What to Do If Sued for Debt in California

Need Help Reviewing Your Account?

Contact UsYou don’t expect a lawsuit to arrive folded inside regular mail. When the word “Summons” appears, your brain jumps straight to loss, courtrooms, and whether your life just tipped sideways.

Only about 8.8% of people who are sued for debt file a response, and two out of three cases end in default because nothing was filed.

This moment marks the start of debt litigation, where silence carries more risk than the debt itself. The real danger is not the lawsuit, but hesitation driven by confusion, fear, or not knowing what the clock demands.

This article explores what a debt lawsuit in California actually sets in motion, what decisions matter first, and how to respond without making the situation worse.

Key Takeaways

- Ignoring a debt lawsuit can lead to default judgments and legal collection actions, so timely, informed responses are crucial.

- Carefully reviewing the summons and complaint helps you verify the debt, spot errors, and understand deadlines that affect your rights.

- Filing a proper Answer and serving the plaintiff opens options for negotiation, payment plans, or a court defense, giving you an advantage.

- California law provides protections for those facing financial hardship, including exempt income, fee waivers, and potential bankruptcy relief.

- Proactive guidance, including educational support from companies like Forest Hill Management, can help you understand available options and next steps without replacing legal advice.

Understanding Debt Lawsuits in California

A summons is a court notice requiring your participation in a legal proceeding. The complaint attached to it describes why someone believes you owe them money and what they want the court to do about it.

Lawsuits are usually filed by three types of entities: original creditors, debt buyers who purchase accounts at a discount, or collection agencies acting on behalf of either. They typically follow months of missed payments, calls, letters, and settlement attempts.

When those fail, litigation forces resolution, and the shift from collection notices to legal action changes how you must respond.

What Happens If You Ignore the Lawsuit?

If you don’t respond to a debt lawsuit, the court may enter a default judgment in favor of the plaintiff. This means the court assumes the debt is valid because you didn’t contest it. After a default judgment, you generally can’t dispute the debt unless you later move to set it aside for valid reasons, like improper service or excusable neglect.

A default judgment becomes part of the public record and may impact your credit, depending on how and whether the judgment is reported by credit bureaus.After that, the creditor can use legal tools to collect the debt, including:

- Wage garnishment: A portion of disposable earnings may be withheld, subject to California’s limits based on income and minimum-wage thresholds.

- Bank levies: Funds in your bank account can be frozen and transferred to satisfy the judgment.

- Property liens: Real estate you own can be encumbered, making it difficult to sell or refinance until the debt is paid.

- Judgment renewal: In California, judgments can remain enforceable for up to 10 years and may be renewed before expiration.

These enforcement actions are generally available once the judgment is in place, though legal procedures and notices must still be followed. Ignoring a lawsuit essentially lets the creditor move from requesting payment to legally collecting it.

Also Read: How to Handle Debt Collection Lawsuits Effectively

Before the creditor can take further action, understanding your options for responding is key to preventing a default judgment and protecting your financial rights.

How to Respond to a Debt Lawsuit in California

Responding to a debt lawsuit isn’t about reacting quickly; it’s about responding correctly. The court process is formal, and small mistakes can limit your options later. The goal is to protect your rights, meet required deadlines, and avoid giving up defenses unintentionally.

Here’s how the response process typically unfolds in California.

Step 1: Review the Summons and Complaint

The summons and complaint contain details that shape every next step you take. First, identify who filed the lawsuit. The plaintiff’s name shows whether the case comes from an original creditor, a debt buyer, or a collection agency. That distinction affects what proof they may need later.

Next, review the amount being claimed. Compare it to your records to see whether interest, fees, or costs appear higher than expected or unfamiliar.

Finally, locate the response deadline listed on the summons. In California, you usually have 30 days from the date you were served to respond. Missing this deadline can lead to a default judgment, even if you have valid defenses.

Step 2: Confirm the Debt and Its Enforceability

Debt lawsuits sometimes rely on incomplete or incorrect information. Start by confirming whether the debt actually belongs to you. Then review whether the amount claimed is accurate.

You should also consider whether the debt may be outside California’s statute of limitations. In many cases, written contracts have a four-year limit, while some oral agreements may have shorter limits.

Whether a debt is time-barred depends on the specific facts, including the type of agreement and recent account activity. If the statute of limitations has expired and is properly raised as a defense, the debt is generally unenforceable through the courts.

Step 3: File a Written Answer With the Court

An Answer is the formal document that tells the court you are responding and disputing the lawsuit. California courts provide standard Answer forms commonly used in debt cases. These forms ask you to admit, deny, or state that you lack enough information to respond to each allegation in the complaint.

