Impact of New Medical Debt Rules on Collections

Transform Your Financial Future

Contact UsMedical debt remains one of the most pressing financial challenges for individuals nationwide. In fact, it is now the number one type of debt in collections on credit reports, with nearly 58% of all bills in collections tied to medical expenses. Recent changes to medical debt reporting rules aim to give consumers a fairer chance at managing these obligations without immediate damage to their credit.

We understand how stressful it can be to juggle unexpected medical bills while managing other financial responsibilities. The weight of these debts often leads to sleepless nights and constant worry about the future.

In this guide, we will explore what these new rules mean, how they affect collections, and steps you can take to regain control of your financial health.

TL;DR

- The CFPB’s 2025 rule aims to remove medical debt from credit reports. However, its implementation has been delayed due to legal challenges.

- Medical debt often arises from emergencies and does not reflect financial responsibility, leading to calls for fairer treatment in credit reporting.

- While the rule protects credit scores, it does not erase the actual debt; unpaid medical bills remain legally collectable.

- Proactive steps, like verifying debts and negotiating with providers, can help manage medical bills and reduce the long-term financial impact.

What Is the New Medical Debt Rule?

The Consumer Financial Protection Bureau (CFPB) finalized a new rule in January 2025 aimed at transforming how medical debt is reported on credit reports. The rule seeks to protect consumers from long-term financial harm resulting from unexpected medical expenses, which are the leading cause of debt collections in the United States.

Here is what the rule changes:

- Medical debts of $500 or less will no longer appear on consumer credit reports.

- Paid medical debts should be removed from credit reports immediately, enabling individuals to repair their credit more quickly.

- Lenders are prohibited from considering medical debt when evaluating loan or credit applications.

This shift recognizes that medical debt often results from emergencies and does not accurately reflect a consumer’s ability or willingness to repay other obligations.

It is clear that the rule is designed to ease financial stress for millions of Americans. To understand why, let us explore why medical debt is treated differently from other debts.

Suggested Read: What Happens If You Miss a Payment on Consumer Easy Credit?

