Most Common FDCPA Violations by Debt Collectors

Need Help Reviewing Your Account?

Contact UsDebt collectors don’t just call; they can reshape how you feel about every dollar in your bank account. When threats, false claims, or nonstop calls happen, it may signal that legal boundaries are being crossed.

These actions are controlled by rules designed to protect you, but the line between pressure and abuse is often ignored. Knowing what those limits are gives you clarity and control over conversations that feel overwhelming.

Understanding these protections is a tool. When collectors misrepresent debts, contact your employer, or skip validation steps, you gain clarity on how to respond, document interactions, and understand your rights.

In this article, we explore common FDCPA violations by debt collectors, how they affect you, and steps to safeguard yourself while managing your financial obligations.

Key Takeaways

- Knowing your rights under the FDCPA helps you handle debt collectors with confidence and avoid unnecessary stress.

- Keep detailed records of every interaction to defend against violations and ensure your case is clear.

- Always ask for written proof of debt to verify its legitimacy before making any payments.

- Debt collectors can’t contact family, friends, or employers without your consent—enforce your privacy.

- Partnering with a compliant agency like Forest Hill ensures respectful, transparent communication and fair resolution.

What the Fair Debt Collection Practices Act Protects

The Fair Debt Collection Practices Act exists because debt collection, left unregulated, became a source of genuine harm. Passed in 1977, it established federal standards for how third-party collectors can interact with you when pursuing unpaid accounts.

The law applies specifically to companies that collect debts on behalf of others, not the original creditor you owed money to. If a medical bill, credit card balance, or personal loan gets transferred to a collection agency, that agency must follow FDCPA rules.

The protections cover specific behaviors: when and how often collectors can contact you, what they're allowed to say, who else they can speak with, and how they must handle disputes. Each rule targets a practice that was causing measurable distress before regulation existed.

Common FDCPA Violations and How to Spot Them

From excessive calls to falsely inflating debts, these violations exploit fear and misinformation to pressure consumers into paying. Here's how to spot these red flags and protect yourself from illegal debt collection practices.

Harassment and Abusive Contact

Federal law sets clear guidelines on what constitutes harassment, and unfortunately, many collectors often cross that line. Here's how you can recognize when the actions go too far:

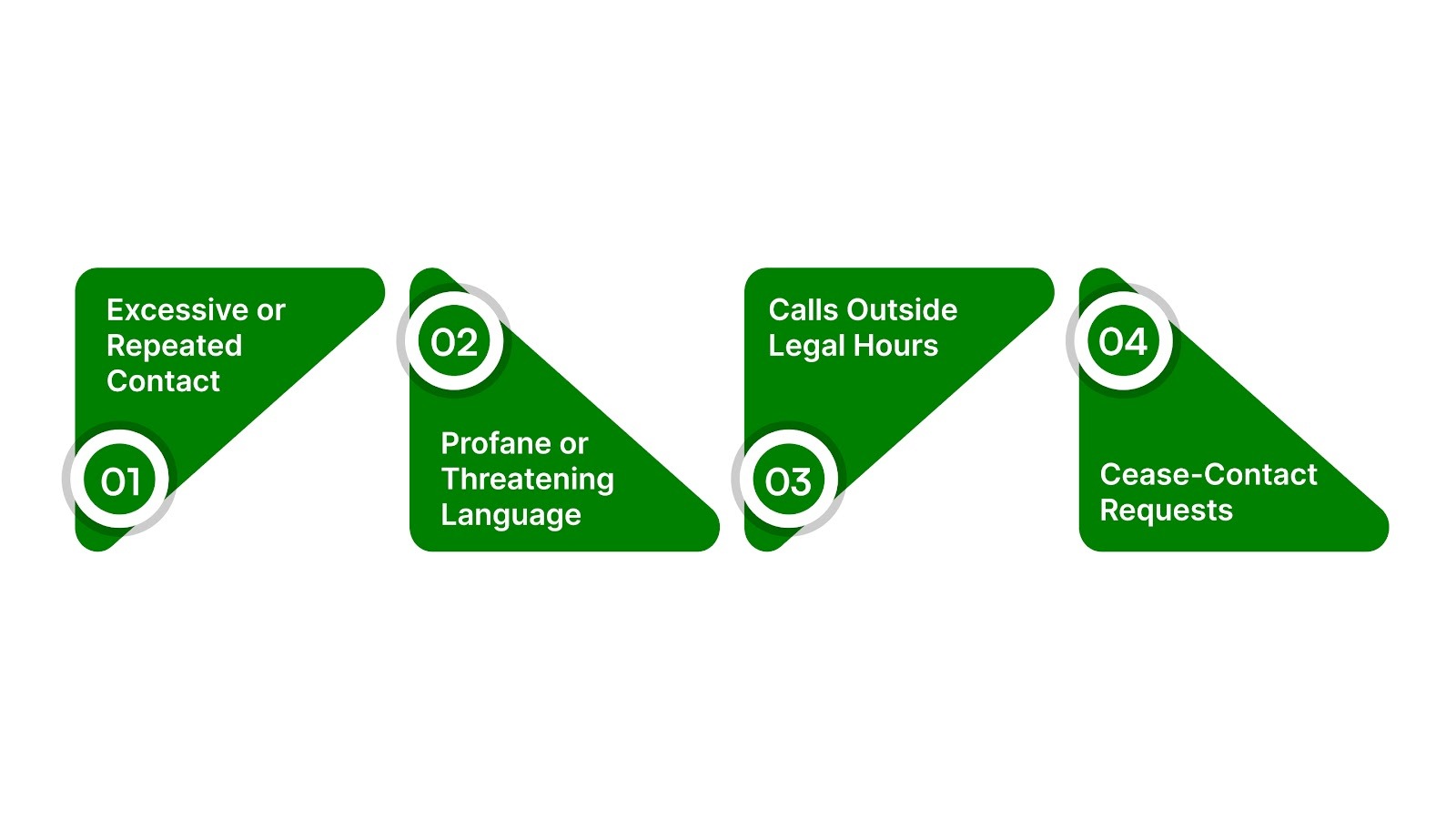

- Excessive or Repeated Contact: Persistent calls with no new information or frequent calls in a short period may be considered illegal under the FDCPA. These attempts to wear you down are meant to annoy, not communicate.

- Profane or Threatening Language: Any use of obscene, insulting, or threatening language during an interaction violates the FDCPA. No matter the circumstances, collectors have no right to yell, insult, or belittle you.

- Calls Outside Legal Hours: Calls before 8 AM or after 9 PM in your time zone are prohibited unless you’ve explicitly agreed to it. These early or late calls are often made to catch you off guard.

- Written Notice to Cease Contact: Once you send a written request for no more contact, they must stop. They can inform you of any specific actions they intend to take, but further calls or letters are illegal.

The pattern across all these violations is the same: contact that prioritizes intimidation over communication.

Also Read: Understanding the Fair Debt Collection Practices Act

Misrepresenting the Debt or Consequences

Debt collectors often use deceptive tactics to manipulate or pressure you into paying, and these tactics are illegal. Here's how you can spot such violations:

- False Claims About Identity: Collectors sometimes pretend to be attorneys, law enforcement, or government officials to instill fear and pressure you into paying. Always verify their identity if they claim to be from a legal office or sheriff's department. In many cases, these claims are inaccurate and meant to pressure payment.

- Inflating the Debt Amount: The amount a collector quotes may include illegitimate fees, penalties, or interest that aren't part of your original agreement. If they try to push you into accepting inflated figures, it's a tactic to get you to pay without questioning.

- Threatening Arrest or Property Seizure: Collectors cannot threaten to arrest you, seize property, or garnish wages unless they have legal authority to do so. Most debts are civil matters, not criminal, so arrest threats are illegal.

- Misleading Legal Action Threats: Threatening a lawsuit or court action that they're not actually planning to follow through with is also prohibited. If they claim a lawsuit is imminent, that statement must be true; using such threats without any intention to pursue them violates the FDCPA.

The common thread here: collectors weaponizing fear through false information to bypass your right to verify and dispute.

Failing to Provide Proper Debt Validation

Debt validation is not just a courtesy; it's your legal right to protect you from paying debts you might not owe. Here's what you need to know:

- Written Notice Within Five Days: Collectors must send you written notice within five days of their first contact. This should include the creditor's name, the amount owed, and your right to dispute the debt. If this notice is missing or arrives late, they’ve violated the law.

- Right to Request Validation: If you request proof that the debt is yours, that the amount is accurate, and that the collector has the right to pursue it, they must provide that information. Refusing to verify or ignoring your request is illegal, and they can't continue collection efforts until they do.

- 30-Day Validation Period: After receiving the initial notice, you have to pause to review the debt details, dispute inaccuracies, or request verification without the threat of further collection actions. If they continue calling, sending letters, or making threats during this period, they are breaking the law.

This rule exists because identity theft, billing errors, and mistaken transfers happen constantly. Validation protects you from paying someone else's debt or an amount that was never accurate.

