How to Analyze a Debt Portfolio Effectively

Transform Your Financial Future

Contact UsManaging a debt portfolio can feel complex, especially when balances grow and recovery rates fluctuate. In early 2025, U.S. commercial banks reported a delinquency rate (the percentage of loans or debts that are past due or have missed a payment) of 1.67% for loans and leases. This highlights how common portfolio challenges are, even for large institutions.

We understand that every debt portfolio tells a different story. Some accounts hold great potential for recovery, while others require careful analysis before any action is taken. Knowing how to evaluate your portfolio effectively helps you make smarter decisions, reduce risk, and improve financial outcomes.

In this guide, we will walk you through key metrics, practical steps, and tips to help you analyze your debt portfolio with confidence.

TL;DR

- Analyze a debt portfolio by reviewing account age, balances, delinquency trends, and debtor profiles.

- Key metrics like delinquency rates, account age, and recovery costs guide your strategy.

- Assess risk levels by reviewing debtor profiles, payment histories, and external economic factors.

- Avoid common pitfalls such as outdated data, poor segmentation, and compliance oversights.

What Is Debt Portfolio Analysis and Why Does It Matter?

Debt portfolio analysis helps you understand the accounts you manage and their potential for recovery. It's about identifying patterns, risks, and opportunities within your portfolio. By analyzing your portfolio, you can identify which accounts require immediate attention and which can be managed using a longer-term strategy.

This prevents wasted resources and improves overall recovery rates. We know it can feel overwhelming to sift through large amounts of data. However, with the right approach, you can transform that data into insights that inform more intelligent, more confident decisions.

Debt portfolio analysis is not just about numbers. It helps you protect your cash flow, meet regulatory requirements, and build stronger relationships with clients.

To start analyzing your portfolio effectively, you first need to know which metrics matter most. Focusing on the right data points can make your analysis faster, clearer, and more actionable.

Key Metrics to Examine in a Debt Portfolio

Knowing which metrics to track helps you understand the health of your debt portfolio. By focusing on these key areas, you can make informed decisions and effectively prioritize your collection efforts.

1. Age of Debt

Older debts are often harder to recover. Tracking account age helps you decide when to escalate efforts or consider alternative strategies.

Major credit reporting agencies, such as Experian, Equifax, and TransUnion, play a crucial role in tracking overdue accounts and reporting them on credit files when debts remain unpaid.

- Review aging reports regularly.

- Prioritize newer debts with higher recovery potential.

- Flag accounts nearing critical thresholds, such as charge-offs.

2. Account Balance Distribution

Understanding your portfolio’s balance spread can help allocate resources where they matter most.

- Group accounts into high-value and low-value segments.

- Focus intensive efforts on larger balances.

- Use automated tools for smaller accounts to reduce costs.

3. Debtor Profiles and Demographics

Analyzing who owes you helps tailor your approach and improve response rates.

- Segment by location, industry, or payment history.

- Spot trends in repayment behavior.

- Adjust communication strategies for different groups.

4. Historical Recovery Rates

Past performance often predicts future success. Use it to set expectations and improve strategies.

- Compare recovery rates across debt types and age brackets.

- Identify which methods worked best.

- Use insights to train teams or refine processes.

Once you know which metrics to track, the next step is putting them to work. A straightforward, step-by-step process can turn raw data into actionable insights for better portfolio management.

Suggested Read: How to Calculate and Improve Days in Accounts Receivable (A/R)

