Understanding Charge-Offs: What Happens After Your Debt

Need Help Reviewing Your Account?

Contact UsA charge-off hits harder than a missed payment because it feels final. With U.S. credit-card charge-offs hovering near 4.5%, you're far from alone when this label suddenly appears on your account.

That word scares people for a reason, but it also misleads. A charge-off means the lender stopped counting on repayment, not that your balance vanished or your responsibility ended.

From there, things usually shift fast. Your credit can carry the mark for up to seven years. Collection contacts often increase, and your debt may be transferred to a new owner while you still owe every dollar.

This article explores what charge-off asset acquisition really means for your debt and who ends up holding your account. You'll also learn how it affects your credit and the practical options you have to regain control.

Key Takeaways

- A charge-off signals the lender expects nonpayment, not that your debt disappears; knowing this prevents costly misunderstandings.

- After a charge-off, debt may be sold or retained, so identifying the current owner is crucial for negotiation or resolution.

- Charge-offs hurt credit, but verifying ownership, negotiating settlements, or setting manageable payments can limit long-term damage.

- Understanding both the statute of limitations and credit reporting timelines helps you make informed decisions and avoid unnecessary risk.

- Working with a management team like Forest Hill helps provide clear account information, secure payment access, and compliant communication.

What a Charge-Off Actually Is

A charge-off occurs when a creditor officially declares your debt uncollectible and removes it from their accounts receivable. This typically happens after 180 days (six consecutive months) of non-payment.

Here's what matters most: the charge-off is an accounting decision, not debt forgiveness. You legally owe the full amount, plus any interest and fees that accumulated before the charge-off date. The creditor has simply acknowledged that they don't expect you to pay it back through regular billing.

The moment this happens, your relationship with that debt fundamentally changes, but not in the way most people assume.

Why Creditors Charge Off Accounts

Creditors charge off accounts because banking rules do not allow severely delinquent debts to remain classified as performing assets indefinitely. At a certain point, lenders must formally recognize that continued non-payment represents a loss rather than expected income.

The charge-off serves three purposes:

- Regulatory compliance: Supervisory agencies require lenders to reclassify long-delinquent accounts to ensure consistent treatment of credit losses across the banking system.

- Financial transparency: Charge-offs allow regulators, auditors, and investors to clearly see how much risk a lender is carrying and how much of its portfolio has failed to perform.

- Operational flexibility: Once an account is charged off, lenders can manage recovery through different internal teams or external partners without treating the account as an active customer relationship.

This step is taken to protect the integrity of the financial system, not to resolve the debt itself.

Also Read: What Happens If You Miss a Payment on Consumer Easy Credit?

Once a creditor charges off an account, the next question is what happens to your debt, and how it might affect your interactions and options moving forward.

