When Does the Collection Process Begin for Overdue Balances

Transform Your Financial Future

Contact UsFalling behind on a payment is a common occurrence for many of us. In fact, nearly 77 million Americans, about 35 percent of adults with a credit file, have debt reported in collections.

We understand how stressful it feels when reminders or calls about overdue balances start coming in. But knowing when the collection process actually begins can help you take control and avoid unnecessary worry.

This guide explains what to expect, when creditors typically act, and steps you can take to manage your situation calmly and confidently.

TL;DR

- The collection process often begins with reminder notices and escalates to third-party agencies if payments remain unpaid. Timelines vary by creditor and type of debt.

- Creditors may act as early as 30 days past due, but most send debts to collections after 90 to 180 days.

- Early warning signs include missed payment notices, changes in account status, and notifications about third-party collection involvement.

- Unpaid debts can appear on your credit report after 30 days and remain for up to seven years, affecting future borrowing.

- Acting early helps avoid added fees, protects your credit score, and may prevent legal action from creditors or agencies.

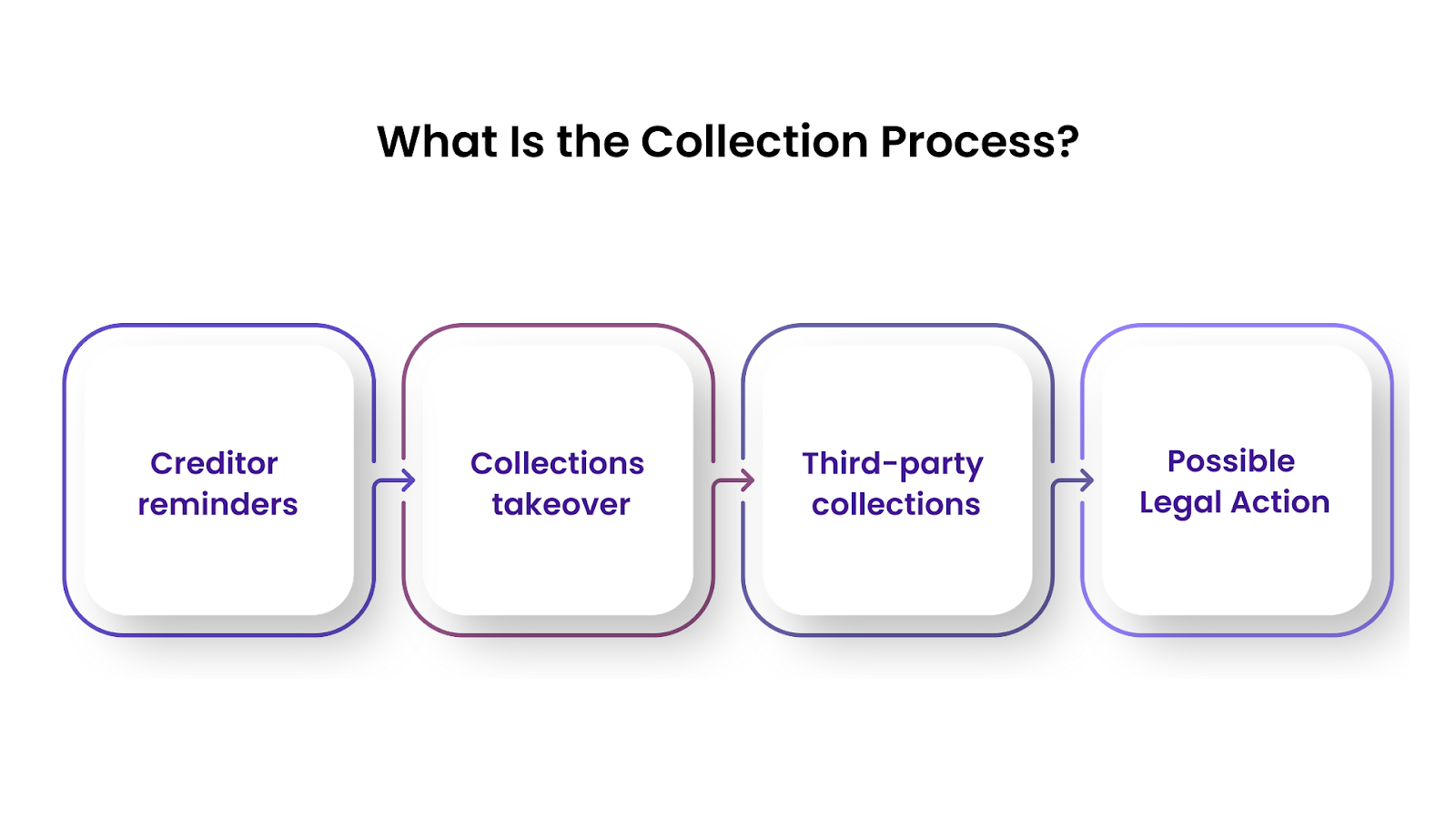

What Is the Collection Process?

