How to Get Out of Debt: Practical Steps that Work

Transform Your Financial Future

Contact UsDebt can feel like it is always one step ahead of you. A missed payment turns into a late fee, a late fee turns into more pressure, and soon you may feel like you are working just to keep up with the next bill. That experience is common, and it can even overwhelm capable people. Consumer guidance from the CFPB and FTC makes clear that many people need a simple plan, not shame, when debt starts to pile up.

The important thing is to focus on the cycle, not just one balance. When you only react to whatever bill is loudest that month, it becomes harder to lower interest, avoid fees, and build any real progress. A steadier approach gives you more control, more clarity, and less stress. That is especially true when debt is connected to everyday expenses, emergencies, high credit card use, or payment plans that stretch your budget thin.

In this blog, we are going to look at what the debt cycle is, how to assess your full situation, how to stop the cycle from getting worse, how to choose a repayment strategy, and when to look for extra help. You will also see how to build habits that help you stay out of the same pattern in the future.

Key Takeaways

- Focus on stopping the debt cycle, not just managing monthly payments.

- Clarity about all debts is the foundation of any effective plan.

- Reducing reliance on credit is essential to making real progress.

- Choosing the right repayment approach improves consistency and results.

- Safe, compliant support can help you move forward with confidence.

What is the Debt Cycle?

The debt cycle is what happens when debt starts feeding itself. You may use credit to cover a shortfall, then pay only part of the balance, then carry the rest forward with interest, fees, and more stress. Over time, the balance can become harder to manage even if you keep making payments. Credit card debt often becomes more expensive when you do not pay the full balance, because interest continues to build.

This cycle often starts with a real-life problem, not careless spending. An emergency expense, a temporary income drop, a high-interest card, or a buy now, pay later plan can create pressure that spreads from one bill to the next. The FTC notes that buy now, pay later plans can carry late fees or other charges, and missed payments may hurt your credit score.

The reason this matters is simple. Paying bills one at a time is not always the same as breaking the cycle. If the underlying pattern stays the same, you may keep sliding back into debt even while you are trying to catch up. The goal is to slow the damage, create a plan, and make each payment work harder for you.