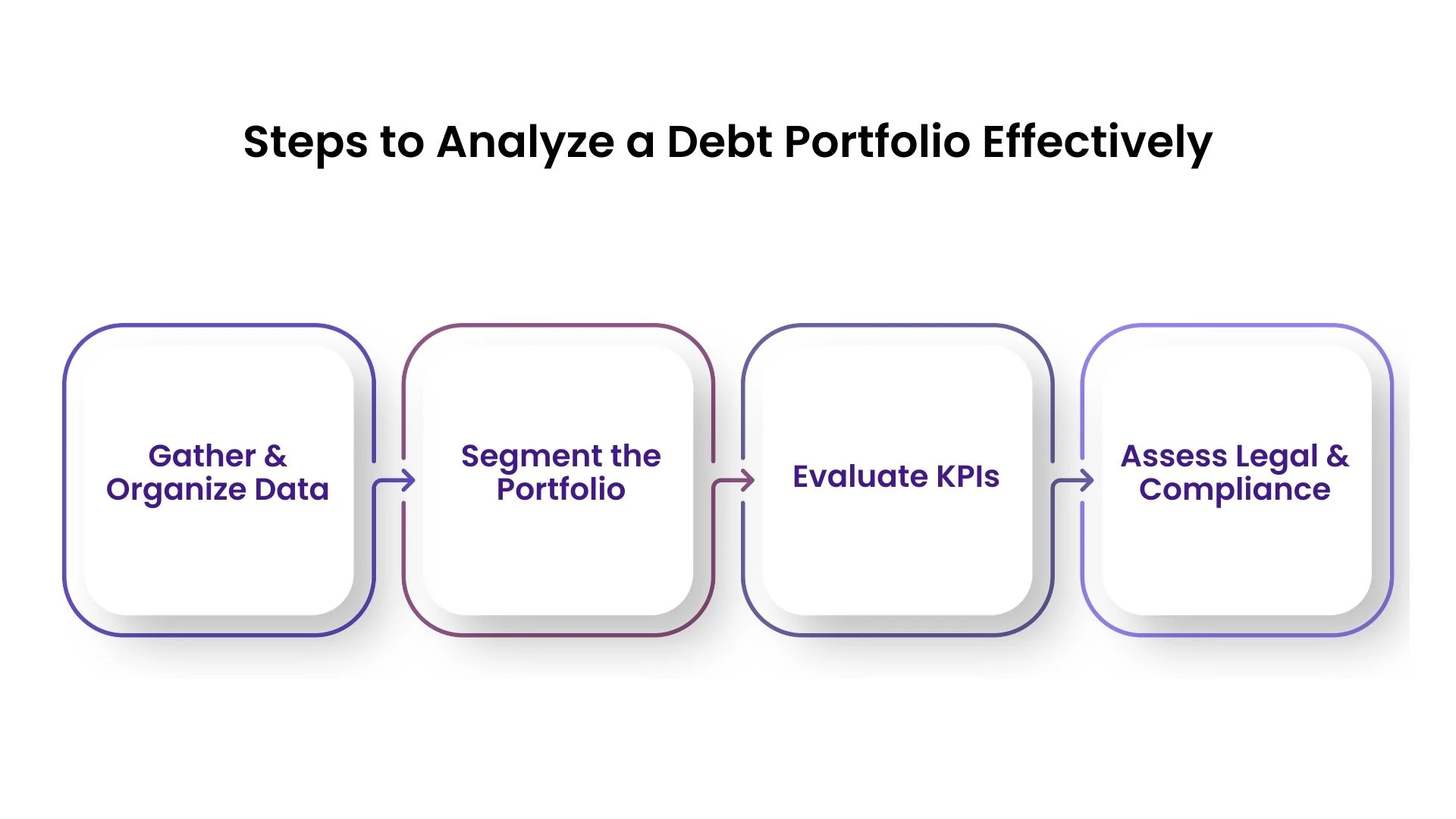

Steps to Analyze a Debt Portfolio Effectively

Breaking down the process into clear steps makes portfolio analysis easier to manage. Each stage builds on the last, helping you see the bigger picture and act with confidence.

1. Gather and Organize Your Data

Accurate data is the foundation of any analysis.

- Consolidate information from all systems and sources.

- Clean your data to remove duplicates or errors.

- Verify account details like balances, contact information, and payment history.

2. Segment the Portfolio

Grouping accounts helps tailor your strategies for different risk levels and recovery potential.

- Segment debts by age, size, or type (secured vs. unsecured).

- Create risk profiles for each segment.

- Prioritize accounts needing immediate attention.

3. Evaluate Key Performance Indicators (KPIs)

Tracking KPIs shows how well your portfolio performs and where improvements are needed.

- Monitor recovery rates, costs per recovery, and average days to collect.

- Compare metrics across segments to spot trends.

- Use results to guide team focus and resource allocation.

4. Assess Legal and Compliance Considerations

Ignoring legal risks can lead to costly mistakes.

