Understanding Debt Collection and Recovery Process

Need Help Reviewing Your Account?

Contact UsStaring at overdue bills, feeling the weight of mounting debt, and constantly worrying about your credit score or potential wage garnishment? These struggles can feel suffocating, and it’s easy to think there’s no way out. But you’re not alone, and the path to financial freedom is within reach.

AI adoption in debt collection has increased recovery rates by 25%, proving that with the right tools, getting back on track is possible.

This blog will break down the debt collection and recovery process, focusing on how secure payments, flexible repayment options, and expert financial advice can help you regain control. We’ll walk you through practical steps to manage and reduce debt, bringing peace of mind and a clear path forward.

Key Takeaways

- Debt Collection vs. Debt Recovery: Debt collection involves communication and negotiation, while debt recovery escalates to third-party involvement and legal actions when collection efforts fail.

- Know Your Rights: The Fair Debt Collection Practices Act (FDCPA) ensures you're protected from harassment and allows you to dispute debts and request validation.

- Effective Communication Matters: Personalizing your communication methods and times can significantly improve engagement and increase repayment chances.

- The Role of Technology: AI and data analytics can streamline the debt collection process, helping determine optimal contact times and predict consumer behavior.

- Best Practices: Clear communication, empathy, and flexibility are essential for successful debt recovery. Working with a third-party agency can be beneficial when in-house efforts fall short.

What is Debt Collection?

Debt collection is the process that begins when a company notices a missed payment. If you’ve forgotten to pay for a service or product, the company will typically reach out via email, letter, or phone call to remind you.

For businesses, outstanding payments can disrupt cash flow and damage their reputation. Here's how the process typically unfolds:

- Evaluating Accounts Receivable: The business reviews its outstanding invoices and identifies overdue payments. If payment isn’t made after 30 days, they begin the collection process.

- Dunning Letters: A common strategy to inform debtors that their payment is overdue. This helps prevent accounts from becoming delinquent.

- Third-Party Involvement: Many businesses hire debt collection agencies to manage the recovery process. These agencies specialize in debt recovery and tackle the complexities of the process.

- Communication and Payment Requests: Debt collectors reach out via calls, emails, or letters to discuss repayment plans. Their goal is to encourage payment by offering settlements or payment arrangements.

- Compliance with Regulations: Debt collectors must follow strict guidelines, like the Fair Debt Collection Practices Act (FDCPA), to ensure fairness and ethical practices in their approach.

- Collection Strategies: Methods include reminders, negotiations, and explaining the consequences of non-payment. Agencies may also use skip tracing to locate individuals who are unreachable.

- Fee or Commission-Based: Most debt collection agencies charge a commission or flat fee for their services, typically based on the amount of debt they successfully recover.

- Documentation and Record-Keeping: Collectors maintain detailed records of each interaction, including payment arrangements and communications, ensuring compliance with legal requirements.

Understanding the debt collection process can provide clarity for both businesses and debtors.

Also Read: Is Paying Debt Collection Agencies a Bad Idea?

Now that you know what debt collection is, it’s important to see why collecting debts on time matters.

Why Timely Debt Collection is Crucial

Timely debt collection is crucial for organizations seeking to maintain financial stability and operational efficiency. Recovering debts on time offers several key advantages:

- Strengthens Financial Stability: Ensuring consistent, on-time payments helps businesses maintain a stable cash flow, meet their financial obligations, and make room for investments and growth.

- Supports Operational Needs: Quick collections provide the necessary working capital to fund day-to-day operations, buy inventory, and handle unexpected costs.

- Reduces Financial Risk: Promptly collecting debts minimizes the risk of cash flow problems, borrowing costs, credit risks, and potential rating downgrades, thereby preventing disruptions in operations.

- Improves Profit Margins: Delayed payments often lead to increased costs, requiring additional resources for collections. The longer the debt remains unpaid, the lower the chances of full recovery.

- Protects Customer Relationships: Addressing overdue debts quickly is less likely to damage relationships compared to prolonged or aggressive collection tactics, allowing businesses to maintain favorable terms.

- Enhances Business Reputation: A reputation for ethical, efficient debt collection builds trust among customers, partners, and stakeholders, positioning the business as reliable and professional in financial matters.