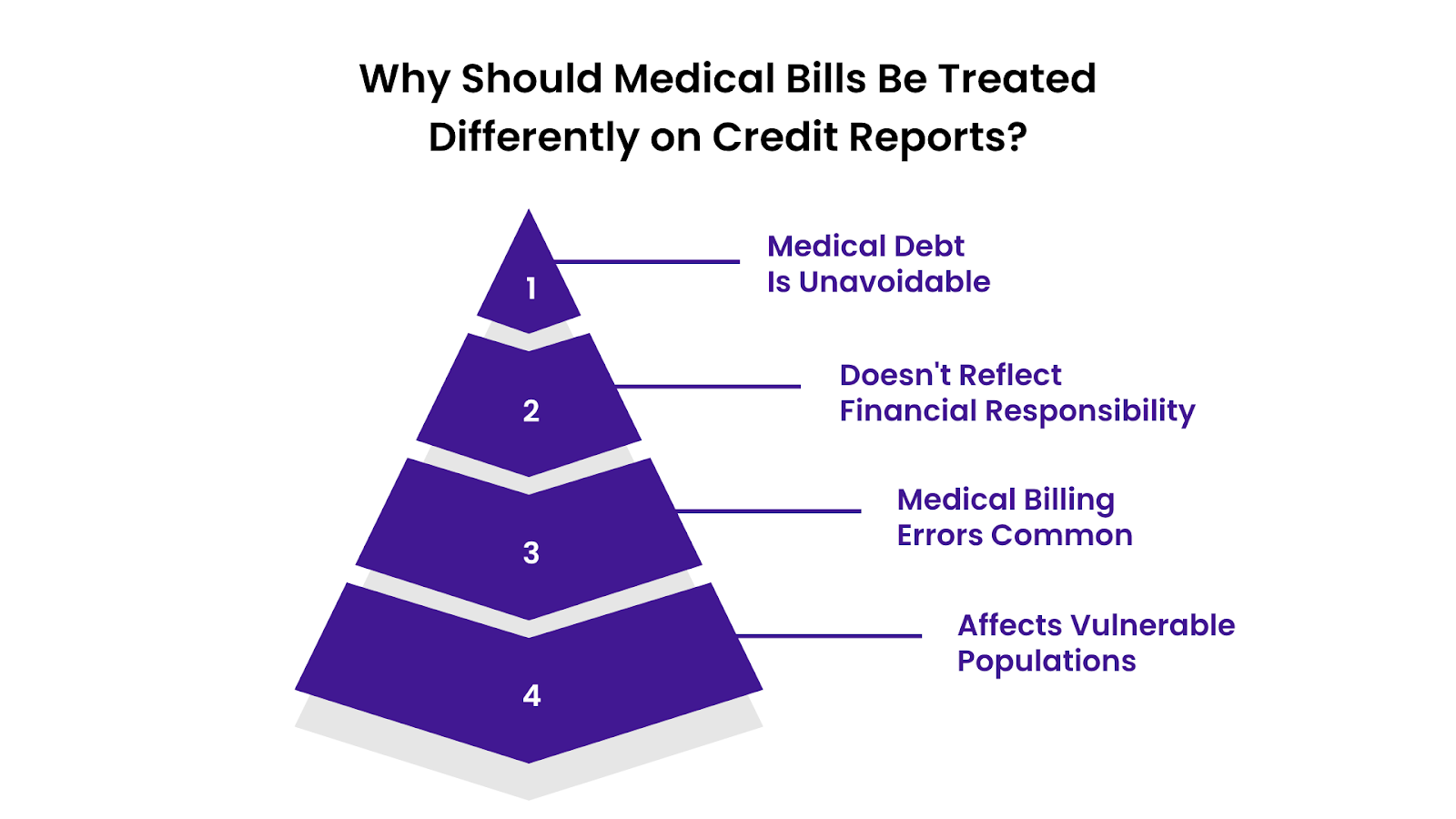

Why Should Medical Bills Be Treated Differently on Credit Reports?

For years, medical debt has been the leading cause of collections on credit reports. However, experts and regulators now recognize it as a unique type of debt. Here is why it deserves different treatment.

1. Medical Debt Is Often Unexpected and Unavoidable

Unlike credit card or personal loan debt, medical bills usually result from emergencies or urgent care. Consumers rarely have the chance to shop for prices or plan these expenses.

2. It Does Not Reflect Financial Responsibility

A poor credit score from unpaid medical bills often says more about someone’s health crisis than their ability to manage money. Removing it from credit reports helps prevent long-term financial harm.

3. High Error Rates Are Common in Medical Billing

Studies show that medical bills frequently contain errors or are sent to collections prematurely. Keeping these debts off credit reports reduces the unfair damage caused by inaccurate reporting.

4. It Disproportionately Affects Vulnerable Populations

Low-income families, the uninsured, and those with chronic illnesses often face the heaviest burden. Changing how medical debt is reported protects these groups from cycles of debt and poor credit.

With these reasons in mind, it is easier to understand why regulators are pushing for change. But where does the new rule stand today? Let us break it down.

Current Status of the New Medical Debt Rule

In 2022, Equifax, Experian, and TransUnion, which are the three major credit bureaus, took a significant step to ease the burden of medical debt. They removed nearly 70% of medical debt from consumer credit reports. This included debts that were paid off and medical collections under $500, giving millions of Americans immediate relief from credit score damage.

Although the CFPB finalized the rule in January 2025, it has not yet taken full effect due to ongoing legal challenges. Originally, the rule was scheduled to take effect in March 2025. However, a federal court issued a 90-day stay in response to a lawsuit, moving the effective date to June 15, 2025.

More recently, another court order has further delayed implementation, pushing the effective date to July 28, 2025. These delays mean that while the rule is finalized, consumers may not yet see its protections reflected in their credit reports.

For now, medical debts may still appear on credit reports, and lenders may continue factoring them into credit decisions until the rule officially takes effect.

Understanding the rule is one thing, but what does it mean for your credit, your medical bills, and your next steps? The next section discusses the impact of the new medical rule.

How Do These Changes Affect You?

The new medical debt rule is designed to provide consumers with fairer treatment regarding their financial health. Once it is fully active, it will influence how unpaid medical bills affect your credit, your repayment options, and your ability to access loans.

Here is what you can expect:

Your Credit Report Will Show Less Medical Debt

The rule changes how and when medical debt appears on your credit report. This could help protect your credit score from unnecessary damage.

- Medical debts under five hundred dollars will no longer be included in your credit report.

- Paid medical debts will be removed entirely, allowing your credit score to improve more quickly.

You Will Get More Time to Resolve Medical Bills

Consumers will now have additional time before unpaid medical bills are reported to credit bureaus. This can reduce the pressure to pay immediately.