- Review accounts for potential disputes or regulatory constraints.

- Check if debts fall under consumer protection laws like the FDCPA.

- Consult legal advisors when needed.

Following these steps gives you a clearer understanding of your portfolio’s strengths and challenges. It sets the stage for a deeper evaluation of potential risks.

Once you have organized and analyzed your portfolio, the next step is understanding its risk landscape. Assessing risk levels helps you prioritize accounts and create strategies that balance recovery potential with resource investment.

How to Assess Risk Levels in a Debt Portfolio

Assessing risk helps you determine which accounts require immediate attention and which may require a different approach. It gives you clarity and helps avoid wasted efforts.

Here are practical ways to evaluate risk in your portfolio:

- Review Account: Older accounts often have lower recovery chances. Flag debts nearing legal limitation periods or charge-off thresholds.

- Analyze Payment History: Accounts with sporadic or missed payments may require higher effort or alternate strategies.

- Check Debtor Profiles: Look at employment status, location, or industry trends to predict repayment likelihood.

- Monitor Economic Indicators: External factors, such as economic slowdowns, can affect a debtor's ability to pay. Adjust your expectations accordingly.

- Evaluate Legal Constraints: Some debts may carry risks like pending disputes or regulatory limits that impact collection feasibility.

Even with a solid process, it is easy to overlook critical details. Knowing the common mistakes in debt portfolio analysis can help you avoid setbacks and strengthen your overall strategy.

