Understanding Portfolio Recovery Associates and Debt Collection

Need Help Reviewing Your Account?

Contact UsThe moment Portfolio Recovery Associates appears on your phone or mail, your attention locks in. Unexpected debt contact triggers a survival response because financial mistakes carry real consequences.

Suspicion follows fast, and it’s justified rather than paranoid. Federal consumer data shows 60% of debt collection complaints involve attempts to collect money people say they do not owe.

That reality forces a sharper question before panic or payment enters the picture. Is Portfolio Recovery a legitimate company, or is this another situation where pressure replaces proof?

This article explores how to interpret that first contact, assess credibility without assumptions, and respond with control instead of fear.

Key Takeaways

- Unexpected contact from debt collectors like Portfolio Recovery can trigger stress, but knowing your rights immediately helps you regain control.

- Verify any claimed debt in writing before making payments or acknowledging it; this protects you legally and financially.

- Keep detailed records of all communications: calls, emails, letters, to defend yourself if disputes or violations arise.

- Understand that legitimate debt collectors operate under strict rules (FDCPA), so recognizing illegal or aggressive tactics helps you respond effectively.

- For guidance beyond basic rights, a structured, supportive approach from a team like Forest Hill Management can help you guide repayment options confidently and safely.

Who Is Portfolio Recovery Associates?

Portfolio Recovery Associates operates as a debt buyer, established in 1996 and now part of PRA Group, one of the largest debt purchasing companies in the United States. Their business model centers on acquiring charged-off accounts from original creditors, then pursuing collection on those debts under their own name.

When your credit card company or lender writes off an unpaid account, they often sell it to companies like Portfolio Recovery. The original creditor takes a loss, and Portfolio Recovery assumes the right to collect the debt it purchased, subject to verification, accuracy, and applicable consumer protection laws.

Understanding who they are matters because it changes how you should respond when they reach out.

Yes, Portfolio Recovery Associates Is Legitimate

Portfolio Recovery Associates (PRA) is a real, U.S.-based debt collection agency, not a fake or fly-by-night operation. The company maintains physical offices in the United States, including its headquarters in Norfolk, Virginia, and operates as part of PRA Group, a publicly traded company.

Being legitimate does not mean their claims are always correct, nor does it remove your right to dispute a debt. It simply means they are a real business subject to real laws.

What confirms their legitimacy:

- Verifiable business registration: PRA is registered with state regulators and listed with the Better Business Bureau

- Subject to the Fair Debt Collection Practices Act (FDCPA): Federal law restricts how, when, and what they can say when collecting debts

- State licensing requirements: In states that require licensing, they may only collect where they are properly authorized.

- Public parent company: PRA Group is listed on NASDAQ (an American stock exchange), which requires public financial disclosures and regulatory compliance

Important distinction:

Legitimacy confirms that the company exists and is regulated. But it does not prove that the specific debt they claim you owe is valid, accurate, or legally collectible. You still have the right to request verification and dispute the debt if necessary.

Also Read: Best Debt Payment Gateways and How They Work

To understand your rights, it helps to know how PRA acquires and collects debt.

How Portfolio Recovery Acquires and Collects Debt

Debt doesn’t move instantly from your original creditor to Portfolio Recovery Associates. There’s a structured process involved, and understanding it helps explain why the information they have may sometimes be limited or imperfect.