You may also include affirmative defenses, which are legal reasons the claim should not succeed even if the debt exists. Common defenses can include statute-of-limitations issues, lack of standing, insufficient documentation, or prior payment.

Your Answer must be filed with the court clerk before the deadline. Filing late may result in rejection and can allow the plaintiff to seek a default judgment without further notice.

Step 4: Serve the Plaintiff as Required

Filing with the court alone is not enough. California law requires that a copy of your Answer be served on the plaintiff or their attorney. Service is usually completed by mail and must be done by someone over 18 who is not you.

That person mails the Answer to the address listed on the complaint and completes a Proof of Service form, which is then filed with the court to confirm delivery.

Also Read: Understanding Debt Collection and Recovery Process

Without proper service, your answer doesn't count as an official notice, and the case can still move forward as if you never responded.

Your Options After Filing an Answer

Filing an answer opens the door to resolution methods that weren't available when you were in default. The plaintiff now has to prove their case instead of simply claiming it. That shift in burden creates leverage you didn't have before.

Here's where that leverage leads:

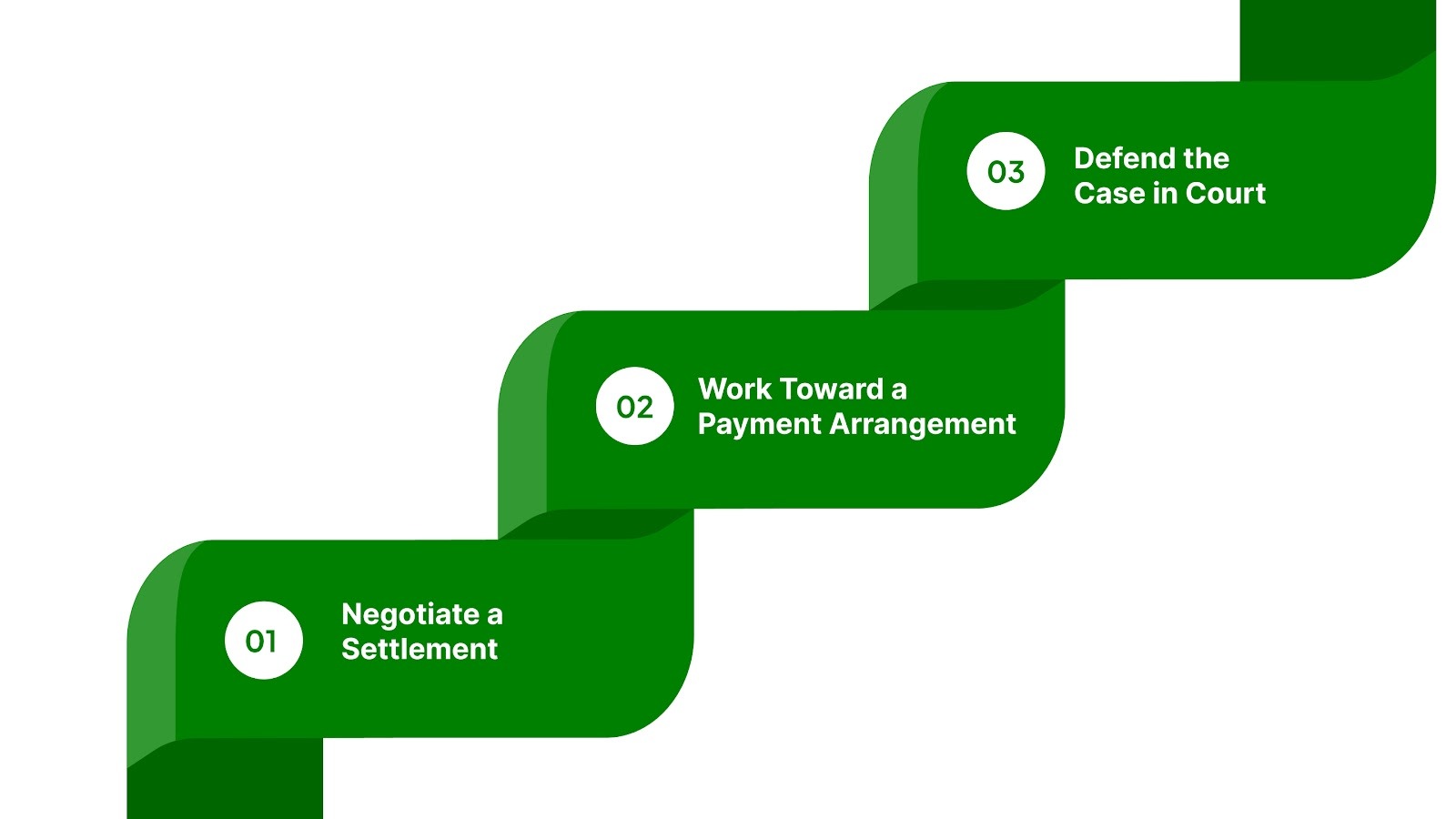

1. Negotiate a Settlement

Most creditors are more open to settlement once you actively defend the case. Settlements may reduce the amount owed, depending on the creditor’s policies and the facts of the case.