Suggested Read: Financial Management Tools to Strengthen Debt Collection

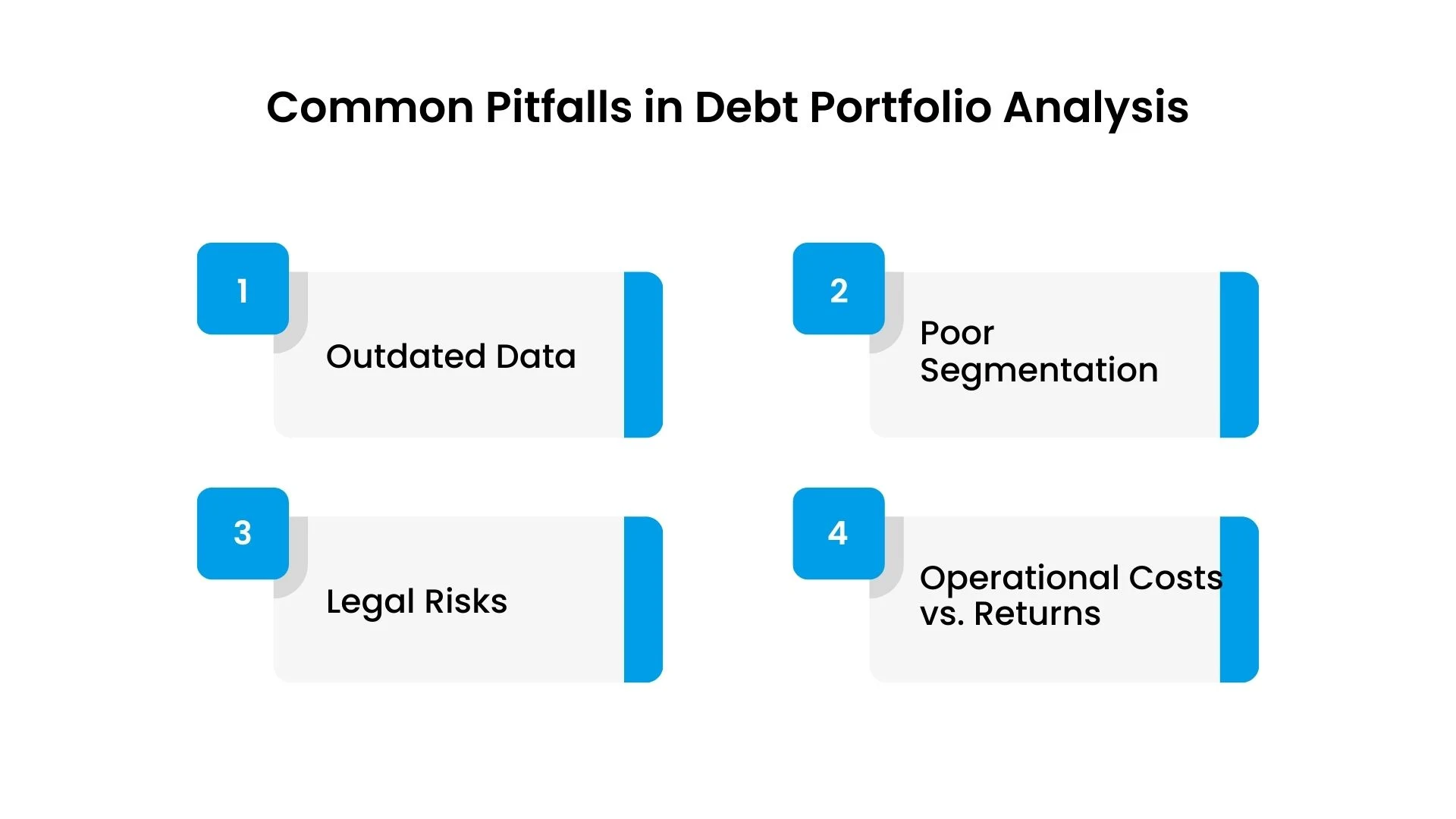

Common Pitfalls in Debt Portfolio Analysis

Overlooking these pitfalls may lead to missed opportunities, higher costs, and reduced recovery rates. Recognizing them early allows you to make smarter, more confident decisions.

Common challenges include:

1. Relying on Outdated or Incomplete Data

Many businesses work with data that is either outdated, missing critical details, or filled with errors. This can lead to incorrect risk assessments and poorly informed collection strategies. For example, an account marked as active might already have been settled.

- Solution: Regularly audit and update your portfolio data. Clean and verify debtor information, such as contact details and balances, before you begin the analysis. Using reliable data sources ensures your insights are both accurate and actionable.

2. Failing to Segment the Portfolio Effectively

Treating all accounts the same often leads to wasted resources. High-risk accounts can drain time and money, while low-risk accounts may be overlooked despite their potential for recovery. This one-size-fits-all approach rarely delivers good results.

- Solution: Divide your portfolio into clear segments based on factors like debt age, balance size, and debtor profiles. This helps you tailor strategies to each group, boosting efficiency and recovery rates.

3. Overlooking Compliance and Legal Risks

Failing to consider regulatory requirements can have serious consequences. Debts subject to consumer protection laws or disputes may expose your business to fines or legal challenges if mishandled.

- Solution: Integrate compliance checks into your portfolio analysis. Stay updated on laws like FDCPA or industry-specific regulations. Consulting legal experts for high-risk accounts adds an extra layer of protection.

4. Ignoring Operational Costs Versus Recovery Returns

Chasing every account, regardless of size or age, can result in spending more on recovery than the debt is worth. This reduces overall profitability and strains internal teams.

- Solution: Evaluate each account’s potential recovery value against the cost of collection. Focus your efforts on accounts with favorable cost-to-recovery ratios and consider outsourcing lower-value accounts to specialized agencies.

While analyzing your portfolio helps identify challenges, improving your payment terms can prevent many of those issues from arising in the first place. Flexible and fair terms encourage timely payments and reduce collection risks.

Using Insights to Build Better Collection Strategies

The real value of debt portfolio analysis lies in how you apply its insights. Once you understand patterns and risks, you can create more innovative, more effective strategies tailored to your portfolio’s needs.

Here are key ways to use your findings:

- Prioritize High-Value Accounts: Focus resources on accounts with the highest balances and strongest recovery potential. Use segmentation data to decide where intensive efforts will deliver the best returns.

- Develop Targeted Communication Plans: Tailor outreach strategies to different debtor groups. For example, newer accounts may respond well to gentle reminders, while older debts may require firm but fair negotiations.

- Adjust Recovery Timelines: Insights about account age and payment history can help you decide when to escalate efforts or consider alternative approaches like settlements or write-offs.

- Allocate Resources More Effectively: Assign your internal teams to manageable segments and outsource more complex or aged accounts to third-party agencies for better results.

