10 Successful Debt Collection Techniques for Maximizing Success

Transform Your Financial Future

Contact UsRecovery rates are stagnating. For many collection agencies, the gap between consumer contact and actual resolution continues to widen. According to Kentley Insights’ 2025 Collection Agencies Industry Report, the U.S. collection sector reached $23.2 billion. Growth was driven by rising consumer debt and increased demand for specialized recovery services.

Yet despite this expansion, many agencies face persistent operational bottlenecks. Outreach models are outdated. Agent training is inconsistent. Segmentation strategies often fail to convert engagement into resolution.

As consumer debt increases and delinquency timelines extend, you must innovate to resolve accounts more efficiently, compliantly, and with reduced resources. This blog shares 10 successful debt collection techniques that accelerate recovery.

Overview:

- Effective debt collection relies on a mix of strategies, including predictive scoring to prioritize accounts, multi-channel automated outreach, customized payment plans, structured escalation frameworks, and portfolio analytics to maximize recovery.

- Having a clear, data-driven collection strategy is essential because it reduces wasted effort, minimizes aging accounts, and ensures compliance with regulatory requirements, ultimately improving overall recovery rates.

- Regular compliance audits and verification processes help prevent legal issues and maintain credibility while ensuring that collection practices remain aligned with regulations.

- Integrating skip tracing and alternative data sources improves contact rates and recovery timelines for hard-to-reach debtors.

- Selling or outsourcing aged portfolios strategically can optimize cash flow, reduce internal administrative burden, and leverage specialized expertise for better returns.

Core Principles Behind Successful Debt Recovery

A successful debt recovery strategy relies on structure, empathy, and data-driven decision-making. Businesses that recover debts effectively follow consistent practices that balance client relationships with financial accountability.

These principles ensure that every interaction, whether automated or personal, contributes to faster resolutions and better recovery rates.

Key aspects include:

- Early Intervention Matters. The sooner communication begins after an account becomes overdue, the higher the likelihood of recovery and client cooperation.

- Personalization Drives Results. Tailoring outreach based on payment history, tone, and customer profile yields stronger engagement and reduces escalations.

- Data Transparency Improves Decisions. Maintaining updated debtor information and tracking recovery metrics helps identify what works and where to intervene.

- Compliance Protects Credibility. Adhering to regulations like the FDCPA and local data protection laws builds long-term trust with both clients and borrowers.

- Collaboration Strengthens Recovery. Sharing insights between finance, sales, and recovery teams ensures a consistent message and faster settlements.

When these foundational principles guide your recovery process, collection efforts become systems for sustained cash flow and reliability. Now, let us look at successful debt collection techniques that have consistently delivered measurable results.

Next, let us explore common mistakes that can quietly erode the effectiveness of even the most advanced debt collection programs.

Suggested Read: How FinTech Is Transforming Debt Collection in 2025

Common Mistakes That Slow Down Debt Collections

Even the most advanced collection program using successful debt collection techniques can underperform when operational blind spots go unchecked.

Small inefficiencies can compound over time, resulting in slower recoveries, reduced contact rates, and weakened client trust. Identifying these issues early helps maintain collection momentum and protect your bottom line.

Table showing debt recovery mistakes and their fixes:

When these mistakes persist, recovery efforts lose precision and scalability. To strengthen your internal process:

- Audit account data regularly to eliminate invalid contacts or outdated debtor profiles.

- Automate performance tracking to help managers identify and address weak spots before they escalate.

- Invest in compliance and communication training to keep teams aligned with industry regulations.

These corrective measures can significantly raise recovery rates, but maintaining them consistently requires ongoing resources and oversight.

That is why, for many businesses, it makes more financial and operational sense to transfer uncollected or aged accounts to a recovery partner. This approach not only accelerates collection timelines but also allows internal teams to focus on core operations without administrative drag.

Let’s explore a few proven debt collection strategies that can help improve recovery success.