You can propose lump-sum or manageable payment terms by contacting the plaintiff’s attorney. But always get the agreement in writing and confirm that the case will be dismissed after payment.

2. Work Toward a Payment Arrangement

In some cases, you can negotiate a payment plan based on what you can realistically afford. These arrangements are not automatic and usually require creditor agreement or court approval. Staying current on approved terms can limit further enforcement actions.

3. Defend the Case in Court

If no agreement is reached, the case moves forward. The plaintiff must prove the debt, their right to collect it, and the amount owed. You may challenge their evidence and rely on defenses raised in your Answer, such as documentation issues or statute-of-limitations concerns.

Even with these options, not every situation allows for immediate payment or settlement. If paying the debt isn’t realistic right now, there are still paths forward worth understanding.

What If You Can't Afford to Pay?

Inability to pay doesn't eliminate the debt, but California law protects certain assets from creditor seizure. The court system offers accommodations for people facing genuine financial hardship. The goal is to prevent total financial collapse while still addressing the obligation.

Here's what protection looks like in practice:

- Exempt income and assets under California law include Social Security benefits, unemployment insurance, workers' compensation, disability payments, and a portion of wages below the garnishment threshold.

- Fee waivers let you participate in court proceedings without paying filing fees if your income falls below specific thresholds or you receive public benefits.

- Bankruptcy typically triggers an automatic stay that stops most collection activity while the case is pending.

Bankruptcy has long-term legal and financial consequences, and eligibility depends on individual circumstances.

Even with legal safeguards, missteps can escalate your situation. Understanding common errors helps you stay in control.

Common Mistakes That Hurt Your Case

Some responses unintentionally weaken your position by creating legal problems you could have avoided. Avoiding these mistakes preserves your defenses and gives you the best opportunity to protect your rights:

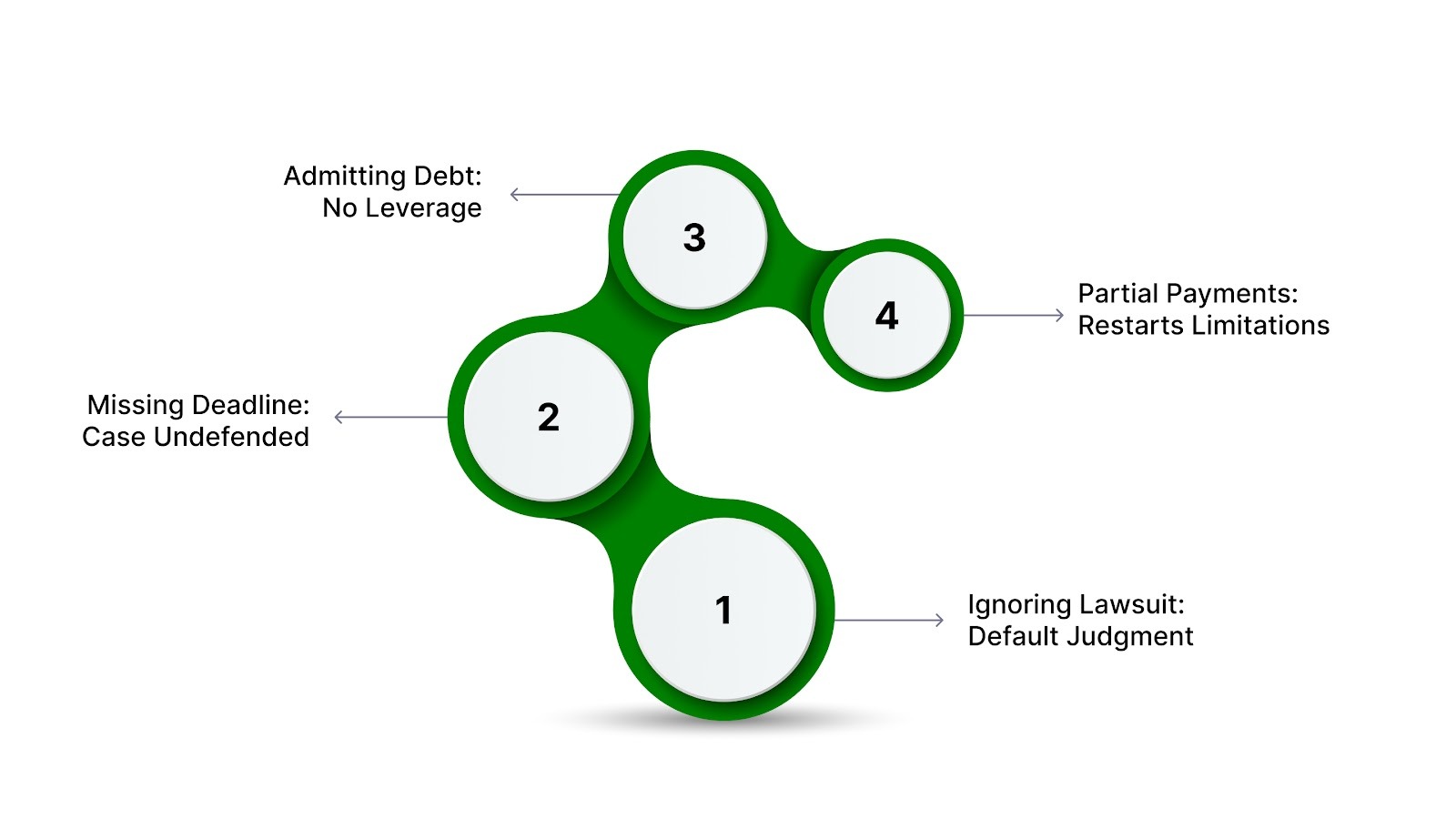

- Ignoring the lawsuit entirely: Letting the deadline pass allows the plaintiff to request a default judgment, deciding the case without your input.

- Missing the response deadline: Filing late usually means the court treats your case as undefended and can enter judgment for the other side.

- Admitting you owe the debt without verification: Acknowledging the debt before confirming its accuracy removes leverage to challenge its validity or raise defenses.

- Making partial payments without clear terms: In some cases, partial payments or written acknowledgments may restart the statute of limitations under California law, depending on the facts.

Each of these errors can limit your ability to contest the lawsuit or negotiate from a stronger position.

Also Read: Debt Relief Plans: How To Choose The Right One For You

Understanding these common pitfalls highlights why proactive, informed action is so important; early steps can prevent unnecessary legal battles and preserve your rights.

How Forest Hill Management Helps Consumers Reduce the Risk of Litigation

Lawsuits are stressful, expensive, and often avoidable when you work with a company focused on proactive resolution instead of aggressive enforcement. Forest Hill Management helps consumers address outstanding accounts early, which in some cases may reduce the likelihood of escalation to legal action.

The difference is in how we approach accounts from the beginning:

- Flexible payment plans: Structured repayment options designed to prevent escalation, not force you into corners that lead to lawsuits.

- Early resolution support: Helping consumers address accounts proactively, where possible, through structured repayment options.

- Transparent communication: You always know where you stand and what comes next, not vague threats that keep you guessing.

- Compliance-focused processes: Every step follows federal and state regulations, so you're protected throughout the process.

- Secure online account access: Make payments and track progress without added stress or confusion.

By taking advantage of these supportive tools, you’re not just avoiding potential legal hassles; you’re gaining clarity and control over your finances.

Conclusion

Facing a debt lawsuit in California can feel overwhelming, but understanding the process and your rights gives you a clear path forward. Taking measured steps, from reviewing the summons to exploring options for resolution, helps you regain confidence and reduces the uncertainty that often comes with legal notices.

While the situation may feel daunting, support is available to help you manage it with clarity and purpose. Forest Hill Management is here as a resource you can rely on, offering guidance and assistance as you take control of your financial journey.

If you’re exploring ways to address an account or understand your options, Forest Hill Management can provide clear, compliant information and support.

FAQs

1. Can a debt collector sue in multiple counties, and how does venue affect the case?

The lawsuit must be filed in a county where you live, signed the contract, or where the debt arose. Challenging an improper venue can delay the case or even lead to dismissal.

2. How do California’s consumer protection laws interact with debt lawsuits?

Violations of the Rosenthal Fair Debt Collection Practices Act (RFDCPA) or other state laws can be raised as defenses or counterclaims, potentially reducing the amount owed or dismissing the case.

3. Can bankruptcy affect a pending debt lawsuit differently in California?

Filing bankruptcy triggers an automatic stay that stops lawsuits. Chapter 7 may discharge the debt entirely, while Chapter 13 can convert it into a structured repayment plan. Timing of filing is critical.

4. How can errors in the service of process invalidate a lawsuit?

If legal documents weren’t served according to California law, for example, left with the wrong person or mailed incorrectly, the court may dismiss the case regardless of the debt’s validity.

5. Can third-party debt buyers lose standing in California courts?

Debt buyers must prove they own the debt and have the right to sue. Missing documentation or chain-of-title gaps can undermine standing, possibly leading to dismissal or a reduced judgment.