What Is a CFPB Debt Validation Letter?

Need Help Reviewing Your Account?

Contact UsOpening a collections letter can feel like stepping into someone else’s story, with numbers, dates, and names that don’t match your memory. You pause, unsure whether the debt is yours or who is actually demanding payment.

A debt validation letter, required under federal law and enforced by the Consumer Financial Protection Bureau (CFPB), exists to cut through that uncertainty. It gives you concrete proof of what you owe, to whom, and provides a 30-day window to challenge inaccuracies before the debt may be treated as valid for collection purposes.

Understanding this notice changes the dynamic. Instead of feeling trapped, you gain control, spotting errors in amounts, creditor names, or account details before making any financial decisions. Every line of the letter is an opportunity to protect your credit and your wallet.

In this article, you’ll see what a CFPB debt validation letter includes, why it matters, and how you can use it to protect your finances.

Key Takeaways

- A CFPB debt validation letter is your legal tool to confirm a debt is accurate before paying, giving you leverage and protection.

- Reviewing the details carefully can uncover errors, misapplied fees, or misattributed accounts, helping you avoid unnecessary payments.

- Acting quickly, within the 30-day dispute window, and sending a clear, written request preserves your rights and pauses collection activity.

- Even if a debt is valid, understanding it fully lets you make informed decisions about repayment or structured plans.

- Working with a transparent, consumer-focused company like Forest Hill Management ensures you get clear information, support, and guidance while addressing your obligations responsibly.

Understanding Debt Validation Under Federal Law

The CFPB oversees debt collectors to prevent unfair or deceptive practices. Under the Fair Debt Collection Practices Act (FDCPA), debt collectors must provide a written validation notice within five days of their initial communication, unless the information was already provided. This notice must show how much you owe, who the original creditor was, and that the collector has the right to collect.

With debt validation established under federal law, the next step is knowing what information the collector must provide in writing.

What Information Must Be Included in a Validation Letter

A debt validation letter is not just a reminder that you owe money. It is a formal disclosure required by federal law that provides the information needed to verify whether the debt is accurate and legally enforceable.

According to the Fair Debt Collection Practices Act (FDCPA) and the CFPB Debt Collection Rule (12 CFR 1006.34), a collector’s notice must include:

- Debt collector identification: A statement that the communication is from a debt collector attempting to collect a debt.

- Current debt information: The exact amount owed as of the date of the notice, including any interest, fees, or other charges, along with an itemized breakdown showing how the balance was calculated.

- Creditor information: The name of the creditor to whom the debt is currently owed. In certain cases (like consumer financial products), the notice must also include the original creditor’s name.

- Account identifier: The account number or another unique identifier associated with the debt.

- Consumer dispute rights: A clear explanation of your right to dispute the debt in writing within 30 days of receiving the notice. The collector must provide instructions on how to request verification or documentation proving the debt is valid.

- Collection suspension during dispute: Notice that if you dispute the debt in writing within 30 days, the collector must cease collection activities until verification is provided.

- Additional consumer protections: References to your rights under the FDCPA and CFPB rules, including how to obtain more information about your rights.

Missing or incomplete information may violate federal requirements.

Also Read: Financial Management Tools to Strengthen Debt Collection

Now that you know what a validation letter must include, it’s important to understand how this information actually protects you.

Why Debt Validation Protects You

Requesting debt validation is about making sure a debt is accurate and legally yours before you pay. Errors can happen: balances may be wrong, fees added incorrectly, or debts may even be mistakenly linked to your name.

Debt validation creates a legal checkpoint, giving you the chance to review and dispute the debt before collection continues:

- Confirms ownership: Ensures the debt is actually yours and not the result of identity theft or clerical mistakes.

- Prevents incorrect payments: Gives you the opportunity to avoid paying debts that have already been settled, are legally unenforceable, or are not yours.

- Identifies billing errors: Helps uncover inflated balances, duplicate charges, or fees added without proper documentation.

- Pauses collection activity: If you dispute the debt in writing within 30 days, most collection efforts must pause until verification is provided.

While validation can stop collection actions temporarily, it does not automatically remove the debt from your credit report. Debt validation gives you a legal tool to protect yourself, confirm the debt is accurate, and resolve mistakes before they escalate.

Before you can benefit from these protections, you need to know the right time and method to request verification.

When and How to Request Debt Verification

The clock starts ticking the day you receive the validation notice. You have 30 days from that date to send a written dispute, and how you handle that window determines whether you keep your legal protections intact.