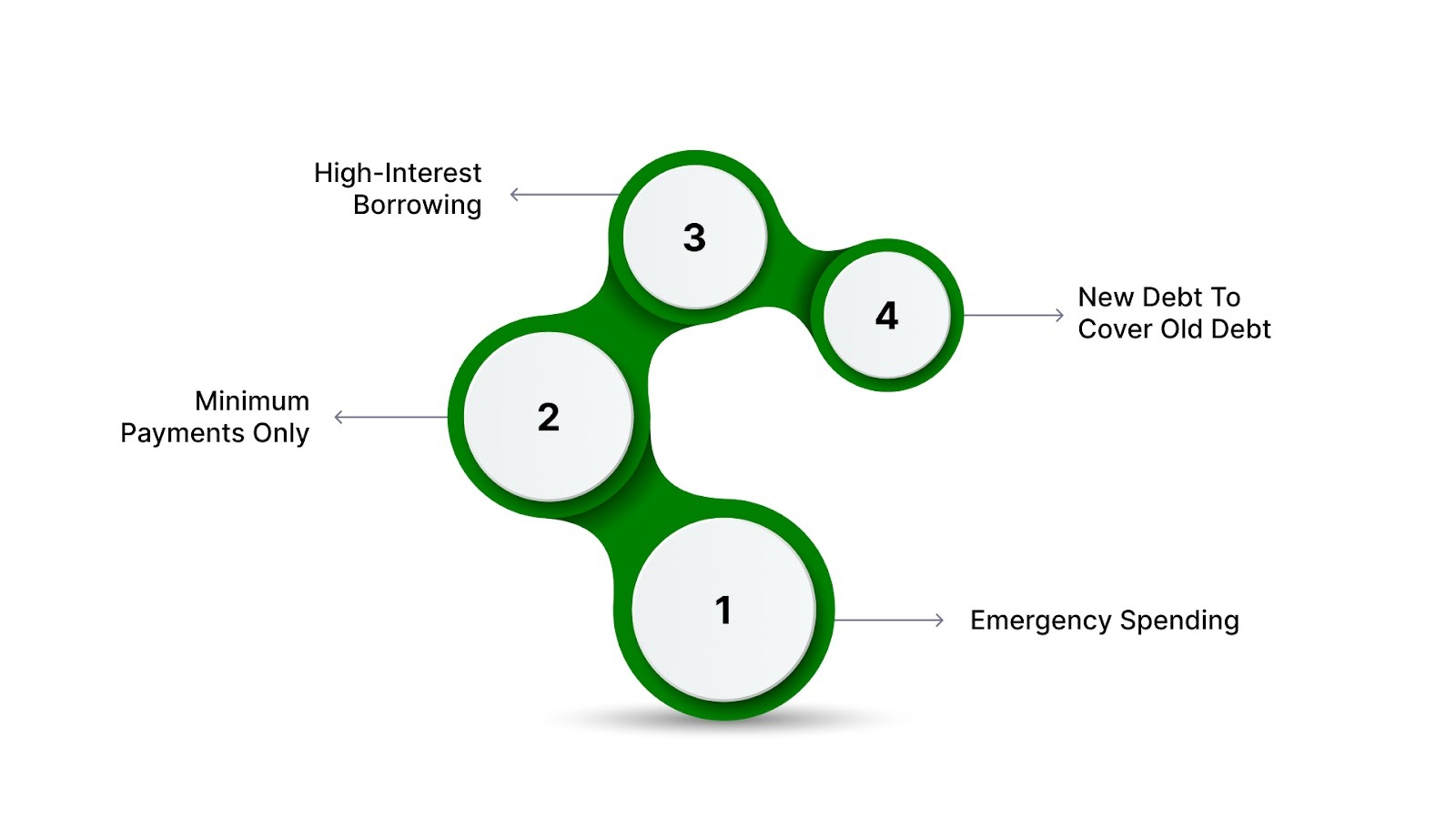

Here are the most common ways the cycle starts, along with what they usually do to your finances:

- Emergency spending: An unexpected expense forces you to rely on credit or to delay payment.

- Minimum payments only: You stay current, but interest keeps the balance alive.

- High-interest borrowing: The cost of carrying the balance grows faster than your payments.

- New debt to cover old debt: One bill gets paid only by creating another bill.

How to Get Out of a Cycle of Debt?

Getting out of a cycle of debt starts with understanding what’s driving it. Repeated balances, missed payments, or relying on credit for essentials can keep the cycle going. This section outlines practical steps to break that pattern and regain control.

Let's look at the steps in detail that you can follow.

Step 1: Start With a Full Debt Assessment

Before you decide how to pay down debt, you need to see the whole picture. The CFPB recommends gathering copies of your bills and interest information and using those details to build a repayment plan that matches your situation. That full snapshot helps you avoid guesswork and choose a strategy based on facts, not fear.

A debt assessment is not about judging yourself. It is about creating clarity. When you know the balance, interest rate, minimum payment, and due date for each account, you can see which debts are costing the most and which ones are closest to being resolved. That makes it much easier to prioritize.

Use this simple template to organize everything in one place:

Once you fill it out, add two more notes:

- Total debt snapshot: This shows your full debt load in one number.

- Principal vs. interest: This helps you see how much of each payment reduces the balance versus the cost of borrowing.

Step 2: Stop Adding New Debt

You cannot break the cycle if new debt keeps entering the picture. The FTC explains that credit becomes more expensive when you carry a balance and only make minimum payments, and BNPL plans can also incur fees and create missed-payment risk. That is why the first rule of debt recovery is to pause the habit of borrowing while you are trying to recover.

That does not mean you must be perfect overnight. It means you need to put friction between you and the next new balance. Even small behavior changes can help you stop losing ground while you work on the debt you already have.

A few practical ways to do that include:

- Freeze unused cards: Put away cards you do not need so they are harder to use impulsively.

- Switch to cash or debit: This keeps spending tied to money you already have.

- Avoid buy now, pay later offers: even low-interest plans can carry fees and late penalties.

- Delay nonessential purchases: Give yourself time before adding anything to a balance.

Step 3: Free Up Cash Faster

Increasing your income can give you a significant advantage in paying off your debt faster. Here are some simple ways to free up cash more quickly:

- Look for short-term side income: freelance work or part-time opportunities to earn extra cash on the side.

- Sell belongings you no longer need or use: This can generate quick cash to help pay down your debt.