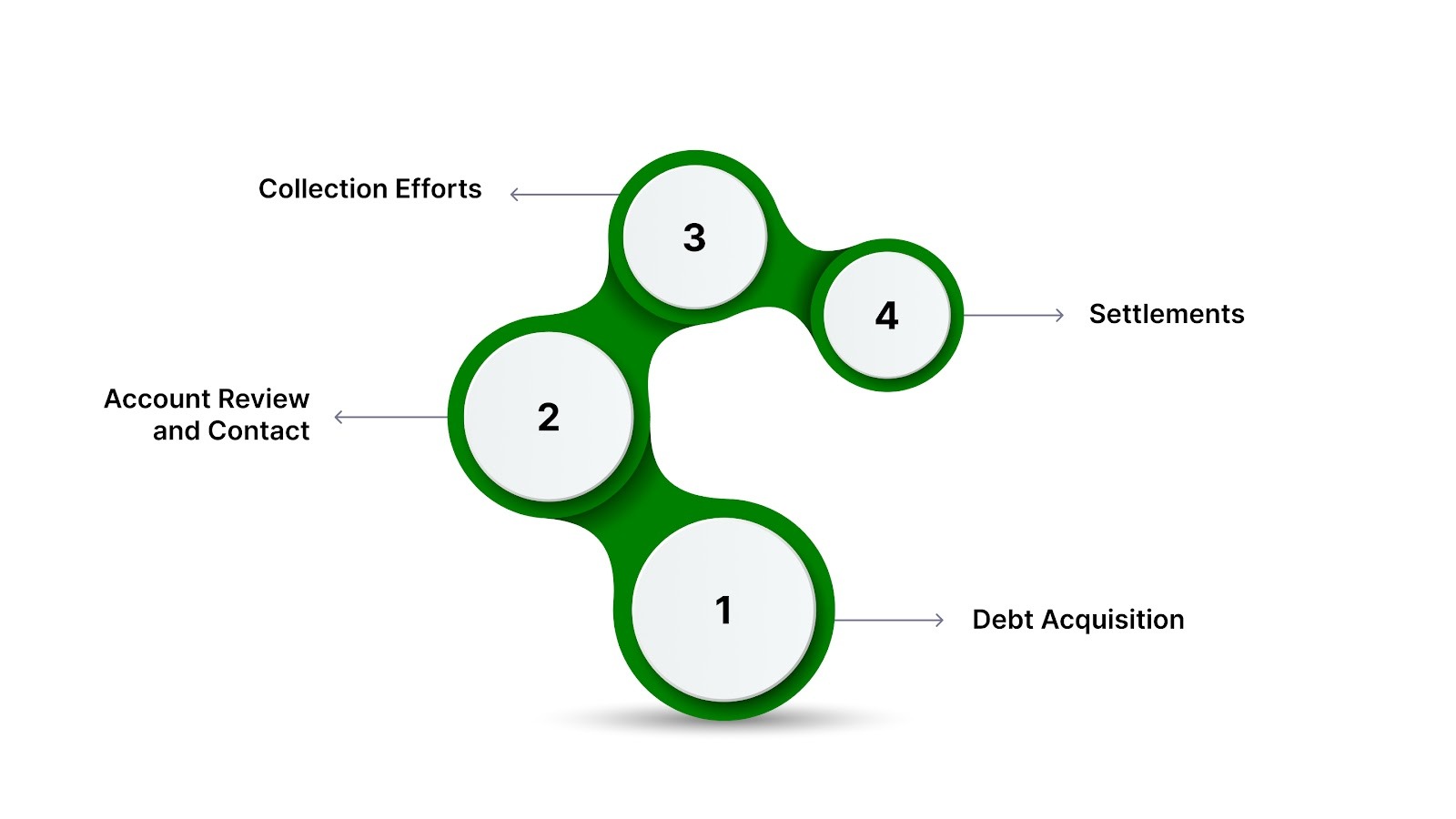

Debt Acquisition

Original creditors typically don’t sell delinquent accounts one by one. Instead, they package large numbers of charged-off accounts into portfolios and sell them in bulk to debt buyers like Portfolio Recovery Associates. These portfolios are usually sold for a small percentage of the total balance owed.

Because the debts are sold in bulk, the accompanying documentation can vary in completeness. In some cases, the buyer may receive only basic account data, such as names, balances, and last known contact information, rather than full payment histories or original contracts.

The difference between what Portfolio Recovery pays for the portfolio and what it ultimately collects is how the company generates profit.

Account Review and Contact

After purchasing a portfolio, Portfolio Recovery attempts to match the accounts to the correct consumers and update contact information. This process may involve reviewing credit reports, public records, and other permissible data sources to locate current addresses or phone numbers.

Once contact begins, Portfolio Recovery typically sends a written notice identifying the debt, the amount claimed, and the consumer’s right to dispute the debt. This initial notice is required by federal law and must provide specific disclosures about how to request verification.

Collection Efforts

Collection efforts usually start with phone calls and letters intended to prompt payment or open settlement discussions. These early attempts are often designed to resolve the account without formal legal action.

If informal efforts do not result in payment or resolution, Portfolio Recovery may decide to pursue a lawsuit, depending on the account, balance, and applicable state laws.

If a court judgment is obtained, it can allow certain enforcement actions, such as wage garnishment or bank account levies, subject to state-specific legal limits and procedures.

