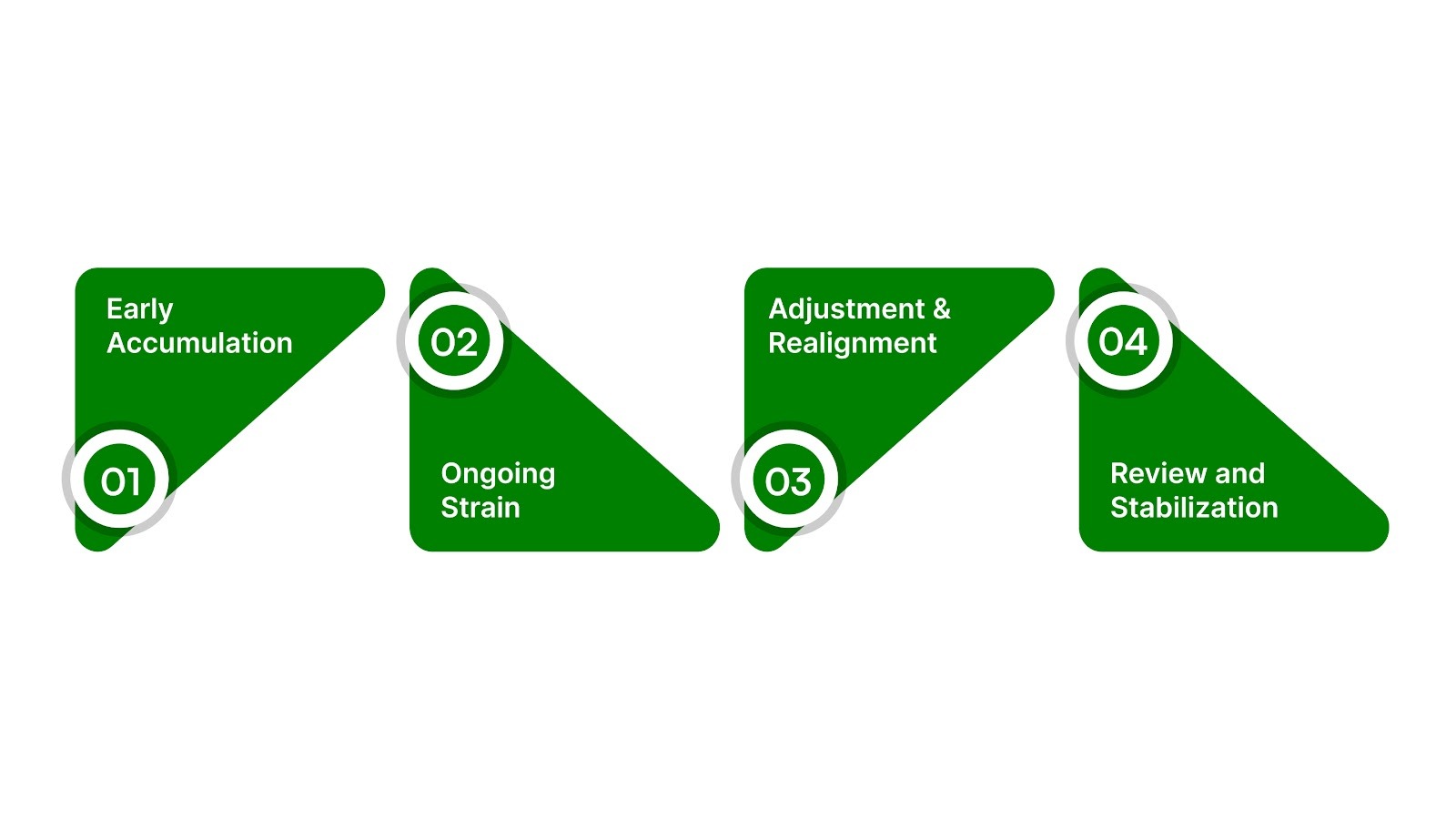

How Debt Moves Through Its Lifecycle

Debt rarely stays the same from month to month. As time passes, balances, interest, and payment demands change, shaping how manageable everything feels. Understanding this lifecycle helps you respond with planning instead of pressure.

Most personal debt moves through a few common stages.