Timely collections are essential, but debt recovery is about recovering the money when early efforts are unsuccessful. Let’s explore this further.

What is Debt Recovery?

.webp)

Debt recovery is a process that businesses use when regular debt collection efforts are unsuccessful. Here's what you need to know:

- Third-Party Involvement: When internal attempts to collect the debt are unsuccessful, businesses often turn to specialized agencies or legal experts to recover funds on their behalf.

- Impact on Credit: Engaging in debt recovery can negatively affect a debtor’s credit score. Ignoring collection efforts can exacerbate the situation, potentially leading to court action.

- Legal Actions: If the debt remains unpaid, creditors may file lawsuits or obtain court orders for wage garnishment or seizure of assets to enforce repayment.

- Negotiation and Settlement: Recovery efforts might also involve negotiation. Debtors and creditors can settle on revised repayment terms or reduced amounts.

- Documentation & Resources: Effective debt recovery requires thorough documentation and may involve either internal teams or external experts to handle complex cases.

- Time, Cost, and Effort: The recovery process can be costly and time-consuming, especially when legal action is necessary.

Debt recovery is a more intensive process that involves legal measures and external assistance, designed for use when traditional collection efforts are ineffective.

Types of Debt Companies Can Recover During Collection or Recovery

The type of debt a consumer holds significantly influences the recovery process and how specific bills are managed. Below are some common debt types that qualify for collection and recovery:

- Unpaid Personal Loans

- Outstanding Credit Card Balances

- Auto Loans (Including Post-Repossession Debt)

- Government and Legal Fees, Including Court Fines

- Medical Debt

- Bank Fees and Overdraft Charges

- Unpaid Utility Bills

- Student Loan Defaults

When a consumer has overdue debt, a recovery agency may notify them through phone calls or written communication.

Also Read: Understanding Legal Collections and Their Processes

With debt recovery explained, it’s important to understand how this differs from the earlier stages of collection.

Key Differences Between Debt Collection and Debt Recovery

While both debt collection and debt recovery aim to recover overdue payments, there are key differences that set these processes apart:

While debt recovery can escalate to more severe measures like legal actions, debt collection focuses on open communication and voluntary repayment.

Now that we've outlined the key distinctions, let's explore specific communication strategies that can help you manage the process effectively.

Examples of Debt Recovery Communications

Effective debt recovery begins with clear and respectful communication. Below are some sample letters you can send to consumers with unpaid balances:

- Initial Payment Reminder: This is the first communication you send to notify the consumer about their overdue payment. Include key details, such as the amount owed, the due date, and clear instructions on how to make the payment to avoid penalties.

- Debt Validation Request: This letter confirms the outstanding debt and the consumer's right to dispute it. Provide the total amount due, the recipient of the payment, and the instructions on how they can dispute the debt.

- Payment Plan Proposal: After discussions, send a letter offering the consumer a structured payment plan. This option enables them to settle the debt gradually, allowing them to manage their financial obligations over time.

- Final Notice Before Legal Action: This is the last reminder sent to inform the consumer that failure to pay will result in legal action. Make it clear that this is their final opportunity to resolve the debt before further steps are taken.

Following these communication steps helps to effectively manage debt recovery while ensuring transparency and fairness for all parties involved.

Next, let's explore your rights and what protections you have during the debt collection process.