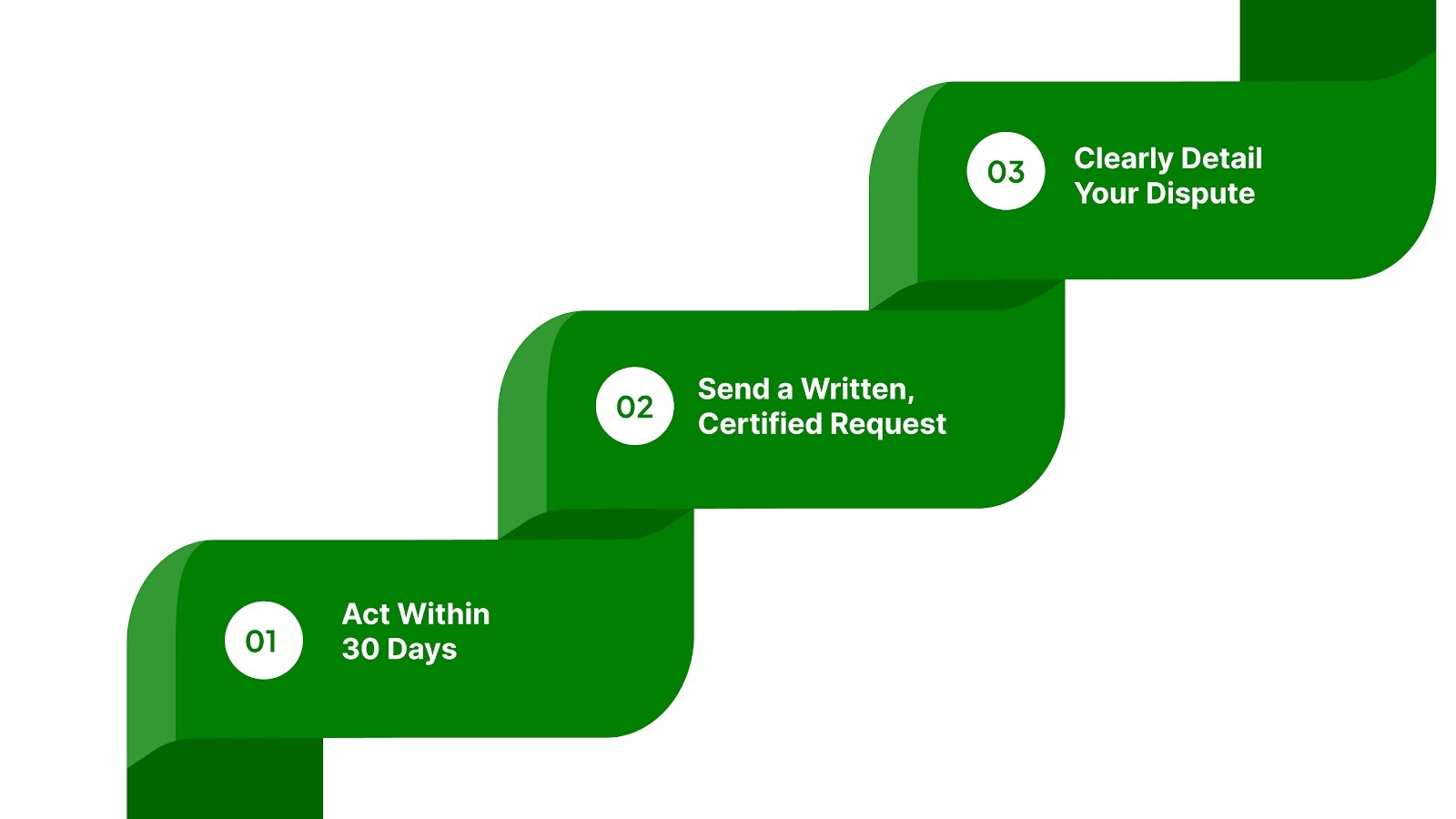

1. Act Within 30 Days

Once 30 days pass, the collector can assume the debt is valid and move forward with collection efforts. You can still dispute later, but you lose certain protections, including the automatic pause on collection activity.

Waiting can make it harder to pause collection activity automatically, even though you still retain the right to dispute inaccuracies later.

2. Send a Written, Certified Request

Phone calls don't count. The dispute must be submitted in writing and sent via certified mail with a return receipt. This creates a paper trail proving the collector received your request and when. Without that proof, they can claim they never got your letter and continue collection efforts.