- The reporting grace period has been extended to twelve months.

- This gives you a full year to pay or arrange a repayment plan without it affecting your credit.

Borrowing Money May Become Easier

When the rule takes effect, lenders will no longer be allowed to factor medical debt into their decisions. This could improve your chances of getting approved for loans or credit cards.

- Lenders must base their decisions on other aspects of your financial history.

- This change could especially benefit consumers with otherwise strong credit profiles who are burdened by medical bills.

These changes are designed to mitigate the long-term impact of medical debt and provide you with a fairer opportunity for financial recovery. While these changes bring relief, they do not mean medical debt will simply vanish. Let us take a closer look at what these rules really mean for your unpaid balances.

Suggested Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2025 Update)

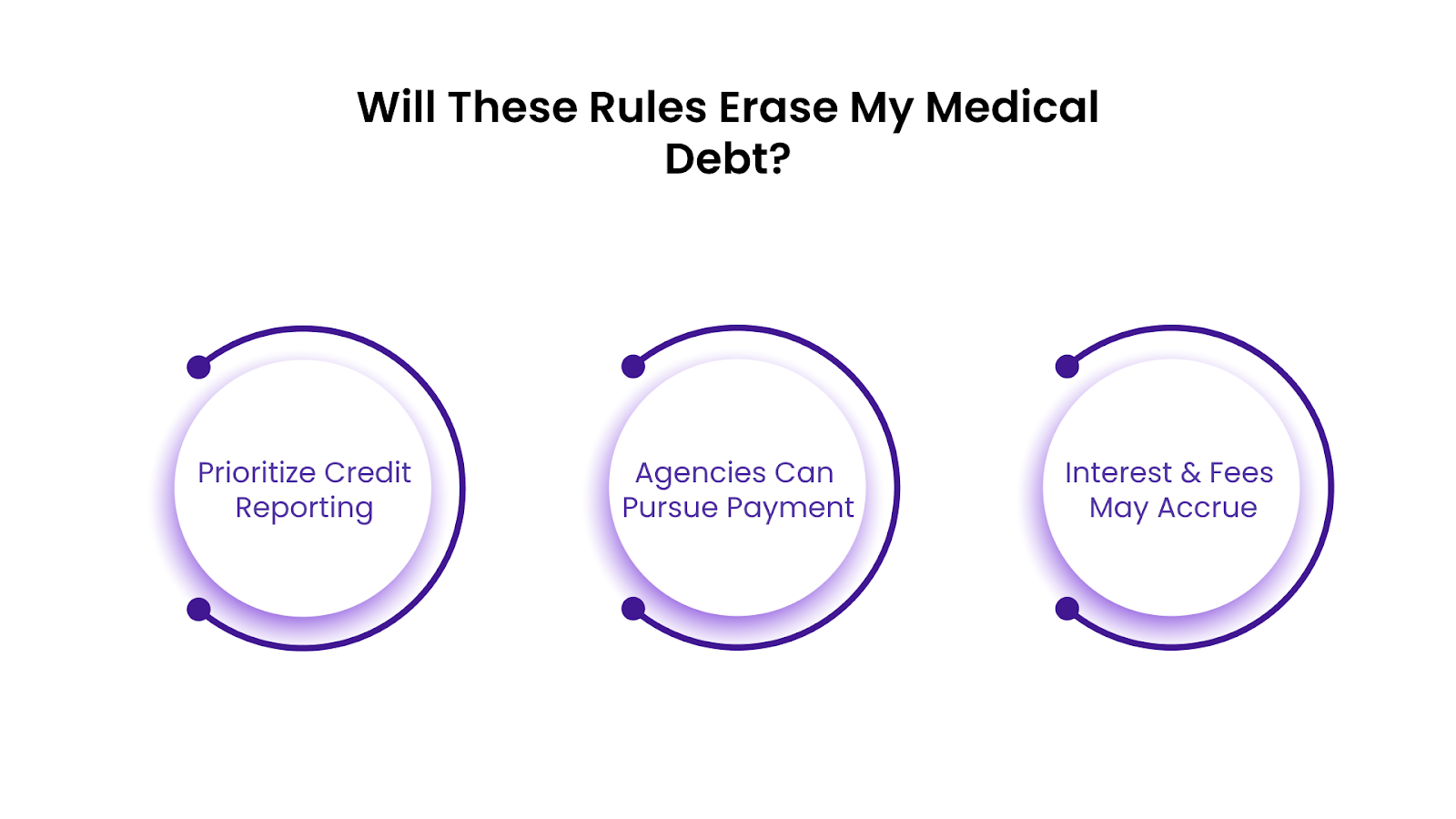

Will These Rules Erase My Medical Debt?