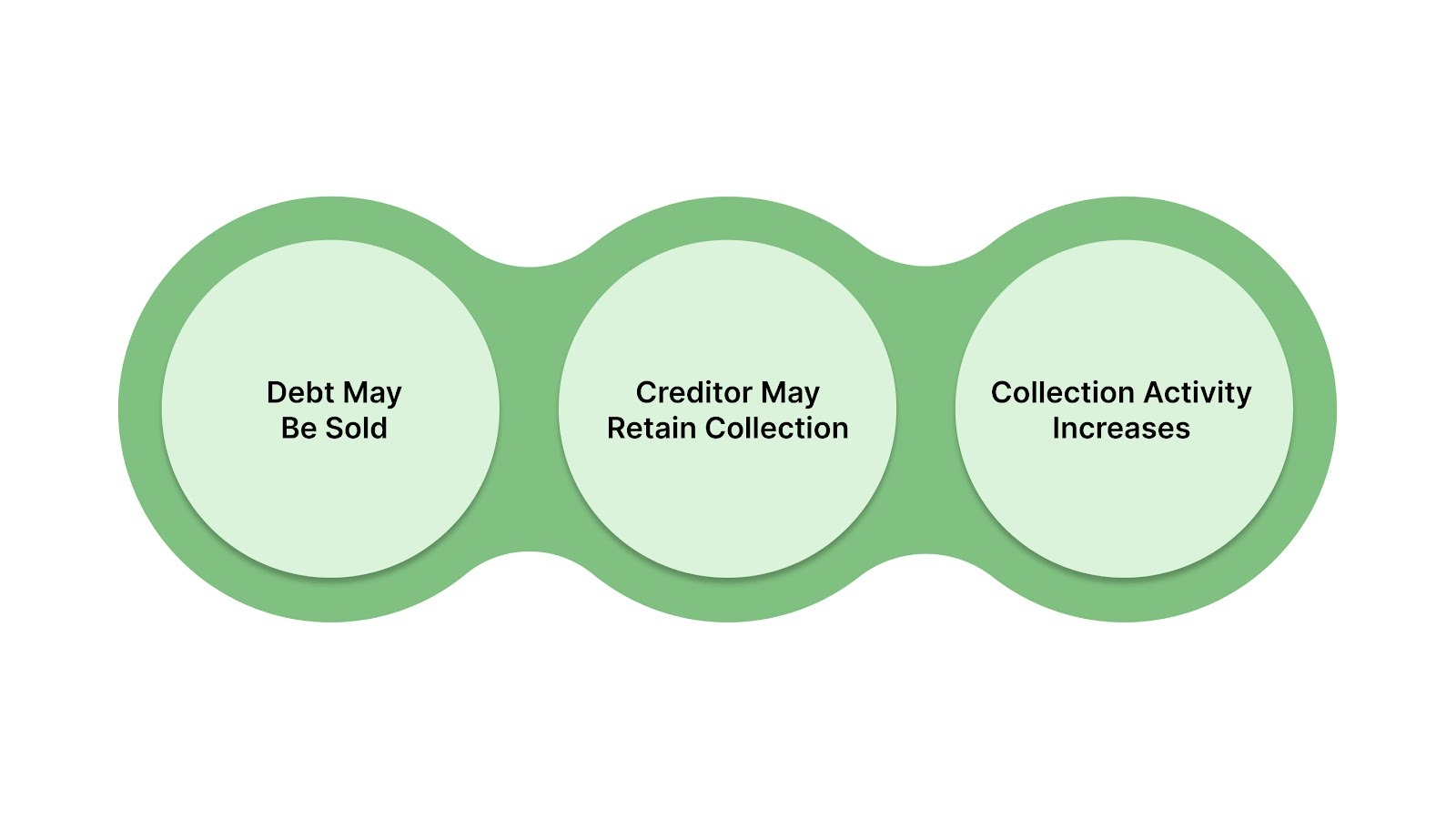

What Happens After Your Debt Is Charged Off

A charge-off does not end collection activity. Instead, it changes how the creditor decides to pursue repayment. After a charge-off, creditors typically review whether to keep the account, involve outside collectors, or transfer ownership to another company.

Each option leads to different interactions, but the debt continues to be pursued.

1. Your Account May Be Sold to a Debt Buyer

Many creditors sell charged-off accounts in large portfolios to debt buyers for a small percentage of the balance owed. These buyers purchase the legal right to collect the debt.

Once sold, the debt buyer becomes the new owner and may contact you directly to seek payment of the outstanding balance. The amount they paid for the debt does not affect how much they are allowed to collect. Some accounts are resold, which can result in ownership changing more than once.

2. The Original Creditor May Keep Collecting

Not all charged-off accounts are sold. Some creditors continue collection internally or assign the account to a third-party collection agency while retaining ownership. In these situations, the creditor still owns the debt, and any outside collector is acting on their behalf rather than as the purchaser of the account.

3. Collection Contact Often Increases

Whether your debt is sold or kept in-house, the frequency and intensity of collection attempts usually escalate after a charge-off. You may receive more calls, more letters, and more settlement offers than you did during the earlier stages of delinquency.

Collectors know the account is charged off, which means there's less concern about preserving the customer relationship. The focus shifts toward recovering the outstanding balance. However, they still must follow the Fair Debt Collection Practices Act (FDCPA), which limits when, where, and how they can contact you.

Seeing how your debt is managed after a charge-off makes it easier to understand the impact on your credit and long-term financial health.

How Charge-Offs Damage Your Credit

A charge-off delivers one of the most damaging blows your credit report can receive. Lenders interpret it as confirmation that you failed to meet your obligation, and that judgment follows you for years.

The consequences unfold across multiple dimensions:

- Significant score impact: A charge-off can substantially lower your credit score, especially if you previously had a higher score or limited positive history.

- Seven-year reporting period: A charge-off stays on your credit report for up to seven years from the date of your first missed payment that led to it, not from the charge-off date itself.

- Harder approval and higher costs: Lenders may view you as higher risk, which can make it harder to qualify for loans or credit cards and can lead to higher interest rates when you are approved.

- Broader financial screening: Some landlords and lenders use credit reports as part of their decision process, and a charge-off can be viewed negatively in those contexts.

There's no shortcut to repairing this damage; only time and consistent positive credit behavior moving forward can rebuild what the charge-off destroyed.

