Understanding Medical Bills and Collections: Know Your Rights

Transform Your Financial Future

Contact UsMedical bills can often feel complicated, especially when they’re filled with confusing codes and unexpected charges. Many people struggle to figure out whether the charges are accurate or reflect the treatments they actually received. It’s common to see a number on a bill that doesn’t seem right, and that can lead to unnecessary stress.

In fact, more than $88 billion in medical debt is currently in collections, affecting one in five Americans.

In this article, you will understand how to check your medical bills for accuracy, what protections are available under laws like the No Surprises Act, and where to find financial assistance.

We’ll also explain what to do if your bills go to collections, outline your legal rights, and share tips on avoiding scams. With a clearer understanding of these points, you’ll be in a better position to manage your medical expenses and protect your financial health.

Key Takeaways

- Medical Bills Can Be Complicated: Errors are common in medical billing. It's crucial to thoroughly review each charge to avoid unnecessary debt collection and ensure you're not paying for services you didn’t receive.

- Know Your Rights and Protections: Laws like the No Surprises Act and the Fair Debt Collection Practices Act restrict abusive collection tactics. The Nursing Home Reform Act and Statute of Limitations also offer additional protections.

- Financial Assistance Is Available: There are multiple resources, hospital charity care programs, government assistance, and nonprofit organizations that help reduce or eliminate medical debt.

- Debt Collection Has Limits: Debt collectors must follow strict rules, including waiting at least 12 months before reporting unpaid medical debt to credit bureaus. You can request debt validation and stop unwanted contact at any time.

- Avoid Scams: Be cautious of anyone offering to erase your medical debt for a fee. Reputable credit counselors won’t pressure you into services. If you believe your rights have been violated, file a complaint with the CFPB or CMS.

What is the Medical Billing Process?

The medical billing process begins with verifying patient insurance details, coding diagnoses and procedures, and submitting claims to insurers. Once the insurance processes the claim, the provider receives payment or a denial.

If there is a remaining balance or a claim is denied, the patient is billed. If the debt goes unpaid, the provider may escalate the issue, sending the bill to collections after 90 to 180 days.

How to Verify the Accuracy of Your Medical Bills?

When dealing with medical bills, one of the first things you need to do is check the accuracy of your charges. Medical billing mistakes can range from simple data entry errors to charges for treatments you never received. Catching these mistakes early will save you from an unnecessary financial hit and from your bills being sent to collections.

Key steps to check your bills for accuracy:

- Review Each Line Item: Examine every charge to ensure it reflects the services or treatments you received.

- Compare to Explanation of Benefits (EOB): Cross-reference your bill with the EOB sent by your insurer to spot any discrepancies.

- Verify Treatment Dates: Make sure the dates listed on your bill align with when you actually received the treatment.

- Check Personal Information: Ensure your name, billing address, and insurance information are correct on the bill.

- Look for Duplicate Charges: Check to make sure you're not being charged more than once for the same service.

- Confirm Billing Codes: Ensure that the billing codes match the services you received.

This process may take a little time, but it’s worth the effort—especially when insurance networks and emergency care collide. Federal legislation has stepped in to address exactly this problem, offering protections that many patients don't realize exist.

Understanding Your Protections Under the No Surprises Act

The No Surprises Act, which took effect on January 1, 2022, was enacted to protect patients from unexpected medical bills, commonly known as "surprise billing", especially in emergency situations or when receiving care from out-of-network providers at in-network facilities.

Here are the key protections under the No Surprises Act that will help you avoid unnecessary financial strain and potential damage to your credit.

- Emergency Services: You cannot be billed more than your in-network cost-sharing amount for emergency services, even if provided by an out-of-network provider or facility.

- Non-Emergency Services at In-Network Facilities: If you receive non-emergency services from an out-of-network provider at an in-network facility without prior notice and consent, you are only responsible for in-network cost-sharing amounts, preventing surprise bills from these providers.

- Air Ambulance Services: Protections under the No Surprises Act also apply to air ambulance services, so that you are not billed more than in-network rates for these services.

- Notice and Consent Requirements: For non-emergency services, providers must give you a "good faith" estimate of charges before delivering services. If the charges exceed $400, you must give written consent before proceeding with the treatment.

- Independent Dispute Resolution (IDR): If there’s a payment dispute between your insurer and an out-of-network provider, the No Surprises Act provides an Independent Dispute Resolution (IDR) process, so you’re not caught in the middle.