Many people assume the new medical debt rule will completely wipe out their unpaid medical bills. This is a common misunderstanding. The reality is that while the rule changes how medical debt appears on credit reports, it does not cancel the debt itself.

Focus on Credit Reporting, Not Debt Forgiveness

The new regulation is designed to protect your credit score by removing medical debts from your credit reports. However, the actual balances you owe to healthcare providers or collection agencies remain legally valid. You are still responsible for paying them.

Collection Agencies Can Still Pursue Payment

Even though medical debt may no longer harm your credit report, collection agencies retain the right to contact you about unpaid bills. They can still send notices, make phone calls, and, in some cases, pursue legal action if the debt is ignored.

Interest and Fees May Continue to Accumulate

Removing medical debt from your credit report does not prevent interest or late fees from being added to your account. These additional charges can increase your total balance over time if the debt remains unpaid.

Understanding these limits is crucial so that you can make the best decisions. Protecting your credit during medical debt challenges requires proactive steps and consistent monitoring. Let us now explore how you can protect your credit and manage medical bills more effectively in light of the new rule.

How to Protect Your Credit While Dealing With Medical Bills

The new medical debt rule offers some protection, but until it is entirely in effect, you still need to safeguard your credit score actively. Here are five practical steps to help you maintain a strong credit profile while managing medical bills.

- Review Your Credit Report: Check your credit report often to ensure medical debts are not inaccurately reported. Dispute any errors with the credit bureaus immediately to prevent unnecessary damage to your score.

- Communicate Early: Contact your provider as soon as you receive a bill. Many offer payment plans or financial assistance programs that can help you avoid collections altogether.

- Prioritize Payment Arrangements: Work out a payment agreement with the provider before the debt is sent to a collection agency. This reduces the chance of adverse reporting and added collection fees.

- Avoid Using Credit Cards: While it might seem like a quick fix, paying medical bills with credit cards can lead to high-interest debt that further harms your credit utilization ratio.

- Stay Current on Other Accounts: Even if medical debt is stressful, keeping up with other payments, like credit cards, auto loans, or mortgages, helps protect your overall credit health.

- Understand Your Rights: Learn what collectors can and cannot do under the Fair Debt Collection Practices Act (FDCPA).

These efforts will reduce long-term financial damage and give you more control over your financial future. Beyond protecting your credit, it is equally important to take practical steps in managing medical debt itself. Let's examine actionable tips for managing medical bills in 2025 and beyond in the next section.

Tips for Managing Medical Debt in 2025 and Beyond

Many people approach medical debt with outdated assumptions, often leading to unnecessary stress or financial missteps. In 2025, with new rules and evolving practices, it is time to rethink how to handle medical bills effectively.

Let us break down common myths and share strategies that work.

Myth: Medical Debt Will Automatically Disappear

Reality: While the new rule removes medical debt from credit reports, the debt itself still exists. You are still responsible for payment unless forgiven by the provider. Contact your healthcare provider or collection agency to set up a payment plan. Ask if they offer income-based reductions or hardship programs.

Myth: Ignoring Medical Bills Buys You Time

Reality: Delaying payment often leads to higher balances due to interest or fees. Reach out early to negotiate or apply for financial assistance. Call the billing office within 30 days of receiving a bill. Request an itemized statement and dispute any errors before making payment arrangements.

Myth: All Providers Treat Debt the Same Way

Reality: Policies vary widely. Some hospitals have robust charity programs, while others send unpaid bills quickly to collections. Always ask about hardship options. Before your account is sent to collections, inquire about hospital charity care policies or sliding scale discounts. Apply as soon as possible.

Myth: Debt Settlement Companies Are Your Best Option

Reality: Many charge high fees and often fail to deliver promised results. Direct negotiation with your provider or nonprofit credit counselors is usually safer. Contact a nonprofit credit counseling agency for advice. They can help you create a budget and negotiate with providers without charging high fees.