Also Read: What it Means to Have an Outstanding Balance on a Credit Card

The long-term impact on your credit underscores why it’s important to carefully explore your options so you can resolve the account on terms that work for you.

Your Options After a Charge-Off

Once the charge-off appears, you face a decision: ignore it and accept the long-term credit consequences, or engage with the current account holder to understand available options. Neither option is painless, but only one gives you any control over the outcome.

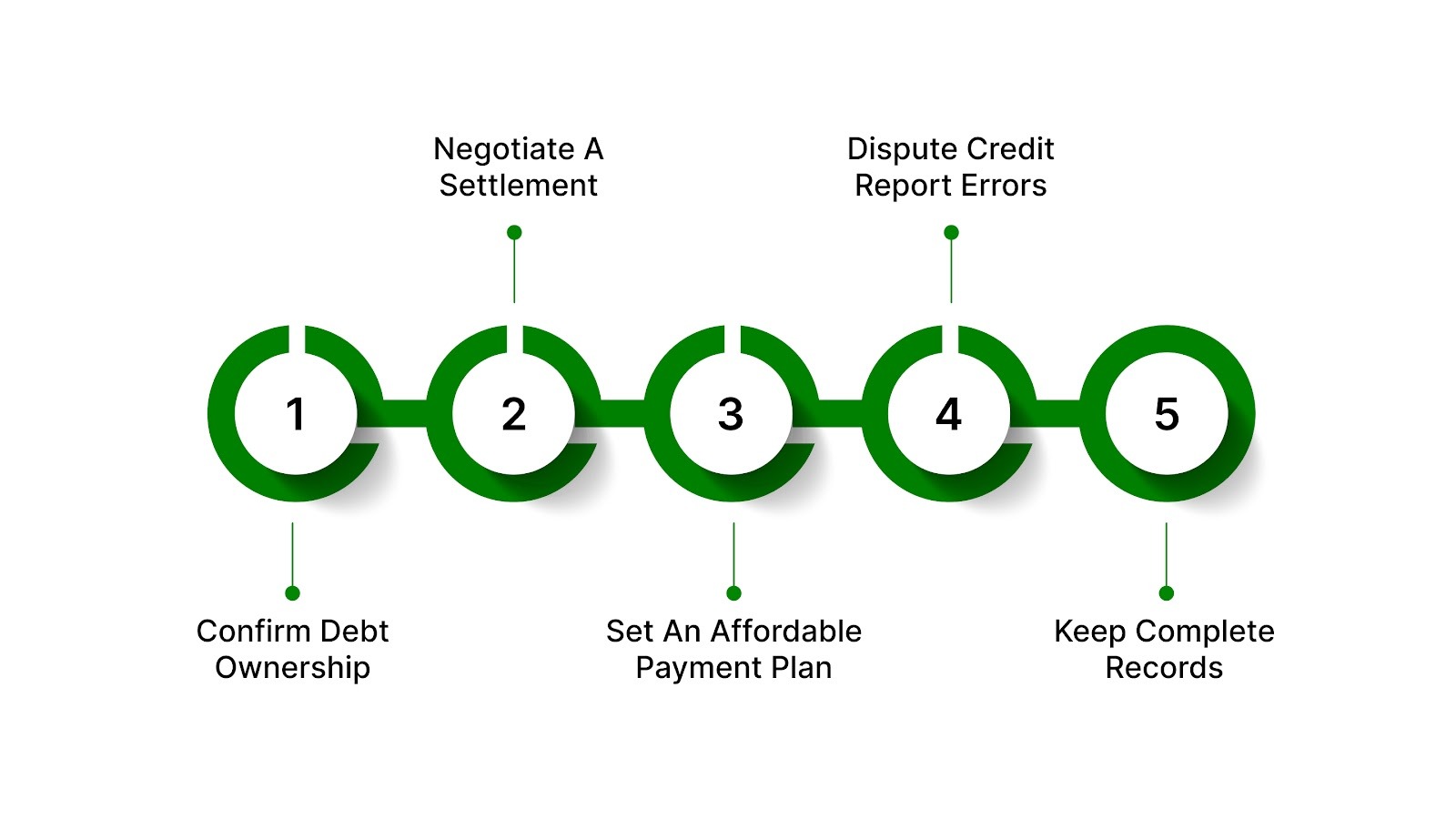

1. Verify Who Owns the Debt Now

Debt can change hands multiple times after a charge-off. Before paying or negotiating, confirm who legally owns the account. Here’s what to do first:

- Request validation in writing: Under the FDCPA, debt collectors must provide proof they are authorized to collect, including the original creditor, the current balance, and the date of first delinquency.