- Redirect tax refunds or windfalls: Use any tax refunds or unexpected windfalls like bonuses or gifts to pay off high-priority debts.

- Use extra income specifically for priority debt: Direct any extra income you earn toward your highest-interest debts to reduce them faster.

Step 4: Review Your Spending

Before you can effectively stop adding new debt, it’s important to review your spending habits. Taking a close look at your past expenses can help you identify patterns and make necessary adjustments.

Steps to review spending:

- Review the last 60–90 days of spending: Look at your recent transactions to understand your spending habits.

- Identify repeat categories driving credit use: Recognize recurring expenses, such as dining out or subscriptions, that may be leading you to use credit.

- Separate essentials from pressure-spending: Make sure to distinguish between necessary expenses (e.g., groceries, utilities) and impulse buys or convenience-driven spending.

- Look for subscriptions, delivery, impulse buys, or recurring BNPL use: These can add up quickly and contribute to debt. Cancel unnecessary subscriptions or services, and reconsider frequent delivery or BNPL services.

Step 5: Updated Budgeting Order

For someone actively breaking the debt cycle, a proper budgeting order is crucial to help prioritize essential needs and avoid exacerbating the debt situation.

Updated Budgeting Order:

- Cover Essentials: Rent, food, utilities, and transportation should be your top priorities. These are necessary for your daily life.

- Protect Minimum Debt Payments: Ensure that you make at least the minimum payments on your debts to avoid late fees or penalties.

- Direct Extra Money Toward Priority Debt: Any additional funds should be applied to your highest-priority debts, such as high-interest credit card balances or overdue balances.

- Build a Small Emergency Buffer When Possible: While focusing on debt repayment, set aside a small emergency fund to avoid taking on more debt in case of unexpected expenses.

Step 6: Choose the Right Repayment Strategy

There is no single repayment method that works for everyone. The CFPB identifies two basic strategies that are widely used: the highest interest rate method and the snowball method. One is designed to save more money over time, while the other is designed to help you feel progress sooner.

The best choice depends on what keeps you consistent. If you are motivated by visible wins, the snowball method may help you stay engaged. If you are motivated by efficiency and lower interest costs, the avalanche-style approach may be better. For many people, a hybrid approach works best because real life is rarely tidy.

Here is a simple way to think about each method:

- The Snowball Method: You clear the smallest debt first so you can build confidence from early wins. The CFPB notes that this method can help you see progress quickly.

- The Avalanche Method: You target the highest-interest balance first, so you reduce what debt costs you over time. The CFPB notes this can save money in the long run.

- A Hybrid Plan: You may use avalanche for expensive debts and snowball for small balances that are causing the most stress.

Step 7: Negotiate and Seek Professional Help

You do not always have to face every bill exactly as it stands. The FTC says you can contact your credit card company directly and ask for a lower interest rate or an affordable payment plan. That conversation does not have to happen through a paid middleman, and in many cases, you can handle it yourself.

If you need external support, look for a legitimate credit counseling organization. The FTC says reputable counselors can help you manage money and debt, create a budget, and review your whole situation before suggesting a plan. It also warns that nonprofit status does not automatically mean a company is free, affordable, or legitimate.