3. Clearly Detail Your Dispute

Your letter should state clearly that you're disputing the debt and requesting verification. Specify what you're questioning: whether it's the amount, the creditor's identity, or your connection to the account. The more precise you are, the harder it is for the collector to send generic documentation that doesn't address your concerns.

Also Read: The Future of Compliance in Debt Collection: Trends and Innovations

Taking these steps protects your rights. Now, let’s look at the consequences if the collector doesn’t verify the debt.

What Happens If the Collector Doesn't Provide Validation

If you dispute a debt in writing within the required period, the collector must stop collection activity until they provide proper proof that you owe the debt.

Without validation, they cannot continue collection calls, letters, or demands for payment on that account. However:

- They are not automatically barred under the FDCPA from reporting the debt to credit bureaus; credit reporting disputes are handled under the Fair Credit Reporting Act (FCRA).

- They can still initiate legal action (sue you), but their failure to validate can be used as a defense and may expose them to legal liability.

You also have the right to file complaints with the Consumer Financial Protection Bureau (CFPB) or the Federal Trade Commission (FTC), or your state attorney general, if a collector violates these rules.

Understanding your rights when a collector fails to validate a debt helps, but it’s also important to avoid common mistakes that can weaken your dispute.

Common Mistakes Consumers Make With Validation Letters

Even small mistakes can weaken your legal protections under federal law. Here’s what to watch for:

- Ignoring the notice: Missing the 30-day window means the collector may assume the debt is valid and continue collection. You can still dispute later, but the automatic pause on collection calls or letters no longer applies.

- Assuming accuracy: Don’t take the debt at face value. Mistakes in the amount, creditor, or account status happen often and can affect your credit.

- Paying too soon: Paying before verification may be seen as acknowledging the debt, making disputes harder. You can still challenge errors, but your leverage is reduced.

- Missing the dispute deadline: After 30 days, FDCPA rules no longer require the collector to stop collection efforts. Credit reporting is still governed by FCRA and must remain accurate.

Tip: Always send disputes in writing, keep proof of delivery, and act promptly to protect your rights.

Also Read: Basics of Getting Free Professional Financial Planning Advice

While mistakes and delays are common with some collectors, Forest Hill Management follows transparent practices to ensure you get the information you’re entitled to.

How Forest Hill Management Handles Debt Validation Transparently

Debt validation shouldn’t feel like pulling teeth. At Forest Hill Management, we prioritize transparency from the start. You’ll receive clear, accurate information about your account, so you can understand your obligations and next steps without confusion.

When we contact you about an account, you can expect:

- Written notice soon after first contact: A clear outline of your account details, in line with your legal rights.

- Identification of the original creditor: Know exactly who you owed and why.

- Accurate amount and account information: No inflated fees or hidden charges.

- Simple dispute process: Step-by-step instructions if you believe the debt is incorrect.

- Compliance with pause requirements: Collection activity is paused when required by law during written verification requests.

With clear validation, you’re not just getting information; you’re gaining control. Knowing your account details allows you to take calm, confident steps toward resolving your debt on your terms.

Conclusion

Dealing with debt can feel overwhelming, but knowing your options is the first step toward moving forward. Taking action, whether reviewing letters, asking questions, or planning next steps, helps you regain a sense of control over your financial journey.

At Forest Hill Management, you’re never facing this alone. With guidance tailored to your situation and support every step of the way, you can start addressing your obligations with confidence.

Take the first step toward financial freedom or contact our advisors for personalized support today.

FAQs

1. Is a “CFPB debt validation letter” actually issued by the CFPB?

The CFPB does not send validation letters directly. The term refers to an FDCPA-required notice sent by a debt collector, with the CFPB acting as the regulator that enforces compliance.

2. Does a validation letter mean the debt is legally enforceable in court?

Validation confirms that a claim is being asserted, not that it’s legally collectible. Factors like expired statutes of limitations or prior bankruptcy can still make enforcement impossible.

3. Can a debt be validated but still incorrectly reported to credit bureaus?

Yes. Debt validation and credit reporting accuracy are governed by different laws. Errors on your credit report must be disputed separately under the Fair Credit Reporting Act (FCRA).

4. Is proof of debt ownership the same as proof you’re legally liable?

Ownership shows who holds the account, not necessarily that you’re contractually responsible, especially in cases involving identity theft or authorized-user disputes.

5. Does requesting validation affect the statute of limitations on the debt?

No. Requesting validation does not reset or pause the clock. However, payments or written acknowledgments made afterward can revive enforceability, depending on state law.