When you miss a payment, creditors typically begin with small reminders before transitioning to a formal collection process. For individuals, this can feel intimidating, but it is important to understand that it is a step-by-step progression, not something that happens overnight.

Here is what typically happens during the collection process:

- Friendly Reminders from Your Creditor: You may first receive emails, calls, or letters requesting that you make the overdue payment. These are usually sent within the first 30–60 days after the due date.

- Internal Collections Team Takes Over: If the payment remains unpaid, the creditor’s internal collections team may start more consistent follow-ups to arrange repayment.

- Third-Party Collection Agencies Get Involved: After a certain point, typically 90 to 180 days, the creditor may transfer your debt to an outside collection agency. These agencies specialize in recovering overdue balances.

- Possible Legal Action: As a last resort, some creditors or agencies may consider legal action to recover the debt, although this is less common and typically occurs after numerous attempts to contact you.

Understanding these stages can make the process feel less overwhelming and help you recognize where you stand if you have fallen behind.

Now that you know how the collection process unfolds, you may wonder when it actually starts. Does it begin with that first reminder call, or only when an agency steps in? Let's take a closer look at the timelines and what triggers each stage so that you can feel more prepared and confident about your next steps.

Suggested Read: What Happens If You Miss a Payment on Consumer Easy Credit?

When Collections Begin: Timeline and Early Warning Signs

The collection process rarely starts with a sudden phone call from a debt collector. It usually unfolds gradually, starting with quiet nudges and only escalating when payments remain overdue. Recognizing these early signs and understanding typical timelines can help you take action before things spiral.

How Soon Can It Start?

The exact timing depends on the type of debt and the creditor’s internal policies. But here’s a general idea of when the collection process may begin:

- Credit Cards & Personal Loans:

Lenders may begin sending reminders as early as 30 days past the due date. By 60–90 days, they typically increase follow-ups. After 180 days, most charge off the debt and sell it to a collection agency. - Medical Bills:

Medical providers are often more lenient. They may wait 90+ days before initiating collections, but this varies depending on insurance delays or provider policies. - Utilities & Service Providers:

These can act quickly. Missed payments might trigger service disruptions within 30–60 days, and unpaid bills may move to collections soon after.

Early Warning Signs to Watch For

Even before your debt is formally transferred to a collection agency, there are clear red flags:

- Missed Payment Notices:

These may come as emails, letters, or text reminders—and they’re often your first opportunity to catch up before fees pile up. - Changes in Account Status:

You may lose access to credit or services. Online portals might reflect a “past due” or “delinquent” label on your account. - Collector Notification:

Some creditors will notify you before sending your debt to a third party. A letter or call mentioning an upcoming transfer is a strong signal that the clock is running out.

Understanding these timelines and warning signs allows you to act early, before late fees add up, your credit score takes a hit, or legal action becomes a risk.

Suggested Read: Calculating Financial Freedom Number using Passive Income Formula