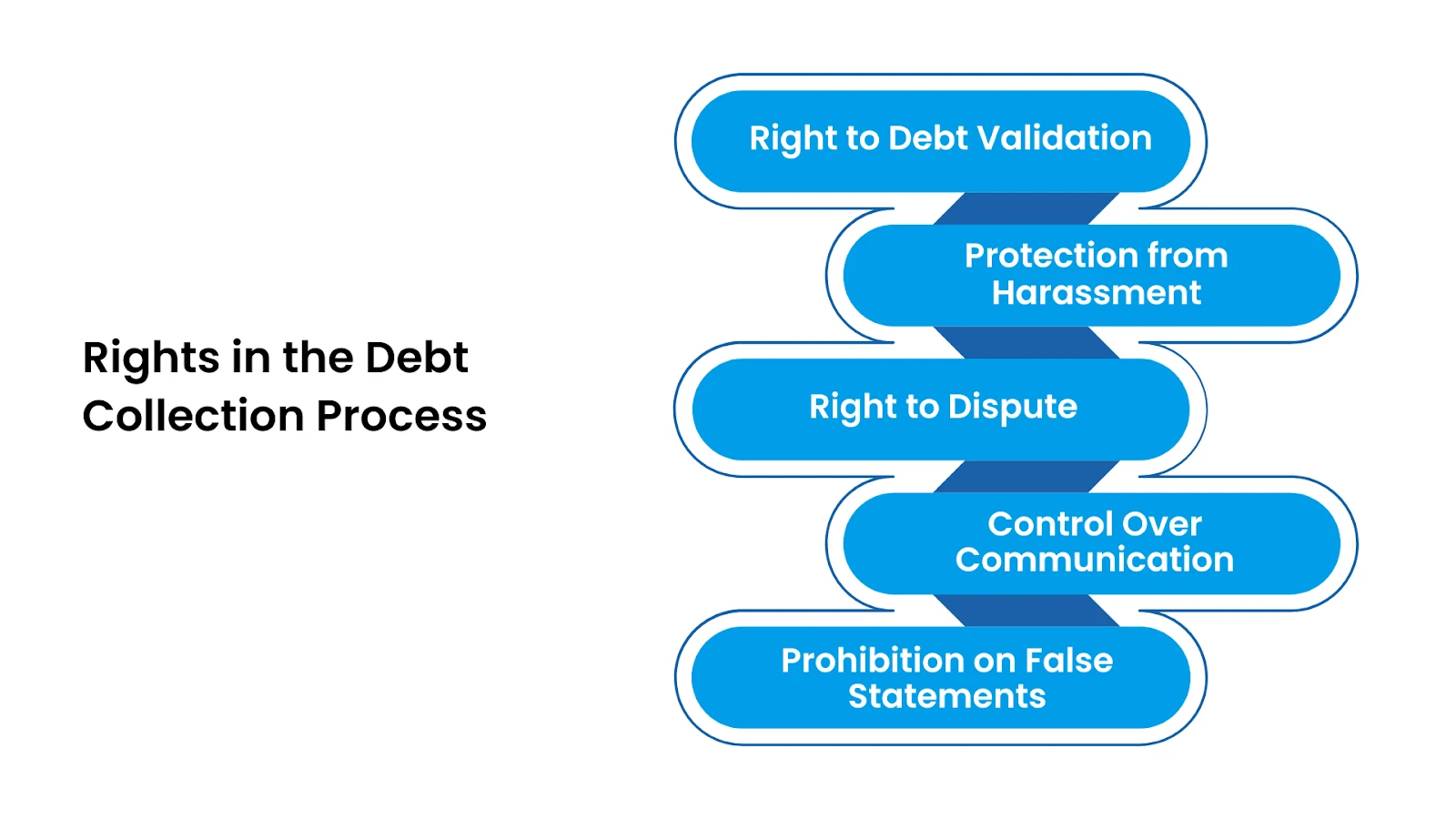

Your Rights in the Debt Collection Process

Dealing with debt collection can be stressful, but it's important to know your rights. The Fair Debt Collection Practices Act (FDCPA) was created to protect you from unfair or aggressive practices. Here’s what you should know:

- Right to Debt Validation: You have the right to request written proof of the debt from the collector. This ensures the debt is legitimate and accurate.

- Protection from Harassment: Debt collectors are prohibited from using threats, abusive language, or making excessive calls.

- Right to Dispute: If you believe a debt is incorrect, you can challenge it. You have the power to dispute the amount or validity of the debt.

- Control Over Communication: You can request that the collector only contact you in writing. This puts you in control of when and how communication happens.

- Prohibition on False Statements: Debt collectors cannot mislead you. They cannot claim you owe more than you do or threaten actions they can't actually take.

These rights help ensure that debt collection remains fair, transparent, and equitable.

Understanding your rights is essential, and it’s the first step in regaining control of your financial journey. If you're ready to move forward, The Forest Hill Management can help you. Contact our financial advisors to create a customized plan that works for you and helps you regain financial freedom.

Understanding your rights is key. Next, we’ll discuss the factors that can affect the success of debt collection and recovery.