- Enhance Staff Training: Share portfolio trends with your team. Training staff on segment-specific strategies leads to more consistent and professional recovery practices.

Building stronger strategies is important, but it must be done responsibly. Staying aligned with ethical practices and regulatory requirements protects your business and ensures positive relationships with debtors.

Suggested Read: Finance: Digital Transformation Predictions for the Future

Ethical and Regulatory Considerations in Portfolio Management

Ethics and compliance are as important as recovery rates. Responsible portfolio management protects your business from legal risks and strengthens relationships with customers and stakeholders.

Here are key areas to focus on:

- Follow Fair Debt Collection Practices: Ensure all collection efforts comply with laws like the Fair Debt Collection Practices Act (FDCPA). Avoid aggressive tactics that could harm your business reputation.

- Respect Debtor Privacy and Data Security: Safeguard personal and financial information. Stay compliant with data protection regulations such as GDPR and similar local laws.

- Adopt Transparent Communication: Clearly explain payment terms, balances, and recovery processes to debtors. Transparency builds trust and can encourage quicker resolution.

- Monitor Third-Party Agencies: If you outsource collections, ensure your partners follow ethical practices and maintain regulatory compliance. Perform regular audits to mitigate risks.

- Stay Updated on Regulatory Changes: Laws and industry standards evolve. Regular training and updates help your teams remain compliant and avoid unintentional violations.

Even with strong internal practices, managing complex or large-scale portfolios can be challenging. This is when partnering with experienced professionals can make a significant difference in outcomes and compliance.

When to Bring in Professional Portfolio Managers?

Managing a debt portfolio in-house can work for smaller volumes, but larger or more complex portfolios often require outside expertise. Knowing when to seek professional help can save time, reduce costs, and improve recovery results.

Here are signs it might be time:

- Rising Delinquency Rates: If overdue accounts are growing faster than your team can manage, a professional agency can provide the systems and resources needed to regain control.

- Limited Internal Resources: Managing data, compliance, and recovery strategies demands time and expertise. Outsourcing allows your staff to focus on core business priorities.

- Challenging Legal or Regulatory Landscapes: Complex portfolios across multiple jurisdictions may expose you to legal risks. Experts bring knowledge of regional laws and help maintain compliance.

- Need for Advanced Analytics and Tools: Professional managers often use sophisticated software and predictive models that can analyze portfolios more effectively than basic internal systems.

- Desire for Faster, Scalable Recovery Processes: Agencies can scale operations quickly to match your portfolio size, helping you avoid delays and improve cash flow.

Choosing the right partner makes all the difference. The Forest Hill Management offers professional, ethical, and tailored solutions to help you manage debt portfolios with confidence and care.

Conclusion

Analyzing and managing a debt portfolio effectively is no small task. From understanding key metrics to developing more effective collection strategies, each step helps you recover more. This is while strengthening relationships and protecting your business reputation. Staying proactive and ethical makes all the difference.

The Forest Hill Management brings the expertise, tools, and ethical practices businesses need to simplify portfolio challenges. With tailored recovery strategies, advanced analytics, and a focus on compliance, they help you achieve your debt recovery goals without compromising on trust or transparency.

Take the first step toward smarter portfolio management today. Contact us to explore personalized debt management solutions that fit your business needs.

Frequently Asked Questions

1. How to analyze a loan portfolio?

Review loan quality, borrower creditworthiness, repayment history, and portfolio diversification. Assess risks, delinquency trends, and compliance with lending policies to identify strengths, weaknesses, and opportunities for improvement.

2. How to analyze debt?

Evaluate outstanding balances, interest rates, repayment schedules, and aging reports. Segment debts by risk and recovery potential. Analyze historical collection performance and legal constraints to design effective recovery strategies and minimize losses.

3. How do you analyze a portfolio?

Examine asset allocation, performance metrics, and risk exposure. Compare portfolio goals with actual results. Assess diversification, potential returns, and market trends to determine adjustments that align with financial objectives and reduce vulnerabilities.

4. How to tell if a company has too much debt?

Check debt-to-equity and interest coverage ratios. Compare total liabilities against assets and cash flow. Excessive debt may signal repayment challenges, reduced financial flexibility, and a higher risk of default during economic downturns.