Early Accumulation

Balances begin to build, often gradually, while minimum payments still feel manageable.

- Spending or life changes outpace repayment.

- Interest starts adding quite a pressure.

Ongoing Strain

Payments take up more of your income, and flexibility starts to shrink.

- Due dates overlap more often.

- Missing one payment creates wider stress..

Adjustment and Realignment

You begin modifying how debts are handled to regain stability.

- Payment structures may change.

- Priorities shift toward sustainability.

Review and Stabilization

Progress becomes more visible as consistency improves.

- Balances decline more predictably.

- Planning replaces reaction.

Knowing which stage you’re in helps you choose actions that fit your situation instead of fighting against it. With that clarity, the next step is identifying the tools and supports that make managing each stage easier.

Also Read: Using Technology to Improve Debt Collection Compliance in 2025

Tools That Support Each Stage of the Lifecycle

Managing debt through different stages becomes easier when you use tools that support consistency instead of adding more decisions to your plate. The right tools help you stay organized, adapt when needed, and avoid falling behind during stressful periods.

Here’s how support can align with each stage of your debt lifecycle:

- During early accumulation, clear tracking helps you understand balances before pressure builds

- During ongoing strain, flexible repayment options help protect essential expenses

- During adjustment, structured plans reduce missed payments and uncertainty

- During stabilization, consistent systems help you maintain momentum

Secure online payment tools play an important role at every stage. When payments are easy to schedule, track, and confirm, you spend less time worrying about logistics and more time focusing on progress.

Flexible repayment arrangements also matter as circumstances change. A plan that can adjust with your income or expenses helps you stay committed without setting unrealistic expectations.

When questions come up, personalized financial guidance can help you interpret what’s happening and decide on next steps calmly. Support should simplify choices, not rush them.

With the right tools in place, the next step is learning how to recognize when it’s time to reevaluate your current approach.

Knowing When to Reevaluate Your Approach

Even a solid plan needs occasional review, especially when your financial situation shifts. Reassessing early helps you make adjustments before small issues become ongoing stress.

Pay attention to signs that your current approach may no longer fit:

- Payments feel harder to keep up with, even when nothing new changed.

- You’re relying on short-term fixes to cover due dates.

- One missed payment disrupts several accounts.

- Financial stress increases despite consistent effort.

These signals don’t mean you’ve failed. They usually mean your debts have moved into a new stage that requires a different strategy. Reevaluate with the goal of protecting essentials and restoring balance, not forcing progress.

At this point, tools that simplify tracking and allow flexible repayment can reduce pressure quickly. Clear guidance can also help you decide whether small adjustments are enough or whether a more structured plan would bring relief.

With a fresh perspective in place, you’re ready to pull everything together and decide how to move forward with clarity and confidence.

Conclusion

Debt doesn’t stay still, and managing it successfully means adjusting your approach as your situation changes.

You’ve learned what portfolio lifecycle management means in personal finance, the different ways people manage debt over time, and how debts move through predictable stages. You’ve also seen how recognizing those stages helps you avoid reacting under pressure and instead plan with intention.

The next step is choosing support that matches where you are right now. Forest Hill Management helps you manage your debt lifecycle with personalized financial advisory support, flexible repayment options that adjust as circumstances change, and secure online payment tools that make staying consistent easier. This combination helps turn uncertainty into structure and steady progress.

When you’re ready to regain control, contact our advisors to create a debt lifecycle plan that fits your financial reality, or make a payment online today to stay on track with confidence.

Frequently Asked Questions

1. Is portfolio lifecycle management only for investments?

No. In personal finance, portfolio lifecycle management focuses on how your debts change over time and how you manage them sustainably.

2. How is this different from just paying bills each month?

Paying bills is reactive. Lifecycle management helps you plan ahead, adjust early, and avoid patterns that quietly increase stress.

3. Do I need to be behind on payments to use lifecycle management?

No. It’s most effective when used early, but it also helps when debt already feels hard to manage.

4. Can lifecycle management help if my income changes?

Yes. A lifecycle approach is designed to adapt when income or expenses shift, instead of locking you into rigid plans.

5. When should I consider professional guidance?

If payments feel harder despite effort, or decisions feel unclear, guidance can help you reset before problems escalate.