These protections are designed to prevent unexpected medical bills from leading to financial hardship and potential collections. By understanding your rights under the No Surprises Act, you can better handle the complexities of medical billing and not be charged unfairly for services.

What are the Financial Assistance Options Available for Medical Bills?

The Affordable Care Act (ACA) has made insurance more accessible, particularly for those with lower incomes. Through programs like Medicare, Medicaid, the Children’s Health Insurance Program (CHIP), tax credits, and cost-sharing tools, a network of assistance is now available.

- Hospitals offer financial assistance programs that provide free or discounted care based on income and family size.

- Eligibility Criteria: Based on income and family size; documentation like pay stubs may be required.

- Required by the Affordable Care Act: Nonprofit hospitals must have a written Financial Assistance Policy (FAP) and an Emergency Medical Care policy.

- Accessing the FAP: You can request a copy, and hospitals must provide it free of charge.

- Protection During the Process: If your bill is in collections, you can still apply, and hospitals cannot sell your debt to collectors while your application is pending.

Hospitals cannot deny emergency care due to your ability to pay, ensuring you get the necessary treatment regardless of financial circumstances.

- Government Assistance Programs: Programs like Medicaid, Medicare, and the Children's Health Insurance Program (CHIP coverage until age 19) can provide coverage or financial assistance for medical expenses.

- Nonprofit Organizations: Organizations such as the HealthWell Foundation and the Patient Access Network Foundation offer grants to help cover out-of-pocket medical expenses, including copayments and deductibles.

- Negotiating with Providers: Contact your healthcare provider or the debt collector to discuss payment plans or negotiate a reduction in the amount owed. Many providers are willing to work with patients to establish manageable payment arrangements.

- Medical Billing Advocates: These professionals can assist in reviewing your medical bills for errors, negotiating with providers, and identifying potential sources of financial assistance. While they may charge a fee, their services can result in significant savings.

Also Read: Impact of New Medical Debt Rules on Collections

Despite these assistance options, some medical bills inevitably slip through the cracks, whether due to paperwork delays, missed deadlines, or simply being overwhelmed by the process. When bills remain unpaid long enough, they enter a different phase entirely.

Debt Collection Challenges in Medical Bills

Dealing with medical debt can be overwhelming, especially when bills are sent to collections. Understanding the timelines and the challenges involved can help you cope with the situation more effectively.

Timeline for Medical Bills to Go to Collections

- 30 to 90 Days: Most healthcare providers allow a grace period of 30 to 90 days for payment. During this time, they will send you reminders or statements, but do not involve collections agencies.

- 90 to 180 Days: If the bill remains unpaid after this period, providers may escalate the issue by sending the debt to a collections agency.

- After 180 Days: At this stage, the collections agency will actively pursue payment, which can impact your credit report and credit score.