Contacting Third Parties About Your Debt

Your debt is private, and collectors are not allowed to spread it around. The law is clear in protecting your privacy:

- No Discussion with Family or Friends: Collectors cannot share your debt details with family members, friends, neighbors, or coworkers. They are only allowed to contact third parties to find your location, and they can’t mention the debt in the process.

- Restrictions on Contacting Your Employer: Calling your employer is highly restricted. While they can verify your workplace, they cannot disclose your debt or discuss any account details with your supervisor, HR, or anyone else at your job.

Some collectors still ignore these rules, either out of negligence or as a deliberate pressure tactic. They know embarrassment and social consequences can push people to pay faster, even if it means breaking the law.

Also Read: Debt Collector Phone Call: When to Answer and What to Ask

These aren't the only violations collectors may commit. Let's explore a few more common FDCPA breaches to watch for.

Other Common FDCPA Violations

In addition to the most common violations, there are other specific practices regularly reported by consumers that also breach federal law. These include actions that disrupt your finances or involve illegal threats.

Here are a few more FDCPA violations to watch out for:

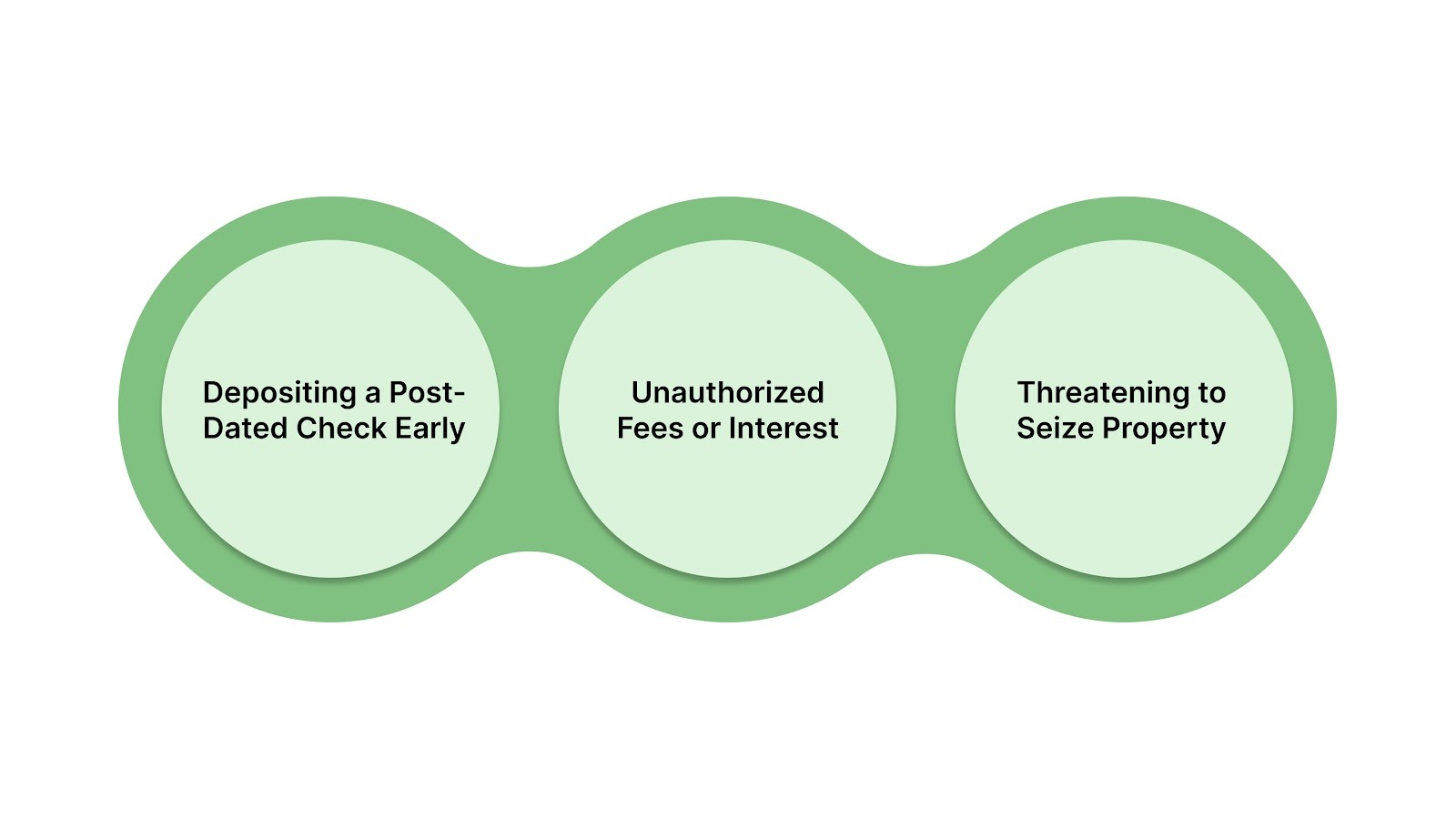

- Depositing a Post-Dated Check Early: Cashing a check before its intended date violates both FDCPA rules and standard banking practices.