Factors Affecting Debt Collection and Debt Recovery

The debt collection and recovery process is shaped by several factors that can influence how agencies proceed. Here are some key factors to consider:

1. Type of Debt

The nature of the debt, whether it’s from credit cards, medical bills, or personal loans, dictates how collection efforts are structured. Different debts may require different tactics.

2. Financial Circumstances of the Debtor

The debtor’s ability to pay plays a crucial role. Financially strained individuals may benefit from flexible repayment plans, while those with stable income may handle standard recovery processes.

3. Legal Regulations

Debt collection practices are governed by laws such as the Fair Debt Collection Practices Act (FDCPA), which sets clear boundaries on how agencies can engage with debtors. These legal constraints guide the recovery process.

4. Debtor’s Cooperation

Some individuals may be open to negotiation, which can lead to a smoother recovery. Others may resist, requiring more persistent efforts to reach an agreement.

5. Time Factor

As time passes, it becomes harder to recover debt. Prolonged non-payment may lead to more aggressive collection measures, impacting the strategy and timing of actions.

6. External Economic Conditions

Broader economic factors, such as job loss or inflation, can affect a debtor’s ability to repay. These external factors can necessitate adjustments in the collection approach to accommodate the debtor’s circumstances.

Considering these factors helps companies tailor their debt collection efforts, offering solutions that strike a balance between recovery goals and empathy for the debtor’s situation.

Also Read: Improving Your Company's Financial Health

Now that we know what influences the process, let’s take a look at some best practices for managing debt collection and recovery effectively.