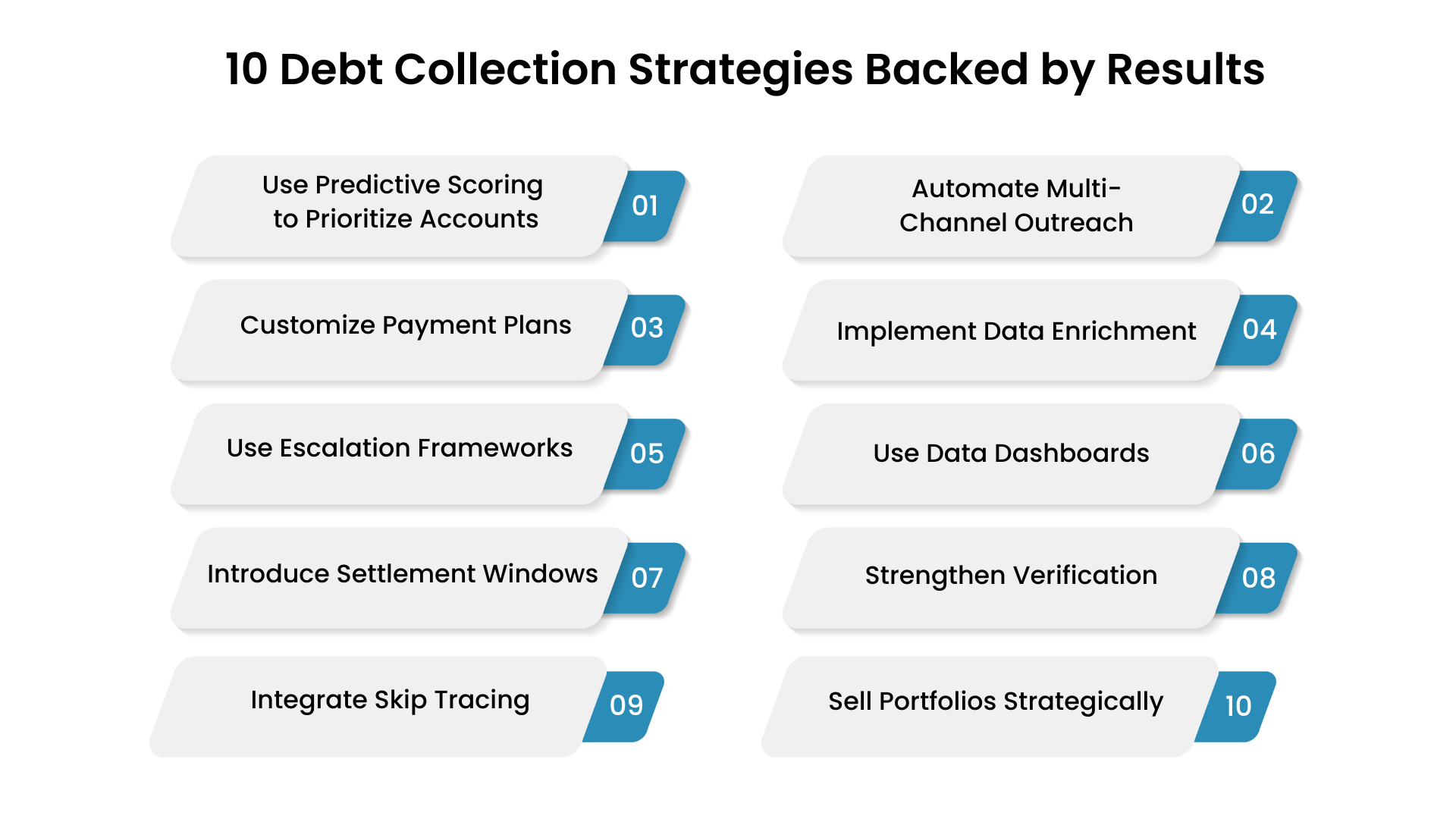

10 Debt Collection Strategies Backed by Results

The best-performing collection teams blend automation with empathy. They use analytics and structured follow-up frameworks to convert overdue accounts into recoveries—without damaging business relationships.

Proven results across diverse industries support the following ten strategies, which can be implemented at scale to enhance efficiency and accountability.

1. Use Predictive Scoring to Prioritize Accounts

Predictive analytics can identify which debtors are most likely to pay based on behavioral and financial data. Prioritizing accounts through AI-driven scoring saves time and focuses efforts where they are most effective.

- Combine demographic, payment history, and credit data for higher accuracy.

- Adjust scoring models periodically based on new repayment patterns.

- Integrate with CRM or collection software to trigger tiered follow-up actions automatically.

Pro Insight: Recalibrating your model every 90 days ensures it reflects real-time borrower behavior and macroeconomic shifts—preventing wasted effort on low-yield accounts.