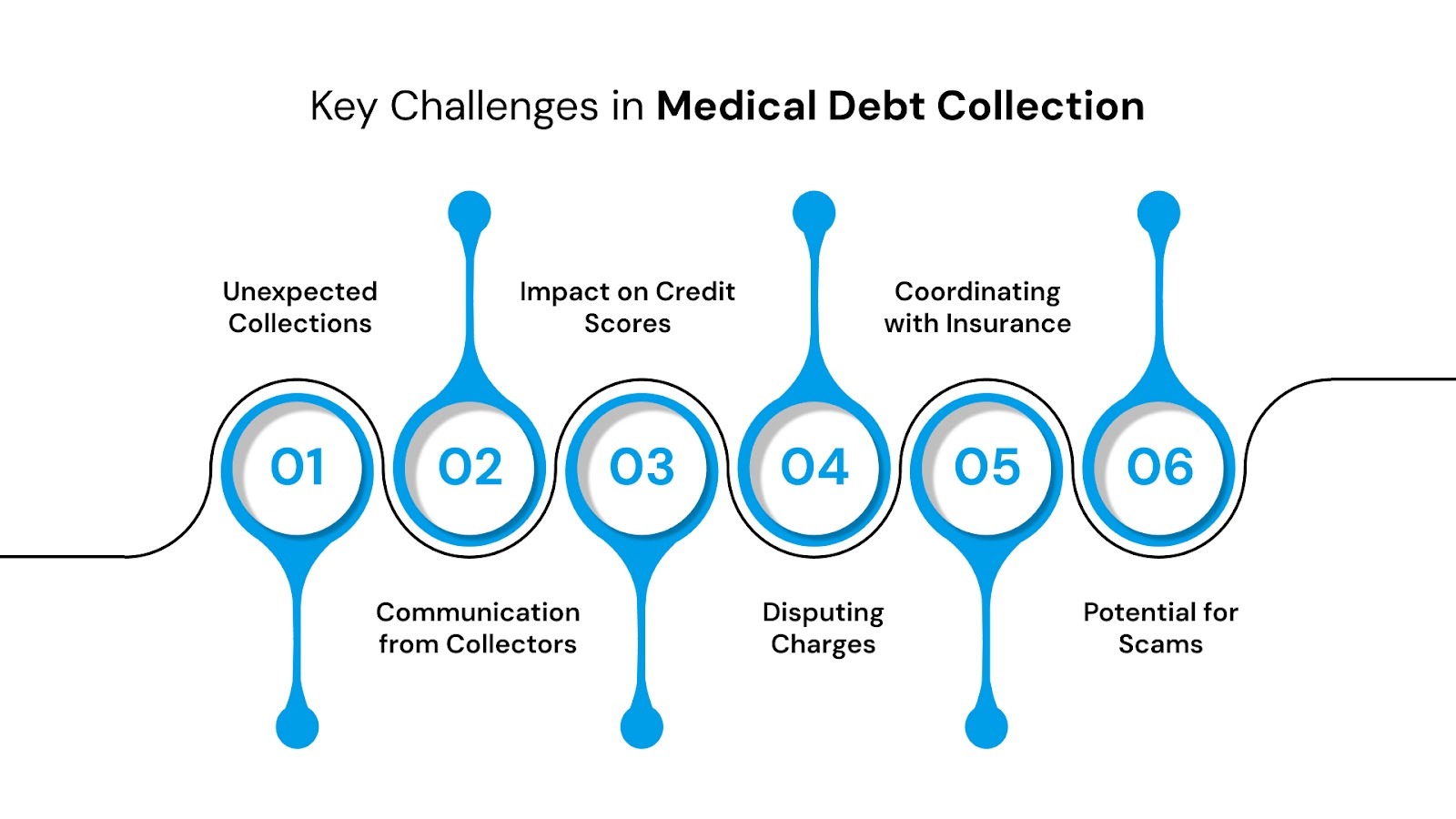

Key Challenges in Medical Debt Collection

- Unexpected Collections: Medical bills can go to collections without much notice, especially if errors on the bill delay payment or insurance processing.

- Communication from Collectors: Collection agencies may contact you frequently, which can be stressful and intimidating. They are required to follow the Fair Debt Collection Practices Act, but the volume of communication can still be overwhelming.

- Impact on Credit Scores: Unpaid medical bills (those with more than $500) sent to collections can negatively affect your credit score, influencing your ability to get loans, credit cards, or favorable interest rates.

- Disputing Charges: Errors in medical billing are common, and disputing a bill while it’s in collections can be challenging, requiring documentation and persistence.

- Coordinating with Insurance: Some bills may go to collections due to insurance delays or miscommunications. Resolving these disputes involves multiple parties and can take significant time.

- Potential for Scams: Debt collectors posing as legitimate agencies can target patients with medical debt. Verifying the legitimacy of collectors is essential to avoid fraud.

Understanding these challenges allows you to approach medical debt collections with more clarity and protect both your finances and your rights. You have the right to verify any debt. By law, you can request validation from the debt collector, which requires them to provide all bills and statements related to your account.

Understanding Consumer Rights and Legal Protections in Medical Billing

Medical bills can be stressful, especially when they are sent to collections, but U.S. law provides multiple protections to ensure debt collection is fair and transparent. Debt collection agencies must wait at least 12 months before reporting an unpaid medical bill to the major credit bureaus. Once reported, unpaid medical debt can remain on your credit report for up to 7 years.

Knowing your rights and the legal safeguards in place can help you prevent unfair practices, protect your credit, and address medical debt responsibly.

- Fair Debt Collection Practices Act (FDCPA): Prohibits collectors from using abusive, deceptive, or unfair practices. They must provide information about the debt upon request, and violations can be legally challenged within one year.

- No Surprises Act: Protects patients from unexpected out-of-network bills in situations such as emergency care or non-emergency care provided by out-of-network providers at in-network facilities.

- Debt Validation Rights: You have the right to request proof of the debt from a collector before they continue collection efforts.