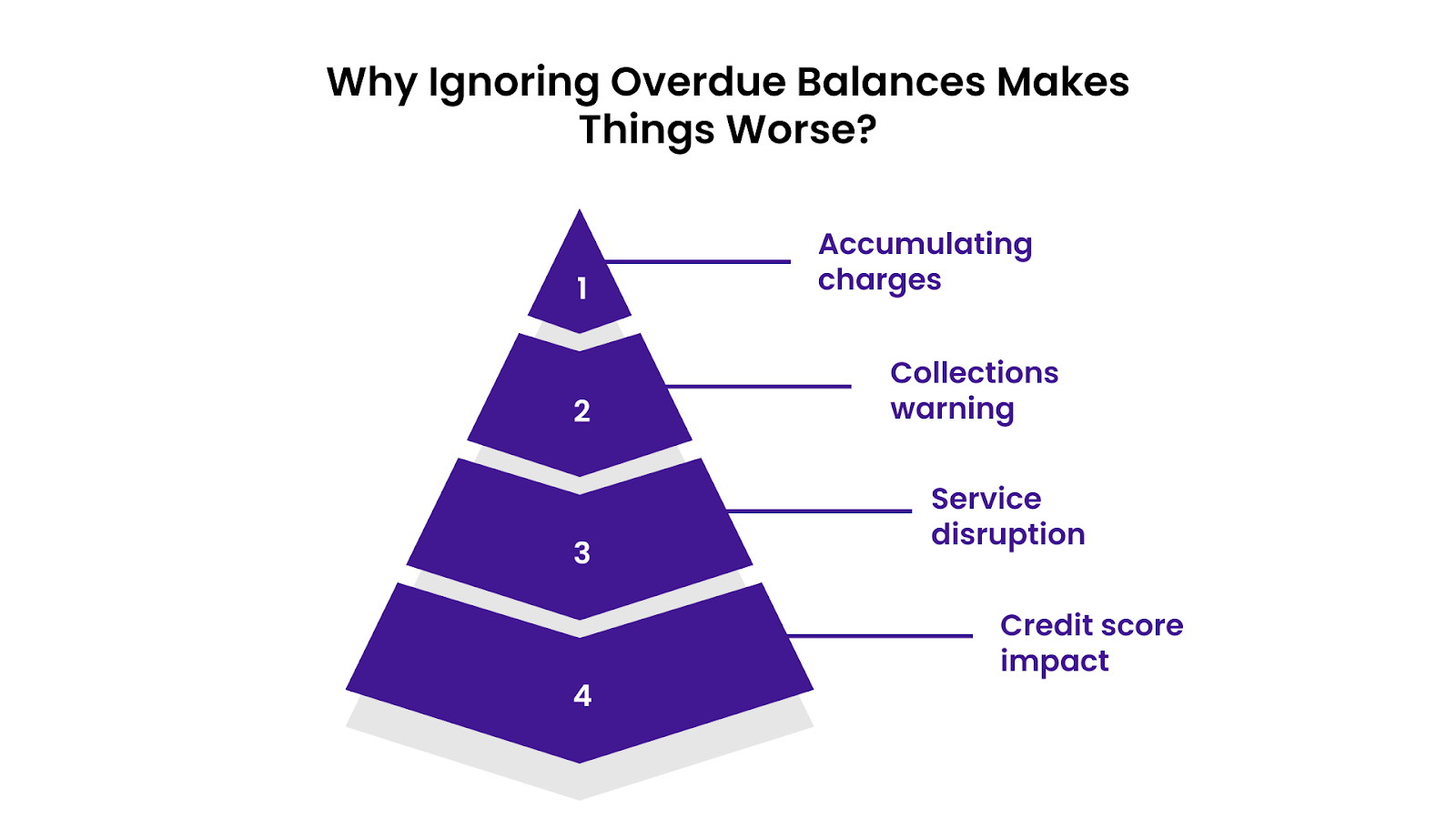

Why Ignoring Overdue Balances Makes Things Worse?

It is easy to put off dealing with overdue balances, especially when the situation feels overwhelming. But letting the debt sit too long often leads to added challenges that can be harder to manage later. Taking small steps early can save you time, money, and stress.

- Late Fees and Interest Keep Adding Up: As payments remain overdue, most creditors apply late fees and interest charges, increasing the total amount you owe.

- Your Account May Be Sent to Collections: After a specified period, creditors may transfer your debt to a collection agency, resulting in increased frequency of calls and letters.

- Potential Service Interruptions or Account Closures: For utilities or services, overdue accounts may result in service suspension or cancellation.

- Greater Impact on Your Credit Score: The longer a debt stays unpaid, the more it can harm your credit history, making future borrowing more difficult.

While these challenges can seem intimidating, understanding how and when overdue balances appear on your credit report can help you plan your next steps. Let's examine how credit reporting works and what you can do to minimize its impact.

How Long Before a Debt Affects Your Credit Report?

One of the primary concerns about overdue balances is their impact on your credit score. Knowing the timelines for credit reporting can help you take steps to limit the damage before it happens.

Most creditors wait until a payment is at least 30 days overdue before reporting it to the credit bureaus, such as Experian, Equifax, and TransUnion. Acting quickly within this window can prevent negative entries from being made. Once a debt is sent to a collection agency, it is usually reported and can remain on your credit report for up to seven years.

If you settle your overdue balance before the creditor reports it, you can avoid a hit to your credit score altogether. Understanding these timelines highlights the value of taking action early. The sooner you address overdue balances, the more options you have to avoid long-term consequences and keep your credit in good standing.

Steps You Can Take Before Your Debt Goes to Collections

If your account is past due but has not yet been sent to a collection agency, you still have time to act. Taking these steps early can help you avoid the added stress of collection calls and protect your credit score.

- Talk to Your Creditor Early: Many creditors are willing to work with you if you explain your situation. Ask about payment extensions, hardship programs, or modified repayment terms.

- Set Up a Payment Plan: Even partial payments can show good faith and sometimes prevent your account from being escalated.

- Review Your Budget and Prioritize Payments: Adjust your spending to focus on overdue accounts. Paying off smaller balances first can free up funds for larger debts.

- Seek Advice From a Nonprofit Credit Counselor: Credit counseling organizations can help you create a manageable repayment strategy and even negotiate with creditors on your behalf.