2. Automate Multi-Channel Outreach

Automation allows teams to maintain consistent communication without overwhelming agents. Using email, SMS, and voice simultaneously ensures debtors receive timely reminders in their preferred format.

- Use variable message timing to avoid message fatigue.

- Automate reminders that escalate tone progressively but remain compliant.

- Track open rates and responses to identify the most effective channels.

Implementation Tip: Pair automation with human follow-ups for high-value accounts. Hybrid outreach models consistently outperform single-channel automation by 25–30%.

3. Customize Payment Plans

Behavioral segmentation helps tailor repayment plans to individual debtor profiles. Offering flexible structures improves recovery while maintaining client goodwill.

- Analyze past engagement patterns before proposing repayment terms.

- Offer variable installments based on income cycles (weekly, biweekly, etc.).

- Use A/B testing to determine which payment plan options drive better commitment.

Pro Insight: Gamified repayment milestones (such as progress dashboards) increase payment adherence—particularly among younger demographics used to visual tracking tools.

Forest Hill Management is known for offering flexible repayment plans that are custom-built for maximum recovery. Our empathetic and data-driven approach is based on a deep understanding of debtor behavior. Connect with our recovery team today to turn uncollected accounts into sustainable results.

4. Implement Data Enrichment

Outdated or incomplete debtor information is one of the main causes of stalled collections. Data enrichment tools fill gaps and correct inaccuracies across databases.

- Regularly update addresses, phone numbers, and employment details.

- Validate contact data through third-party verification services.

- Cross-reference databases to ensure multi-source accuracy.

Automating data refresh cycles at the start of every quarter can improve your data accuracy by 2.1%.

5. Use Escalation Frameworks Instead of One-Off Follow-Ups

Structured escalation frameworks introduce predictable, compliant next steps when a debtor fails to respond. This prevents delays and keeps the process transparent.

- Set clear thresholds for escalation (e.g., no contact after 14 days).

- Define escalation types into manager review, legal notice, or skip tracing.

- Log every escalation in a centralized system for audit readiness.

Pro Insight: Visual escalation dashboards enable managers to identify drop-offs early, thereby turning reactive supervision into preventive management.

6. Use Data Dashboards to Monitor Collection KPIs

Real-time dashboards reveal performance trends and recovery bottlenecks. They help management allocate resources to deliver the best results.

- Track key metrics such as Days Sales Outstanding (DSO), Promise-to-Pay ratio, and Recovery Rate.

- Compare agent-level performance for training and improvement.

- Set automated alerts for accounts that fall below the target recovery probability.

Implementation Tip: Combine operational KPIs with behavioral metrics (like average response time or message tone shifts) to gain a fuller picture of debtor intent.

Suggested Read: How to Automate Complex Collection Processes Step-by-Step

7. Introduce Settlement Windows for Faster Conversions

Short-term settlement offers can push undecided debtors to act quickly. When positioned strategically, these offers reduce long-term aging accounts.

- Offer limited-time discounts for lump-sum settlements.

- Automate reminder messages as deadlines approach.

- Use historical data to time these offers when payment probability peaks.

Pro Insight: Limit these windows to 10–14 days to maximize urgency. Anything longer reduces the psychological impact and conversion rate.

8. Strengthen Verification and Compliance Audits

Regular compliance audits reduce the risk of legal disputes and protect the agency’s credibility. Verification ensures all communications and processes align with current regulations.

- Audit call logs and correspondence to ensure FDCPA and GDPR compliance.

- Train collectors should regularly update their knowledge on legal frameworks.

- Maintain detailed audit trails for every account.

Implementation Tip: Conducting a quarterly mock audit to simulate an external review helps identify procedural errors before they escalate into violations. You should also consider integrating a compliance management system.

At Forest Hill Management, compliance is not an afterthought. It is the foundation of every recovery strategy we execute. Our internal audit systems and verification checkpoints ensure that every interaction stands up to regulatory scrutiny while preserving the client’s reputation. Get in touch with us today to learn more.

9. Integrate Skip Tracing and Alternative Data Sources

Utilize advanced skip tracing tools to access public records, utility data, and social activity, helping locate unresponsive debtors. This improves contact rates and recovery timelines.

- Combine skip tracing with predictive modeling for more accurate targeting.

- Use alternative data (e.g., rental or subscription payments) for trace verification.