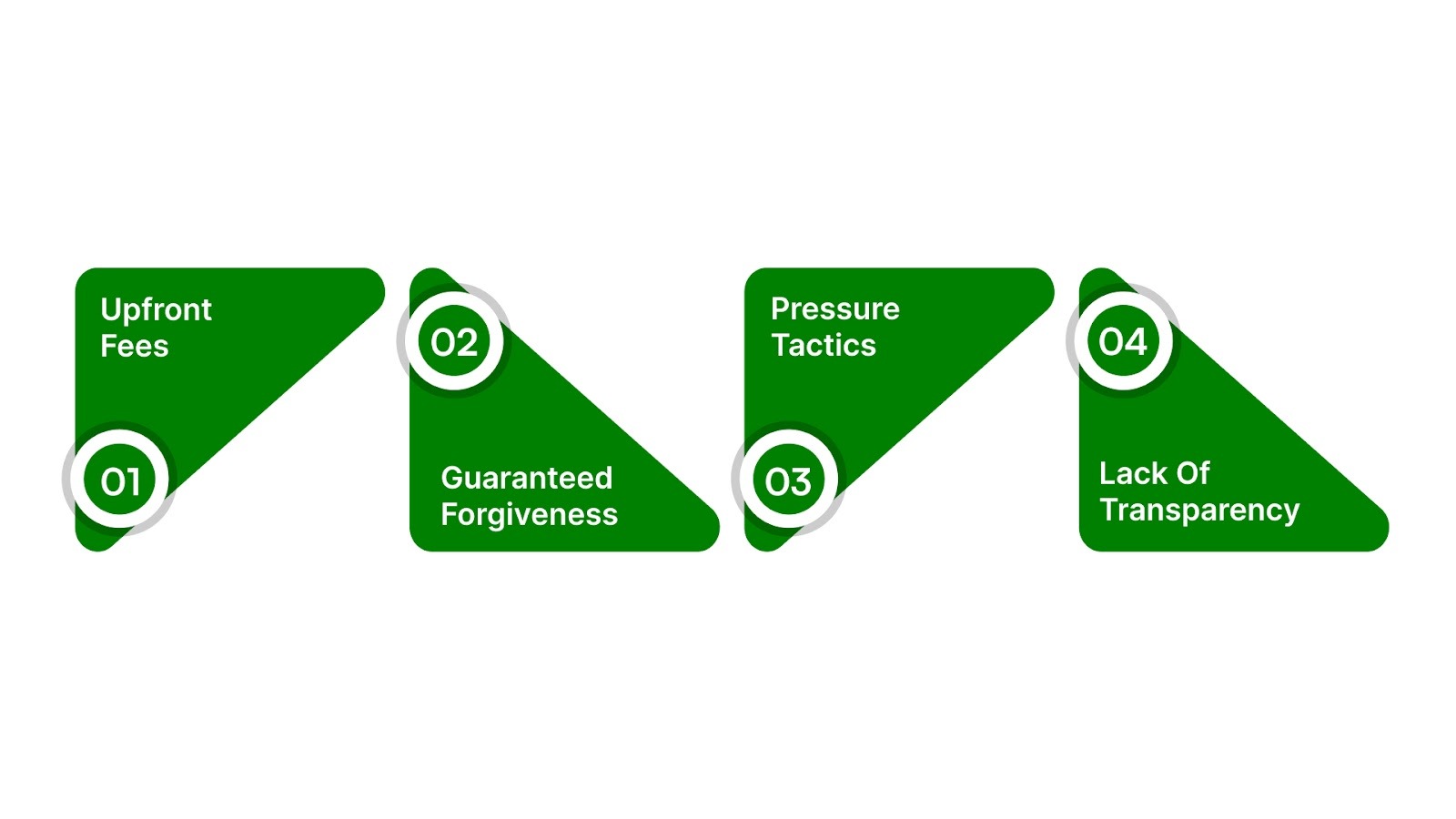

Be careful about red flags. The FTC says a legitimate debt relief company will not charge you upfront, and no one can guarantee that creditors will forgive your debts. The agency also warns against companies that promise quick fixes, hide fees, or make unrealistic claims.

A few warning signs to watch for:

- Upfront fees: Paying before any real help is provided is a major warning sign.

- Guaranteed forgiveness: No one can promise that creditors will approve debt forgiveness.

- Pressure tactics: Fear-based urgency is often used by scam operations.

- Lack of transparency: Legitimate help should be clear about fees, steps, and results.

Step 8: Budgeting and Financial Discipline

Budgeting is not punishment. It is a way of seeing the truth about your money so you can make better choices with less stress. The CFPB says budgeting is a key step toward getting a handle on debt and working toward savings goals, because you need a realistic picture of income and expenses before you can know what is left over.

A debt-focused budget should tell your money where to go before it disappears into daily spending. That means covering essentials first, then making debt payments part of the plan instead of hoping there is enough left at the end of the month.

Use this order to build a practical budget:

- Pay yourself first: Set aside a small amount for savings or an emergency cushion when possible.

- Cover essentials: Rent, food, utilities, and transportation should be clear priorities.

- Protect debt payments: Include minimums in the budget so you do not fall behind.

- Direct extra money wisely: Put any extra funds toward the debt that matters most to your plan.

- Review monthly: Check what worked, what did not, and where adjustments are needed.