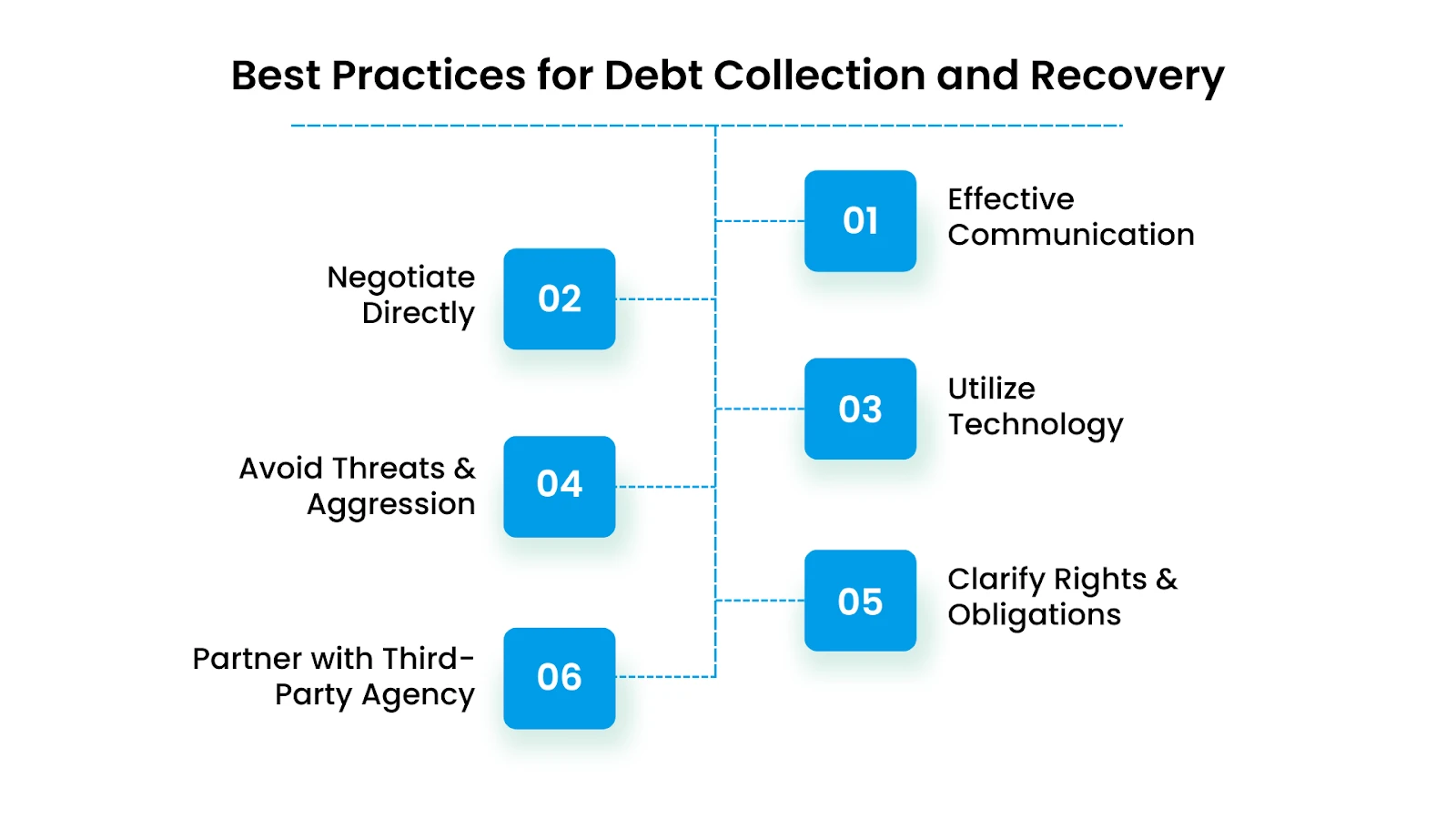

Best Practices for Debt Collection and Recovery

If you're looking for better strategies to recover debt while maintaining customer relationships, there are several ways you can streamline your processes. Here are six effective practices to consider:

1. Use Effective Communication Techniques

The key to successful debt collection is promoting open, positive communication. Be flexible and adaptable with the method and timing of communication.

Some people prefer calls outside of work hours, while others may respond better to emails or text messages. Personalize communication according to each customer’s preferences to enhance engagement and repayment rates.

2. Negotiate Directly With Decision Makers

Always negotiate with the person who has the authority to make decisions about payment. This could mean dealing directly with the customer or their lawyer, rather than with intermediaries.

3. Utilize Technology and Data Analytics

AI tools and automated systems can determine the best times and channels for communication, resulting in better outcomes than repeated, threatening calls. Data analytics can also help you assess risk and track accounts receivable, improving your debt recovery strategy.

4. Avoid Threats or Aggressive Tactics

Threatening customers is not only ineffective but also illegal under the Fair Debt Collection Practices Act (FDCPA). Emphasize the urgency of the situation while remaining respectful and understanding. Always confirm any agreements in writing for future reference.

5. Clearly Communicate Rights and Obligations

Ensure that customers understand their rights and obligations throughout the collection process. Explaining the importance of the debt and your company’s responsibilities makes the process transparent.

6. Partner With a Trusted Third-Party Agency

If in-house efforts fall short, consider partnering with a third-party agency. The Forest Hill Management is here to help you regain financial control.

We provide:

- Secure online payment platforms for easy debt management

- Personalized financial advisory services to guide you through recovery

- Flexible repayment options tailored to your needs

Take the first step toward financial freedom. Contact our financial advisors to create a custom plan today.

Conclusion

Debt recovery can feel overwhelming, but you don't have to tackle it alone. Understanding the debt collection and recovery process, you’re already taking the first step toward regaining control of your finances.

Remember, effective communication, flexible repayment options, and expert advice are essential tools in managing and overcoming debt. Partnering with the right resources, like The Forest Hill Management, you can find a path that works for you.

Stop wage garnishment, explore your repayment options now, and take charge of your financial future.

FAQs

1. What are the steps for debt recovery?

The debt recovery process typically begins with contact from the creditor, followed by negotiation of payment terms. If that doesn't work, the creditor may escalate the issue to a third-party agency or even take legal action.

2. What is the collection and recovery process?

Debt collection is when a creditor or agency tries to get you to pay what you owe. Debt recovery becomes necessary when the situation becomes more serious, involving third-party agencies or legal actions to recover the debt.

3. How likely is it that a debt collector will sue you?

It depends on the amount of debt and your communication with the collector. If you’re unresponsive or unable to pay, they may take legal action, but this is typically a last resort after other efforts have failed.

4. How can I avoid being sued by a debt collector?

The best way to avoid a lawsuit is by staying in touch with your creditor or debt collector. Open communication and working out a payment plan can go a long way in keeping things from escalating.

5. Can I negotiate my debt with a collector?

Yes, in most cases, debt collectors are open to negotiating. Setting up a payment plan or other options is worth having a conversation to find a solution that works for both parties.