- Unauthorized Fees or Interest: Collectors sometimes add "processing fees" or inflated interest rates that aren’t authorized by your original agreement or state law.

- Threatening to Seize Property: Collectors cannot threaten to take your property (like your car or home) without a court judgment. If they do, they’re lying.

In addition to these specific violations, it's important to know how to respond if you suspect your rights under the FDCPA have been violated

What to Do If You Suspect an FDCPA Violation

Trust your instincts if something feels off during a collection call. Violations leave a trail, so start by documenting everything. Record the date, time, collector's name, company, and exact quotes, especially if threats or abuse occurred. Written records hold up better than memory.

File a complaint with the Consumer Financial Protection Bureau (CFPB), which tracks violations and can take action against repeat offenders. If the violations are severe or ongoing, you may consider seeking professional guidance if violations are ongoing or severe. Many work on contingency, meaning they only get paid if you win.

To protect yourself:

- Keep a folder (physical or digital) for all debt-related documents

- Keep notes of calls and save voicemails or written messages when possible

- Never give bank info until the debt is verified in writing

- Send dispute or cease-contact letters via certified mail

- Save screenshots of texts and voicemails with threats or false claims

Also Read: Can a Debt Collector Take My Car? Understanding Your Rights

While knowing how to protect yourself is essential, it’s also important to work with a collection agency that prioritizes your rights and adheres to FDCPA regulations.

How Forest Hill Management Ensures FDCPA Compliance

At Forest Hill Management, we don’t just meet the minimum requirements of the Fair Debt Collection Practices Act (FDCPA). We operate within FDCPA guidelines to ensure respectful, transparent, and compliant communication.

Here’s what that looks like in practice:

- Respectful contact hours: Contact occurs within legally permitted hours in accordance with federal guidelines.

- Clear, accurate information: You’ll receive written validation of your debt with all the necessary details, ensuring transparency and trust.

- Privacy first: We never discuss your account with anyone but you, ensuring your personal information stays secure.

- Respectful communication: We communicate professionally and respectfully, focused on helping you resolve your financial situation without pressure or intimidation.

- Complete transparency: Every step we take complies with federal regulations, designed to protect your rights, not maximize collections.

We’re committed to compliant account management and clear communication throughout the process. Ready to take the next step? Make a payment online today or call us at (888) 471-0109 for support.

Conclusion

The FDCPA provides essential protections, but knowing how to spot violations and defend your rights gives you the confidence to handle debt collectors effectively. While the law sets boundaries, understanding how to manage these situations is key to avoiding unnecessary stress and confusion.

When you're ready to take control, Forest Hill Management offers a clear, compliant, and supportive path to resolution, without the added pressure. We’re here to provide clear, compliant support as you manage your account.

Make a payment online today or contact our support team to learn more about your options.

FAQs

1. Can a debt collector be held liable for internal employee misconduct?

If an employee or agent violates the FDCPA, even without direct management approval, the company itself can be held responsible. Liability extends to improper training, oversight failures, or allowing illegal practices to persist.

2. Are oral agreements with a collector legally binding under the FDCPA?

Potentially, but only if supported by documented consent. The FDCPA emphasizes written records; oral agreements can be difficult to verify without written confirmation.

3. Does FDCPA protection extend to digital communications like email or text?

Yes. The FDCPA covers electronic communication if it relates to debt collection. Threatening, misleading, or harassing emails and texts are considered violations just like phone calls or letters.

4. Can a collector pursue debt from a deceased person’s estate?

Yes, but only through the estate, not the family personally, unless they co-signed. Misrepresenting authority over family members or pressuring heirs violates the FDCPA and can trigger liability.

5. Are there record-keeping requirements for collectors under the FDCPA?

While the FDCPA doesn’t mandate exact formats, collectors must maintain accurate documentation of contacts, notices, and disputes. Poor records can undermine a collector’s legal position and strengthen a consumer’s claims.