While these steps can often prevent collections, sometimes contact from a debt collector becomes unavoidable. Knowing your rights in these situations is crucial for handling calls and letters with confidence and protecting yourself from unfair practices.

Suggested Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2025 Update)

Understanding Your Rights When Dealing With Collectors

It can feel stressful to hear from a debt collector, but it is important to know you have legal rights that protect you. Understanding these protections can make the process less intimidating and help you respond with confidence.

- You Have the Right to Be Treated Fairly: Debt collectors cannot use harassment, threats, or abusive language when contacting you under the Fair Debt Collection Practices Act (FDCPA).

- You Can Request Verification of the Debt: If you are unsure about a debt, you can ask the collector to provide written proof before you make any payments.

- They Must Respect Your Communication Preferences: Collectors are not allowed to call you at unreasonable times (before 8 a.m. or after 9 p.m.) or at work if you ask them not to.

- You Can Dispute Incorrect Debts: If you believe the debt is not yours or the amount is wrong, you have the right to dispute it in writing within 30 days of first contact.

While knowing your rights gives you confidence, there are situations where handling collectors on your own can feel overwhelming. This is when reaching out for professional guidance might be the best next step to protect your financial well-being.

When Professional Help May Be Necessary?

Managing overdue balances can feel overwhelming, especially if you are juggling multiple debts or facing constant collection calls. Sometimes, getting professional support is the most effective way to regain control and reduce stress.

- You Are Struggling to Negotiate on Your Own: Debt professionals can communicate with creditors or collectors on your behalf to explore repayment plans or settlements.

- You Have Multiple Debts in Collections: When several accounts are overdue, a credit counselor or debt management company can help you organize and prioritize repayment.

- You Are Unsure About Your Legal Rights: Professionals can guide you on consumer protection laws and help you respond appropriately to collector contact.

- You want to Avoid Legal Action: Seeking help early can sometimes prevent creditors from taking further steps, like filing lawsuits.

The Forest Hill Management offers compassionate support if you are feeling uncertain about the next steps or need someone to help you handle the process. They can help you manage overdue balances and move forward with confidence.

The Forest Hill Management: Support for Overdue Balances

Dealing with overdue balances can feel isolating, but you do not have to manage it alone. The Forest Hill Management offers personalized support to help you address your debts with care, dignity, and a clear plan for the future.

Their approach combines expertise with compassion, making the process less stressful for individuals facing collection challenges.

1. Compassionate Debt Recovery

The team understands the emotional weight of debt and works to resolve balances in a respectful and empathetic manner. Their goal is to help individuals find solutions, rather than adding to their stress.

2. Flexible Repayment Options

The Forest Hill Management helps set up repayment plans that align with your financial situation, giving you more control over how you pay down overdue accounts.

3. Legal Compliance and Consumer Rights Focus

They ensure all interactions adhere to regulations like the Fair Debt Collection Practices Act (FDCPA), so you can feel confident your rights are protected throughout the process.

Whether you are in the early stages of overdue payments or already receiving collection calls, The Forest Hill Management can help you repay your debt with confidence. Their client-focused approach offers guidance, solutions, and peace of mind every step of the way.

Conclusion

Understanding when the collection process begins and the steps you can take early on can make a world of difference. By staying informed and proactive, you can avoid unnecessary stress and protect your financial future.

The Forest Hill Management is here to guide you through the process with compassion and expertise. From flexible repayment options to ensuring your rights are respected, we provide the support you need to handle overdue balances with confidence.

If you are facing challenges with overdue accounts, do not wait for things to escalate. Contact us today and take your first step toward financial peace of mind.

Frequently Asked Questions

1. How long before an unpaid bill goes to collection?

Creditors typically wait 90 to 180 days before sending unpaid bills to a collection agency. However, some industries, like utilities, may act sooner. Timelines vary by creditor, type of debt, and internal collection policies.

2. How does the collection process begin?

The process starts with reminders in the form of emails, calls, or letters from the creditor about overdue payments. If the debt remains unpaid, it escalates to internal collection teams and, eventually, third-party agencies handling recovery efforts.

3. How late does a payment have to be before it is sent to collections?

Most accounts are sent to collections after 90 to 180 days of nonpayment. For certain debts, such as utilities or medical bills, the timeline may vary depending on the provider's policies and local regulations.

4. How soon can a company send you to collections after a due date?

Some companies may refer accounts to collections as early as 30 days past due, though many wait 90 days or more before involving third-party collection agencies.

5. What is the 7-day rule for collections?

Under the Fair Debt Collection Practices Act (FDCPA), debt collectors must wait seven days after speaking with you about a debt before making another phone call regarding the same debt, unless you agree otherwise.