- Nursing Home Reform Act: Limits certain collection activities for medical debt. Nonprofit hospitals must evaluate patients’ eligibility for financial assistance before attempting to collect, or they risk losing their tax-exempt status. Nursing care facilities are also prohibited from collecting debt from third parties.

- Statute of Limitations: Debt collectors cannot pursue very old debts. Most states set the limit between 3 and 6 years. Consulting a consumer protection attorney can help clarify the specific time frame in your state.

- State-Specific Protections: Some states provide additional safeguards. For example, California requires hospitals to provide an itemized bill before sending debt to collections and mandates that collectors inform patients of financial assistance programs.

These protections collectively ensure that medical debt collection is conducted fairly. If you believe your rights have been violated, you can file a complaint with the Consumer Financial Protection Bureau (CFPB), the Federal Trade Commission (FTC), or your state attorney general’s office. However, despite all these, there are vulnerabilities to legitimate debt collection that make you a target for fraud.

How to Protect Yourself from Medical Debt Scams and Report Complaints

Medical debt collectors can only contact you about valid debts you actually owe. You have the right to request verification to confirm that the debt is yours and accurate.

If the bill is legitimate, collectors may attempt to recover the money, including pursuing legal action that could result in wage garnishment or liens. However, they must follow federal and state laws, which prevent abusive calls, excessive contact, or violations when reporting the debt to credit bureaus. You can also instruct them to stop contacting you.

Debt collectors cannot report a medical bill to credit bureaus without first attempting to collect from you. If you notice incorrect reporting, you have the right to dispute it to protect your credit.

Be cautious of anyone offering to remove medical debt from your credit report or guarantee protection from out-of-network costs for an upfront fee. Reputable credit counselors will clearly disclose their services, fees, and avoid high-pressure tactics.

If you believe your rights under the No Surprises Act or debt collection laws are being violated, you can submit a complaint online.

Dealing with medical debt requires both knowledge and support. While understanding your rights is essential, having experienced professionals on your side can make the difference between financial stress and a clear path forward.

Your Trusted Partner in Navigating Debt Challenges

Forest Hill Management is a leading receivables management organization, specializing in the management of past due accounts. With over two decades of experience, we specialize in providing compassionate solutions to help individuals and businesses manage and resolve outstanding financial obligations.

Key Services:

- Portfolio Management: We assist in managing and resolving overdue medical accounts, ensuring a structured approach to debt repayment.

- Flexible Payment Plans: Our team collaborates with you to create customized payment solutions that fit your budget and financial situation.

- Expert Guidance: Receive support from knowledgeable advisors who provide clear information about your rights and options, helping you make informed decisions.

- Compliance Assurance: We adhere to all relevant regulations, ensuring that your rights are protected throughout the debt resolution process.

- Educational Resources: Access materials that help you understand the implications of medical debt and how to avoid future financial challenges.

Conclusion

Managing medical bills, especially when they’re sent to collections, can feel overwhelming. However, understanding how to check for accuracy, knowing the protections available under laws like the No Surprises Act, and recognizing your legal rights can empower you to take control of the situation.

From utilizing financial assistance options to addressing debt collection challenges and avoiding scams, this knowledge helps ensure that you’re not unfairly burdened by medical debt. Additionally, understanding your rights and knowing how to file complaints is essential for protecting your financial health.

At Forest Hill Management, we specialize in helping individuals navigate medical debt and financial challenges. Our expert team offers tailored solutions to help you manage medical bills, understand your rights, and resolve outstanding debts. Contact our advisors today to learn how we can support you in overcoming financial obstacles and securing a healthier financial future.

FAQs

1. What does collection mean in billing?

Collection in billing refers to the process where a debt is transferred to a collections agency after being unpaid for a certain period, typically 90 to 180 days.

2. What are the two different types of collections in medical billing?

The two types of collection in medical billing are internal collections (handled by the healthcare provider) and external collections (handled by third-party debt collectors).

3. Can I negotiate a collection?

Yes, you can negotiate with the debt collector to reduce the total amount owed, set up a payment plan, or settle the debt for less than the full amount.

4. How to get a collection removed?

You can request a debt validation, dispute inaccuracies, or negotiate a pay-for-delete agreement with the collector to remove the collection from your credit report.

5. What is the maximum in medical billing?

The "maximum" in medical billing typically refers to the highest allowable charge or payment that an insurer or payer will cover for a specific medical service, which is determined by the provider’s contract with the insurer. For patients, the maximum out-of-pocket cost is often capped by their insurance policy, including deductibles, copayments, and coinsurance.