Myth: You Cannot Negotiate Medical Costs After Receiving a Bill

Reality: Many providers are willing to reduce charges or set up affordable payment plans, even after sending a bill, if you ask proactively. Call and explain your financial situation. Offer to pay a portion upfront in exchange for a reduced total or request a zero-interest payment plan.

Challenging these common myths is key to managing medical debt effectively in 2025. But what if a debt collector has already contacted you about unpaid medical bills? The following section explains how to respond and protect yourself during these interactions.

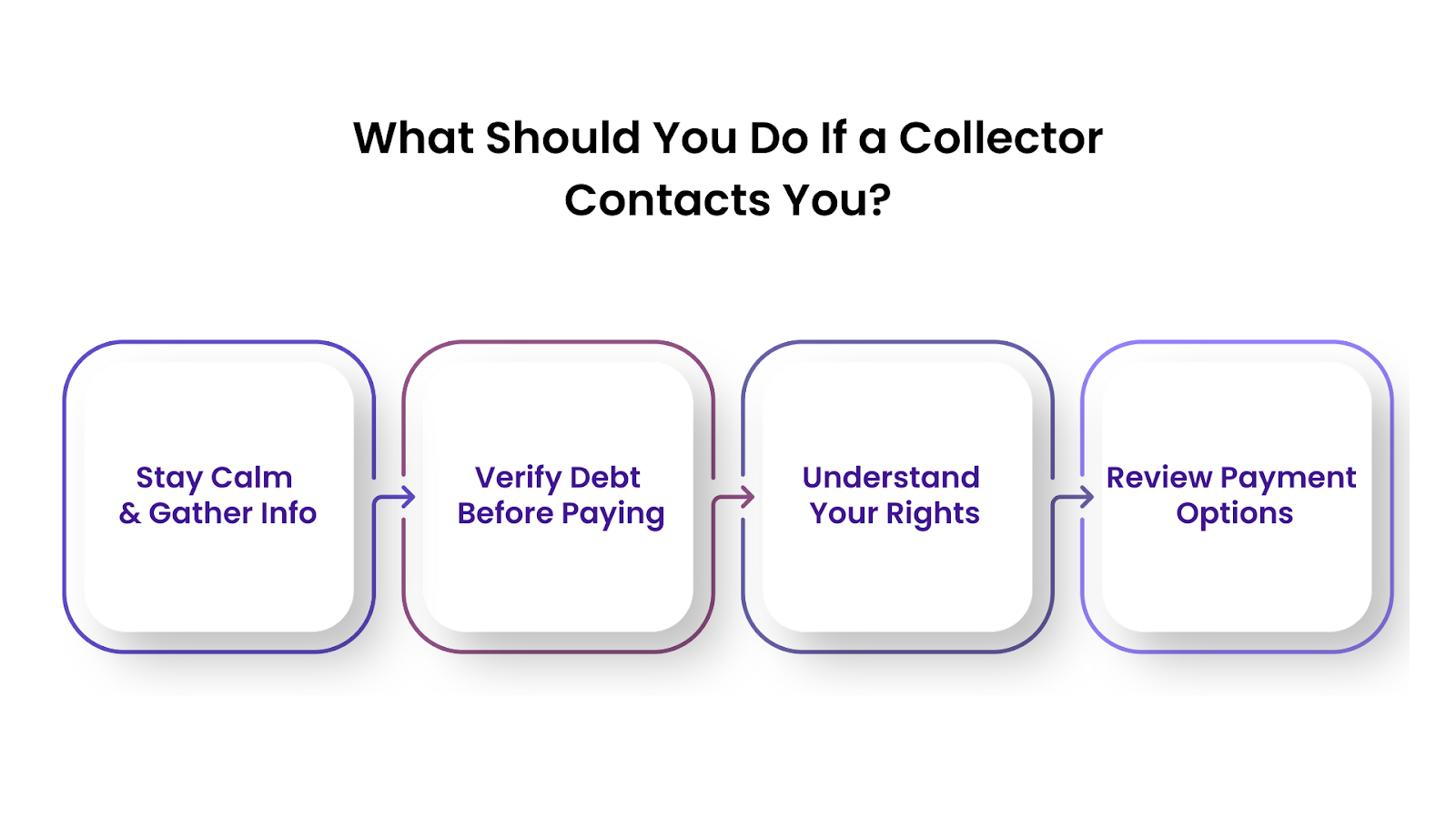

What Should You Do If a Collector Contacts You?