- Ensure all data collection methods comply with privacy laws.

Pro Insight: Pair skip tracing with AI-driven pattern recognition to flag potential “data dead ends” before resources are wasted on unreachable leads.

10. Outsource or Sell Portfolios Strategically

When internal recovery costs exceed expected returns, outsourcing or selling portfolios to collection agencies ensures continued cash flow without internal strain.

- Evaluate the ROI of outsourcing versus in-house collection.

- Use agencies that specialize in specific account types (e.g., aged debt).

- Structure agreements with performance-based fees to maintain accountability.

Implementation Tip: Before selling a portfolio, conduct a micro-audit to remove accounts with active negotiations—these often yield higher returns through continued internal effort.

By combining advanced analytics with transparent communication, Forest Hill Management helps creditors recover more while maintaining their reputation and client relationships.

Suggested Read: The Role of Artificial Intelligence in Enhancing Compliance in Debt Collection

Maximize Returns on Your Aged or Uncollected Accounts

Recovering value from delinquent or stagnant accounts can be complex, especially when regulatory compliance, cost of pursuit, and diminishing returns come into play. Forest Hill Management can convert your uncollected portfolios into liquid assets through a strategic, compliant, and data-driven approach.

Our core services:

- Portfolio Acquisition: We purchase aged or uncollected debt portfolios directly, providing creditors with immediate liquidity and eliminating the burden of long-term collection cycles.

- Regulatory Compliance: Our processes adhere to all significant debt collection and data protection regulations, including FDCPA and GDPR, ensuring ethical and lawful recovery.

- Advanced Analytics: Using behavioral scoring and modeling, we determine optimal recovery strategies for each portfolio segment, maximizing yield with minimal friction.

- Recovery Models: We create repayment structures based on debtor affordability and case complexity, improving both recovery rates and consumer goodwill.

- Transparent Reporting: Clients receive detailed performance and compliance reports that provide full visibility into the recovery process, reinforcing accountability at every stage.

By selling or transferring accounts to Forest Hill Management, you can reduce regulatory exposure, improve cash flow, and eliminate administrative overhead. Our rigorous compliance standards and empathetic recovery framework ensure that every collection effort aligns with your brand values.

Conclusion

Uncollected or aging accounts tie up capital and increase administrative costs. There is also the risk of bad debt, which can leave businesses frustrated and limit their growth potential. Implementing strategic, compliant collection techniques ensures that outstanding debts are recovered efficiently without damaging client relationships.

Forest Hill Management helps businesses turn uncollected accounts into actionable assets. With our flexible, data-driven, and compliance-focused approach, we structure recovery efforts that are both effective and respectful of debtors.

Optimize your collections, protect your brand, and maximize returns. Contact our team to explore a plan or other successful debt collection techniques that can meet your portfolio’s needs.

Frequently Asked Questions

1. What industries see the highest success with outsourced debt collection?

Success varies by industry; B2B, healthcare, and utilities often benefit most due to predictable payment structures and regulatory clarity.

2. How long should I wait before considering outsourcing my accounts?

While it depends on internal capacity, many agencies consider outsourcing after 60–90 days of non-payment on high-value accounts.

3. Can debt collection strategies differ for domestic vs. international accounts?

Yes, international accounts require compliance with local regulations, currency management, and culturally sensitive communication strategies.

4. What role do credit reporting agencies play in accelerating debt recovery?

Reporting delinquent accounts to credit bureaus can increase accountability and encourage repayment, especially for long-term or repeat debtors.

5. Are there tax implications when selling or outsourcing debt portfolios?

Yes, selling accounts may trigger gains or losses for accounting purposes; consulting a tax advisor ensures compliance and accurate reporting.

6. What is the 11-word phrase to stop debt collectors?

The 11-word phrase is: “I am requesting that you cease all communication with me.”

Under the Fair Debt Collection Practices Act (FDCPA) in the U.S., sending this in writing instructs a debt collector to stop contacting the debtor. You can only contact the debtor in this case to notify them of specific actions, like legal proceedings.

7. What is the 7-7-7 rule in collections?

The 7-7-7 rule is a guideline for structured follow-ups. Contact the debtor 7 days after the initial due date, then 7 days later, and again 7 days after that. This approach balances persistence with compliance, giving debtors multiple opportunities to respond without overwhelming them or violating regulatory limits.