Also Read: Why One-Size-Fits-All Debt Solutions Don't Work for Real Relief.

Step 9: Build Healthy Money Habits That Last

Getting out of debt matters, but staying out of it matters just as much. The FDIC recommends automatic transfers as a simple way to build emergency savings and says even small amounts can help. It also notes that many experts generally recommend six months of living expenses in a federally insured savings product, although building a smaller cushion is still useful.

That kind of cushion can keep a car repair, medical bill, or temporary setback from becoming another debt cycle. Once you are no longer in crisis mode, your money can start working toward future goals instead of only reacting to emergencies.

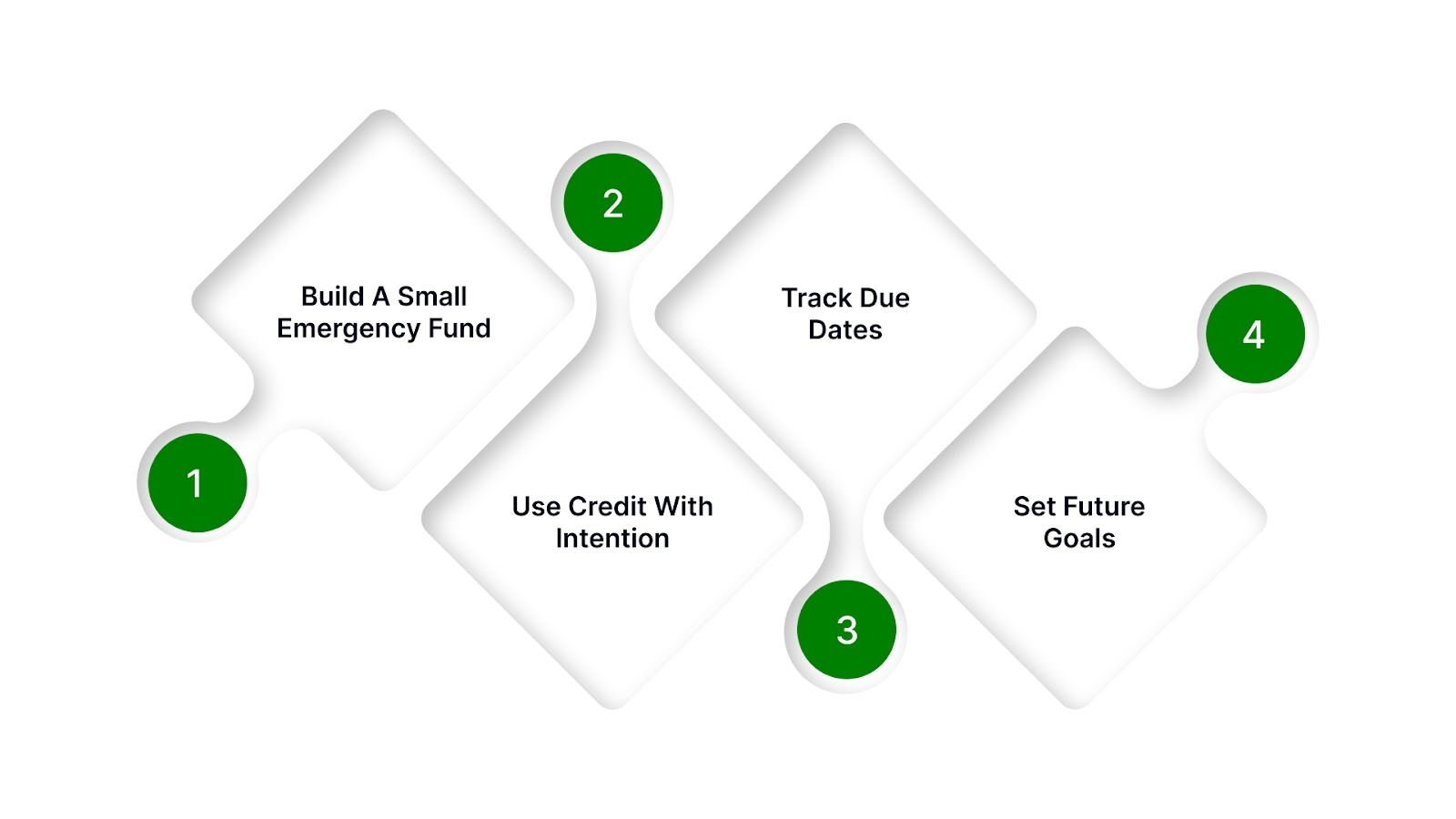

Healthy habits that can make a big difference include:

- Build a small emergency fund: Even a modest cushion can reduce the need to borrow again.