Hearing from a debt collector can be stressful, but knowing how to respond can help you protect your rights and prevent the situation from worsening. Here is how to handle the process with confidence and responsibility.

Stay Calm and Gather Information

Your first step is to avoid panic and collect details about the debt. Take time to understand what the collector is asking before taking any action.

- Ask for the name of the collection agency and the original creditor.

- Request the amount owed and the date of the original debt.

- Take notes during the call and save any written communication for your records.

Verify the Debt Before Paying

Never agree to pay or share personal financial information until you confirm the debt is valid. Collectors are legally required to provide proof.

- Request a written debt validation notice within 30 days of initial contact.

- Compare the details with your records to verify accuracy and identify any errors or duplicates.

- If the debt is not yours, dispute it in writing with the collection agency and credit bureaus.

Know Your Rights Under the Law

Federal and state laws protect you from harassment and unfair practices. Being informed helps you take control of the conversation.

- The Fair Debt Collection Practices Act (FDCPA) prohibits the use of abusive, threatening, or deceptive collection tactics.

- Collectors cannot call before 8 AM or after 9 PM unless you agree.

- You can request in writing that the collector stop contacting you.

Explore Your Payment Options Carefully

Once the debt is verified, plan your next steps based on your financial situation. Avoid rushing into agreements that might harm you later.

- Negotiate for a lower lump-sum payment or a structured payment plan.

- Ask if the agency will report the debt as “paid in full” after settlement.

- Consider speaking with a nonprofit credit counselor for guidance.

Responding to a debt collector strategically can prevent further damage to your finances and give you time to resolve the issue effectively. While these steps can help you handle debt collectors on your own, having expert support can make the process far less stressful.

At The Forest Hill Management, we offer compassionate, tailored solutions to help you handle medical debt and regain control of your finances.

The Forest Hill Management Can Help

Dealing with medical debt can feel overwhelming, especially when collection calls and credit concerns keep adding to the stress. At The Forest Hill Management, we understand these challenges and offer solutions that focus on reducing your financial burden while protecting your peace of mind.

Personalized Debt Resolution Plans

Every situation is unique. That is why we create custom strategies to address your specific medical debt challenges. Whether negotiating with providers or exploring repayment options, our team works to find a solution that suits your needs and financial capacity.

Advocacy With Creditors and Collectors

Speaking with creditors or collection agencies can be intimidating. Our experts step in as your advocates, communicating on your behalf to negotiate settlements, halt harassment, and help you regain control of your financial situation.

Financial Education and Guidance

We believe knowledge is power when it comes to debt management. Alongside our services, we offer resources and guidance to help you understand your rights, avoid common pitfalls, and make informed financial decisions moving forward.

At The Forest Hill Management, we are committed to supporting you through the challenges of medical debt. With compassionate guidance and practical solutions, we help you move closer to financial freedom and peace of mind.

Conclusion

Tackling medical debt in 2025 requires understanding the new rules, staying proactive about your credit, and taking steps to manage unpaid bills effectively. From learning how medical debt impacts your credit report to knowing your rights when dealing with collectors, every action you take can help secure your financial future.

At The Forest Hill Management, we are here to guide you through this process with personalized debt resolution plans, skilled negotiation with creditors, and financial education to help you make informed decisions. Our team works to reduce your stress, protect your credit, and help you get back on the path to financial recovery.

Take control of your medical debt today. Contact us to explore your options and discover a solution that suits your needs.

Frequently Asked Questions

1. What is the new rule for medical collections on credit reports in 2025?

The CFPB’s 2025 rule removes medical debt from credit reports and prohibits lenders from considering it in credit decisions. However, the rule’s implementation is delayed due to legal challenges and is not yet entirely in effect.

2. Are medical bills going to collections a bad thing?

Yes, unpaid medical bills sent to collections can negatively impact your credit, result in additional fees, and lead to increased collection calls. The new rule aims to reduce credit score damage, but you still owe the debt until it is resolved.

3. Are medical bills no longer affecting credit scores?

Not entirely. The 2025 rule will remove medical debts from credit reports, but until it is fully enforced, some medical debts may still impact your score. Paid debts and small balances under $500 are already excluded under earlier changes.

4. Is it a HIPAA violation for medical bills to go to collections?

No. HIPAA protects your health information, but it does not prevent providers from sending unpaid bills to collections. However, collectors cannot disclose your medical details to unauthorized parties while pursuing payment.