- Dispute if needed: If the collector cannot provide proper validation, you may dispute the debt in writing within 30 days of first contact.

- Avoid verbal promises: Always get documentation from anyone claiming to own or collect the debt.

2. Negotiate a Settlement for Less Than You Owe

Creditors and debt buyers may accept less than the full balance to recover at least part of the debt. Here are important considerations if settlement options are available:

- Settlement amounts vary: Offers depend on the age of the debt, the owner, and the creditor’s policy; there is no guaranteed percentage.

- Decide what you can afford: Make an initial offer lower than the maximum you can pay to leave room for negotiation.

- Get everything in writing. The agreement should state the settlement amount, that it satisfies the debt in full, and that no further collection will occur. Do not rely on verbal promises.

3. Set Up a Payment Plan You Can Afford

If a lump-sum settlement isn’t possible, some creditors or collectors may agree to monthly payments. Here’s how to handle a payment plan:

- Be realistic: Only agree to a monthly amount you can consistently pay; missing payments can void the agreement and restart collection efforts.

- Confirm terms in writing: Include monthly payment amount, total number of payments, total amount to be paid, and what happens if a payment is missed.

4. Dispute Inaccurate Information on Your Report

Charge-offs may contain errors, such as incorrect balances, dates, or ownership information. Let’s review the steps to dispute inaccuracies:

- File disputes separately: with Experian, Equifax, and TransUnion.

- Provide supporting documentation: Bureaus must investigate within 30 days and correct or remove inaccurate entries.

- Know the limits: Disputing errors does not erase legitimate debts, and collection may continue while the dispute is resolved.

5. Keep Documentation of Everything

Whether you negotiate, pay, or dispute, maintain copies of all letters, agreements, and communications. Written records protect you if disagreements arise.

Also Read: How Much Do Collection Agencies Charge and How It Affects You

Once you understand your options, it’s also important to know the timelines that affect how long a debt can be reported or legally pursued.

Statute of Limitations vs. Credit Reporting Timeline

Two separate clocks affect a charge-off: one determines if a collector can sue you (statute of limitations), and the other controls how long it appears on your credit report (credit reporting timeline). Understanding both is key to avoiding unexpected legal or financial consequences.

Here’s a quick comparison:

A debt can be time-barred (lawsuit protection expired) but still appear on your credit report. Conversely, a debt might fall off your credit report while the statute of limitations remains active.

Timelines matter, but knowing your options and getting support makes all the difference, and that’s where Forest Hill Management can help.

How Forest Hill Management Handles Charged-Off Accounts

When a charged-off account is placed with Forest Hill Management, we understand you may already be dealing with credit stress and uncertainty about what happens next. Our role is to provide clear information and maintain compliant communication about your account.

If you're working with us on a charged-off account, here's what you can expect:

- Clear information about the account, including the original creditor and current balance

- Available payment options are clearly explained so you understand what may apply to your account

- The ability to review account details and understand available payment options

- Secure, convenient online payments that give you control and visibility

- Straightforward communication about your account status and updates related to your account

You deserve clear answers and straightforward communication, and that's what Forest Hill Management prioritizes.

Conclusion

Facing a charge-off can feel overwhelming, but understanding the mechanics, timelines, and your rights gives you clarity and control. While the account itself represents a past challenge, each step you take now, from verification to structured resolution, lays the foundation for moving forward with confidence.

Working with Forest Hill Management means you receive clear communication and secure account management support.

Contact our team to review your account details or get assistance understanding your options.

FAQs

1. Can a charge‑off indirectly affect my insurance premiums?

A charge‑off itself doesn’t directly determine insurance rates, but insurers often use credit‑based scores in pricing decisions. A lower credit score, which a charge‑off can contribute to, may lead to higher premiums for some policies.

2. What happens to a charge‑off if I file for bankruptcy?

If you include a charged‑off debt in bankruptcy and it’s discharged, you are no longer legally responsible for paying it. However, the charge‑off can still appear on your credit reports for the full seven‑year reporting period.

3. Does a charge‑off affect joint accounts differently than individual debts?

On joint accounts, a charge‑off can affect both parties’ credit reports and liability. Both account holders are responsible for the debt, so the charge‑off status will show on each person’s credit history.

4. Can a creditor still sue me after a charge‑off?

Yes. A charge‑off does not eliminate legal liability. Creditors or debt buyers can still pursue repayment or sue you within your state’s statute of limitations.