- Use credit with intention: Paying in full when possible helps keep credit less expensive.

- Track due dates: Staying current protects your credit history and lowers stress.

- Set future goals: Emergency savings, retirement, and major purchases all deserve a plan.

When Debt Consolidation or a Debt Management Plan Might Help?

If you're struggling with multiple debts, consolidating them or enrolling in a Debt Management Plan (DMP) could simplify repayment.

- Debt Consolidation: This method may help when it lowers your interest rate and consolidates multiple balances into a single payment. By consolidating debts, you can simplify your finances, reduce interest costs, and streamline payments.

- Debt Management Plans (DMPs): A DMP, facilitated by a reputable credit counseling agency, helps organize unsecured debts. With a DMP, your counselor may be able to negotiate lower interest rates or waive certain fees with your creditors, making repayment more manageable.

- Limitations: Both debt consolidation and DMPs will not resolve your debt if spending habits remain unchanged. These options help organize payments, but long-term success requires addressing the root causes of your debt, such as overspending or relying on credit.

When to Consider More Serious Options?

Sometimes debt becomes too difficult to manage with budgeting and repayment alone. In those situations, it is reasonable to learn about bankruptcy and other serious options. The FTC explains that Chapter 7 bankruptcy may involve liquidating nonexempt assets, while Chapter 13 generally uses a court-approved repayment plan over three to five years.

Bankruptcy is not a casual step, and it can affect your credit for years. FTC guidance notes that bankruptcy information can appear on a credit report for up to 10 years, depending on the type of bankruptcy. Even so, for some people, it can create a lawful fresh start when other options are no longer realistic.

Before taking that path, it is wise to speak with a qualified financial or legal professional. That helps you understand your options, obligations, and potential long-term effects before you make a decision.

Conclusion

Breaking the debt cycle is not about perfection. It is about changing the pattern that keeps pulling you backward. When you understand your full debt picture, stop adding new balances, choose a repayment strategy that fits your situation, and build a budget that reflects reality, you give yourself a much better chance of steady progress.

You may still have hard months along the way, but that does not mean you are failing. It means you are working through a problem that many households face, and you are doing it one decision at a time. Paying attention to the cycle, not just the balance, is what creates a path forward.

If your account has been placed with The Forest Hill Management, you can review your account details, understand your current status, and explore available repayment options through a structured and compliant process.

Contact us for a clear next step that respects your situation and helps you move forward with confidence.

FAQs

1. What is the first step to breaking the debt cycle?

Start with a full debt assessment. List every balance, rate, minimum payment, and due date to see the full picture. This helps you understand where your money is going and which debts are costing you the most. It also gives you a clear starting point for prioritising repayments and avoiding missed payments.

2. Is the snowball method better than the avalanche method?

Neither is always better. Snowball helps with motivation, while Avalanche can save more money by targeting high-interest debt first. The right choice depends on your situation and mindset. If staying consistent is difficult, snowball can help build momentum. If reducing total interest matters more, avalanche is often the more efficient approach.

3. Should I stop using credit cards while paying off debt?

Yes, if possible. Stopping new debt helps break the cycle and keeps your repayment plan from being undermined by fresh balances. Continuing to use credit cards can slow progress and increase interest costs. If you still need them for essentials, consider limiting usage or setting strict spending rules to stay in control.

4. How do I know if a debt help company is legitimate?

Be cautious with upfront fees and guaranteed forgiveness. Reputable help is transparent, and legitimate counselors review your full financial situation first. Look for clear explanations of services, written agreements, and no pressure to commit immediately. It’s also helpful to check reviews and verify if they are affiliated with recognised credit counselling organisations.

5. When should I think about bankruptcy?

Consider it only after reviewing your full options with a qualified professional. Bankruptcy can provide relief, but it also has long-term credit effects. It may be relevant if your debt is unmanageable and other solutions are not working. Always understand the consequences, timelines, and alternatives before making a decision.