Settlements

Settlement offers are common in debt collection. Accepting a reduced amount can allow Portfolio Recovery to close an account more efficiently than continuing long-term collection efforts. Settlement terms vary based on factors such as account age, balance, and prior payment history.

Also Read: Simple Steps to Pay Off Debt Fast

Now that we’ve covered how Portfolio Recovery handles debt, it’s important to look at the legal boundaries that govern their collection practices.

What Portfolio Recovery Can and Cannot Do Under Federal Law

Debt collectors, including Portfolio Recovery Associates, must follow rules set by the Fair Debt Collection Practices Act (FDCPA). They can attempt to collect a debt they believe you owe, but they cannot harass, deceive, or threaten you illegally.

Let’s understand these limits so it's easier to recognize when your rights are being violated.

Knowing these rules lets you spot illegal behavior and protect your rights. If Portfolio Recovery violates them, you can report it to the CFPB, FTC, or your state attorney general, and may pursue legal remedies under the FDCPA.

Knowing your legal protections is one thing; knowing how to act when Portfolio Recovery reaches out is the next crucial step.

What to Do If Portfolio Recovery Contacts You

Ignoring Portfolio Recovery won't make them disappear. Avoidance might buy time, but it also opens the door to lawsuits, judgments, and wage garnishment if the debt is legitimate and enforceable.

Responding strategically means protecting your rights while keeping your options open. Here's the approach that gives you the most control:

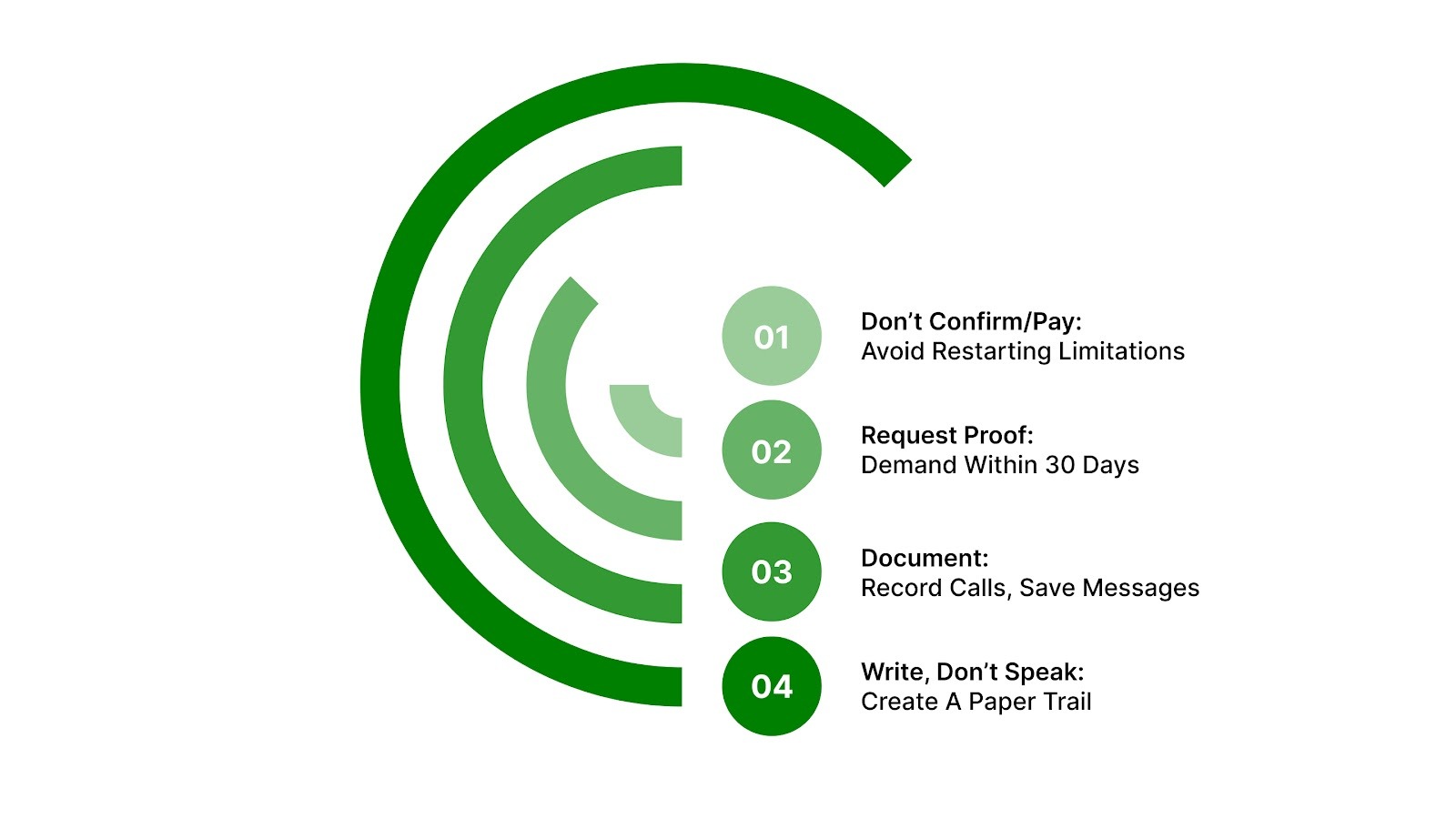

- Don't confirm the debt or make a payment immediately: In some cases, payments or written acknowledgments can restart the statute of limitations under state law.

- Request written validation before discussing payment terms: Use your first 30 days after initial contact to demand proof. Once you make that request, they're legally required to pause collection efforts until they provide documentation.

- Document every interaction: Keep records of calls (date, time, who you spoke with), save all letters and emails, and note what was said. If they violate the FDCPA, your documentation becomes evidence.

- Respond in writing, not over the phone: Verbal agreements and conversations are harder to prove. Written communication creates a paper trail that protects you if disputes escalate.

Taking action early prevents Portfolio Recovery from controlling the narrative. You set the terms, not them.

Also Read: Financial Infrastructure of Real-Time Payment Systems

Dealing with debt collection can feel overwhelming, even when you know your rights. For those who want a clear, guided path to regain control, Forest Hill Management provides a different, consumer-first experience.

How Forest Hill Management Differs From Debt Buyers Like Portfolio Recovery

Unlike debt buyers such as Portfolio Recovery Associates, who purchase charged-off accounts in bulk, Forest Hill Management focuses on helping you regain control of your finances. We do this through structured, compliant account management. We don’t purchase debt portfolios; our role is to provide clear information and structured account management options where applicable.

Here’s how working with Forest Hill is different for you:

- Transparent Account Management: You know exactly what you owe and to whom from the start, with clear visibility into balances and next steps.

- Flexible Repayment Plans: Payment options are designed around your ability to pay, giving you a structured path forward without unnecessary pressure.

- Compliance-First Approach: Every process follows federal consumer protection laws, so your rights and privacy are always protected.

- Secure Online Access: View balances, track progress, and make payments anytime with our safe, user-friendly platform.

- Supportive Advisor Guidance: Speak directly with knowledgeable advisors who can answer your questions and help you plan your next steps.

If you want to understand your account and explore available options, you can review your information online or speak with a Forest Hill Management advisor.

Conclusion

Financial challenges can feel isolating, and being contacted by a debt collector often heightens that stress. The key is remembering that you remain in control. Staying informed, understanding your rights, and taking deliberate steps can turn uncertainty into actionable options.

When it feels overwhelming, you don’t have to navigate it alone. Working with a company that prioritizes transparency, compliance, and clear communication can make the process easier to manage.

Take the first step toward regaining control - contact Forest Hill Management for guidance tailored to your situation today.

FAQs

1. How does Portfolio Recovery prioritize accounts?

Accounts are prioritized based on collectability, balance size relative to purchase cost, and likelihood of successful resolution. Some accounts see frequent outreach, while others are less active.

2. Can multiple sales of the same debt cause issues?

Yes. Multiple sales can create incomplete or conflicting records, leading to duplicate notices or balance discrepancies. Tracking your account history helps identify errors.

3. Can timing affect contact frequency?

Contact frequency may vary due to operational or portfolio management cycles, but there’s no guarantee that specific timing always increases outreach.

4. Does the age of an account influence settlements?

Debt age can be one factor in negotiations, along with the type of debt and purchase price. Accounts near legal time limits may sometimes be treated differently, but outcomes vary.

5. How are co-signers or secondary parties handled?

Co-signed accounts require extra verification, and secondary parties can complicate communication or settlement. All actions follow federal and state collection laws.